Carvana Is Worth Zero

$55 billion in market cap built on a business that made $16 million selling cars last quarter, while one family extracted $5.8 billion.

cc: FT Alphaville, Temple 8 Research, Legal Special Situations, Indra, LongYield

On the evening of February 18, 2026, Carvana reported the most impressive quarter in its history. Record revenue. Record units. Headline EPS of $4.22 against a consensus of $1.13. A nearly fourfold beat.

Within hours, $10 billion in market capitalisation had evaporated.

The stock cratered over 20% in after-hours trading, briefly touching $300 before settling near $304. By the following pre-market session, shares were indicated down a further 10%, with multiple analysts slashing targets before the opening bell. Combined with the Gotham City Research short report three weeks earlier, CVNA has now shed 42% from its January high of $486.89.

Something does not add up. Either the market misread the best quarter in company history, or the market finally read the quarter correctly.

We believe it is the latter.

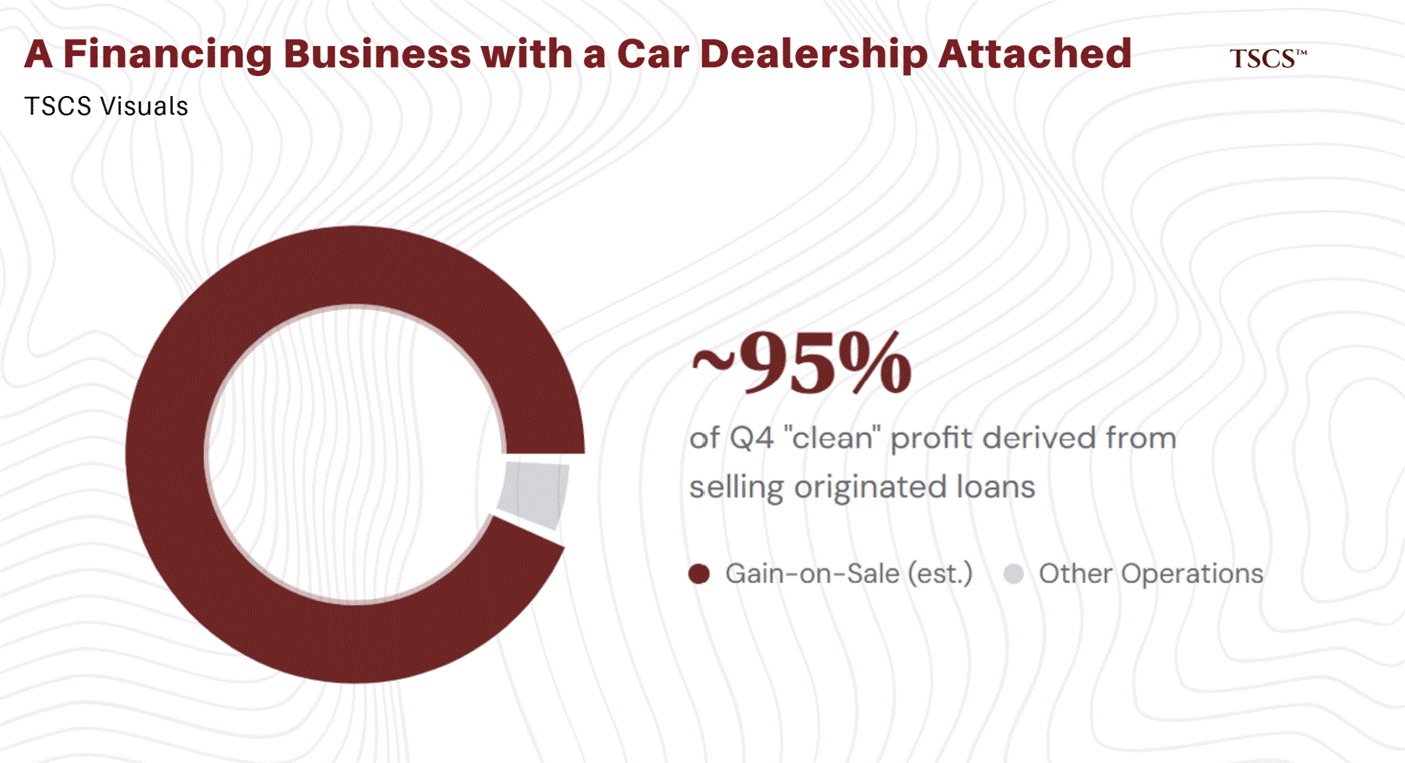

Strip away a one-time $685 million non-cash tax benefit, and the earnings story inverts. Strip away gain-on-sale income from lending, and it nearly disappears. What remains is a company that generated roughly $16 million in operating profit from actually selling cars, valued by the market at $55 billion.

That is not a typo. Sixteen million dollars.

The CFO sold shares at $410 sixteen days before this report. The father of the CEO has extracted $5.8 billion since the IPO, nearly four times the company’s total cumulative net income, while his private entity burned $1 billion in cash. Not a single insider has purchased a share in over a year. And the SEC has an open investigation with subpoena power into the very loan origination practices that produce the overwhelming majority of Carvana’s “profits.”

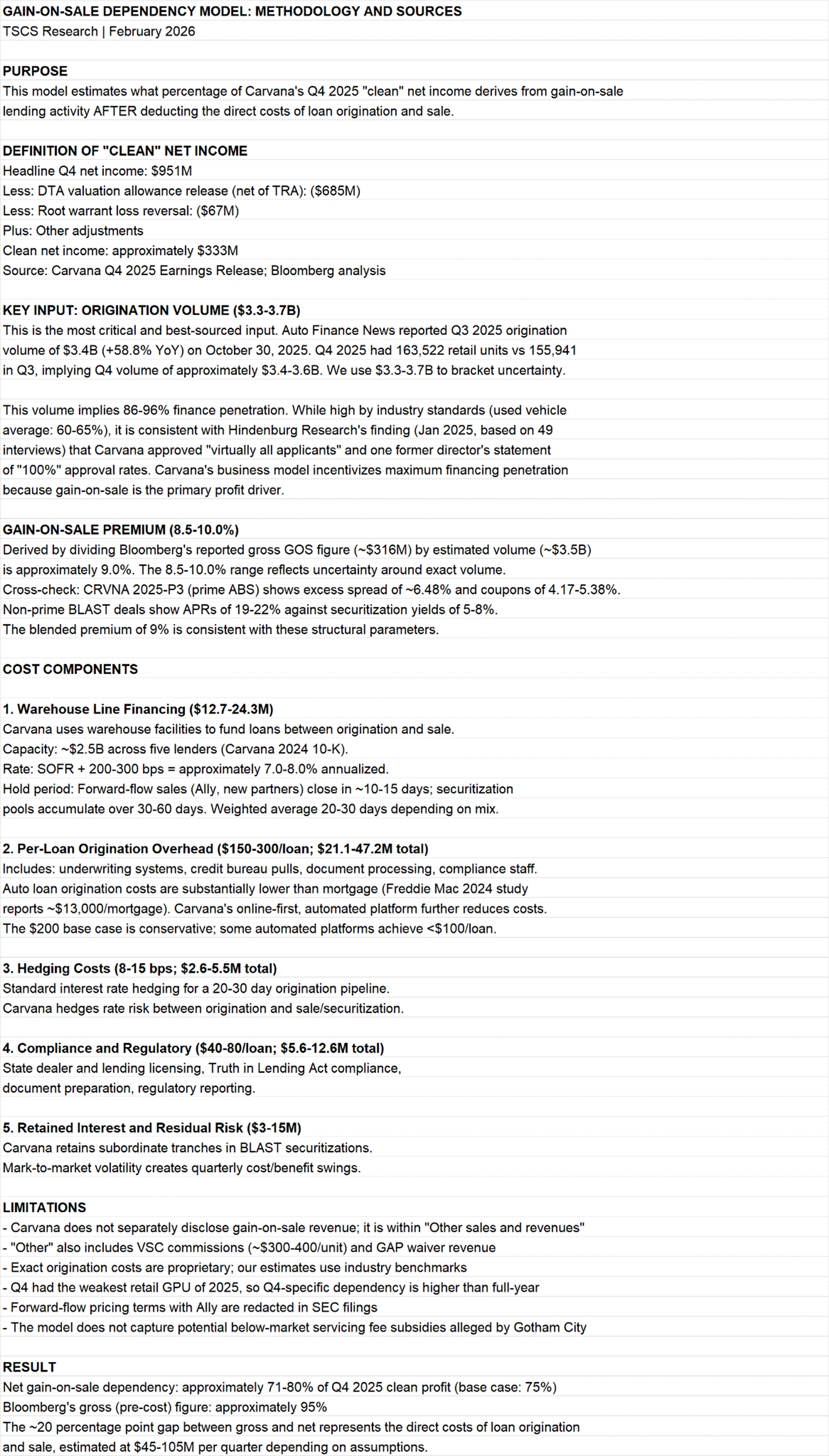

We built our own bottom-up Gain-on-Sale Dependency Model for this report, using publicly verifiable inputs (origination volumes, warehouse line costs, hedging estimates, compliance overhead, and retained interest assumptions) to calculate the net contribution of loan sales to quarterly earnings.

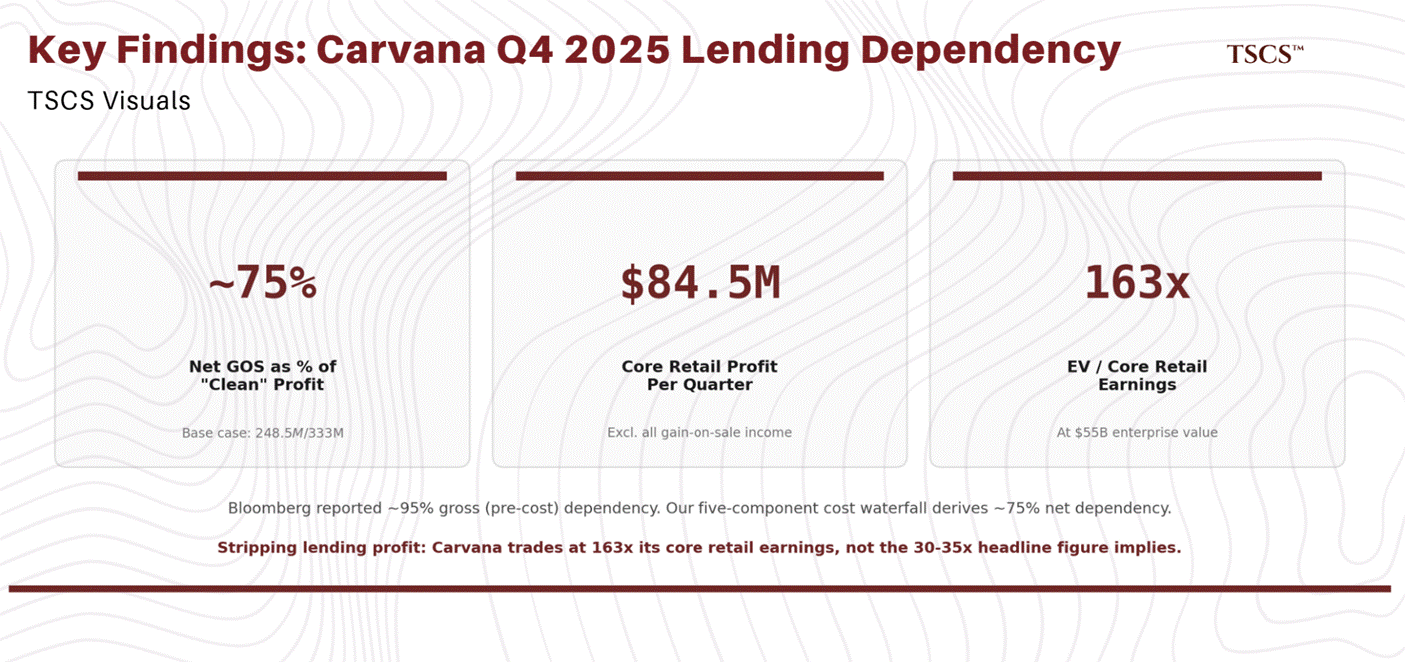

Bloomberg reported that 95% of Q4 clean profit came from gain-on-sale. Our proprietary model, which accounts for direct origination costs that Bloomberg’s gross figure does not deduct, estimates the true net dependency at 70 to 80%, with a base case of 75%. The full methodology, sourced assumptions, and sensitivity tables are included below. Either way, the conclusion is the same: this is a financing business with a car dealership attached, not the other way around.

What this report covers

This is a forensic breakdown across five critical dimensions:

Earnings quality and the gain-on-sale illusion. Why EBITDA missed by 5 to 6%, GPU hit its lowest level of 2025, and margins are compressing during explosive growth.

The Garcia family ecosystem. $5.8 billion extracted, $1 billion burned at DriveTime, below-market servicing fees at Bridgecrest, undisclosed VIN overlaps, and an SEC subpoena.

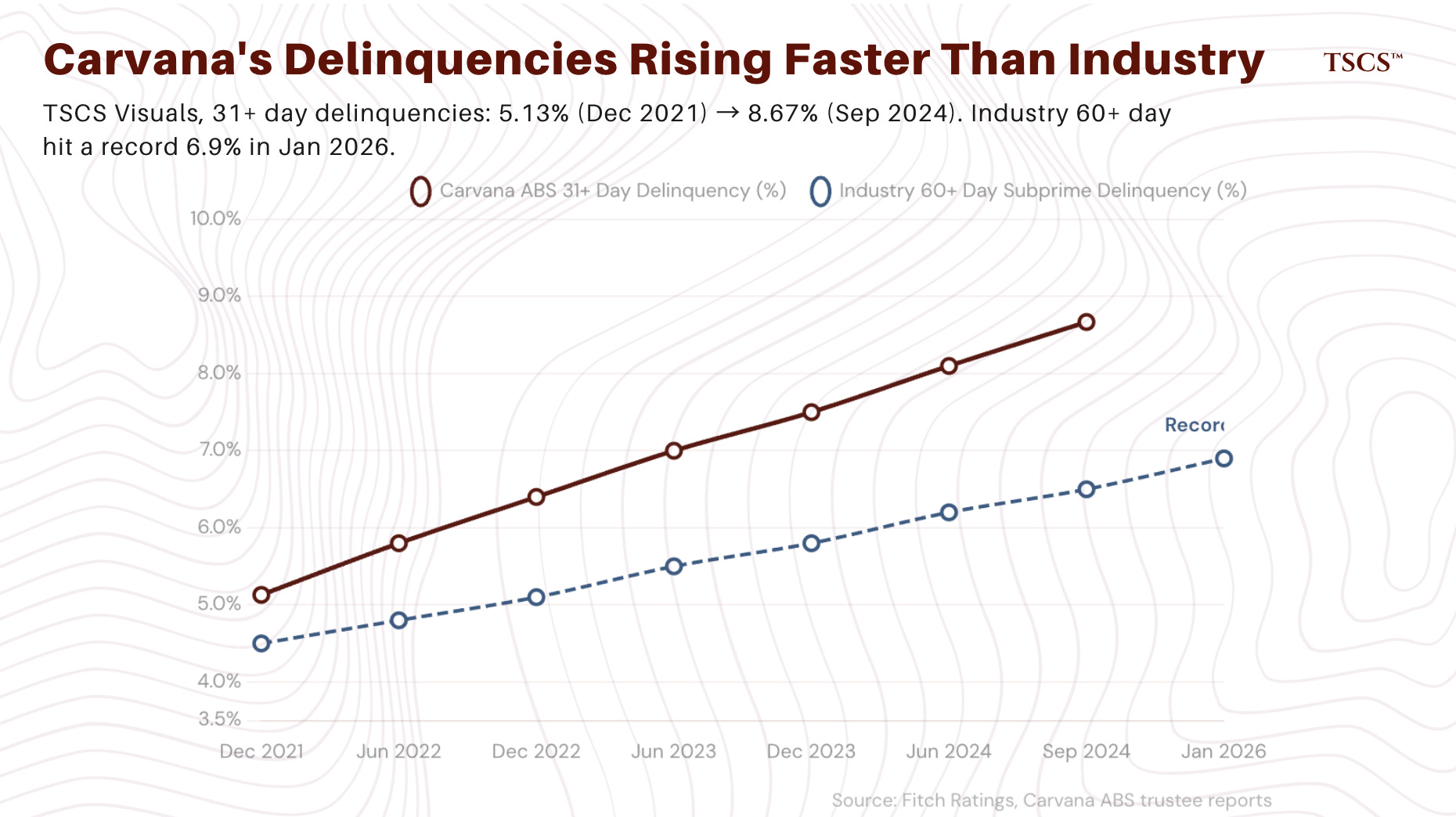

Credit cycle risk. Record 6.9% subprime delinquencies, Carvana prime borrower defaults running at 4x industry averages, and the Ally Financial renewal cliff in October 2026.

The honest bull case. Why the longs are not wrong about operational scaling, and why they are wrong that it matters at this valuation.

What the price requires you to believe. A concrete valuation framework, from the bear case ($120 to $160) through the bull case ($550 to $650), and what assumptions each requires.

Why this matters beyond Carvana

This is not just a story about one overvalued car company. It is a case study in how gain-on-sale accounting, related-party opacity, and dual-class governance structures can sustain a valuation disconnected from economic reality for years, right up until the moment they cannot.

If you care about earnings quality, credit cycles, or corporate governance, this report is for you.

This post is free.

Our paid research covers the ideas that Wall Street either ignores or gets wrong. This week alone we published on Korean governance arbitrage trading at negative enterprise value, why the hedged Treasury return just turned negative for Japanese investors for the first time in 30 years, and the semiconductor equipment monopoly nobody wants to talk about. If the depth of this Carvana analysis is useful to you, the rest of the publication operates at the same level, across equities, macro, and commodities globally.

5,000 investors read us. Here is why

Disclaimer: This report represents our opinion and analysis based on publicly available information. We may hold positions in securities discussed. This is not investment advice. See full disclaimer at the end of this report.

Let’s get into it.

The headline beat masks an EBITDA miss and GPU collapse

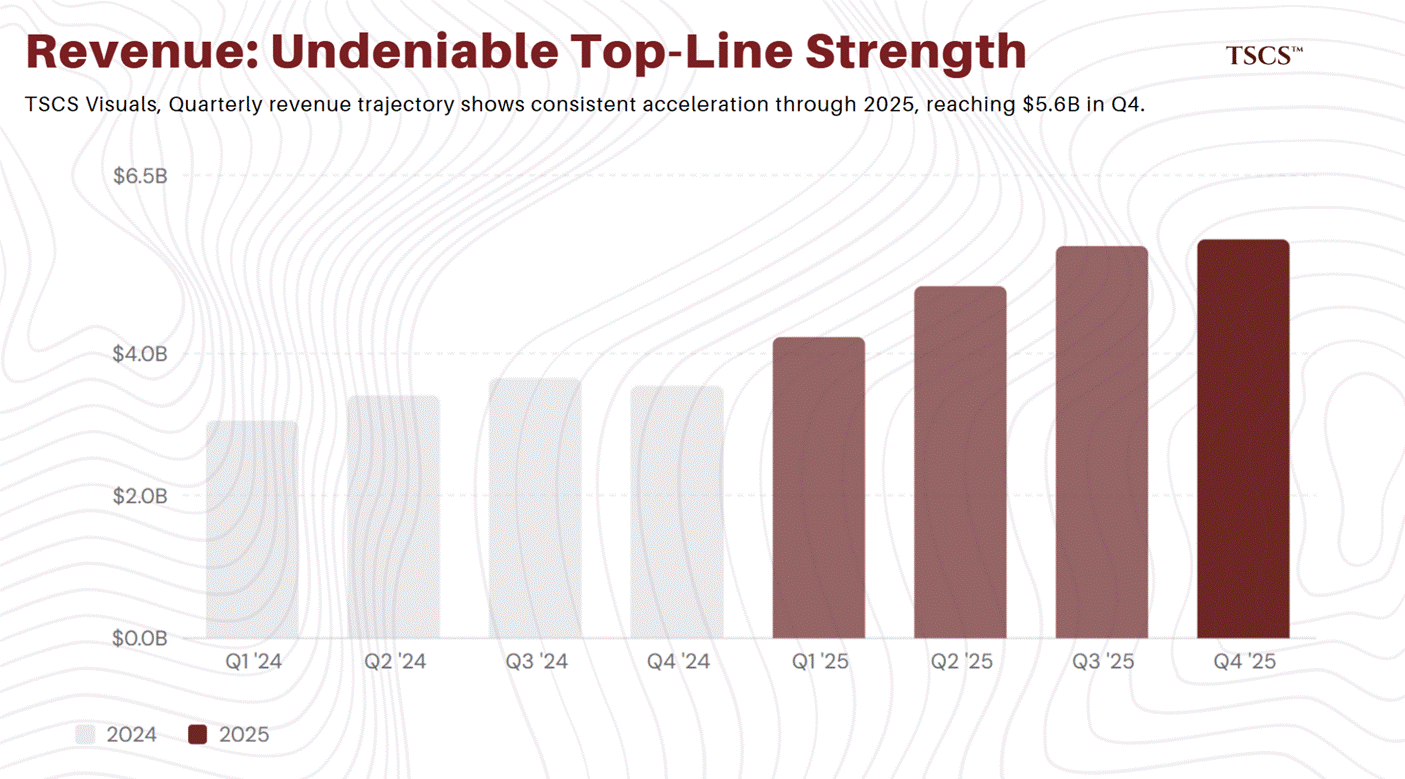

Carvana’s Q4 2025 top-line performance was undeniably strong. Revenue of $5.603 billion beat the $5.27 billion consensus by 6.8%, growing 58% year-over-year. Retail units sold reached 163,522, beating estimates of ~157,226 and growing 43% YoY. Full-year 2025 revenue hit $20.3 billion (+49% YoY), with 596,641 retail units sold.

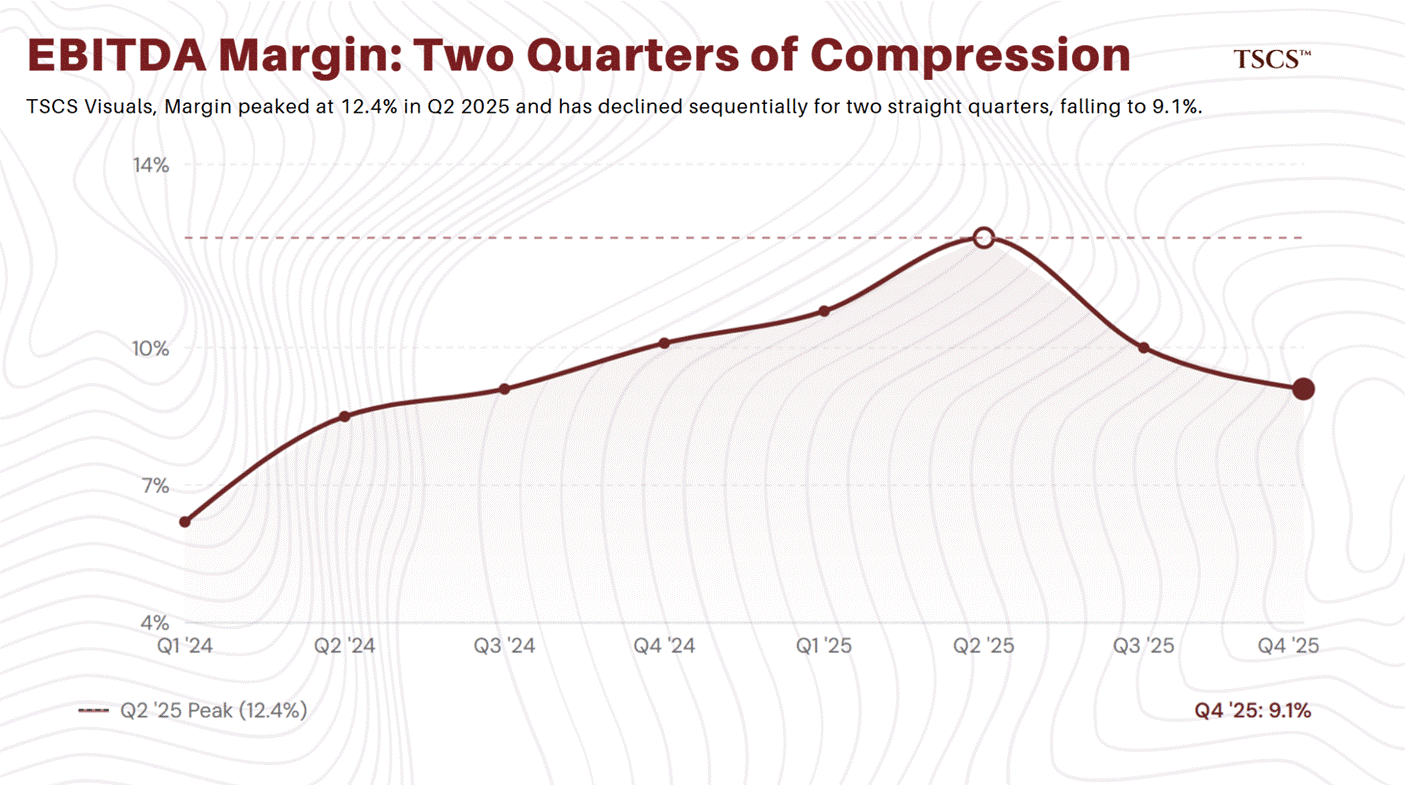

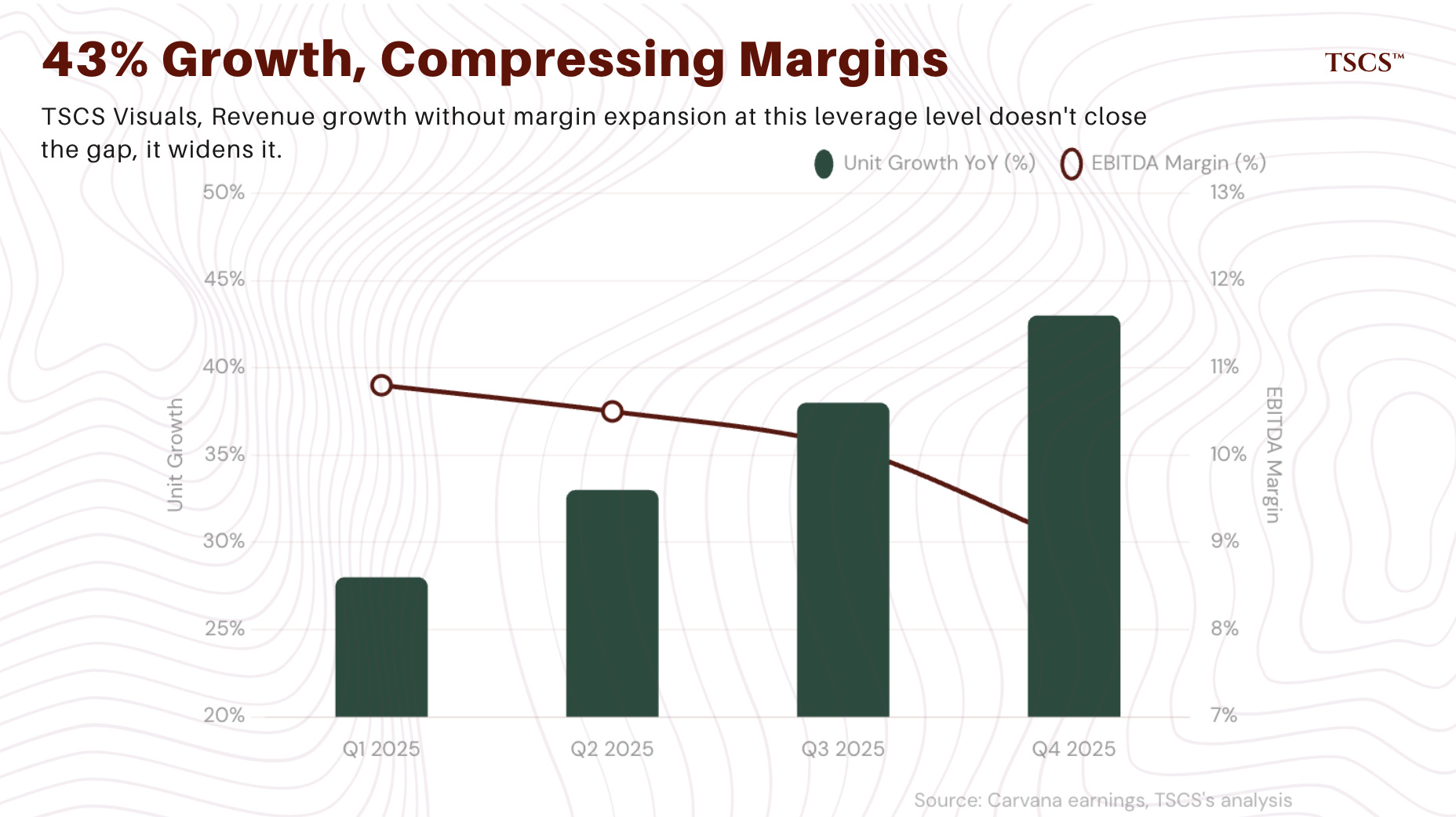

But the metrics that actually determine whether this business can service $4.8 billion in debt told a different story. Adjusted EBITDA of $511 million missed consensus of $536–$539 million by approximately $25-28 million, a 5-6% miss. More troublingly, EBITDA margin fell to 9.1%, down from 10.1% in Q4 2024 and 12.4% at its Q2 2025 peak. This marks two consecutive quarters of margin compression despite explosive revenue growth, the operational leverage that bulls relied upon is running in reverse.

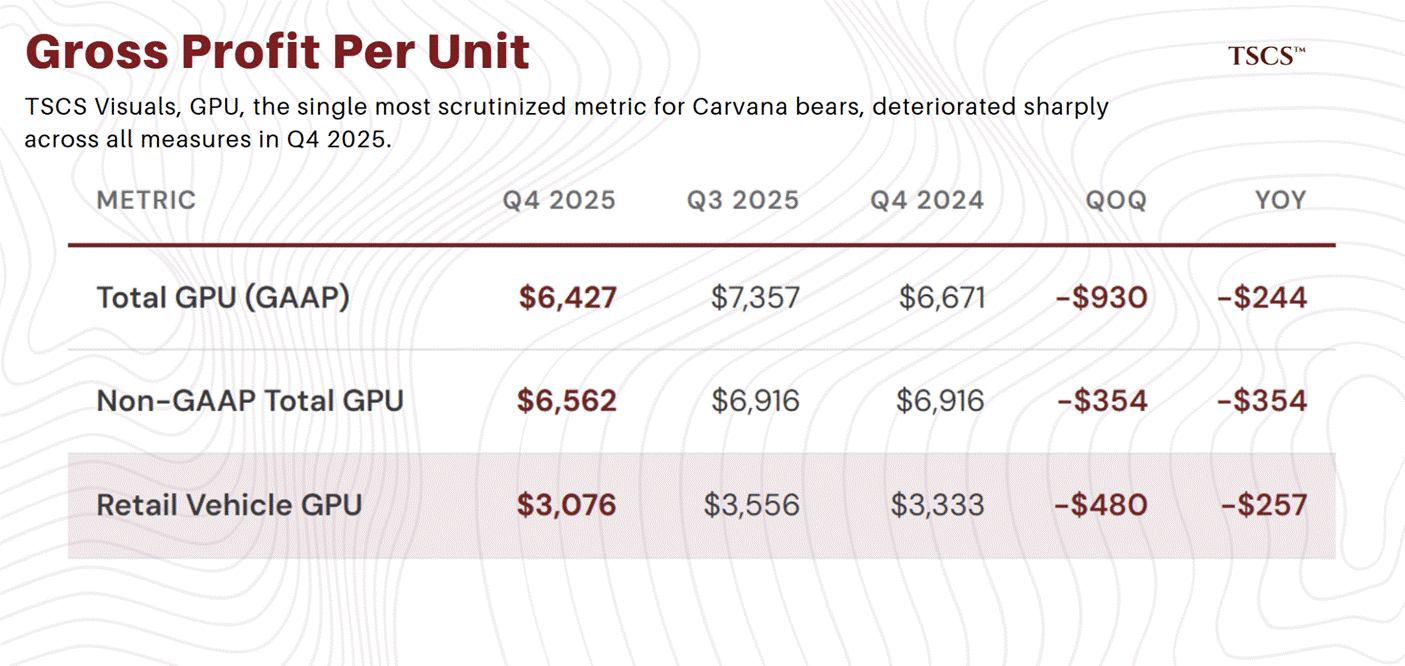

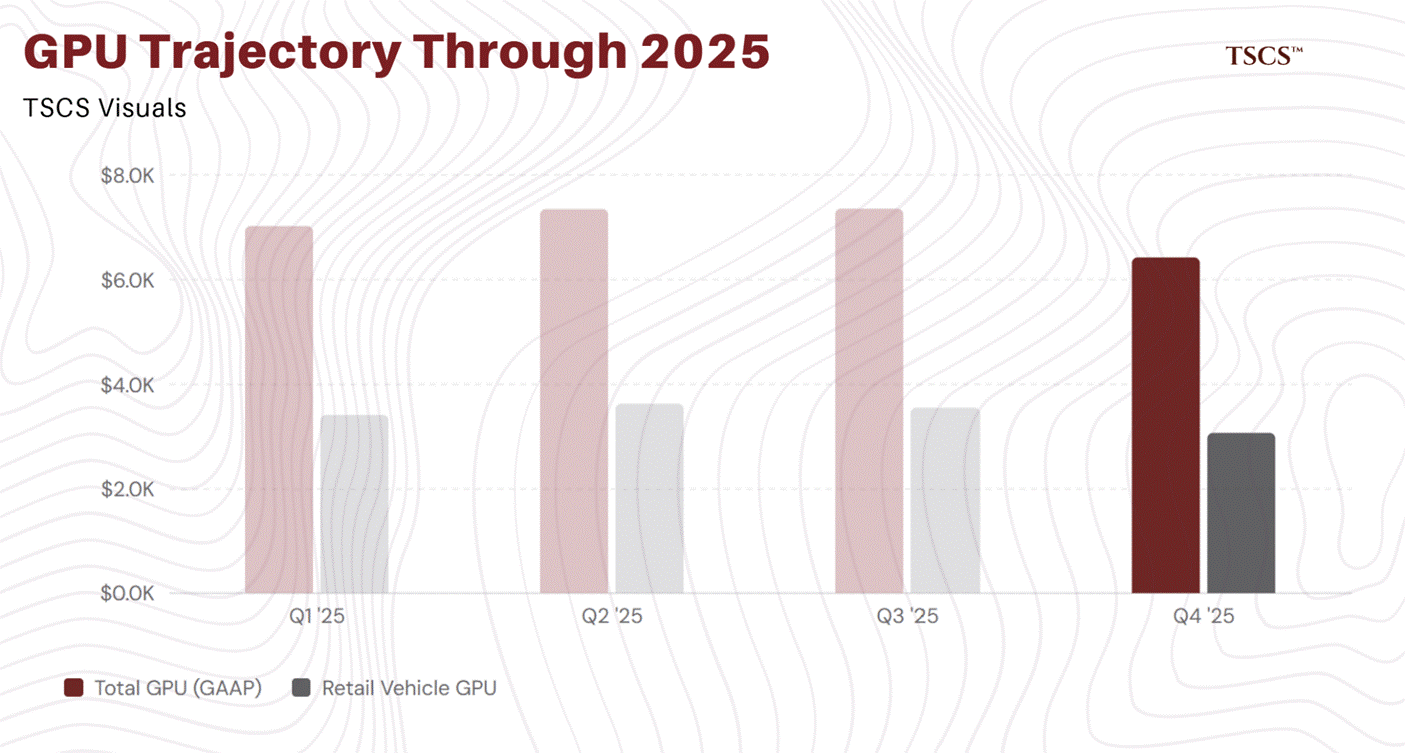

Gross profit per unit, the single most scrutinized metric for Carvana bears, deteriorated sharply:

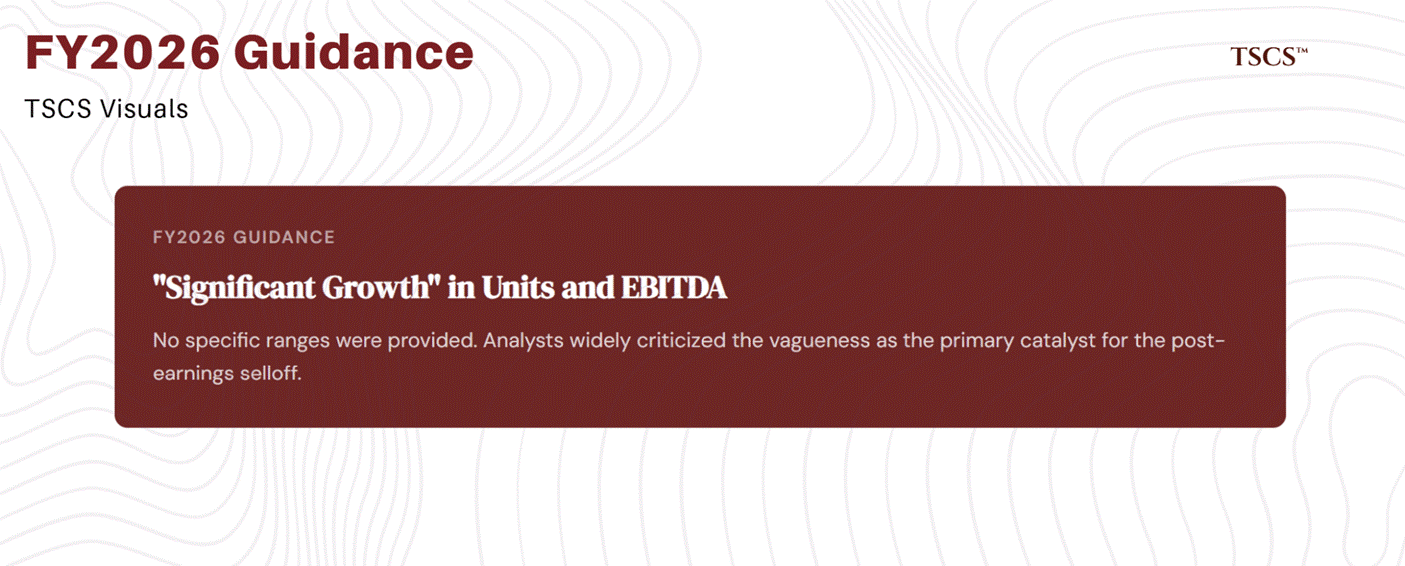

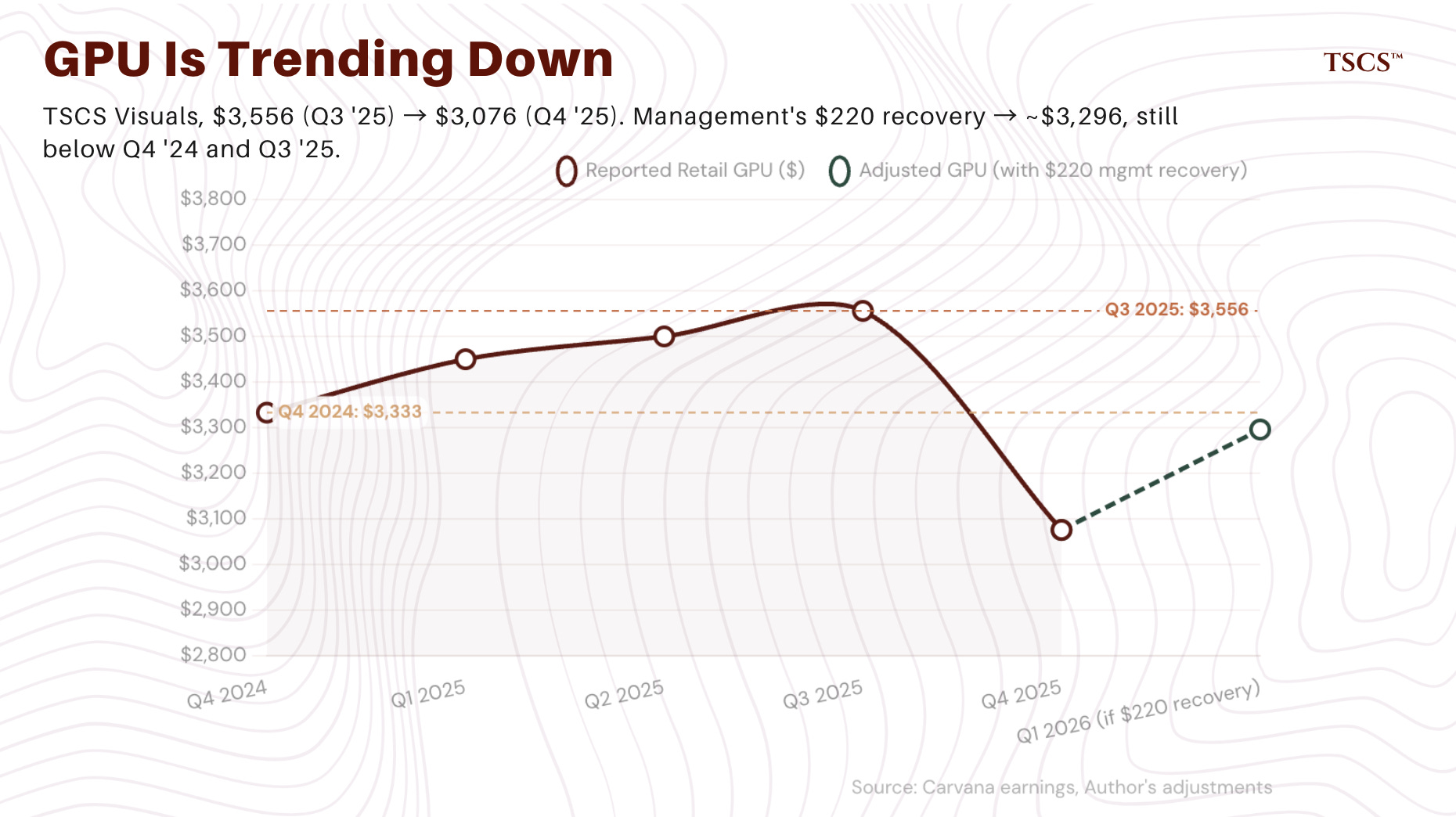

Retail GPU of $3,076 was the lowest of all four quarters in 2025. Management attributed the decline to three factors: lower shipping fees passed to customers, higher reconditioning costs (particularly at newly integrated ADESA locations with the youngest management teams), and higher industry-wide depreciation rates. CEO Garcia III acknowledged reconditioning issues would persist into Q1 2026, estimating that if all locations matched top-quartile per-unit costs, reconditioning would be ~$220 lower per unit. The guidance for FY2026 was conspicuously vague, just “significant growth” in units and EBITDA, with no specific ranges, which analysts widely criticized as the primary catalyst for the selloff.

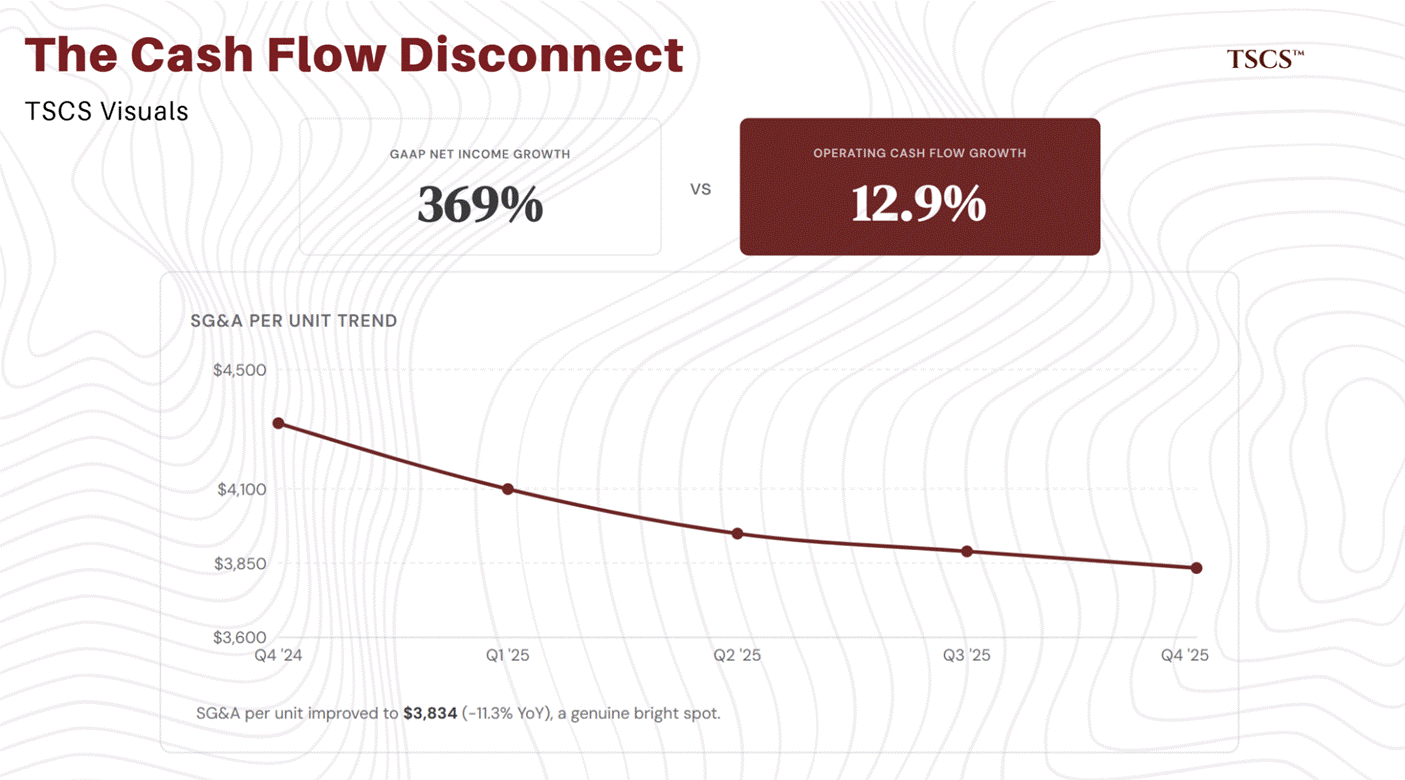

SG&A totaled $627 million (+26.9% YoY), though SG&A per unit improved to $3,834 (-11.3% YoY). Full-year operating cash flow of approximately $1.036 billion grew just 12.9%. GAAP net income grew 369%. When earnings grow 29 times faster than cash flow, the earnings are not real in any economically meaningful sense.

Bulls will argue, as they did with our previous analysis, that operating cash flow growth was suppressed by an approximately $800 million inventory build (from $1.6 billion to $2.4 billion) driven by ADESA integration and unit growth, and by increased cash interest payments as PIK expired, and that adjusting for these “investment” items reveals healthy underlying cash generation. The argument is not wrong on the mechanics, but it is wrong on the implications.

First, the inventory build is not purely discretionary investment. In a gain-on-sale model, Carvana needs to acquire and sell ever-more vehicles to maintain the loan origination pipeline that generates the vast majority of its clean profit. Inventory builds in this context are not analogous to a retailer stocking shelves ahead of demand; they are the necessary input cost of maintaining the financing engine.

Second, the cash interest transition itself illustrates the earnings quality problem: the PIK period artificially depressed cash interest expense by roughly $450 million annually, making both reported profitability and operating cash flow look stronger than the steady-state economics warrant. We are now entering that steady state, and the gap between GAAP earnings growth (369%) and cash flow growth (12.9%) is not a temporary distortion. It is the distortion resolving itself.

The $685 million accounting mirage and gain-on-sale dependency

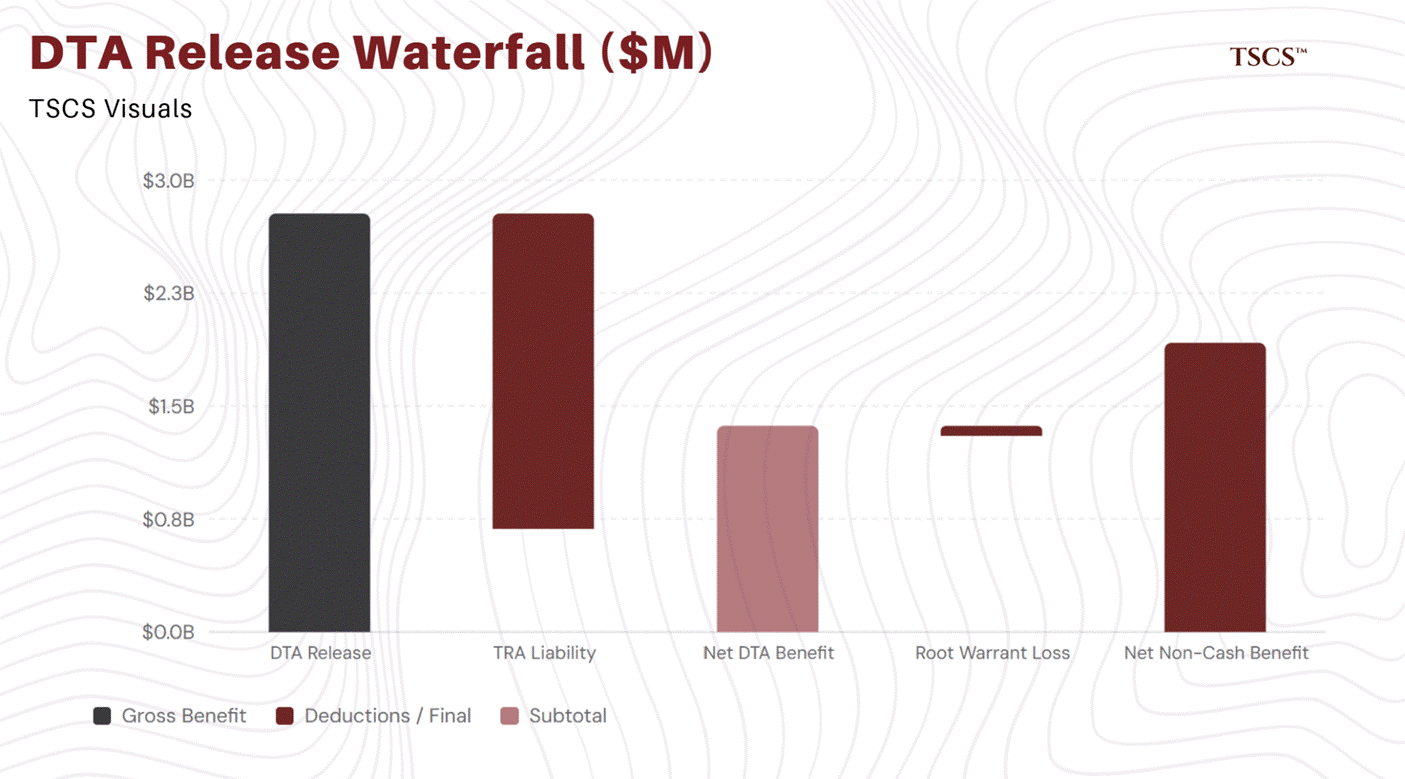

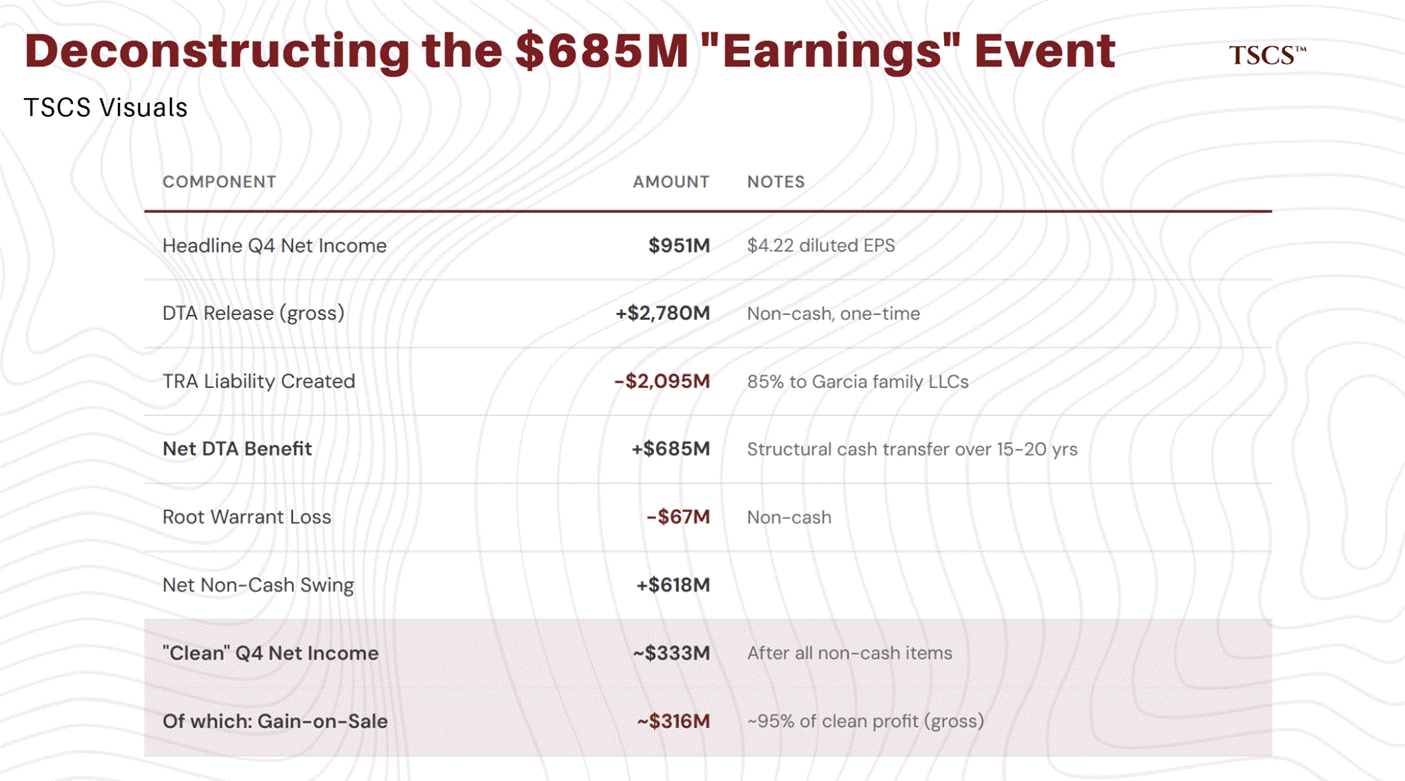

The headline Q4 net income of $951 million ($4.22 diluted EPS versus consensus of $1.13) was overwhelmingly driven by a one-time, non-cash event. In Q4, Carvana released the valuation allowance against its deferred tax assets, generating a gross income tax benefit of $2.78 billion. Because of Carvana’s Up-C corporate structure, 85% of tax savings must be shared with LLC unit holders via a Tax Receivable Agreement (TRA), creating a simultaneous $2.095 billion TRA liability. The net impact: a $685 million positive swing to net income. After subtracting a $67 million loss on Root Inc. warrants, the net non-cash benefit was $618 million.

Critically, the TRA liability is not merely an accounting offset. It represents a contractual obligation to pay 85% of realized tax savings to Garcia family-controlled LLC unit holders over the next 15 to 20 years. As Carvana utilizes its deferred tax assets against future taxable income, it will owe cash payments to the Garcia entities, estimated at $100 to $200 million annually at current profitability levels. This creates a structural cash transfer from the public company to the controlling family that persists regardless of whether the underlying tax benefit was legitimately recognized.

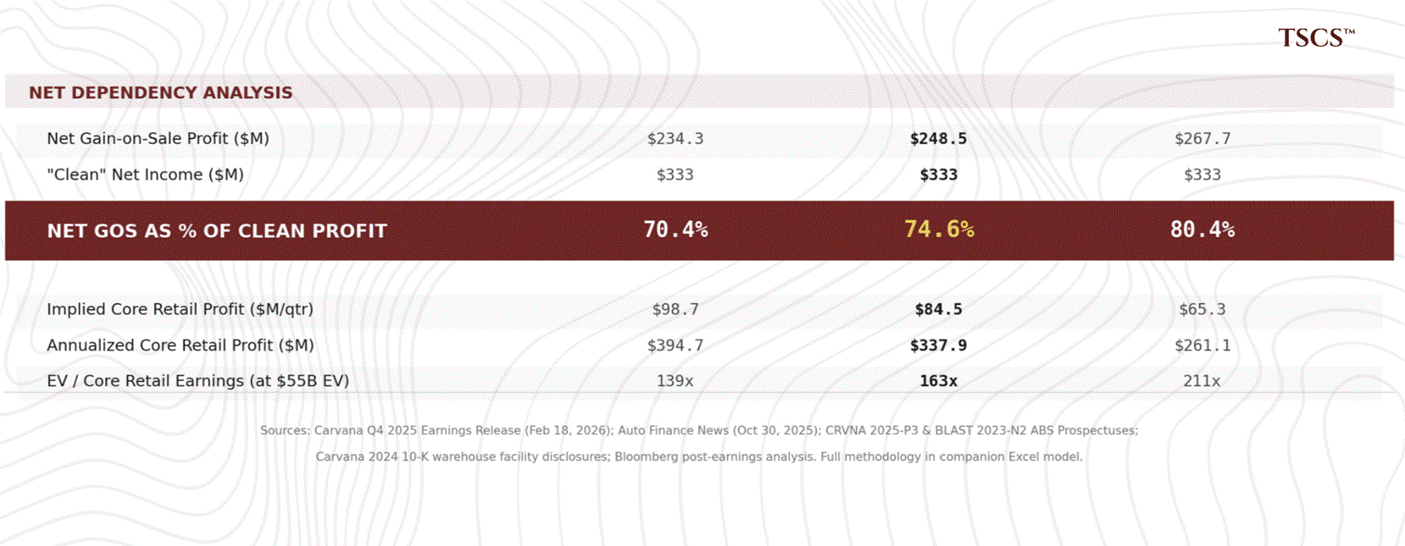

Stripping out all non-cash items, Q4 net income was approximately $333 million. GAAP operating income, which excludes the tax benefit, was $424 million on a 7.6% margin, essentially flat from the 7.3% operating margin in Q4 2024 despite 58% revenue growth. Put differently: Carvana grew revenue by $2.1 billion year-over-year and its operating margin improved by 0.3 percentage points. Growth at this rate is not generating leverage. It is dilutive.

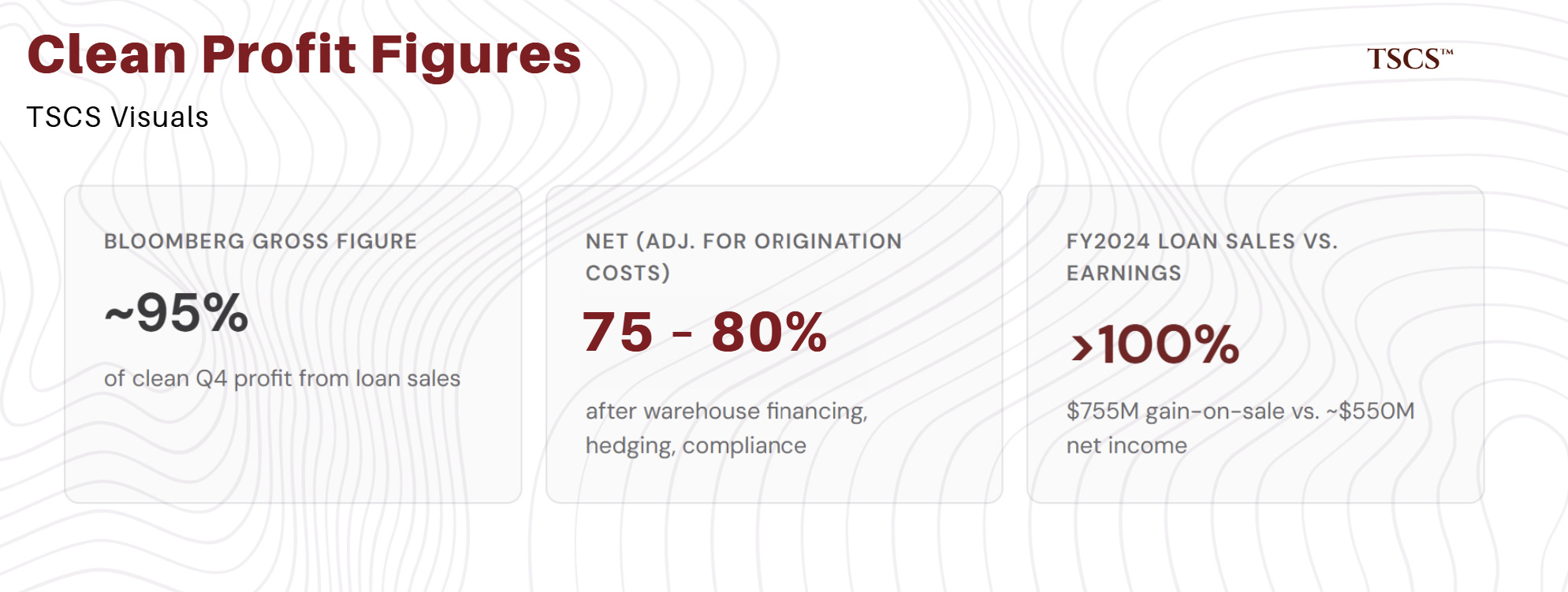

The even more troubling finding from Bloomberg’s post-earnings analysis: loan sales accounted for approximately 95% of the $333 million in Q4 “clean” profit, meaning roughly $316 million of the quarter’s adjusted earnings derived from selling originated loans rather than from selling cars.

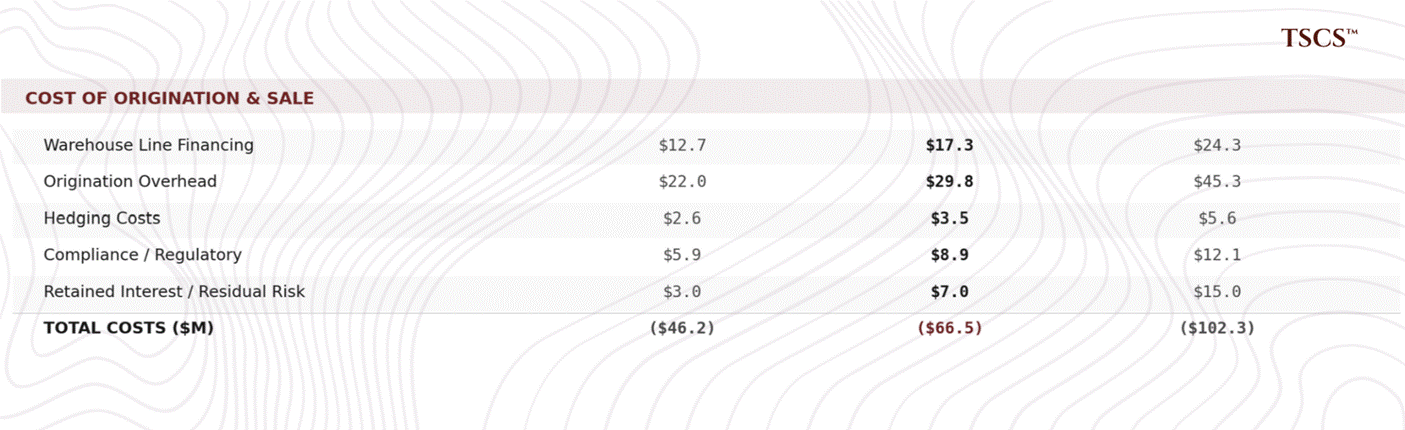

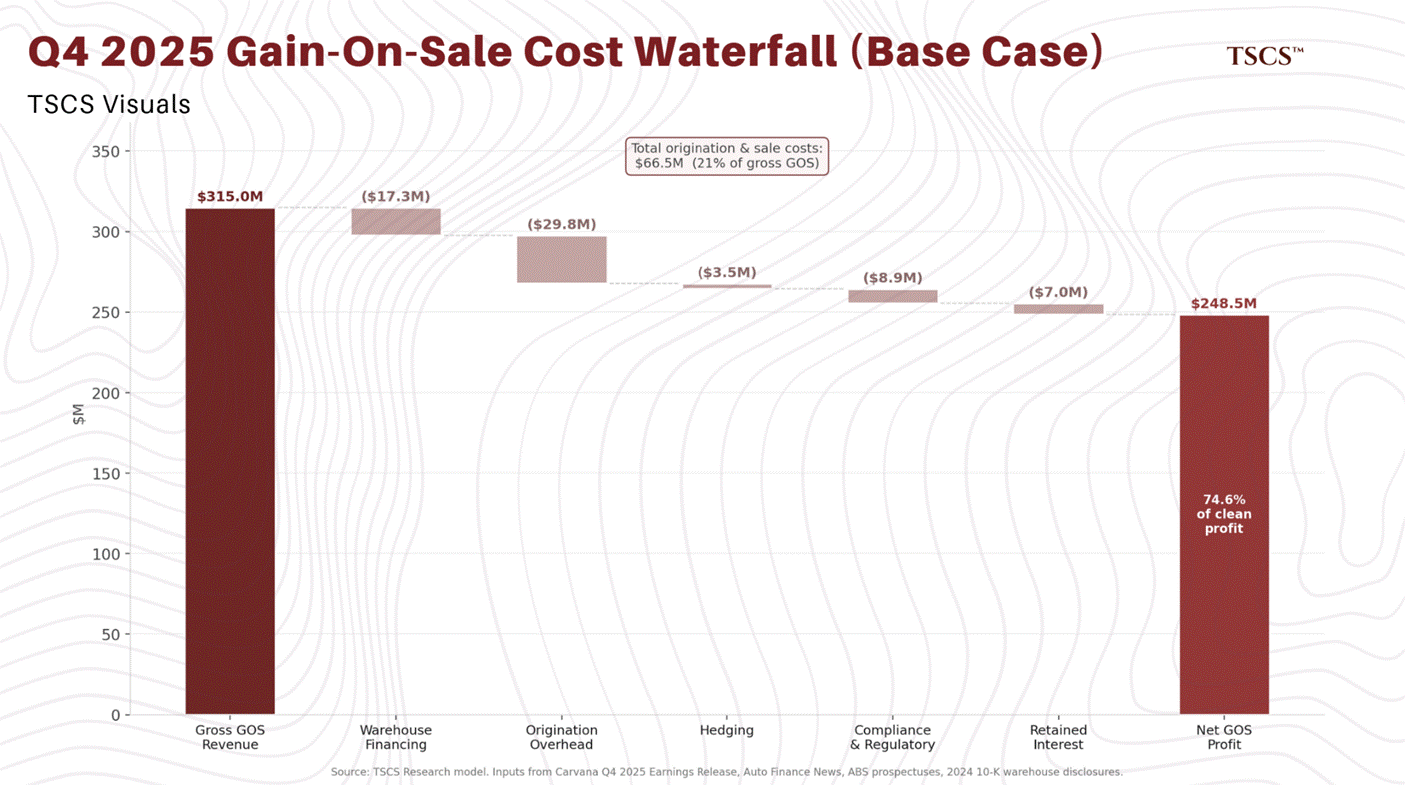

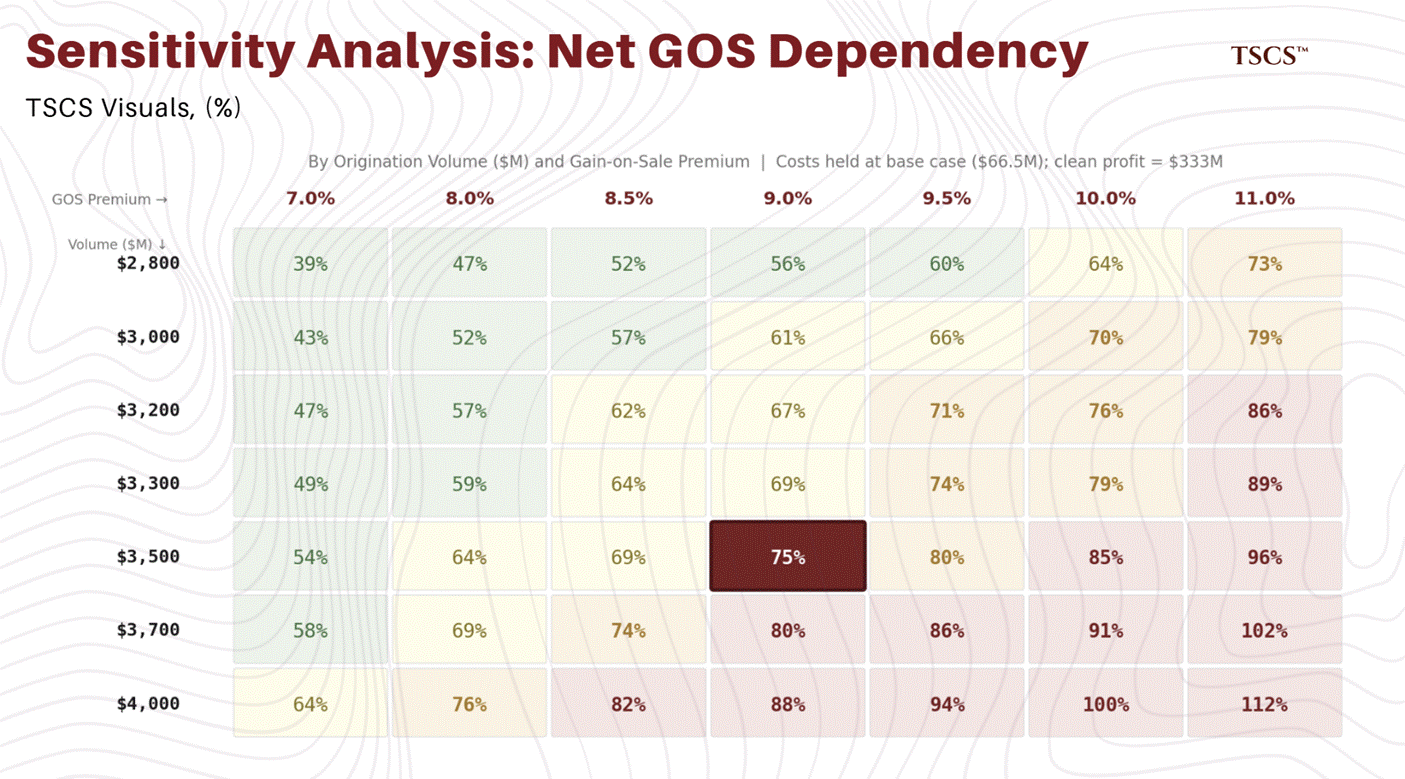

Bloomberg arrived at this figure by stripping the $685 million DTA release and the $67 million Root warrant loss from headline net income, then comparing the residual to reported gain-on-sale income. This methodology likely overstates the dependency somewhat, because it compares gross gain-on-sale revenue to bottom-line net income without deducting the direct costs of loan origination and sale (warehouse line financing, origination overhead, hedging, compliance). The true net profit contribution from gain-on-sale is lower than the gross figure. To estimate the net dependency, we built a bottom-up unit economics model using publicly verifiable inputs.

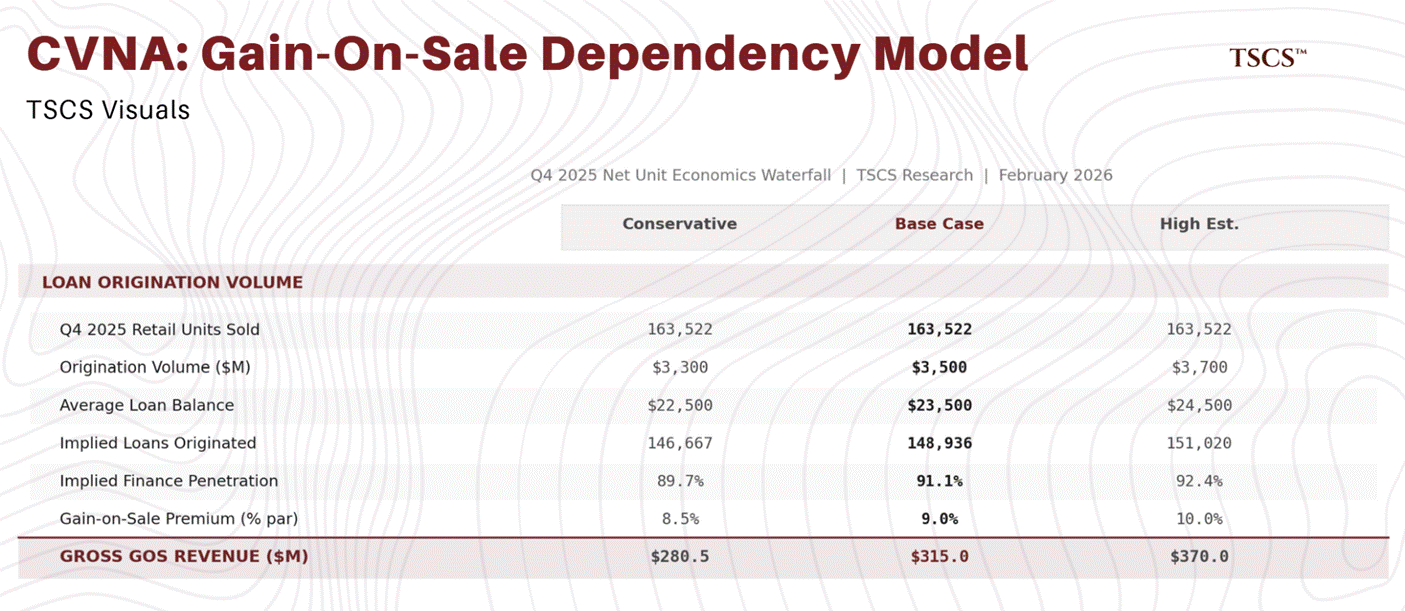

Q3 2025 loan origination volume was $3.4 billion (per Auto Finance News, October 30, 2025); scaling for Q4’s higher unit count yields approximately $3.3 to $3.7 billion in Q4 originations. At the implied 9% gain-on-sale premium (derived by dividing Bloomberg’s ~$316 million gross figure by estimated volume), gross gain-on-sale revenue was approximately $280 to $370 million.

Deducting estimated direct costs of origination and sale, including warehouse line financing ($13 to $24 million at SOFR plus 200 to 300 basis points on a 20 to 30 day weighted average hold period), per-loan origination overhead ($150 to $300 per loan across approximately 147,000 to 151,000 originated loans), interest rate hedging ($3 to $6 million), compliance and regulatory costs ($6 to $13 million), and retained interest mark-to-market ($3 to $15 million), total origination costs were approximately $46 to $102 million. The resulting net gain-on-sale contribution was $234 to $268 million, representing approximately 70 to 80% of Q4 clean profit, with a base case of 75%. The full model, with sourced assumptions and sensitivity tables, is available as a companion to this analysis.

In FY2024, gain on loan sales totaled $755 million against total reported earnings of approximately $550 million, meaning loan sales exceeded 100% of reported profits (with core retail operations running at a loss or breakeven). The direction is unambiguous regardless of the precise quarter measured: this is a financing business with a car dealership attached, not the other way around.

Full methodology and sourced assumptions are appended at the end of this report.

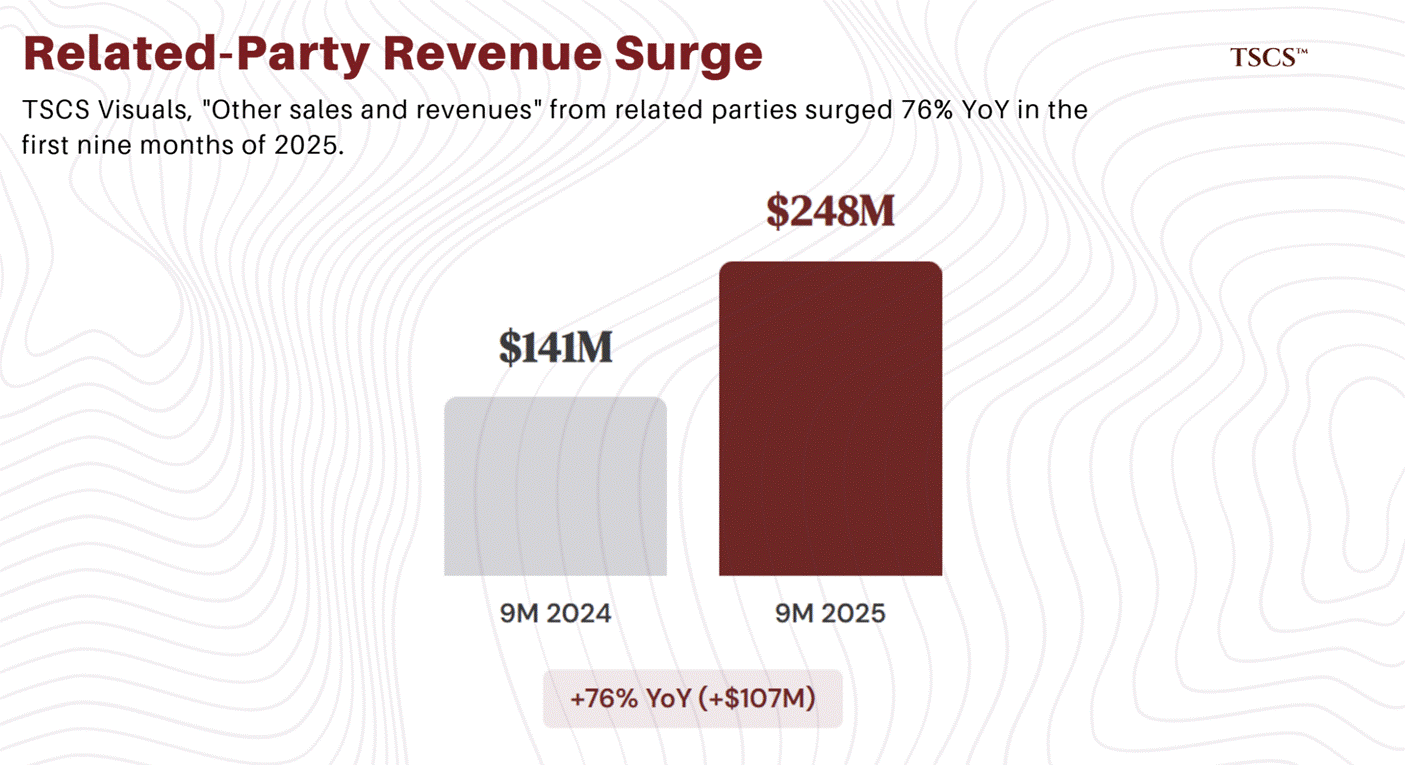

Related-party “other sales and revenues” surged 76% YoY in the first nine months of 2025 to $248 million (versus $141 million in the same period of 2024).

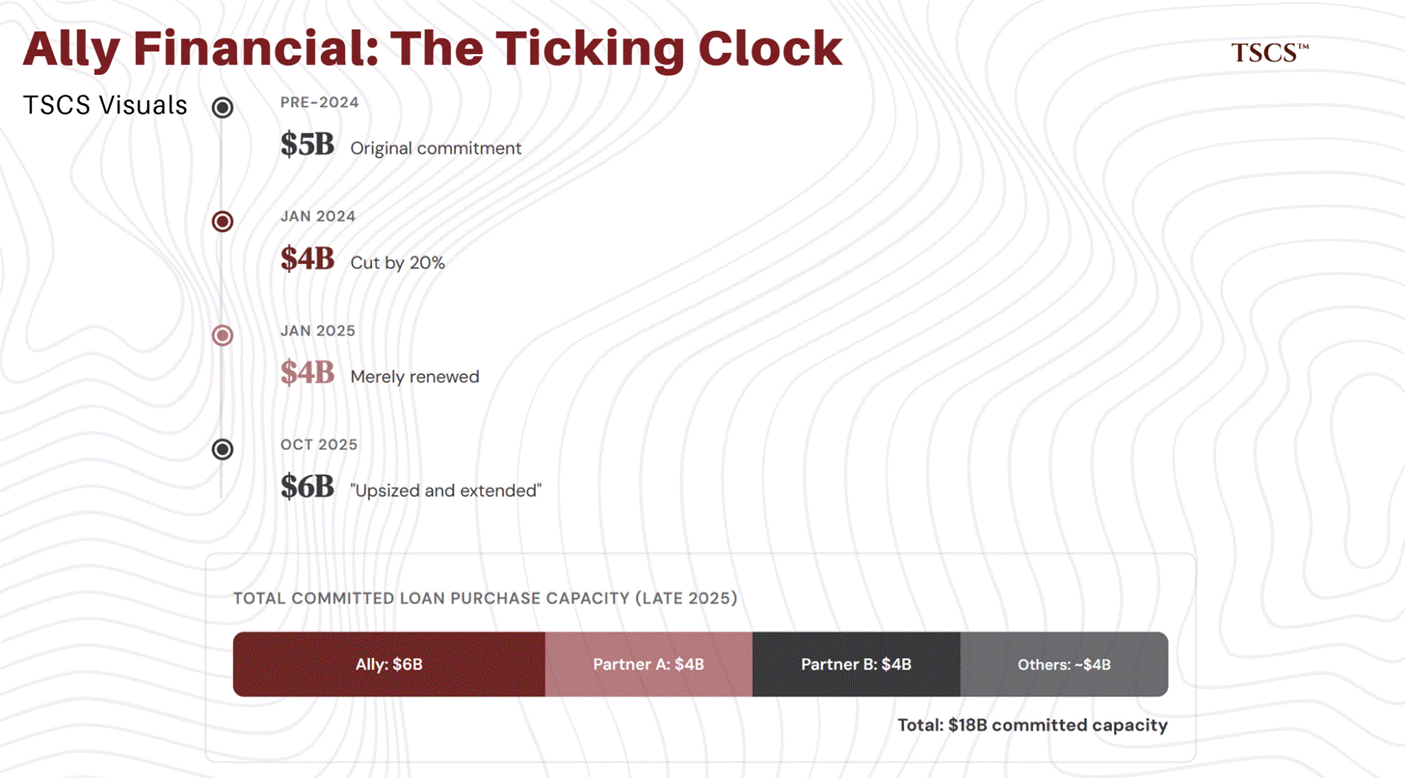

The gain-on-sale model is inherently volatile and subject to manipulation through timing. In its January 2025 report, Hindenburg Research cited a former Carvana executive with knowledge of loan sales who stated that the company could “move very large amounts of income around quarter to quarter” by holding loan sales over quarterly boundaries. Hindenburg provided supporting evidence: in Q1 2023, Carvana reported a 41% reduction in year-over-year loan sales, then two days after CEO Garcia III purchased $126 million in company stock amid depressed earnings, the company announced its “best quarter in company history” featuring re-accelerated loan sales. The Garcias realized approximately $427 million in gains on those precisely timed purchases. Carvana expanded its loan purchase agreements to $18 billion in total committed capacity across all partners by late 2025, but Ally Financial, historically the largest buyer (purchasing $3.6 billion or approximately 60% of originations in 2023), has a complicated recent history with Carvana that the company uses to project confidence but which actually reveals growing counterparty caution.

In January 2024, Ally reduced its forward-flow commitment from $5 billion to $4 billion, a move that predated Hindenburg’s report by a full year. Following the Hindenburg publication in January 2025, Ally merely renewed at the existing $4 billion level, via an 8-K filing on January 3, 2025. Carvana subsequently announced on its Q3 2025 earnings call (October 29, 2025) that the Ally agreement had been “upsized and extended” to $6 billion through October 2027. On the Q4 2025 earnings call (February 18, 2026), CEO Garcia referenced the Ally commitment as “$6 billion with Ally through October 2026,” a shorter term than the Q3 disclosure, though it is unclear whether this reflects an amendment or a misstatement, alongside two new $4 billion partnerships with unnamed loan sale partners, bringing total committed capacity to $18 billion.

However, the trajectory prior to that upsizing tells a different story from the one Carvana presents. Ally cut its commitment by 20% in January 2024, then merely renewed at the reduced level in January 2025, and its expansion came only in the context of Carvana simultaneously securing two additional $4 billion partnerships, a diversification driven by necessity rather than choice. When your largest historical buyer’s first instinct at each sign of scrutiny is to hold or reduce, the subsequent upsizing looks more like a negotiated quid pro quo (likely involving cherry-picking rights on credit quality) than a ringing endorsement of loan quality. Ally has progressively shifted its exposure toward prime and near-prime paper, effectively selecting the best credits and leaving Carvana to place subprime loans with less established buyers at worse economics.

The question is not whether Carvana can find buyers for its loans today, but what happens in October 2026. That is when the Ally Financial agreement, Carvana’s largest and longest-standing loan purchase relationship, comes up for renewal. Ally will make that decision against the backdrop of record 60-day subprime delinquencies (6.9% and rising), Carvana prime borrower default rates running at four times the industry average, and an active SEC investigation into the very loan origination practices that produce the paper Ally is buying. If Ally tightens terms, reduces commitments, or declines to renew the gain-on-sale engine that produced an estimated 70 to 80% of Q4 clean profit faces its first real stress test. The clock is running.

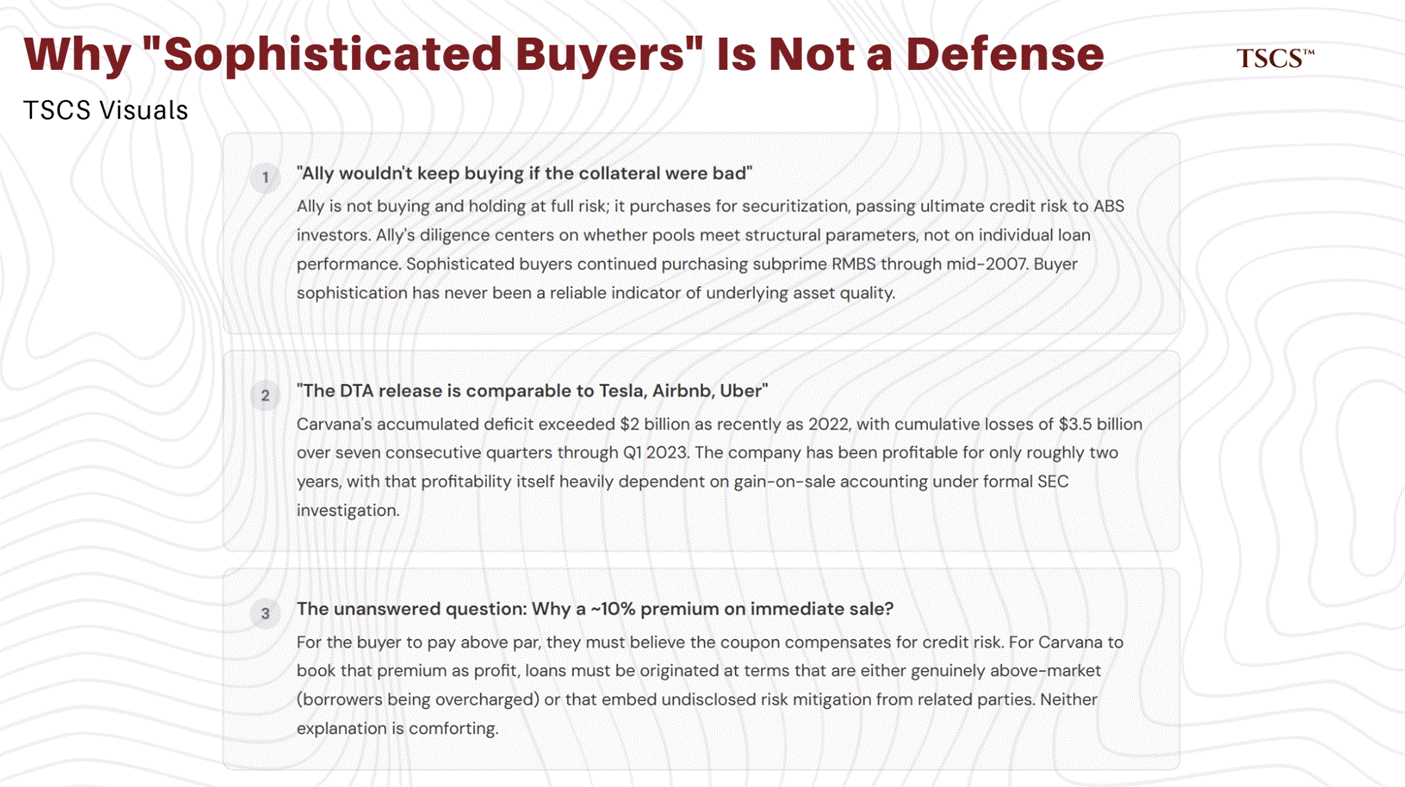

A frequent bull defense is that Ally Financial and other loan purchasers are sophisticated institutional investors who would not continue buying if the underlying collateral were deteriorating. This deserves serious engagement. The argument has surface appeal but collapses under scrutiny. Ally is not buying and holding these loans on its balance sheet at full risk; it is purchasing them for securitization, where the ultimate credit risk is passed to ABS investors. Ally’s due diligence centers on whether the loan pools meet the structural parameters of its securitization programs, not on whether each individual loan will perform.

More critically, the argument proves the opposite of what bulls intend. Sophisticated buyers continued purchasing subprime RMBS through mid-2007 and originating structured products until months before systemic collapse. The auto ABS market is structurally different from pre-crisis mortgage securitization (more granular, shorter duration, recoverable collateral), but the principle is identical: buyer sophistication has never been a reliable indicator of underlying asset quality. What matters is not who is buying, but what they are buying, and at what price, and whether the originator has any economic incentive to maintain underwriting discipline when 75 to 90% of its profit comes from the sale itself rather than the performance of the underlying loan.

The more important question, which no bull has convincingly answered, is why Carvana can originate a loan and immediately sell it for a roughly 9% premium.

For the buyer to pay above par, they must believe the coupon rate compensates them for the credit risk. For Carvana to book that premium as profit, the loan must be originated at terms that are either genuinely above-market (implying borrowers are being overcharged) or that embed undisclosed risk mitigation from related parties. Neither explanation is comforting.

Carvana compares its DTA valuation allowance release to similar actions by Airbnb, Tesla, and Uber upon reaching “sustained profitability.” But the justification is debatable: Carvana’s accumulated deficit exceeded $2 billion as recently as 2022, with cumulative losses of $3.5 billion over seven consecutive quarters through Q1 2023. The company has been profitable for only roughly two years, with that profitability itself heavily dependent on gain-on-sale accounting and related-party economics that are now under formal SEC investigation.

The Garcia ecosystem: $5.8 billion extracted, $1 billion burned, and an SEC subpoena

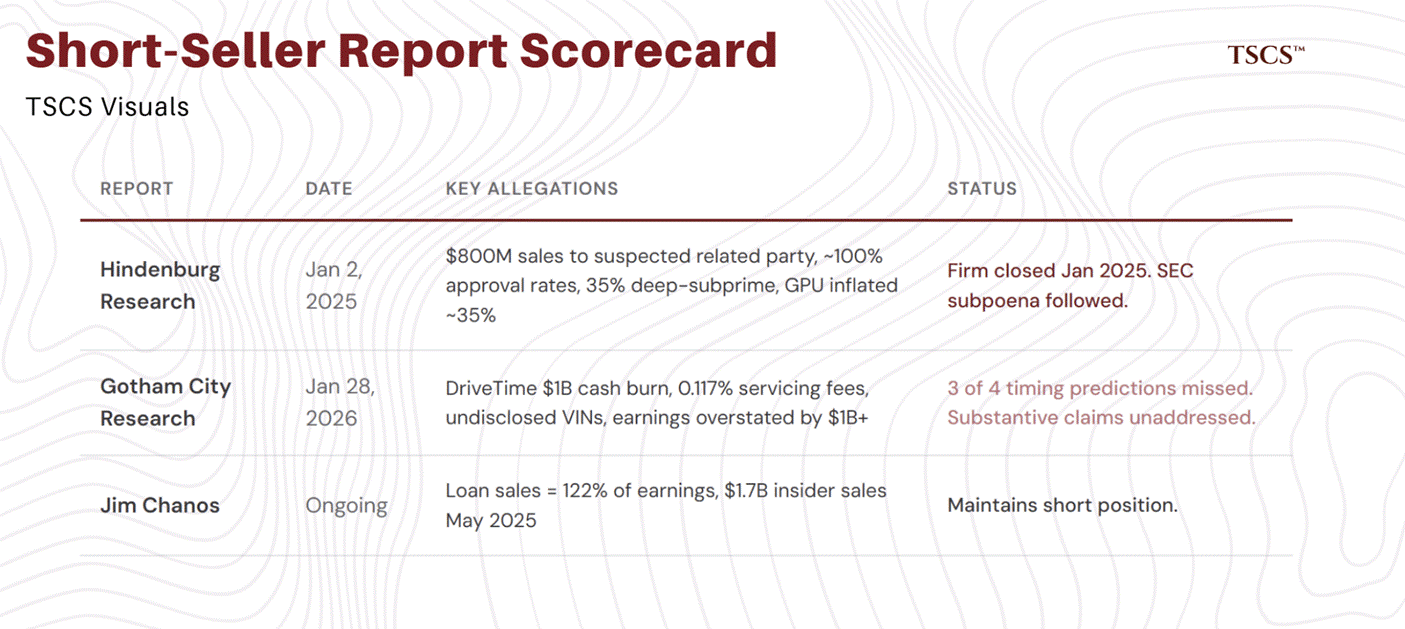

On January 28, 2026, Gotham City Research published “Carvana: Bridgecrest and the Undisclosed Transactions and Debts.” Gotham’s breakthrough was obtaining previously unavailable private company financials: DriveTime’s 2024 Annual Report and GoFi LLC’s 2024 financials, secured via FOIA requests. These documents, never before available to equity investors, revealed the financial condition of the Garcia family’s private entities that sit at the center of Carvana’s gain-on-sale ecosystem. For context, Carvana’s total reported earnings in 2023–2024 combined were approximately $550 million; Gotham alleges overstatement exceeding $1 billion, roughly 2x actual reported earnings.

The substantive findings, which remain unaddressed by either Carvana or its auditor, are as follows:

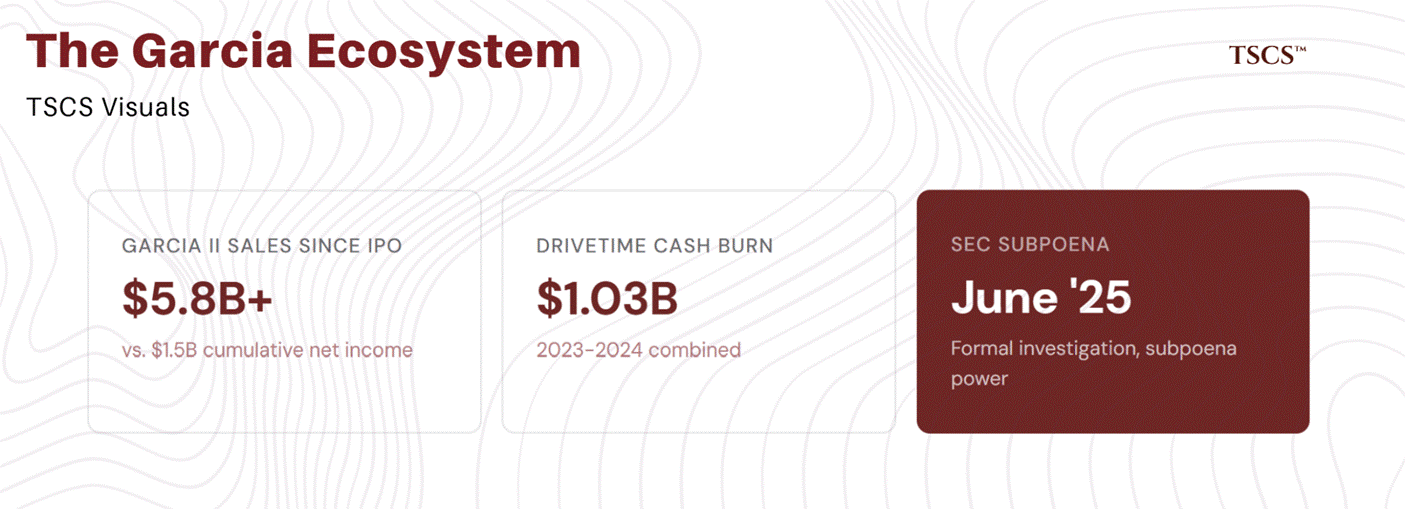

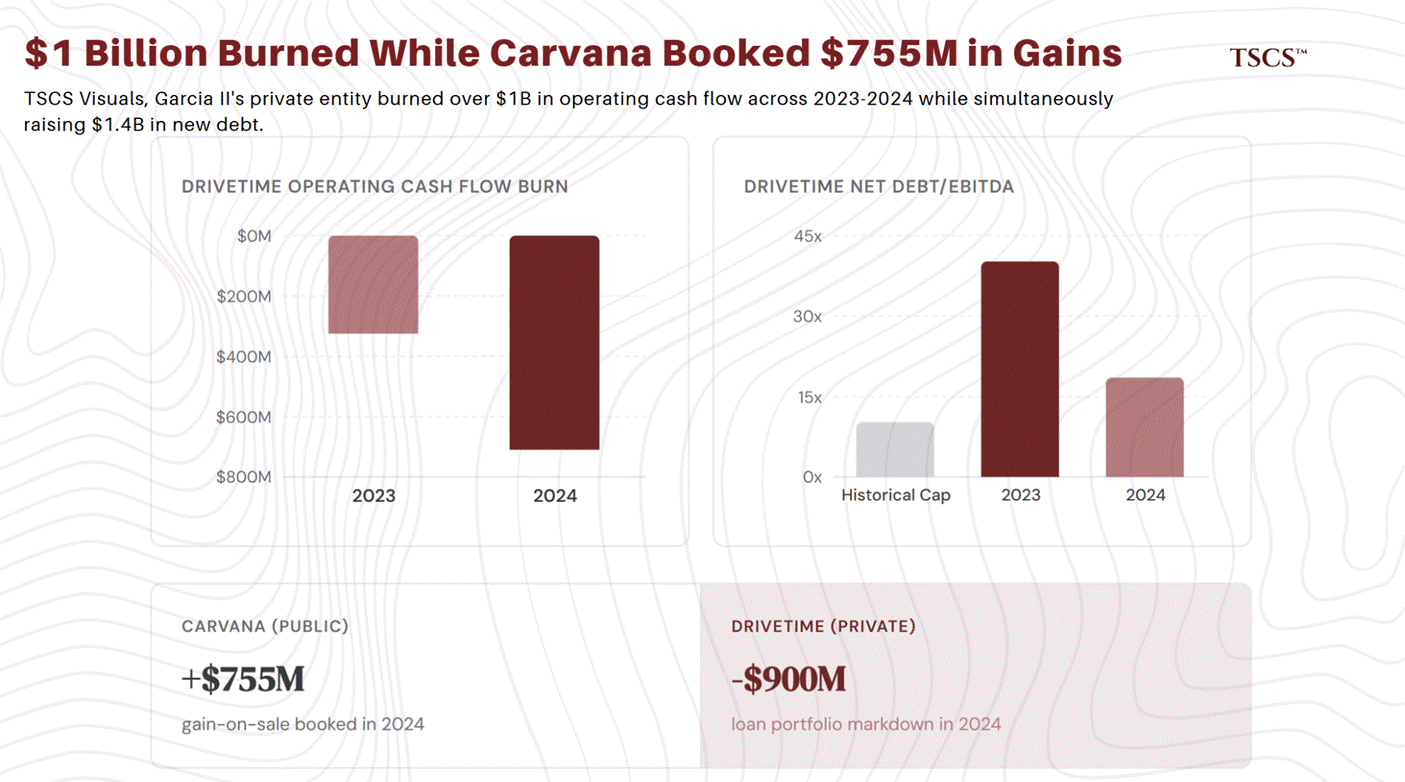

DriveTime (controlled by Ernest Garcia II, the CEO’s father) burned $324 million (2023) and $708 million (2024) in operating cash flow, over $1 billion combined, while simultaneously raising $1.4 billion in new debt. DriveTime’s net debt-to-EBITDA leverage exploded to 40.2x (2023) and 18.6x (2024), versus a historical cap of 10.3x. During this same period, Carvana booked $755 million in gain-on-sale of loans in 2024 alone, while DriveTime marked down its loan portfolio by $900 million, a concurrent divergence central to the manipulation allegation.

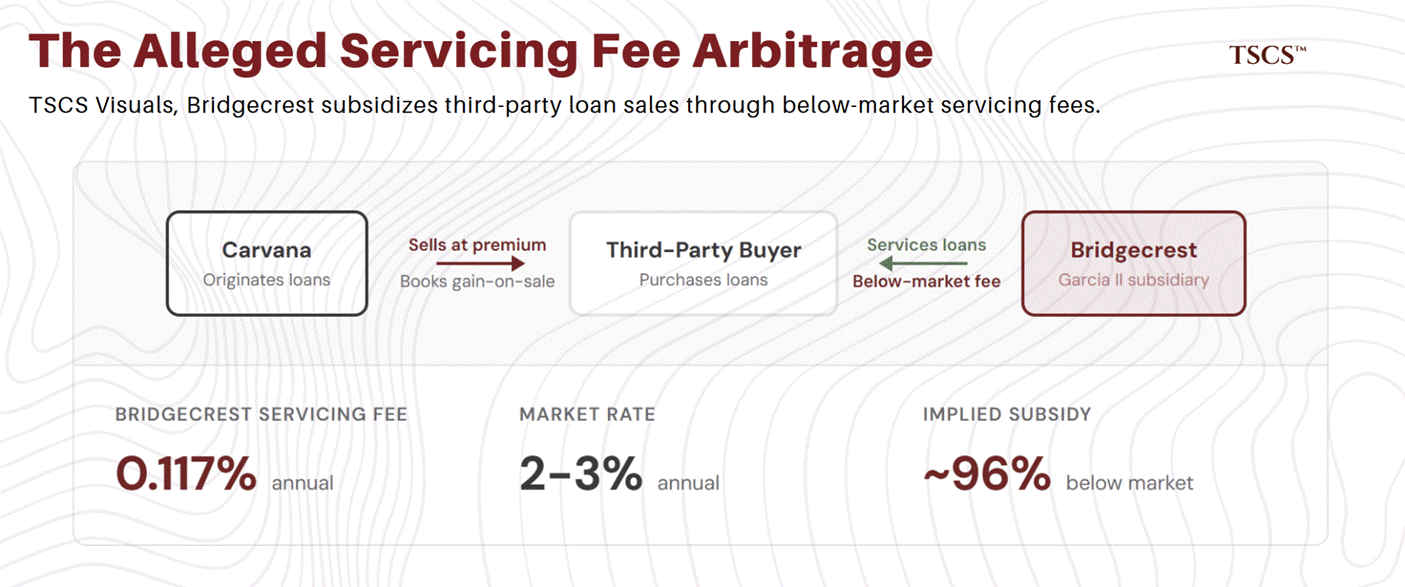

Gotham identified a servicing fee arbitrage mechanism: Bridgecrest (Garcia II’s loan servicing subsidiary) charges “third-party” loan buyers an estimated 0.117% annual servicing fee, versus a market rate of 2–3%. The theory: Carvana sells loans to third parties at inflated prices (booking gain-on-sale), while Bridgecrest subsidizes the arrangement through below-market servicing fees. Gotham also found dozens of VINs tied to Carvana-sold vehicles appearing on Bridgecrest’s balance sheet with Bridgecrest listed as originator, undisclosed by either company. A follow-up report identified 34 additional VINs with the same pattern.

GoFi LLC, also owned by Garcia II and sharing Carvana’s mailing address, generated nearly 100% of its 2024 revenue ($7.1 million) from gains on sale of finance receivables, suggesting it exists primarily to move loans between entities. All three Garcia entities (Carvana, DriveTime/Bridgecrest, GoFi) are audited by Grant Thornton, the same mid-tier auditor that gave clean opinions to Tricolor Holdings during its multi-year fraud (executives now indicted).

On the Q4 earnings call, CFO Jenkins stated: “We do not sell loans to related parties,” calling short-seller claims “100% inaccurate.” This denial is technically precise but non-responsive to the core allegation, which is that related parties subsidize the economics of loan sales to third parties. A denial of direct sales does not address indirect subsidization through servicing fee arbitrage. The stock fell 14.2% on the day of Gotham’s report, from $477.72 to $410.04.

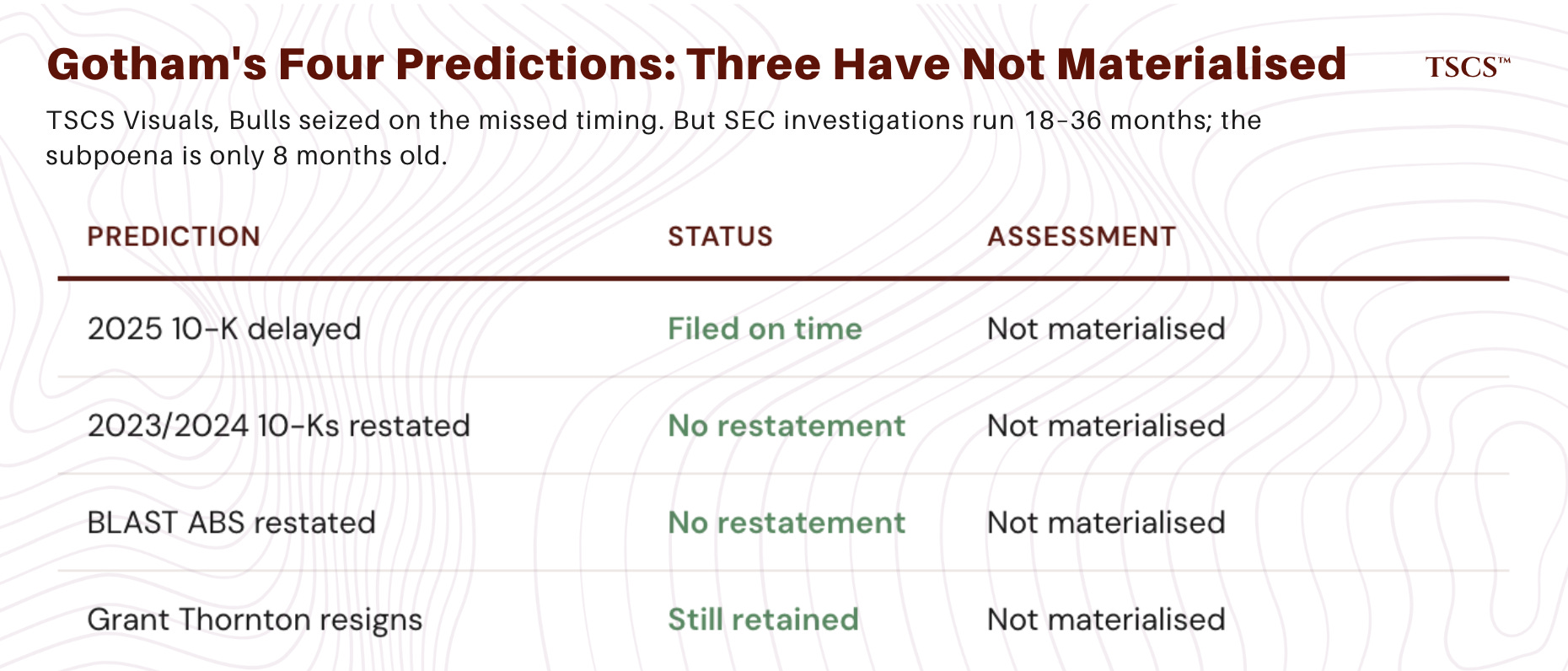

Gotham made four specific timing predictions: (1) Carvana’s 2025 10-K would be delayed, (2) 2023/2024 10-Ks would be restated, (3) BLAST ABS would be restated, and (4) Grant Thornton would resign. As of February 18, three of these four predictions have failed to materialize: the 10-K was filed on schedule, Grant Thornton has not resigned, and no restatements have been announced. Bulls, including JPMorgan’s Rajat Gupta, seized on these missed predictions to argue that the short thesis is discredited. BTIG called the report’s most serious allegations “not well-founded.” Needham’s Chris Pierce stated he did not believe Carvana needed “sweetheart deals” to sell subprime loans.

This sell-side pushback deserves scrutiny of its own. JPMorgan, whose analyst Rajat Gupta maintained his Overweight rating and $510 price target, has underwritten Carvana debt offerings. The banks telling investors to dismiss an active SEC investigation have, in several cases, direct financial relationships with the company they are defending. This does not mean their analysis is wrong. It means their conflicts are at least as material as those of the short sellers they dismiss, and should be weighted accordingly.

First, timing predictions about regulatory and audit actions are inherently uncertain, and the failure of a 10-K to be delayed within three weeks does not exonerate the underlying accounting questions. SEC investigations routinely run 18 to 36 months before producing enforcement actions; the formal subpoena was issued only eight months ago. Second, the sell-side’s track record on Carvana’s accounting is abysmal: every analyst covering CVNA maintained Buy or Hold ratings through the 2022 collapse, when the stock fell 99% from its peak, and the same analysts who are now dismissing related-party concerns were uniformly silent on the $3.5 billion in cumulative losses that preceded the “turnaround.” Third, and most importantly, Gotham’s substantive allegations about DriveTime’s cash burn ($1 billion in two years), below-market servicing fees, and undisclosed VIN overlap remain unaddressed by either Carvana or its auditor.

Hindenburg Research’s January 2, 2025 report (”A Father-Son Accounting Grift For The Ages”) laid the foundation, identifying $800 million in loan sales to a “suspected undisclosed related party” linked to Cerberus Capital Management (where Carvana director Dan Quayle serves as chairman). Hindenburg, which conducted 49 interviews with industry experts, former employees, competitors and related parties over four months, alleged nearly 100% approval rates, 35% deep-subprime originations, prime borrower delinquency rates 4x the industry norm, and that GPU was inflated ~35% by dumping selling costs into SG&A. Jim Chanos has maintained a CVNA short position throughout, flagging in a June 2025 Forbes presentation that gain on loan sales represented 122% of earnings and that insiders sold $1.7 billion in May 2025 alone.

Hindenburg Research announced its closure in January 2025, shortly after publishing the Carvana report, meaning the original short-seller is no longer actively pressing the thesis or releasing follow-up research. This shifts the burden of maintaining public scrutiny to Gotham City Research and independent analysts. The insiders’ own behaviour suggests they take these allegations far more seriously than the sell-side does. The selling pattern at Carvana is among the most extreme in public markets.

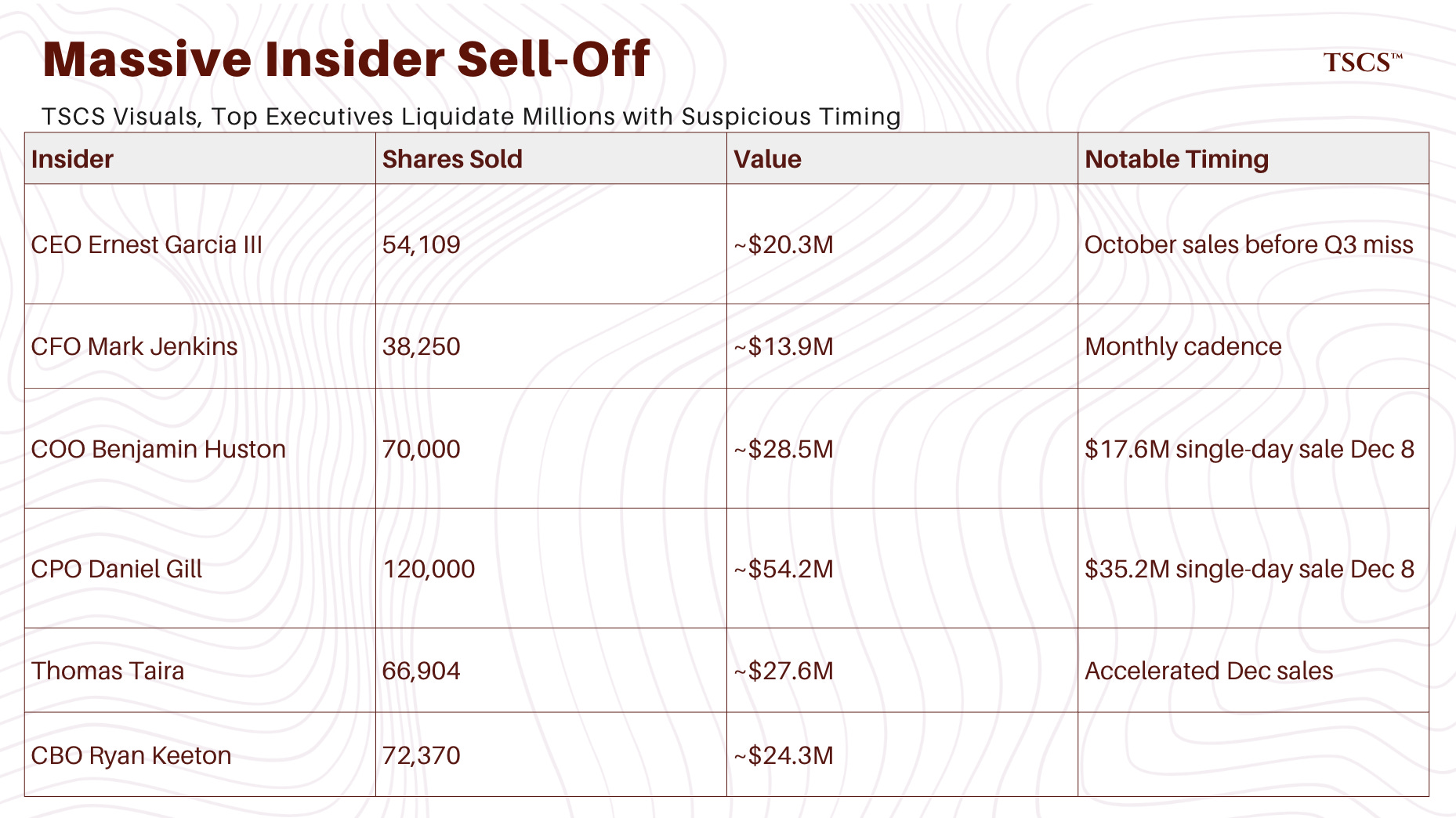

Not a single insider has purchased shares in over a year. In the last 90 days alone, insiders sold $183.6 million in stock across 420,351 shares, with zero offsetting purchases. The only insider buy in recent history: board member Neha Parikh’s 2,600 shares (~$200,000) at $77 in 2023.

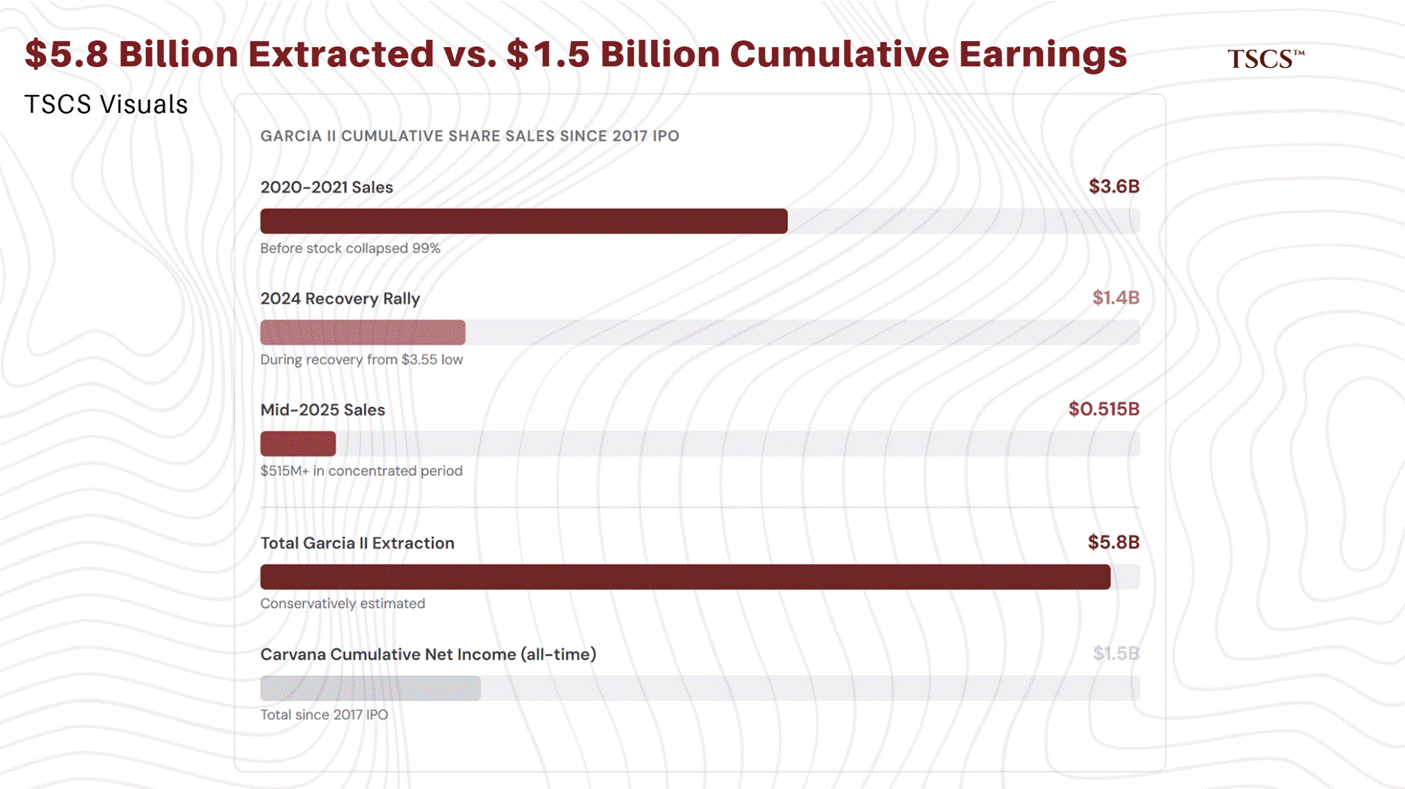

Ernest Garcia II’s cumulative sales since Carvana’s 2017 IPO now conservatively exceed $5.8 billion: $3.6 billion during 2020–2021 (before the stock collapsed 99%), $1.4 billion during the 2024 recovery rally, and $515+ million in mid-2025 alone. For context, Carvana’s total cumulative reported net income since its IPO is approximately $1.5 billion. The controlling family has extracted nearly four times what the company has ever earned. Enron insiders sold approximately $1.1 billion before that company’s collapse. Wirecard’s executives extracted roughly $200 million. Garcia II alone has extracted more than four times what Enron and Wirecard insiders took out combined.

He simultaneously pulled $352 million in distributions from DriveTime while it burned $1 billion in cash and raised $1.4 billion in debt. Despite these massive liquidations, Garcia II retains ~78 million shares (35.9% of the company) and controls 84%+ of voting power through dual-class supervoting Class B shares.

The timing of executive sales is particularly notable. In Q4 2025:

Five sales in two months

On December 8 alone, two weeks before S&P 500 inclusion, Gill, Huston, Taira, and Breaux collectively sold $75 million in a single day, selling into index-inclusion-driven passive demand. CFO Jenkins and COO Huston then sold shares at $393–$418 on February 2, 2026, just 16 days before the disappointing Q4 report. Carvana has not disclosed whether these sales were executed under pre-scheduled 10b5-1 trading plans; if they were, the timing inference weakens considerably, though the unanimous direction of insider activity (sell, never buy) remains significant regardless of scheduling mechanism. Meanwhile, UBS Asset Management cut its position by 69.6%, even as passive index funds were forced to add. The institutional response to these allegations extends well beyond stock sales. The legal landscape has intensified dramatically.

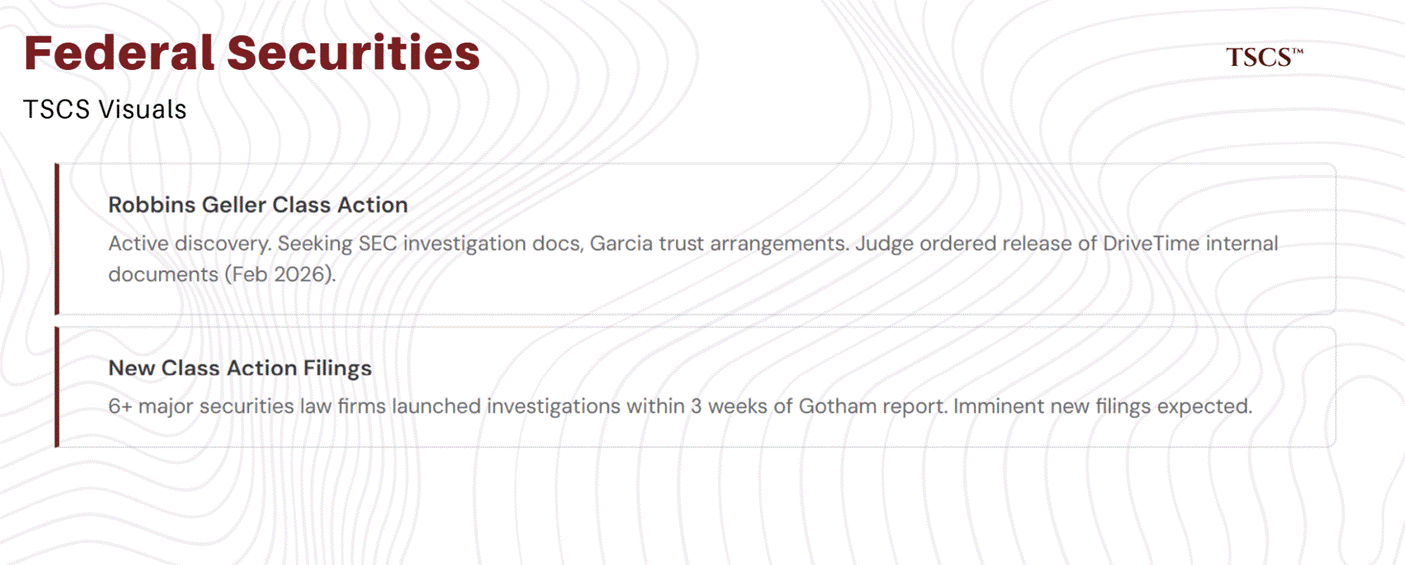

The Robbins Geller securities class action (United Association National Pension Fund v. Carvana, No. 2:22-cv-02126, D. Ariz.) is now in active discovery after surviving multiple motions to dismiss. In recent hearings, plaintiffs are seeking documents related to two SEC investigations (2019 and 2025), the Garcia father-son trust arrangements, and accusing Carvana of intentionally misusing online discovery tools to delay document production. Carvana has refused to release DriveTime financial details in this lawsuit. A federal judge reportedly ordered the release of previously withheld DriveTime internal documents in mid-February 2026.

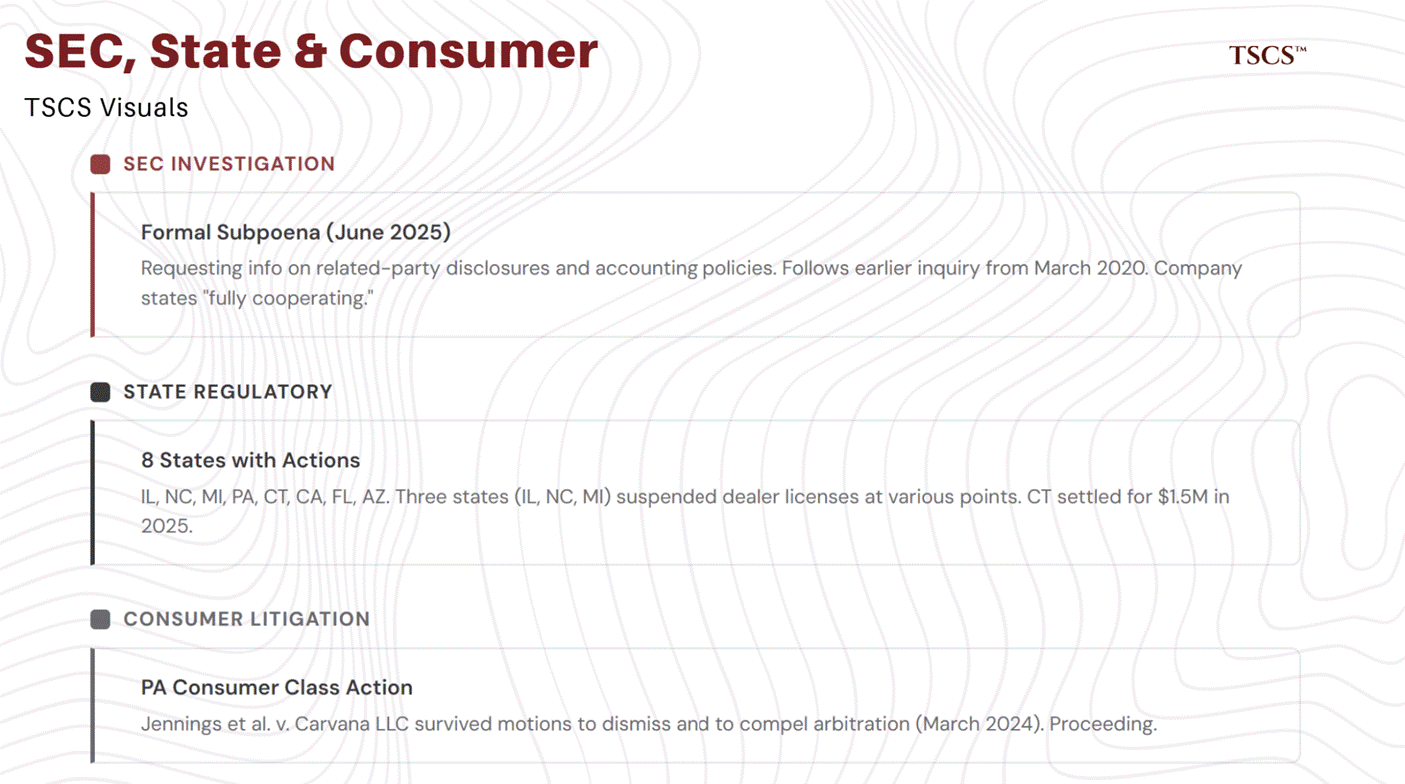

The SEC has a formal investigation with subpoena power. Carvana disclosed receiving a formal SEC subpoena in June 2025 (in its July 2025 10-Q), requesting information primarily related to Hindenburg’s allegations about related-party disclosures and accounting policies. This follows an earlier SEC inquiry dating to March 2020. Carvana states it is “fully cooperating.” Under the current regulatory environment, the threshold for formal subpoena issuance is elevated, making the fact that one was issued a significant signal.

Post-Gotham City, at least six major securities law firms launched investigations within three weeks, a pace that strongly suggests imminent class action filings with a new class period.

On the consumer front, the Pennsylvania consumer class action (Jennings et al. v. Carvana LLC) survived motions to dismiss and to compel arbitration in March 2024 and is proceeding. At least eight states (Illinois, North Carolina, Michigan, Pennsylvania, Connecticut, California, Florida, Arizona) have taken regulatory action against Carvana, with Illinois, North Carolina, and Michigan having actually suspended Carvana’s dealer license at various points. Connecticut settled for $1.5 million in 2025. All three Delaware shareholder lawsuits (direct offering, insider trading, supervoting challenge) have been resolved in Carvana’s favor, but the factual record they established feeds directly into the ongoing federal case and SEC investigation.

Record subprime delinquencies meet Carvana’s aggressive lending

Carvana’s lending practices sit at the epicenter of the subprime auto crisis. 44% of loan originations are classified as non-prime, with over 80% of recent non-prime ABS deals featuring “deep subprime” weighted-average FICO scores of 567–584. The company’s minimum income requirement for financing is just $5,100 annually, 36% below the federal poverty level. In Hindenburg’s January 2025 report, which drew on 49 interviews including with former Carvana employees and a former director, multiple sources confirmed the company approved virtually all applicants; one former director explicitly stated approval rates were “100%.” Hindenburg also cited a former reconditioning leader who disclosed the existence of an undisclosed “economy line” of lower-quality vehicle reconditioning that Carvana had not disclosed to investors.

The timing is ominous. Fitch Ratings reported that 60+ day subprime auto loan delinquencies hit a record 6.9% in January 2026, the highest since tracking began in the early 1990s. Across Carvana’s own ABS pools, 31-day-plus delinquencies (a broader measure than Fitch’s 60-day standard) increased from 5.13% (December 2021) to 8.67% (September 2024). While this is not a direct apples-to-apples comparison with the industry’s 60-day metric, the trajectory is unambiguous: Carvana’s delinquencies are rising faster than the broader market, even on the less stringent 31-day threshold, at a time when the company claims credit quality is improving.

Most strikingly, Carvana’s 60-day delinquencies among “prime” borrowers run at four times the industry average, suggesting their internal credit classifications do not match industry standards. S&P data shows Carvana’s subprime loans have the highest extension rate among all subprime auto issuers, a mechanism facilitated by Bridgecrest that masks true delinquency levels.

The broader environment confirms deterioration. Repossessions hit 1.73 million in 2024 (the highest since 2009), auto loan defaults surpassed recession-era peaks at 2.3 million, and the total delinquent balance exceeded $60 billion in 2025. Most pointedly, Tricolor Holdings, a subprime auto lender with the same auditor (Grant Thornton) and similar structures to Carvana’s lending ecosystem, filed for Chapter 7 liquidation in September 2025 amid fraud allegations, with $2 billion in ABS impacted.

Bulls point to KBRA’s October 2025 decision to affirm and upgrade 12 classes of Carvana Auto Receivables Trust notes as evidence that the ABS pools are performing. This is misleading. ABS rating upgrades reflect structural credit enhancement (overcollateralization, subordination) being sufficient to protect senior tranche holders, not that the underlying loans are performing well. A pool can experience worsening delinquencies and defaults while its senior tranches remain well-protected. The upgrades tell you about the ABS structure, not the loan quality. What would concern ABS investors is not a gradual rise in delinquencies but a sudden, correlated spike, exactly the kind of event that record subprime delinquencies and rising repossession volumes foreshadow.

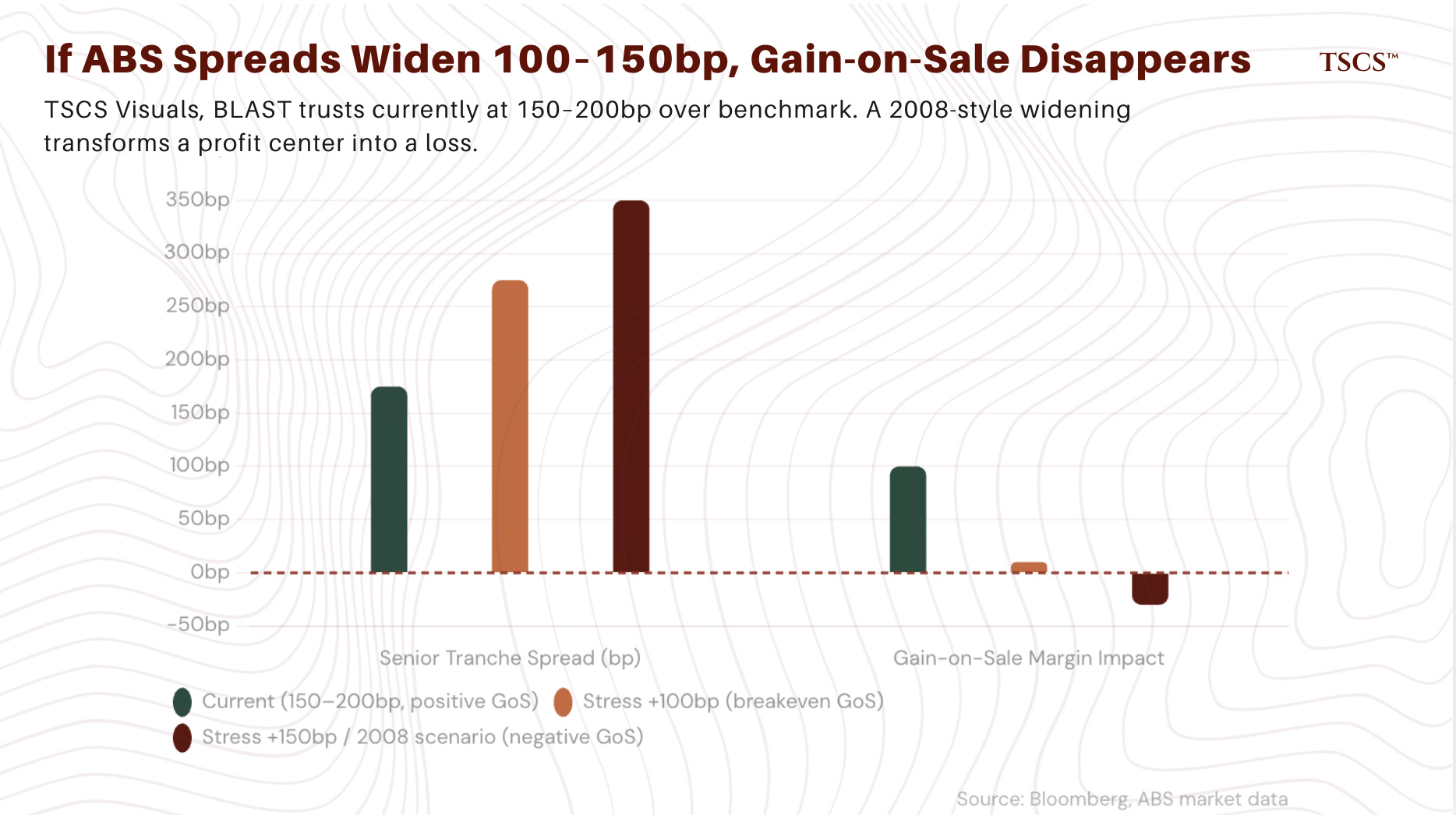

The transmission mechanism is ABS spread widening. Carvana’s BLAST securitization trusts currently price at roughly 150 to 200 basis points over benchmark for senior tranches, but subordinate tranches have seen spread compression reverse in late 2025. If subprime auto ABS spreads widen by 100 to 150 basis points, as occurred in 2008 and briefly in early 2020, the gain-on-sale premium that Carvana books at origination compresses or disappears entirely. The company would still be selling loans, but at par or below, transforming a profit center into a break-even or loss-making activity. This is not a tail risk; it is the base case if delinquency trends continue on their current trajectory.

Carvana books no loss reserves on loans held on its balance sheet, which increased 50% since 2021 to $553 million by Q3 2024. This accounting choice flatters current earnings but creates unrecognized exposure.

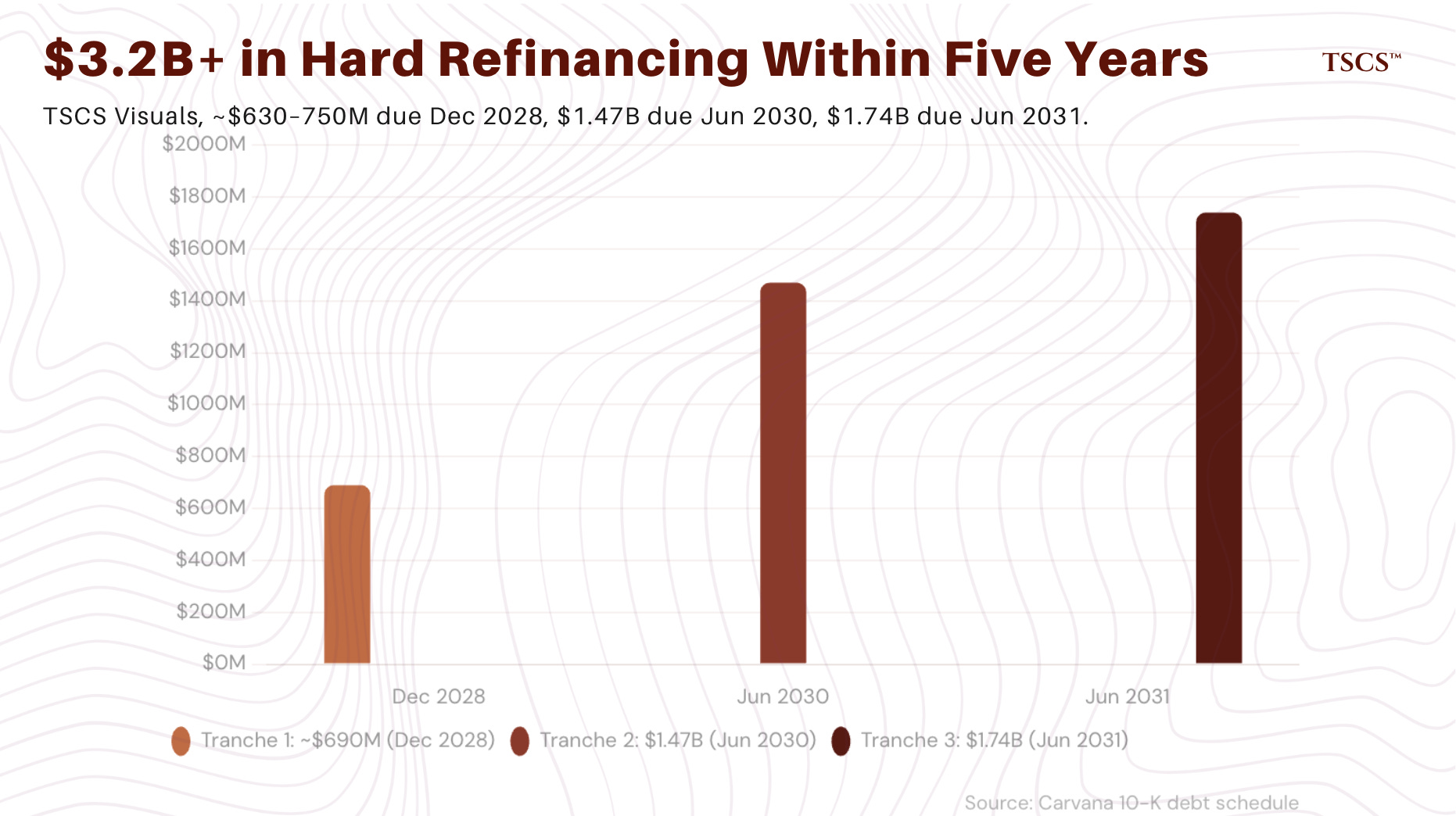

These credit risks collide with a balance sheet that has improved but remains stretched. Total debt stands at approximately $4.8 to $5.2 billion, with cash of $2.3 billion and net debt of approximately $2.9 billion (1.3x trailing EBITDA), materially improved from the 2022 crisis. The PIK-to-cash interest transition is now largely complete, with annualized net interest expense running at approximately $392 million by Q4 2025, consuming roughly 49% of operating cash flow. Over $3.2 billion in hard refinancing needs come due within five years (approximately $630 to $750 million in December 2028, $1.47 billion in June 2030, and $1.74 billion in June 2031). If gain-on-sale margins compress at the same time ABS spreads widen, the company faces deteriorating debt service coverage precisely when it needs to refinance at reasonable rates. Bears should acknowledge that 1.3x net leverage is a genuine improvement; bulls should acknowledge that a single bad quarter of loan sales could rapidly change the math.

The bull case is genuinely compelling, and that is precisely what makes this dangerous

If you are long Carvana, you are not stupid. The bull case is real, and dismissing it is how bears got crushed on the ride from $4 to $486. Understanding exactly why it is compelling is the only way to understand why it is insufficient.

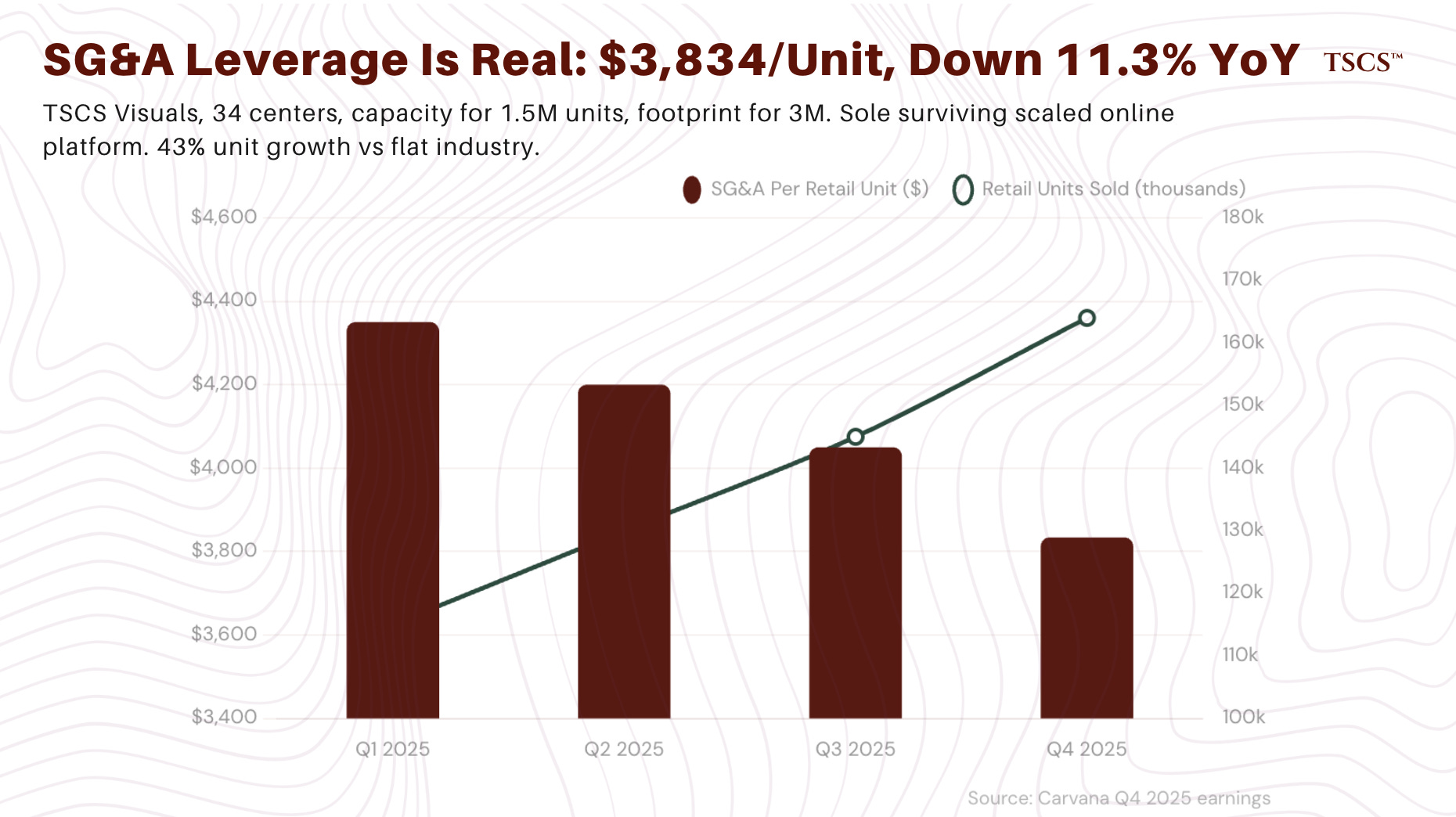

Carvana is achieving genuine SG&A leverage. Q4 SG&A per retail unit fell to $3,834, down 11.3% year-over-year, with improvements across compensation, advertising, and logistics. This is not accounting fiction; it reflects real operational scaling as the ADESA infrastructure absorbs higher volumes. The company now operates 34 inspection and reconditioning centers with built capacity for 1.5 million annual units, and management claims the real estate footprint supports 3 million. SG&A leverage at these volumes is the structural bear killer: if Carvana can push through to 1 million units with the current cost base, the profit math changes dramatically even without any improvement in GPU.

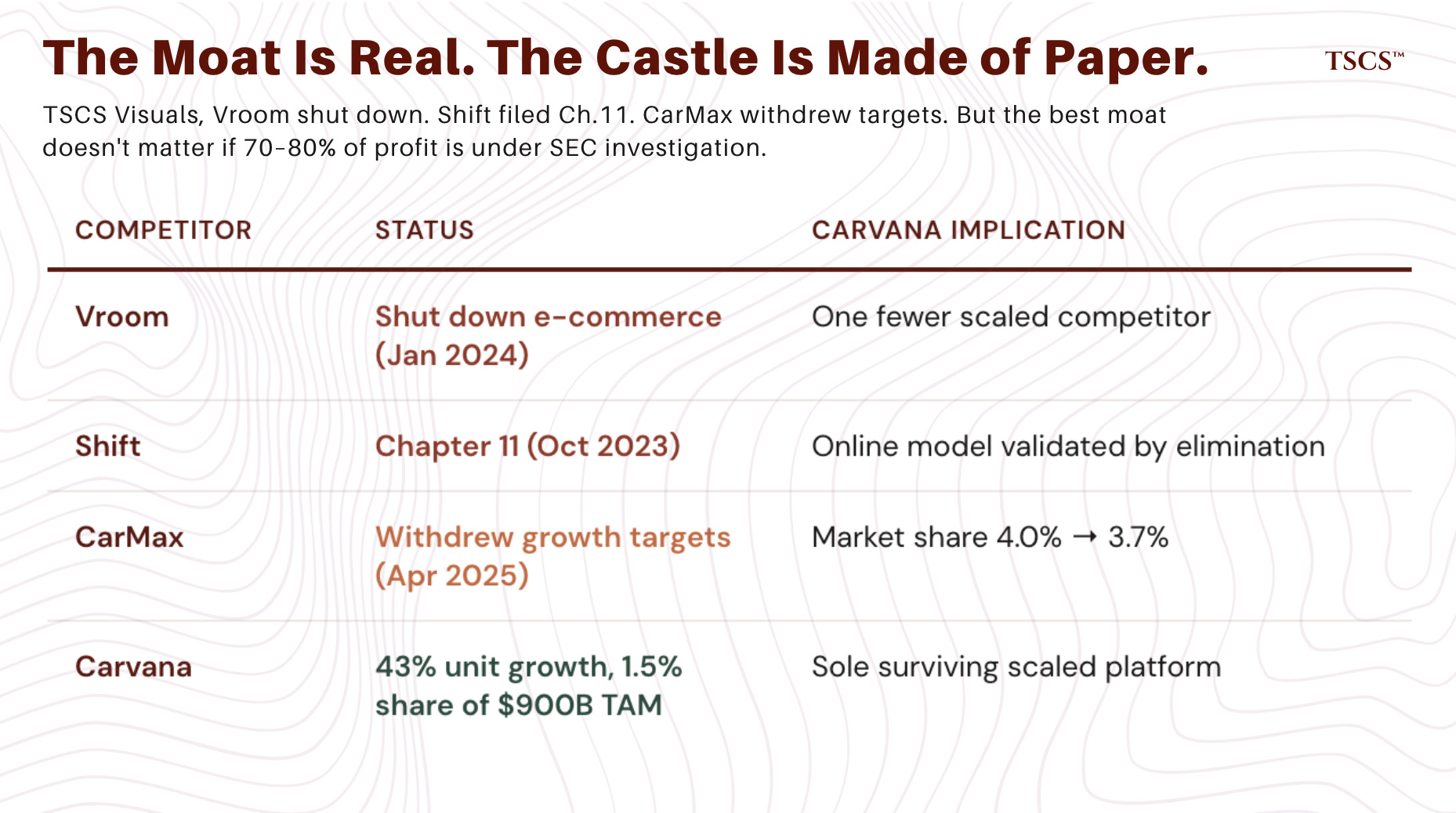

Competitively, Carvana now operates as the sole surviving scaled online used-car platform. Vroom shut down e-commerce in January 2024. Shift filed Chapter 11 in October 2023. CarMax, the largest traditional competitor, withdrew its long-term growth targets in April 2025 and watched its market share decline from 4.0% to 3.7%. Carvana’s 43% unit growth against an industry that was flat or declining is a genuine achievement that no public competitor is matching. At 1.5% market share in a $900 billion annual market, the runway is vast.

But here is the critical distinction the bulls elide: operational scaling and market share gains are necessary conditions for the Carvana thesis, not sufficient ones. The company had 43% unit growth and 58% revenue growth in Q4, and EBITDA margins still compressed. GPU still fell. Operating margin was essentially flat year-over-year despite massive top-line growth.

Bulls will argue that the GPU decline is temporary, driven by reconditioning cost inefficiencies at newly integrated ADESA locations, and that management’s own estimate of $220 per unit in recoverable costs suggests a snapback in Q2-Q3 2026. This is plausible but insufficient. Even if we grant the full $220 recovery, retail GPU would rise from $3,076 to approximately $3,296, still below Q3 2025’s $3,556 and still below Q4 2024’s $3,333. The trend is downward even after adjusting for the acknowledged temporary headwind. More fundamentally, even a full GPU recovery does not address the core vulnerability: the retail vehicle business, absent gain-on-sale income, generated approximately $16 million in Q4 operating profit. GPU improvements of $220 per unit across 163,522 units would add roughly $36 million per quarter, bringing core retail operating profit to approximately $52 million quarterly, or $208 million annualized. On a $55+ billion enterprise value, that is still approximately 265x. The SG&A leverage story is real, but it is a story about a cost line that is already performing well; the revenue quality problem is what the market is mispricing.

The competitive moat is real. It is also irrelevant to the question the market is actually pricing. Carvana has built the best online used car platform in America. It has no scaled competitors. It has infrastructure for 3 million units. All of this is true, and none of it changes the fact that an estimated 70 to 80% of clean profit on a net basis (and as high as 95% gross, pre-cost, per Bloomberg’s Q4 analysis) comes from a financing activity that is (a) under SEC investigation, (b) dependent on willing counterparties in a deteriorating credit environment, and (c) controlled by a family that has extracted $5.8 billion while their private entity burned $1 billion in cash. You can build the best moat in the world. It does not matter if the castle inside it is made of paper.

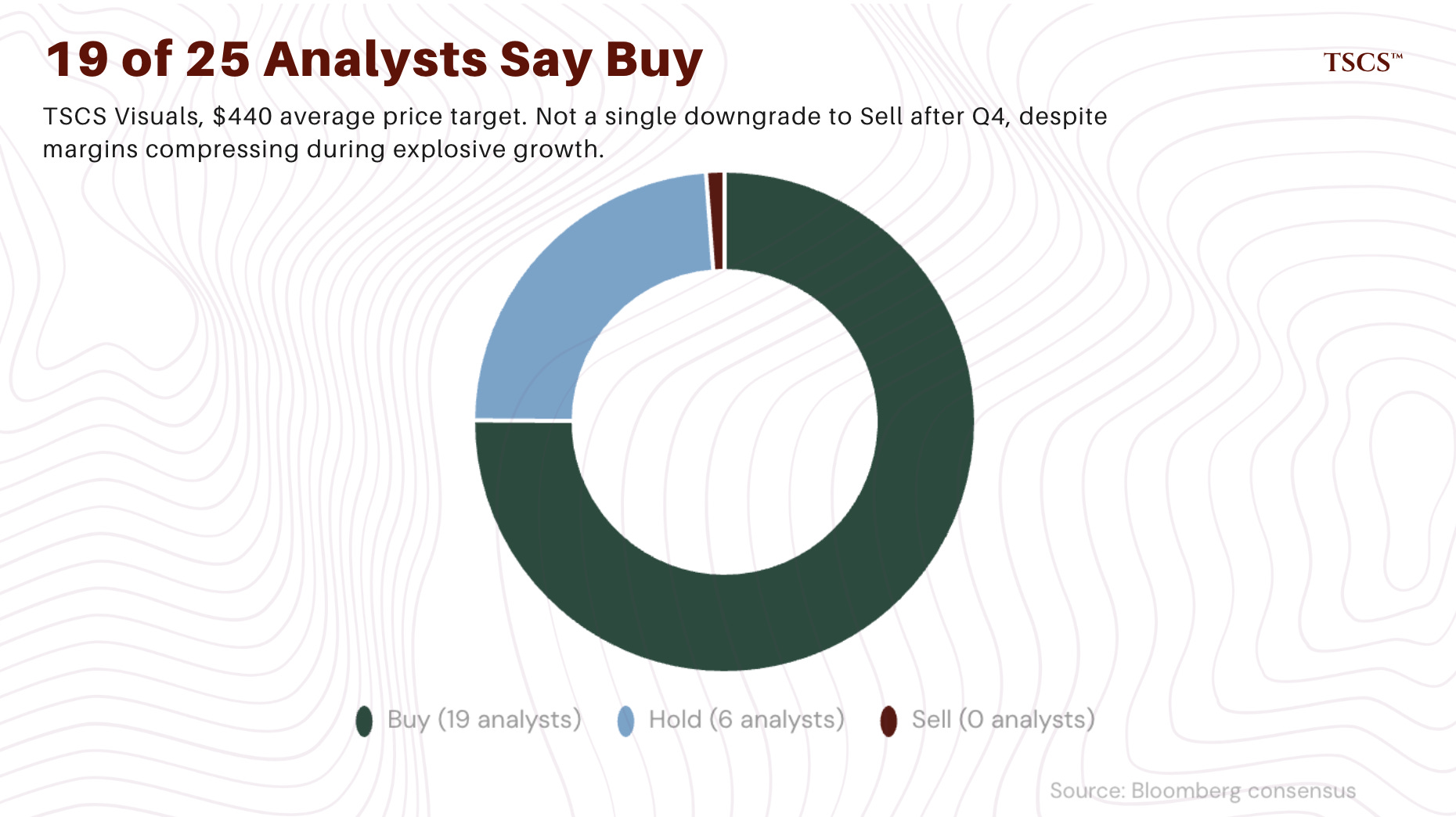

The bulls are right that Carvana has operational advantages. They are wrong that operational advantages make the earnings quality and governance questions irrelevant. The sell-side agrees, at least implicitly: every major bank covering CVNA lowered its price target after Q4, but not a single analyst downgraded to Sell.

Conclusion: When the accounting tide goes out

The Q4 2025 report crystallized the tensions that have been building beneath Carvana’s turnaround narrative. The company is genuinely growing fast, 43% unit growth and $20 billion in annual revenue are real achievements. But growth without margin expansion at this leverage level is not a turnaround; it’s a treadmill.

Three converging forces threaten the bull thesis simultaneously.

First, approximately $400 million in annual cash interest is now fully embedded in the run rate, consuming nearly half of operating cash flow precisely as EBITDA margins compress. Second, the gain-on-sale dependency, representing the overwhelming majority of clean Q4 profit per Bloomberg’s analysis, is under structural pressure from record subprime delinquencies and a credit cycle that is deteriorating at exactly the moment the company’s loan buyers must decide whether to tighten standards. Third, the Gotham City and Hindenburg allegations have forced an SEC formal investigation and active discovery that could expose the true economics of the Garcia family ecosystem.

The insiders themselves are providing the clearest signal. $5.8+ billion in cumulative sales against zero purchases. A CFO selling shares at $410 sixteen days before an earnings miss. A family patriarch extracting $352 million in distributions from a related entity burning $1 billion in cash while Carvana books $755 million in “gains” from the same loan pool. The valuation allowance release provided one quarter of headline camouflage, but it cannot repeat, and the operating metrics beneath it are deteriorating on every margin that matters.

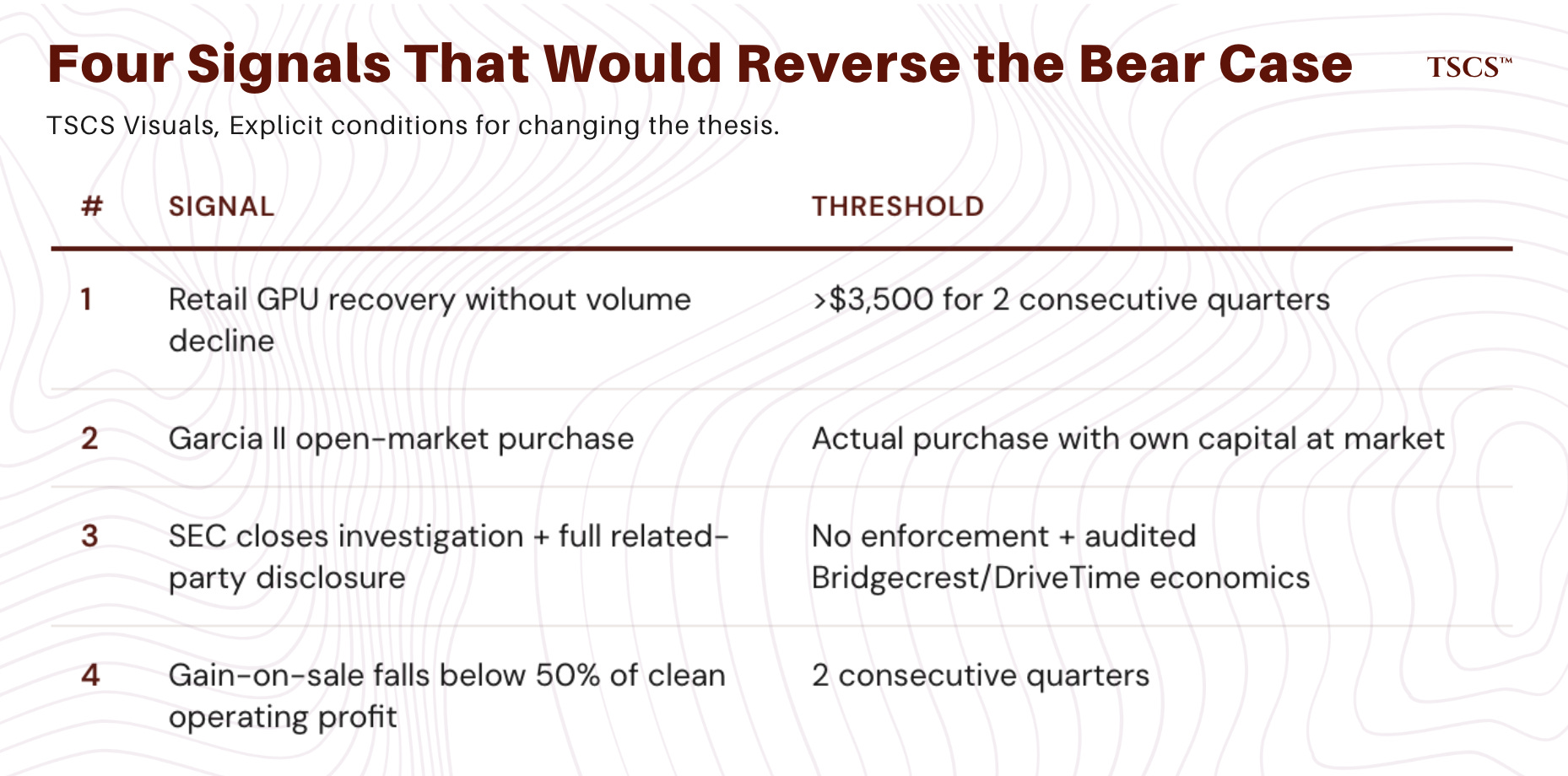

What would change this thesis? We believe in stating explicitly what evidence would cause us to reverse our position. First, if retail GPU recovers above $3,500 for two consecutive quarters without a corresponding decline in unit volume, that would indicate the reconditioning cost issue was genuinely temporary. Second, if Ernest Garcia II makes a meaningful open-market purchase (not an options exercise or a gift, an actual purchase with his own capital at market prices), that would be the single strongest counter-signal to six years of uninterrupted selling. Third, if the SEC closes its investigation without enforcement action and Carvana provides full, audited disclosure of all related-party economics including Bridgecrest servicing fees and DriveTime’s loan portfolio performance, that would substantially reduce the opacity premium the stock deserves. Fourth, if gain-on-sale income falls below 50% of clean operating profit for two consecutive quarters, that would demonstrate the retail business can stand on its own. We are not holding our breath on any of these.

We want to be clear about what this analysis is and is not claiming. Carvana is not a zero. The company has real revenue, real competitive advantages, and a genuine operational scaling story. If the bull case plays out, with margins expanding toward 13.5% on 2 to 3 million units, the stock could be worth multiples of today’s price. The sell-side consensus, at 19 of 25 Buy ratings and a $440 average target, reflects this possibility.

But the bear case does not require Carvana to be a fraud. It requires only that the current valuation, roughly 33x EV/EBITDA and 50x adjusted earnings, is unsustainable when: (a) the profitability it prices in derives an estimated 70 to 80% from a single financing activity under active SEC investigation, (b) the family controlling 84% of voting power has extracted $5.8 billion while a related entity burned $1 billion in cash, (c) EBITDA margins are compressing, not expanding, during a period of explosive growth, and (d) the credit cycle is deteriorating at exactly the moment the company’s loan buyers are becoming more selective. You do not need to believe Gotham City Research on every detail to conclude that this stock is mispriced. You need only believe that a business trading at 50x earnings should not derive the vast majority of those earnings from a single opaque revenue stream controlled by a family with a documented pattern of self-dealing.

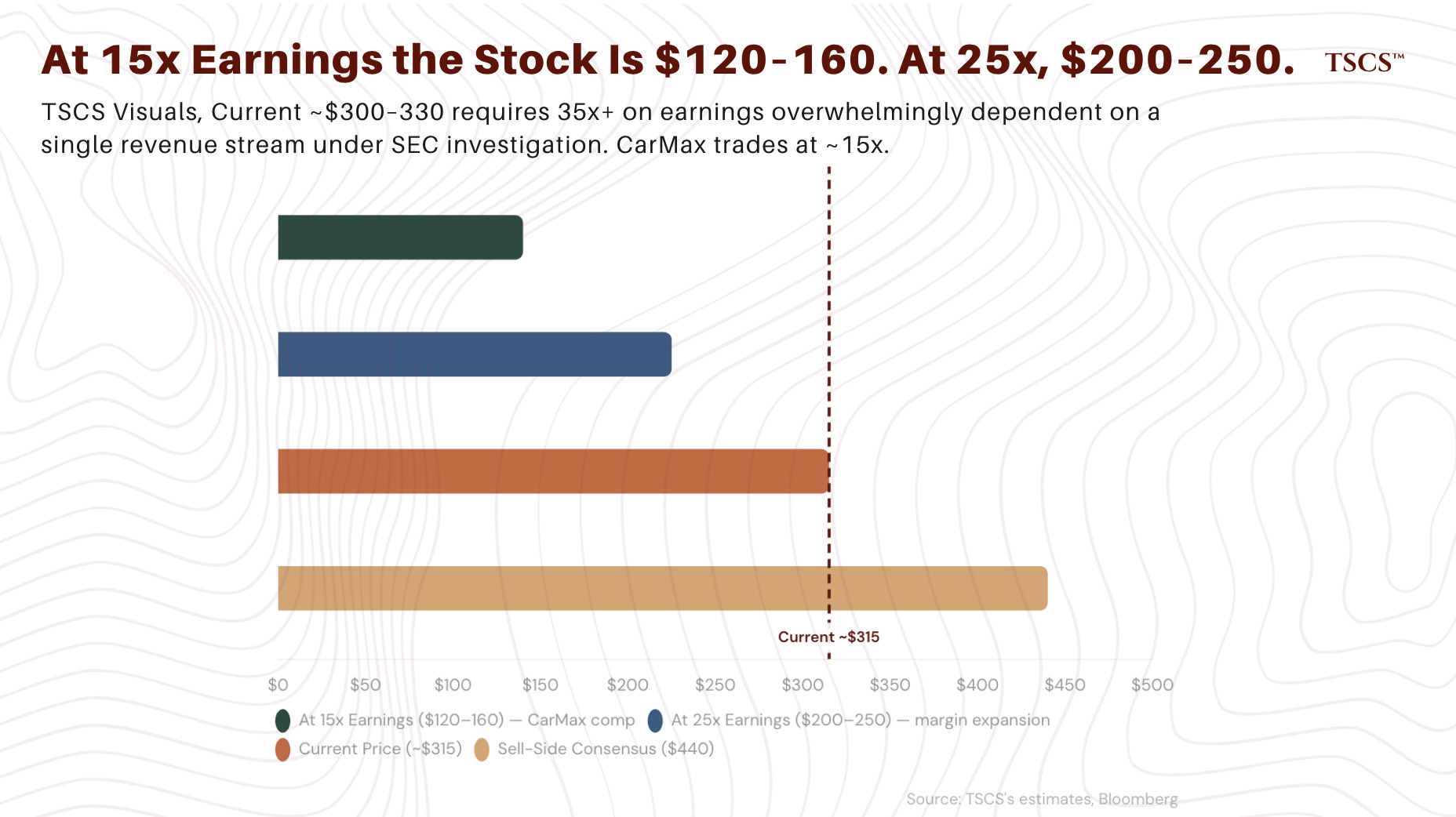

To frame the valuation question concretely: strip out gain-on-sale income and Carvana generated approximately $16 million in Q4 operating profit from its core retail operations. Annualized, that implies the vehicle retail business alone, excluding the financing engine, is earning roughly $64 million pre-tax on a $55+ billion enterprise value, or approximately 860x. Even if you credit the full gain-on-sale stream at face value but apply a 15x earnings multiple (generous for a capital-intensive retailer with 9% EBITDA margins and $4.8 billion in debt), the stock would be valued in the $120 to $160 range. At 25x, which assumes sustained margin expansion and uninterrupted financing income, the range extends to $200 to $250. For comparison, CarMax, the largest traditional used car retailer, trades at roughly 15x P/E. The current price of approximately $300 to $330 requires a 35x+ multiple on earnings that are overwhelmingly dependent on a single revenue stream under active SEC investigation.

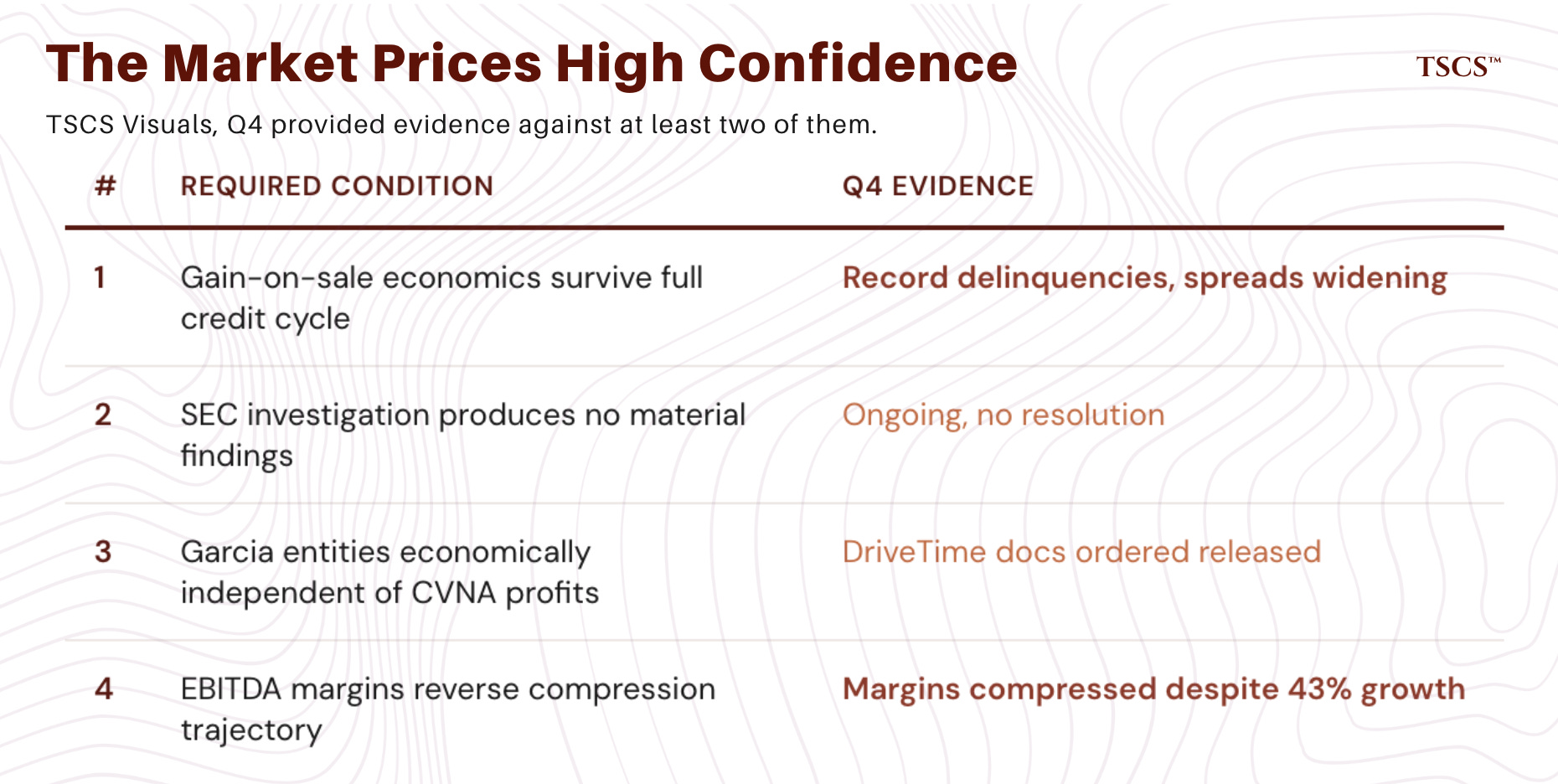

To be explicit about the bull scenario: if Carvana achieves 1.5 million units at 13.5% EBITDA margins (management’s implied long-term target), that produces roughly $4.1 billion in EBITDA. At 15x EV/EBITDA, a premium but not unreasonable multiple for a scaled platform with competitive moats, the equity would be worth $550 to $650 per share after netting debt. At 20x, it approaches $800. The bull case is not irrational; it is genuinely possible. But it requires that gain-on-sale economics remain intact through a full credit cycle, that the SEC investigation produces no material findings, that the Garcia family’s private entities are economically independent of Carvana’s reported profits, and that EBITDA margins reverse their current compression trajectory. The market is pricing in high confidence across all four conditions simultaneously. Q4 provided evidence against at least two of them.

Ernest Garcia II has extracted $5.8 billion from a company whose core retail business generates $64 million a year. He is not confused about what Carvana is worth. The market is.

Appendix:

Incredibly detailed analysis. Great job!

“Pay no attention to the man behind the curtain…”

Great article