Eat The Pension

Private equity bought your annuity, your pension, and the life insurance balance sheet. Apollo shipped the capital to Bermuda.

There is a phrase the consulting industry uses when it explains, to private equity firms, why they should buy life insurers. The phrase is “permanent capital.”

Sit with that phrase. It’s the whole story.

When a private equity fund raises money, the money has a clock on it. Ten years, maybe twelve, then the fund must return capital to its investors. That clock is a constraint. It forces discipline, and discipline costs return.

Life insurance liabilities have no clock. When a 62-year-old retired teacher buys a fixed annuity, that money sits on the balance sheet for the rest of her life and often longer. It cannot be recalled at the discretion of an investor. It cannot be redeemed because of a bad quarter. McKinsey, in the report that launched a thousand acquisitions, called it “an enticing form of permanent capital.”

Notice what it doesn’t say. It does not say “permanently safe.” It does not say “permanently the policyholder’s.” It says permanent capital, and the capital it is describing is the teacher’s. Her money is the permanent thing. The safety she was sold is not.

This piece is about the distance between those two facts. It builds on the open letter Nick Nemeth published to Speaker Johnson in March, which translated a single insurer’s 9,612-page regulatory filing into one number most people had never seen.

We are going to do something narrower and, we think, more alarming. You do not need a leaked document or an investigative source to see the structure. The companies have written it down themselves, in filings any member of the public can pull, and we will read it back to you in their own words.

We name names. Athene. Apollo. Blackstone. We use primary documents, Bloomberg terminal data, and one live, unfolding case, the CDK Global term loan, that sits where the insurance story and the private credit story meet.

If you take one thing from this piece, take this: the most conservative corner of American finance has been quietly rebuilt into something that is not conservative at all, the rebuild is documented in public filings, and the people who will absorb the consequences are the people who were told they had bought safety.

Let us read the filings.

1. The Thing That Used to Be Boring

For most of the last century, life insurance was the most boring business in finance, and boring was the product.

The model was simple. You collect premiums from a large pool of people. Actuaries, using mortality tables refined over decades, tell you with genuine precision how much you will have to pay out and when. You invest the premiums in long-dated, investment-grade bonds whose maturities you match against your expected liabilities. The spread between what the bonds earn and what you owe the policyholders is your profit. It is not a large spread. It was never supposed to be.

The conservatism was not an accident or a failure of imagination. It was the point. A life insurer sells a promise that comes due in thirty or forty years. The entire value of the promise is the credibility of the institution making it. The boring balance sheet was the asset.

That industry still exists. The mutual insurers, owned by their policyholders rather than by shareholders, still largely run the old model. New York Life, Northwestern Mutual, MassMutual. No stock price to manage, no quarterly earnings call, no activist investor. They are the Green Bay Packers of American finance, and they remain, by some distance, the most conservative balance sheets in the country.

Around 2009, a different kind of owner discovered the life insurance balance sheet. It had a different idea.

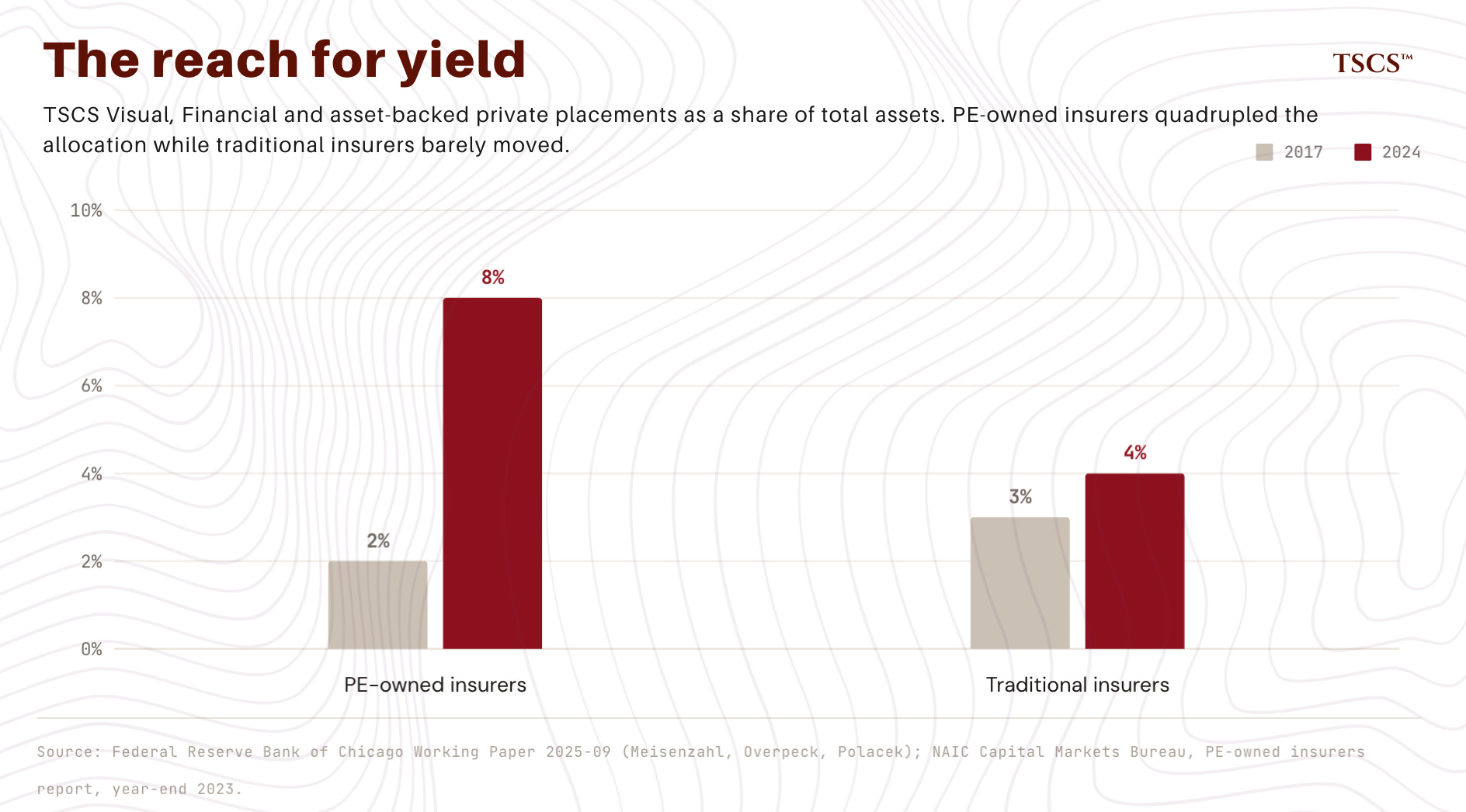

The idea was this. The conservative bond portfolio that a traditional insurer holds looks lazy. It earns a modest, safe yield. But what if you replaced the conservative portfolio with higher-yielding assets? Private credit. Collateralized loan obligations. Structured products. Asset-backed finance. The liabilities stay the same, the cost of funding stays the same, but the asset side now earns several hundred basis points more. That incremental spread, multiplied across a balance sheet of hundreds of billions of dollars, is an enormous and durable stream of profit.

And the assets you replace the bonds with can be assets that your own firm originates and manages, which means you collect a second stream of income: the management fees.

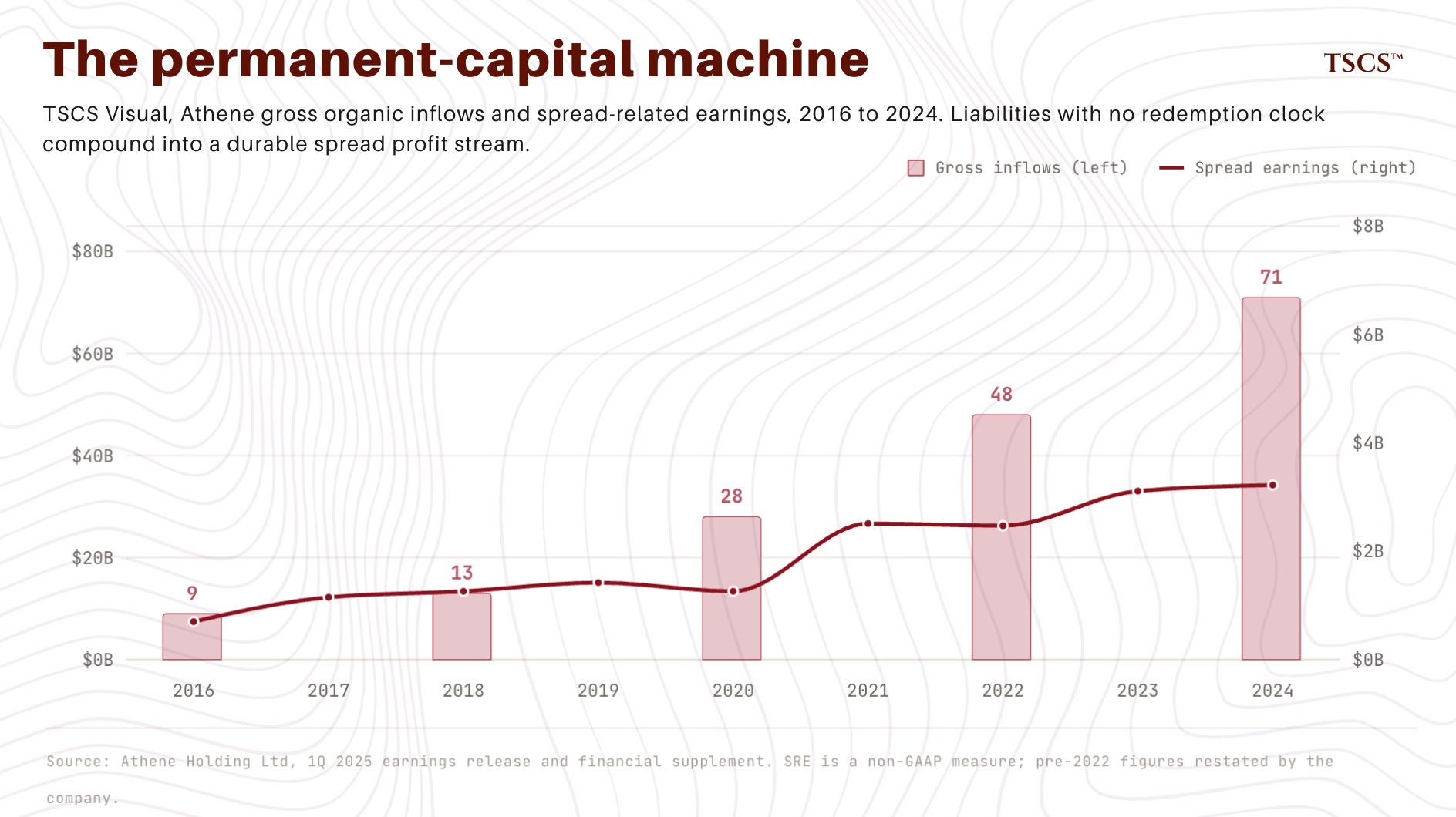

This is the trade. Buy the insurer, keep the permanent capital, swap the boring assets for assets you manufacture yourself, and collect the spread and the fees. Athene, the vehicle that executed this trade most completely, did not exist in its current form fifteen years ago. It now manages a larger general account than Prudential.

The standard objection at this point is that there is nothing wrong with an insurer earning a higher yield, and that objection is correct as far as it goes. Higher-yielding assets are not, in themselves, a scandal. The question is never the yield. The question is always what you gave up to get it, whether the people relying on the institution understand the trade, and what happens to the structure under stress.

Athene has been the most willing to show its work. What it has shown is, in our view, one of the most important disclosures in the industry, and it has had nothing like the attention it deserves.

2. What Athene Told the SEC

Athene Annuity and Life Company is the United States operating insurer inside Athene, which is in turn owned by Apollo Global Management. It is the entity that issues the annuities. It is the entity that holds the promises.

Buried in Athene’s 10-K, in the section on reinsurance, is the following sentence. The exact words matter.

“Subject to quota shares generally ranging from 80% to 100%, substantially all of the existing deposits held and new deposits generated by Athene’s U.S. insurance subsidiaries are reinsured to its Bermuda reinsurance subsidiaries.”

Read it slowly. “Substantially all” of the deposits. The existing ones and the new ones. Reinsured, meaning transferred, to the company’s own Bermuda subsidiaries. At a quota share that runs as high as 100%.

In plain English: when an American buys an annuity from Athene’s US insurer, the money does not stay at the US insurer in any meaningful sense. It is shipped, very nearly in its entirety, to a reinsurance company in Bermuda that the same parent owns. The US entity becomes something close to a pass-through. It collects the premium, books the liability, and reinsures the economics offshore.

The next sentence in the filing tells you why.

“As a result of its internal reinsurance structure and third-party direct to Bermuda business, a significant majority of Athene’s aggregate capital is held by its Bermuda reinsurance subsidiaries.”

The capital is in Bermuda. Athene is telling you this directly. Not most of the assets. The capital, which is to say the buffer, the surplus, the thing that stands between a promise and a broken promise.

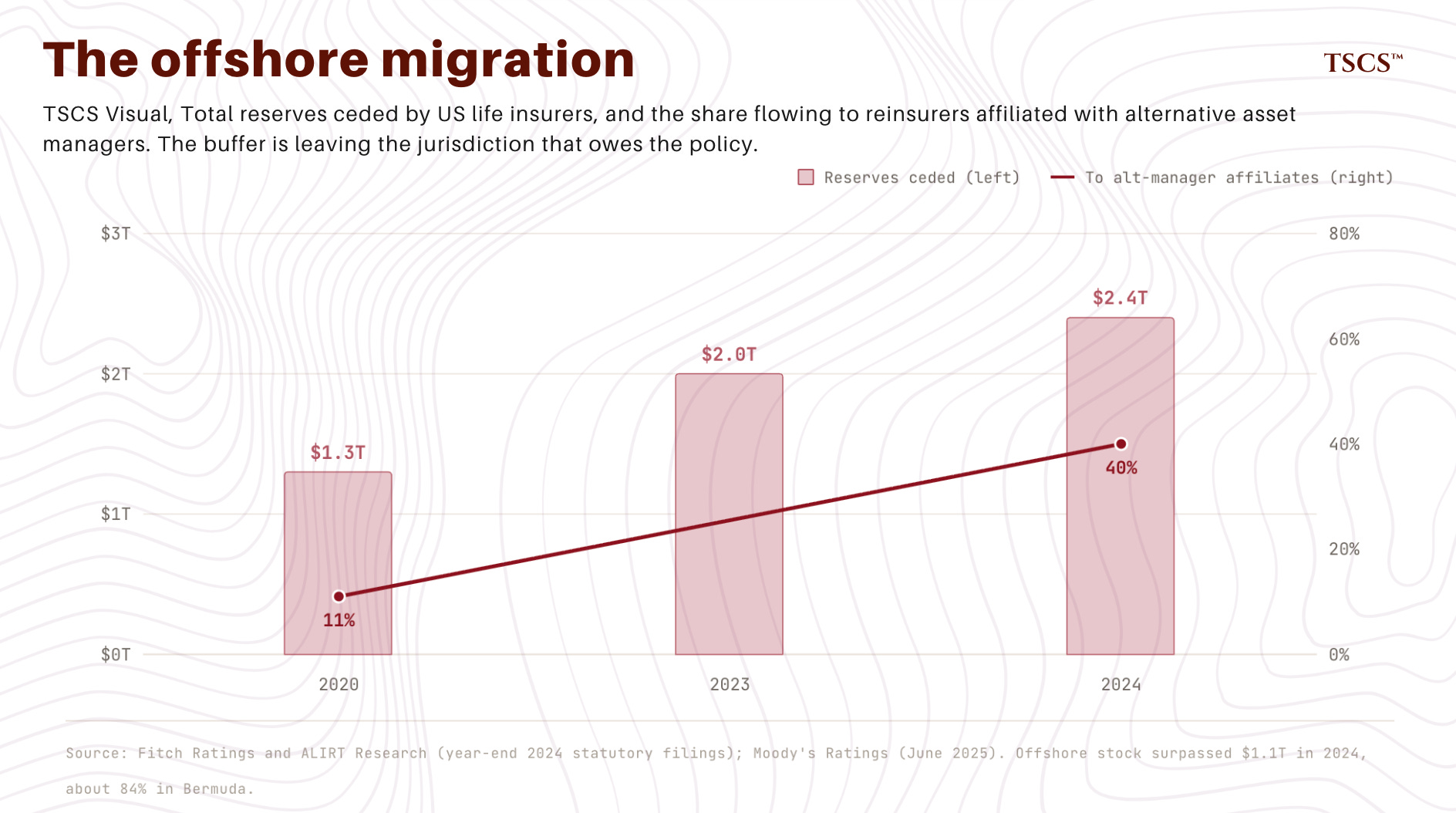

The distinction that sounds technical, and is in fact the entire point: insurance regulation is local. When an insurer fails, it does not fail as a global consolidated enterprise. It is seized and wound up by the regulator of the jurisdiction in which the failing entity is domiciled, against the assets legally available to that entity. Athene’s annuity contracts, by Athene’s own disclosure, are the obligation of the issuing US insurer. The capital, by the same disclosure, is largely in Bermuda.

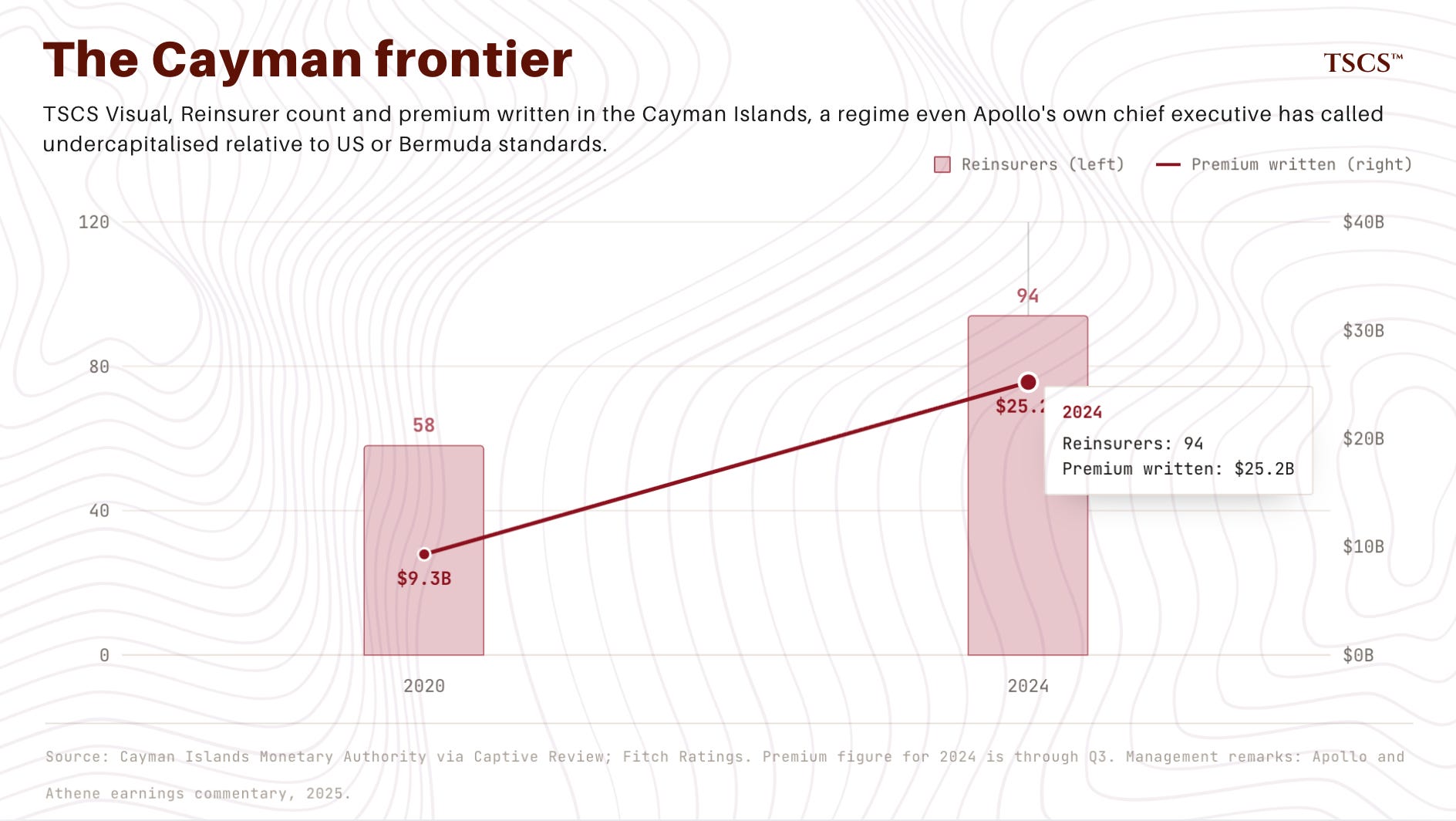

Bermuda is not a secret and it is not, in itself, a crime. It is a sophisticated, well-regulated jurisdiction with a competent monetary authority. But Bermuda’s solvency regime is not the United States’ solvency regime. Athene’s own filing says it applies the same reserving principles in Bermuda as in the United States, and we take that at face value: the concern here was never reserving. It is capital treatment, and above all public disclosure, where the gap is dramatic. Nemeth’s letter put the disclosure gap in concrete terms: Athene’s US entity files a statutory return of more than nine thousand pages. Its Bermuda entity files eight. The ratio of disclosure between the entity that owes you the money and the entity that holds the capital is roughly twelve hundred to one.

A third actor is named in the same passage of the 10-K: ACRA, the Athene Co-Invest Reinsurance Affiliate. Remember it. ACRA is a sidecar. It allows third-party investors to put capital alongside Athene inside the reinsurance structure. Those third-party investors have their own economics and their own exit rights, and they have no statutory obligation to the US policyholder. We will come back to what that means.

While we are in the 10-K, one more sentence, from the section on ratings. Athene notes, revealingly, that financial strength ratings “are based upon factors of concern to policyholders, agents, intermediaries and ceding companies and are not directed toward the protection of investors.”

We’d push that further. The “A+” on the door is a signal calibrated for the comfort of the people buying the product. It is not, and was never designed to be, a measurement of the distance between this balance sheet and an adverse outcome.

Nemeth’s letter set out to make that measurement, and Athene’s own filings make it easy. As of year-end 2025, Athene’s US insurance companies, the entities that issue the annuities and legally owe the money, held $9.5 billion of total adjusted capital and reported a risk-based capital ratio of 436%. The ratio sounds like a fortress. It reads that high only because the requirement it is measured against is tiny: the risk charges the formula applies to a 97% investment-grade bond book come to a fraction of one percent of assets, so 436% is more than four times a very small number.

And the $9.5 billion sits at the wrong end of the structure. As Athene itself disclosed above, a significant majority of the group’s capital is in Bermuda: the filings show $18.6 billion of statutory capital in the Bermuda reinsurers against $9.5 billion in the US companies that actually owe American annuitants.

None of this is alleged. None of it is leaked. It is the company’s own description of its own structure, filed with the Securities and Exchange Commission, available free to anyone who wants to read it. The scandal, if there is one, is not that the structure is hidden. It is that it is disclosed in plain sight, and almost no one outside the regulators and a handful of specialists reads the disclosure.

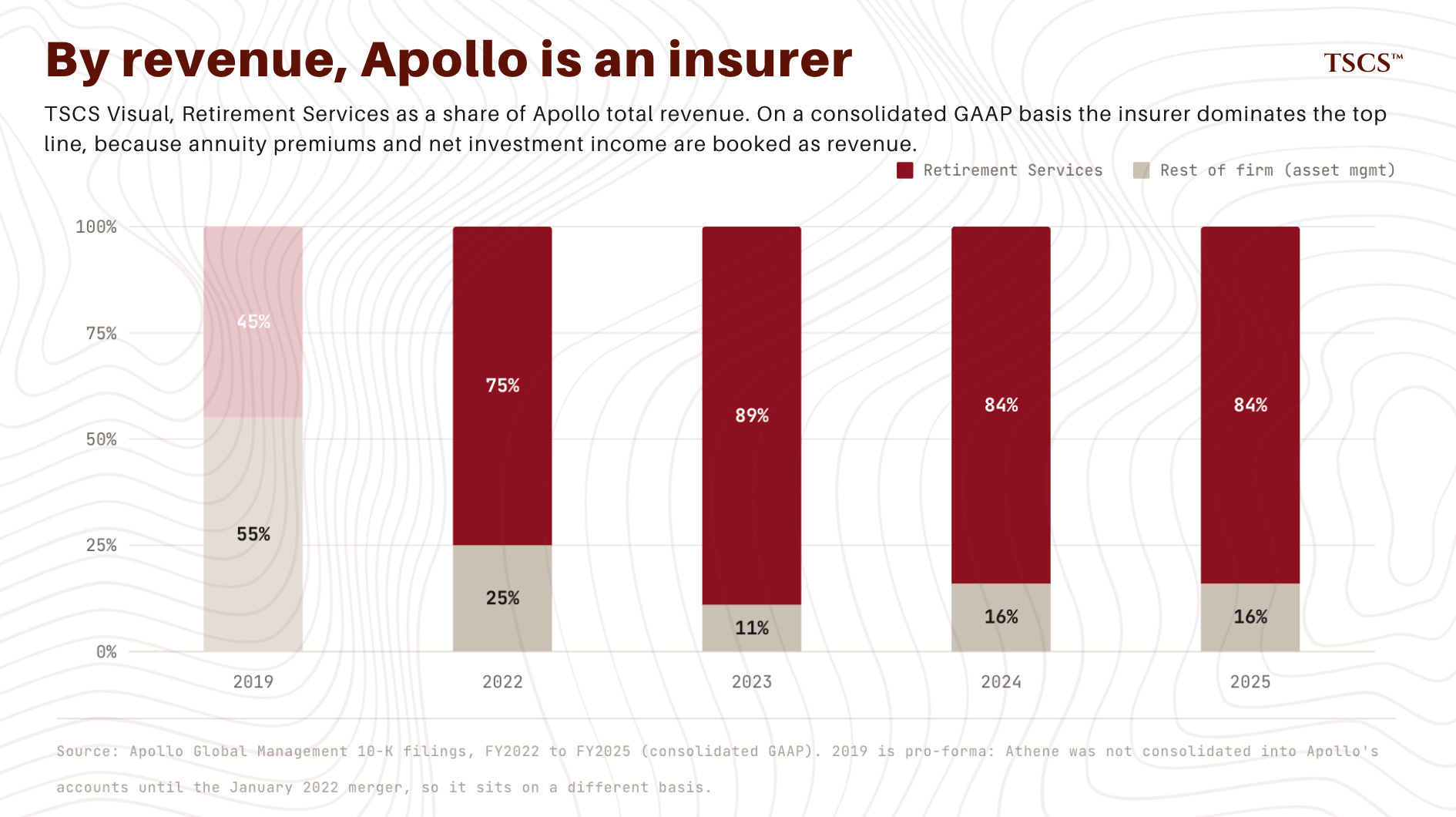

3. Apollo Is Not a Private Equity Firm

Apollo Global Management is described, by the financial press and by itself, as one of the three or four largest private equity firms in the world. One table retires that description.

It is the segment breakdown of Apollo’s own revenue, pulled straight from the terminal.

Here’s the number. In 2025, Apollo’s most recent full year, the Retirement Services segment, which is to say Athene, the insurance business, was 84% of Apollo’s total revenue, $27.0 billion of a $32.0 billion total. The figure is straight from Apollo’s own 10-K, and it is not a one-year artifact: in 2023 it was 89%.

Two honest qualifications. First, this is revenue, and revenue flatters an insurer: consolidated accounting books gross premiums and gross investment income at the top of the income statement, against large policy-benefit expenses recorded below it. On Apollo’s own preferred non-GAAP segment metrics, which weight recurring fee earnings differently, the asset-management business looks larger and the split is less lopsided, though insurance is still the bigger half. Second, cutting the other way: on GAAP pre-tax income the tilt is sharper, not gentler, with Retirement Services accounting for the overwhelming majority of what Apollo earned before tax in 2025.

Choose whichever lens you find fairest. On none of them is Apollo, today, primarily a private equity firm. It is first a life insurance and annuity company, and the asset-management business the world still calls “Apollo” is the smaller half.

This isn’t a criticism. It’s a correction of a category error, and the error changes the question you should ask. Nobody is especially alarmed when a private equity firm takes risk. Risk is the job. Limited partners in a buyout fund are sophisticated, they are compensated for the risk, and they can lose their entire investment without anyone calling it a crisis. That is the deal.

An annuitant did not sign up for that deal. The retired teacher with the fixed annuity is not a limited partner. She was not sold an exposure to private credit spreads. She was sold a contractually guaranteed stream of payments by an institution rated A+. The marketing said safety. The structure, as we have just read in the filings, says something else.

The same shape, with different timing, shows up across the industry’s new owners. KKR, through Global Atlantic. Carlyle, through Fortitude Re. Brookfield, through Brookfield Reinsurance and American National. Blackstone, through its stake in Corebridge and the management of large insurance mandates. The asset managers did not all enter insurance at the same moment, but they all entered, and they all entered for the same reason: the permanent capital. The McKinsey report did its job.

4. The Wall

There are two ways money arrives on a life insurer’s balance sheet.

The first is the obvious one: policyholders pay premiums. Annuity deposits. That money is genuinely long-dated and genuinely sticky, and it is the money the “permanent capital” thesis is actually about.

The second is less visible and, for our purposes, far more interesting. Modern insurers, including the traditional ones, also raise money in the wholesale debt markets through vehicles called funding agreement backed notes. A funding agreement is, in effect, an institutional deposit with the insurer. The insurer bundles funding agreements into notes and sells the notes to bond investors all over the world. The proceeds get invested alongside everything else, earning the spread.

Funding agreement backed notes are not exotic and they are not, in isolation, sinister. MetLife has used them for decades. But they have one characteristic that annuity deposits do not, and the characteristic is the whole of this section: they have a maturity date. They are debt. They come due. And when they come due, the insurer must either pay them off or, far more commonly, refinance them by issuing new notes.

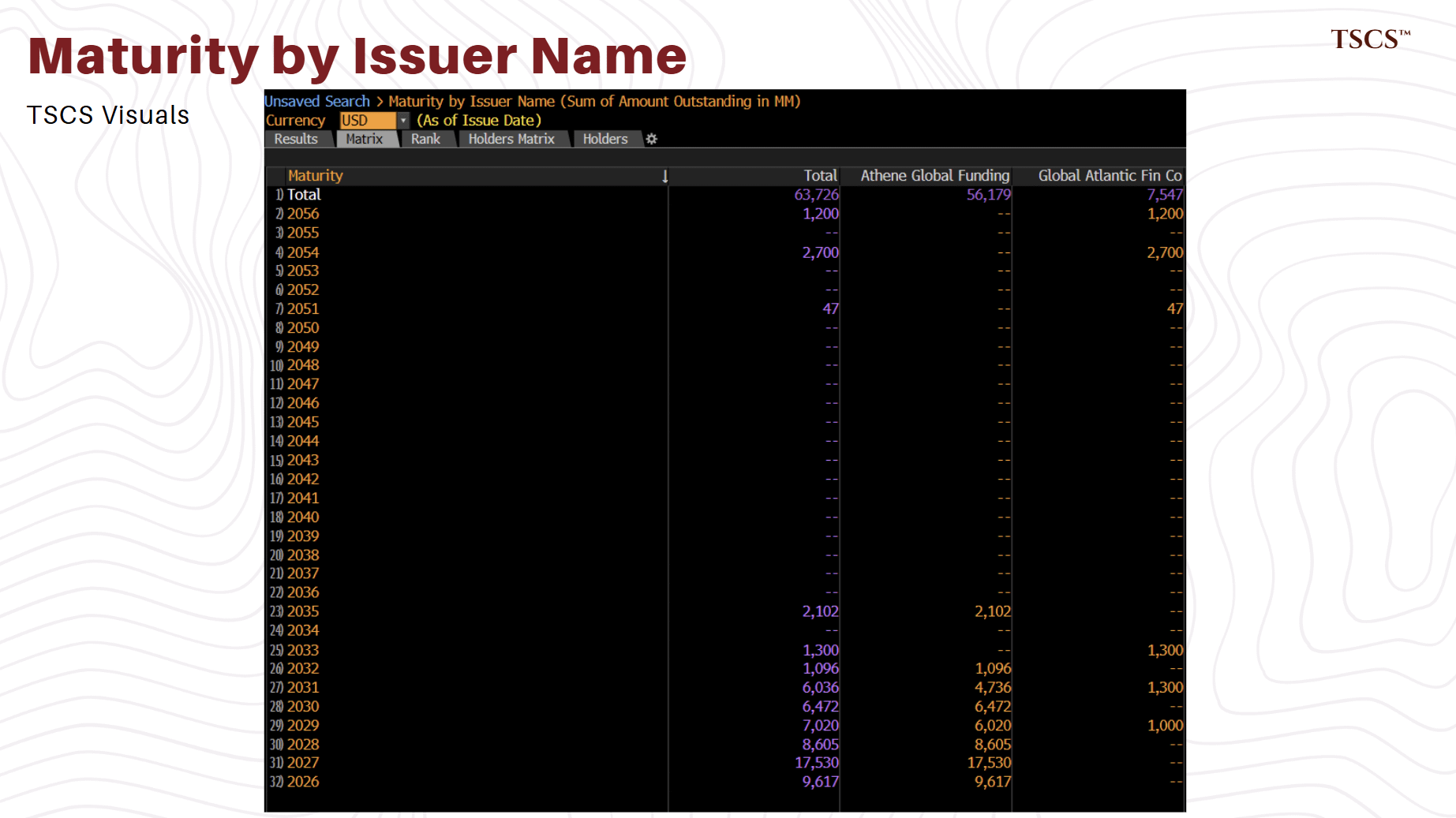

We pulled Athene’s funding agreement program off the terminal and laid out its maturity schedule.

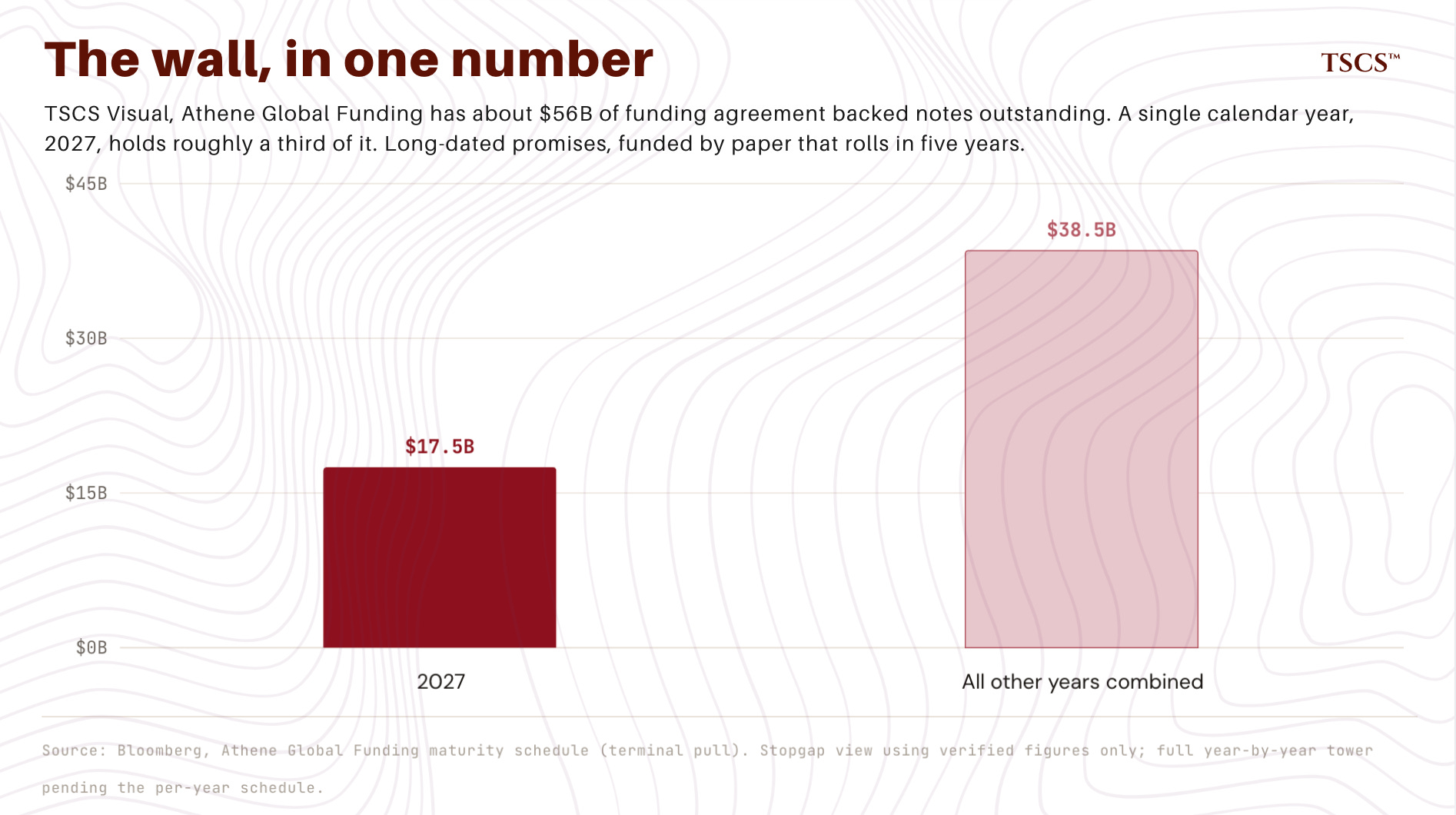

Across its maturity-dated wholesale funding, Federal Home Loan Bank advances, the FABN medium-term-note program issued through Athene Global Funding, the FABR repurchase program, and direct funding agreements, Athene had roughly $90 billion outstanding as of March 2026. The FABN notes this section opened with are $34.5 billion of that. The FABR program, repo-based funding raised through special-purpose entities, is another $21.5 billion; together those two programs total about $56 billion. Now look at when they come due. This is not a smooth ladder spread evenly across decades. It is a wall. The single largest maturity year is 2027, and in 2027 alone, approximately $17.5 billion comes due. That is close to a third of the entire program landing inside one calendar year. The bulk of the rest lands in the handful of years on either side of it.

Hold that next to a fact from Section 1. The liabilities this balance sheet exists to support, annuities and pension obligations, run ten, twenty, thirty years and longer. A meaningful slice of the funding behind those decades-long promises rolls over inside the next five years, and a third of it inside one.

This is the oldest and most dangerous shape in finance. Borrow short, lend long. Fund long-dated, illiquid assets with short-dated money that has to be refinanced. It works, beautifully, for as long as the refinancing market stays open. It is precisely, mechanically, what failed at Silicon Valley Bank: long-duration assets, funded by liabilities that turned out to be far less stable than the model assumed, and a forced sale into a falling market the moment the funding ran.

Three honest caveats.

First, funding agreement backed notes are not retail deposits. They are held by institutional investors, and institutional investors do not “run” in a literal panic the way retail depositors did at SVB. The failure mode is slower and quieter. It’s a refinancing that gets harder, then more expensive, then, in a genuinely bad credit environment, unavailable on workable terms.

Second, Athene isn’t unique, and it isn’t even the most aggressive user of this funding. MetLife’s comparable program is larger. Corebridge, Global Atlantic, Equitable, Prudential’s Pricoa vehicle, Brighthouse, and American National all run the same structure. This is an industry-wide funding model, not an Apollo invention. That cuts in Athene’s favor and we say so plainly.

But it also cuts the other way, and this is the part the industry would prefer you did not dwell on. If the wholesale funding market for insurance paper seizes, in a 2027 that happens to coincide with a credit downturn, it does not seize for one issuer. It seizes for the asset class. Every name on that list refinances into the same closed window at the same time.

Third, the difference that matters between these issuers is not the funding. It is the asset side. MetLife funds short and lends long too, but MetLife lends into a relatively conservative, relatively liquid book. The question is what happens when an insurer funds short, lends long, and lends into a book of private credit and structured assets that does not trade, cannot be sold quickly, and is carried on the books at a value the market never gets to vote on.

That is the next section.

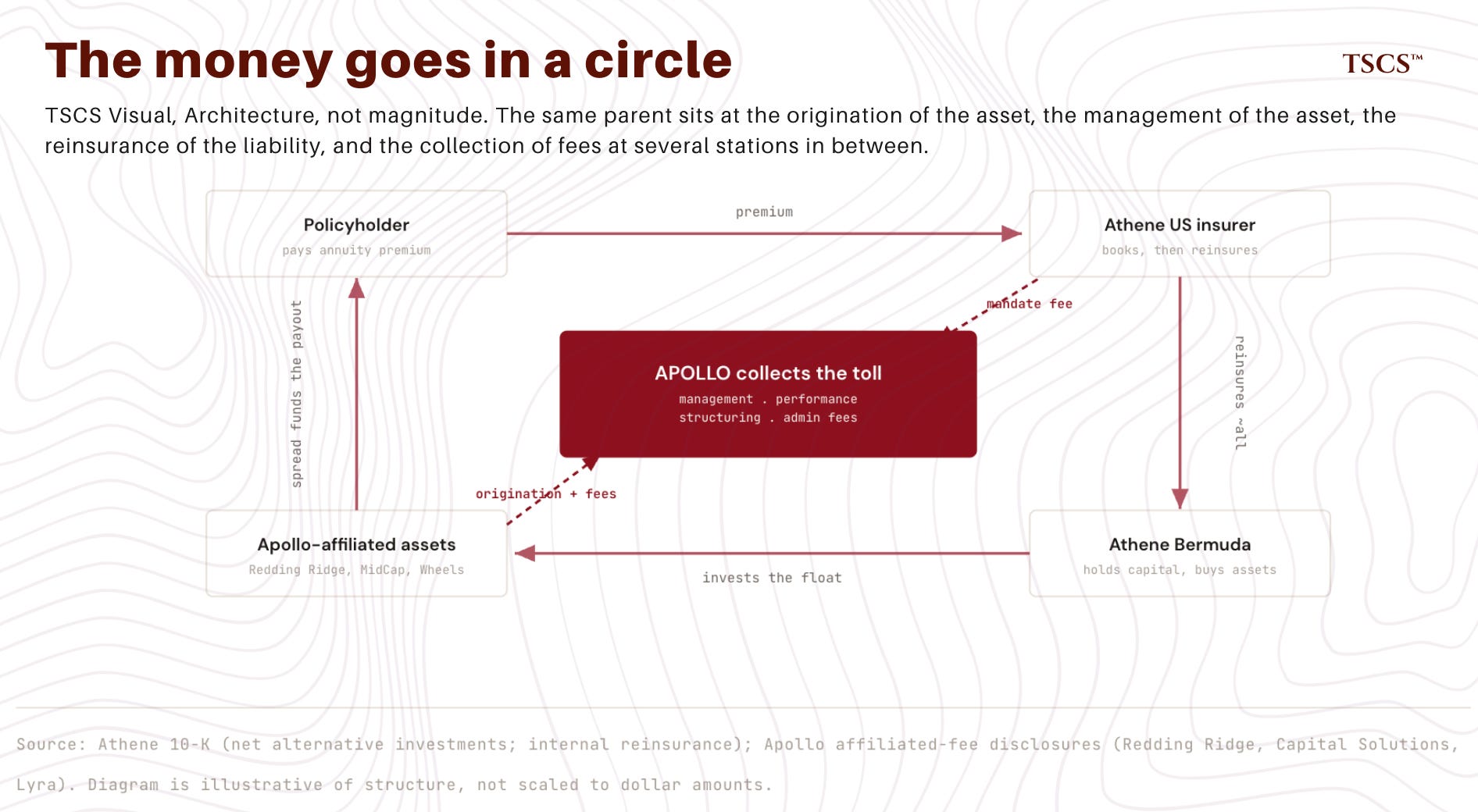

5. The Money Goes in a Circle

What the insurer actually buys with all this money is, again, in its own filings.

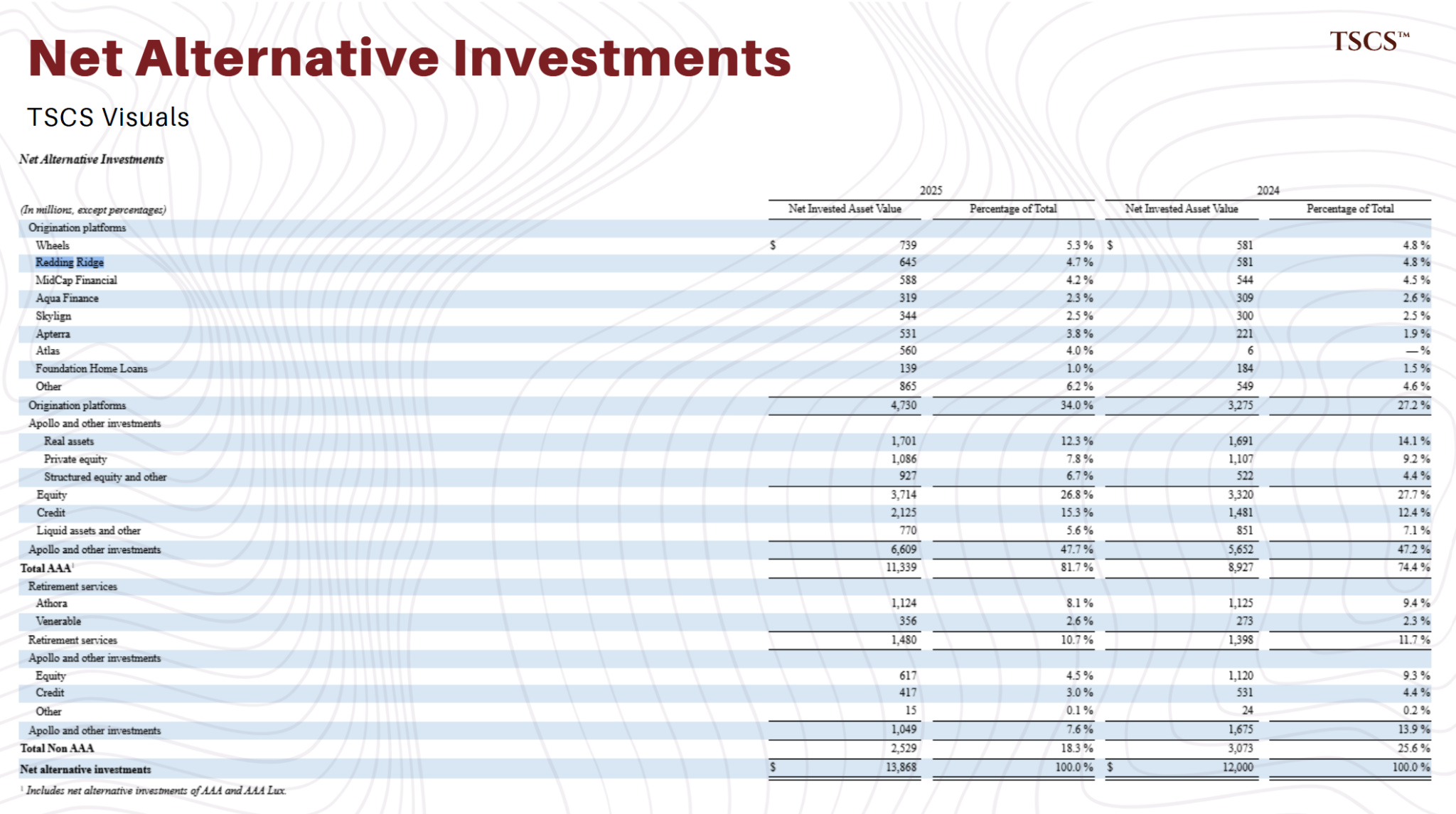

Athene’s 10-K breaks out a category it calls net alternative investments. At year-end 2025 it totaled roughly $13.9 billion.

The list: origination platforms with names like Wheels, MidCap Financial, Apterra, Atlas, Foundation Home Loans. A line called, simply, “Redding Ridge,” at $645 million. And then a large block, nearly half the total, labeled “Apollo and other investments.”

The structure: Athene, the insurer, is invested in a set of platforms and funds. A great many of those platforms and funds are originated, managed, or affiliated with Apollo, the parent. The insurer’s “alternative investments” are, to a substantial degree, Apollo products.

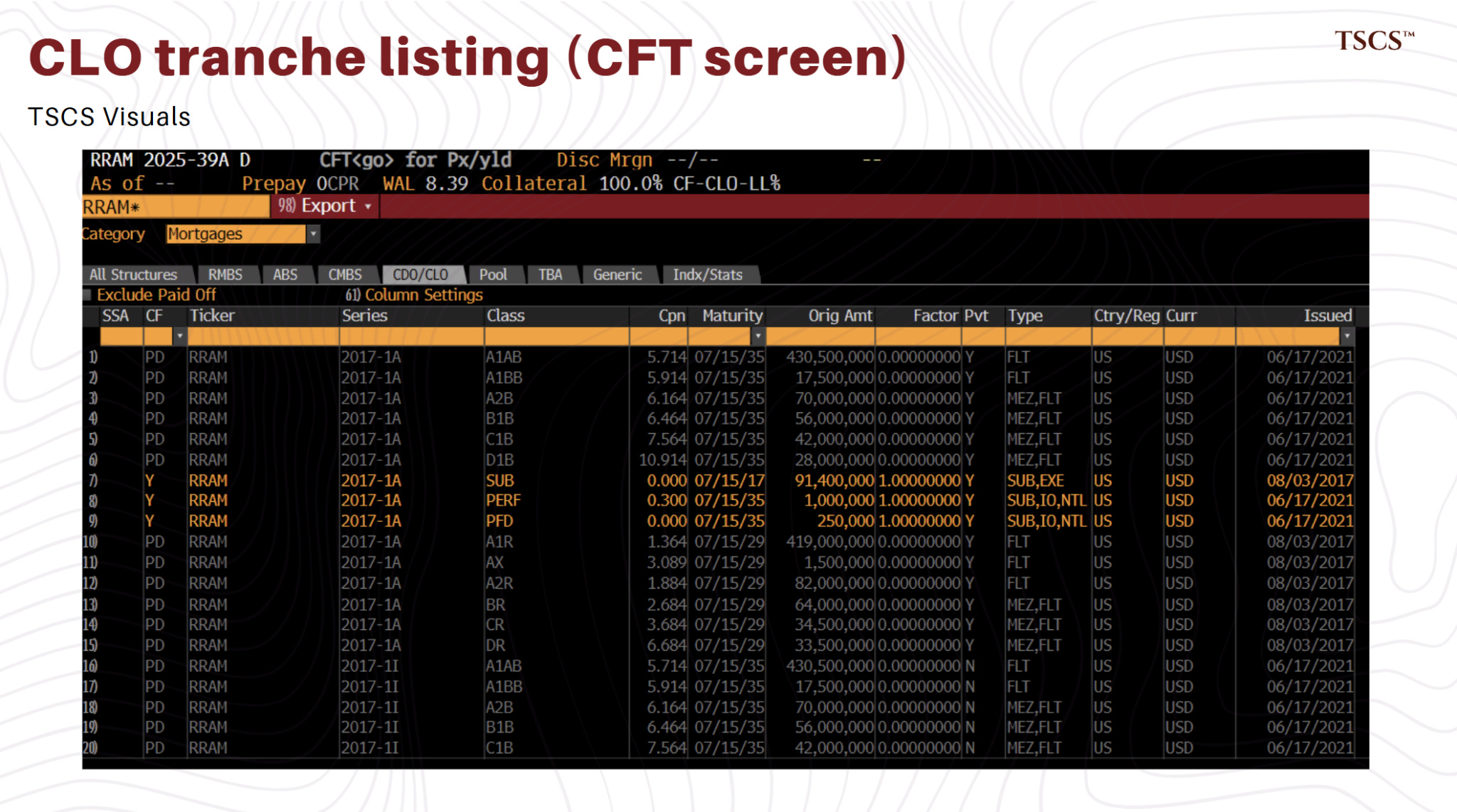

Follow Redding Ridge. It’s the cleanest illustration. Redding Ridge is an Apollo-affiliated manager of collateralized loan obligations. Athene holds $645 million of it. And in a separate part of the filings, Apollo discloses what Redding Ridge does with the relationship.

The disclosure states that Redding Ridge made payments to affiliates of the Operating Manager for management and performance fees, and for credit research and administrative fees. The Operating Manager’s affiliate is Apollo. There are parallel disclosures for collateral management fees, for “Capital Solutions” fees on asset-backed finance, and for a separate Apollo-affiliated client services platform called Lyra.

Trace the dollar. A retired teacher pays a premium to Athene’s US insurer. Substantially all of it is reinsured to Athene’s Bermuda subsidiary. The Bermuda balance sheet invests in, among other things, Apollo-affiliated vehicles like Redding Ridge. Those vehicles pay management fees, performance fees, structuring fees, and administrative fees to Apollo affiliates. The teacher’s premium has become an asset. It generates a spread for the balance sheet, and a toll, collected by the parent, at multiple points along its path.

The individual fee amounts disclosed in any single quarter are not, on their own, enormous numbers. Some of them are surprisingly small. The point is not the size of any one toll. The point is the architecture. The same parent sits at the origination of the asset, the management of the asset, the reinsurance of the liability the asset funds, and the collection of fees at several stations in between. Apollo is on every side of the table.

This is the part the word “extraction” is reaching for. The fees are not hidden. They are disclosed, quarter after quarter, in the filings. But they are disclosed in a hundred different footnotes across thousands of pages, and a structure disclosed in a hundred footnotes is, for any practical purpose, a structure that has not been disclosed at all.

There is one more property of this asset side that does more work than any fee. The assets do not trade. And because they do not trade, the value of them is, to a degree most people do not appreciate, a matter of opinion.

6. The Opacity Is the Product

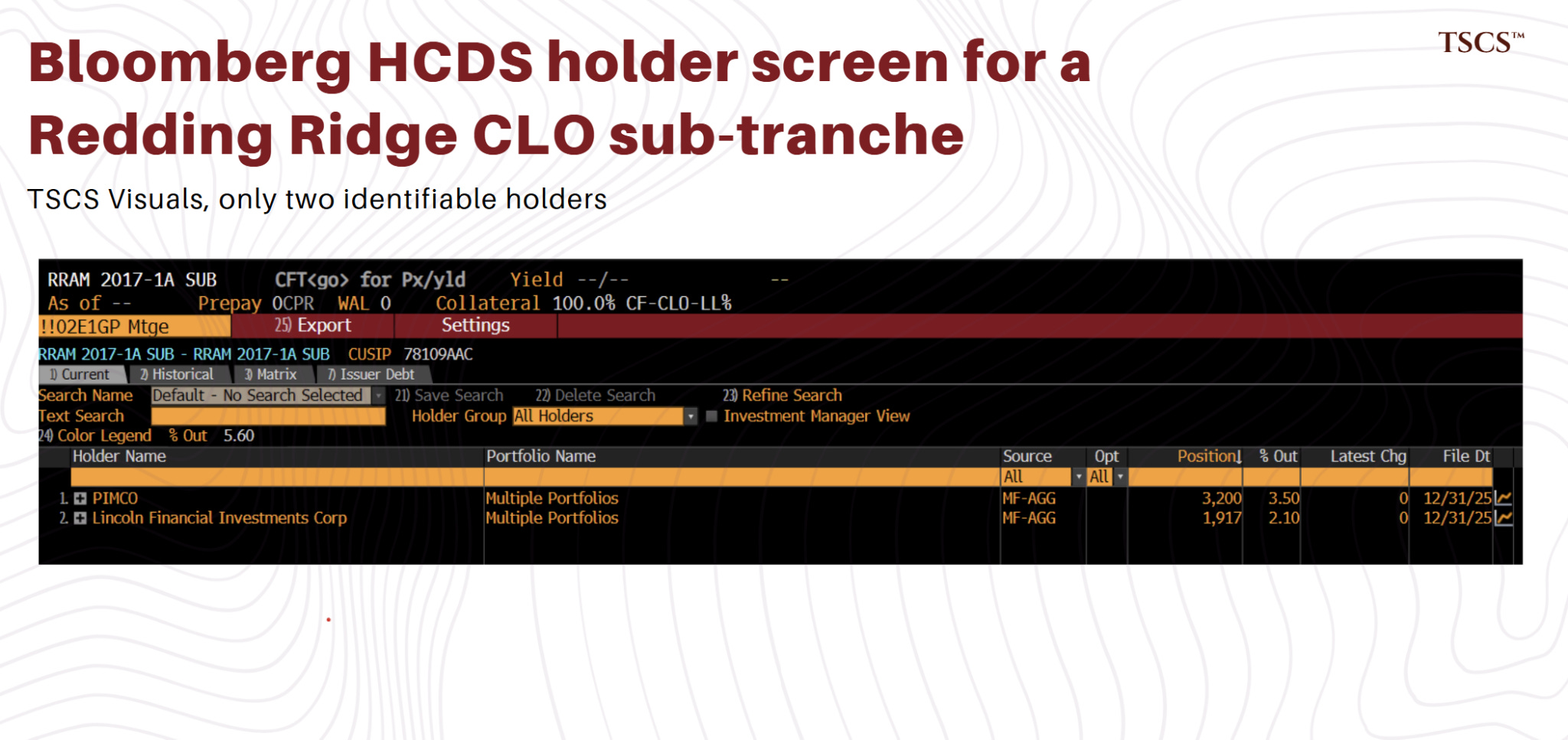

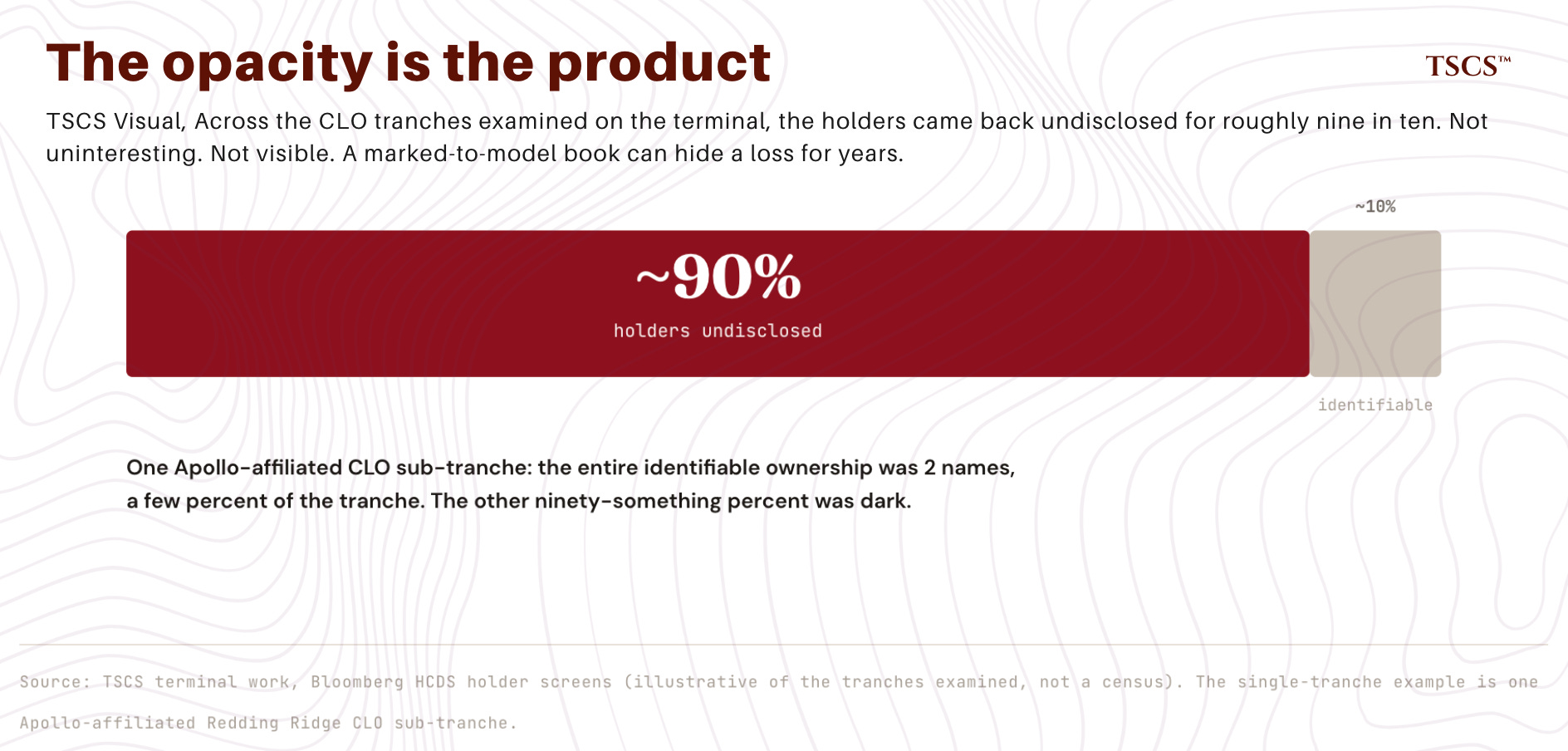

The terminal work turned up something we didn’t expect. On reflection, it’s the quiet center of this whole story.

We went looking for the holders of specific collateralized loan obligations, the structured credit instruments that sit on these balance sheets. The Bloomberg function for this, HCDS, shows you who owns a given security. We ran it across a range of CLO tranches.

For the large majority of the tranches we examined, roughly nine in ten, the holders came back as undisclosed. Not “held by someone uninteresting.” Undisclosed. The ownership is simply not visible.

When we did get a result, it was thin. On one Apollo-affiliated CLO sub-tranche, the entire identifiable ownership was two names, together a few percent of the tranche. The other ninety-something percent was dark.

The instinct, when you see this, is to treat it as a data limitation. A gap in the terminal’s coverage. It is not a gap. It is the design.

Three different things are at work here, and the industry’s defenders will, fairly, attack anyone who runs them together. First, “privately placed” describes how a bond was sold, directly to institutions rather than into the public market, not how risky it is. A private placement trades less, but it is not by definition unrated or unreviewed.

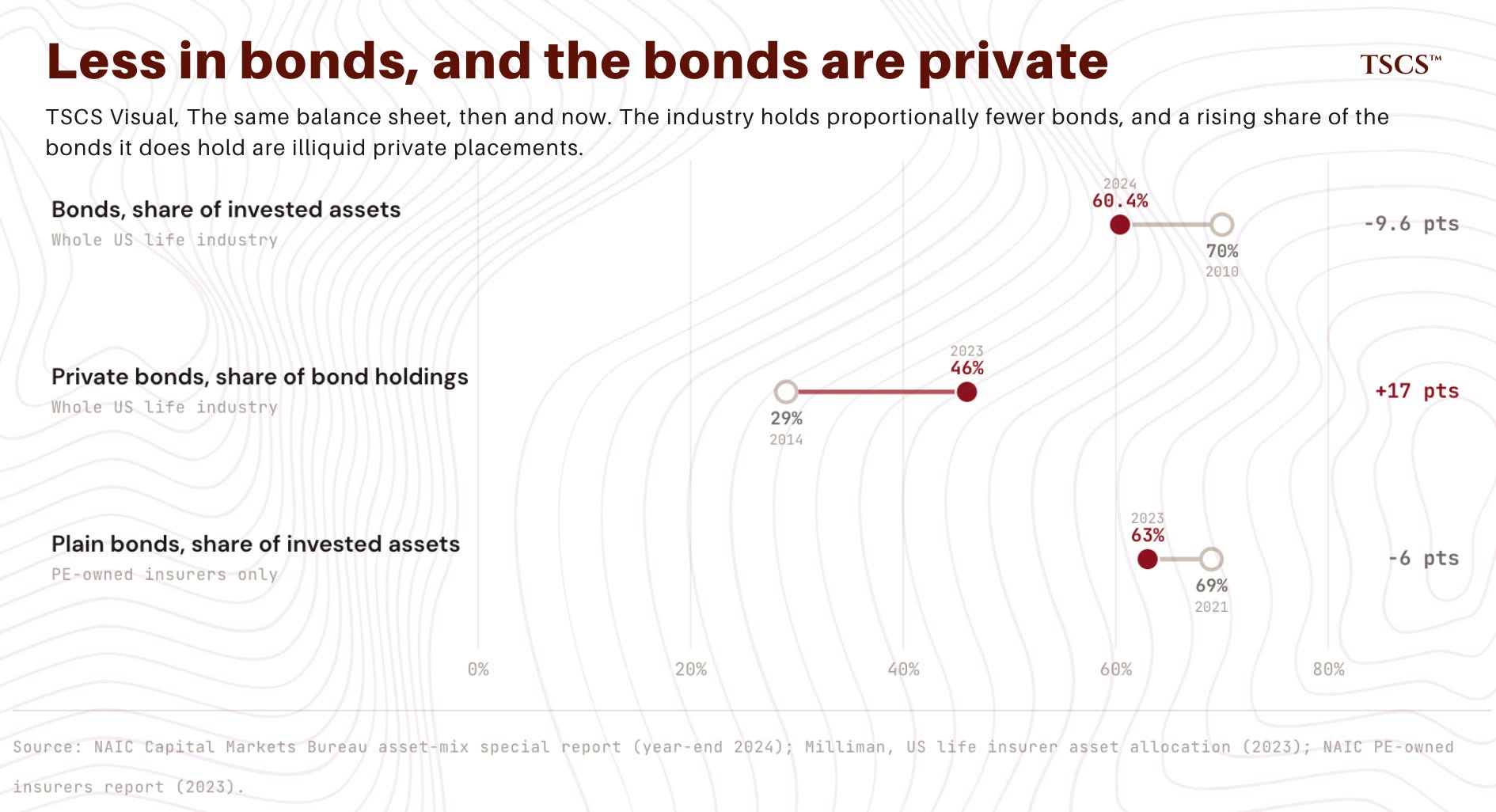

Second, valuation. A security without an active market is still assigned a fair value, and that value is graded: Level 2 when the inputs are observable, such as a price from a third-party service, Level 3 when it rests on significant unobservable inputs and management judgment. Most of an insurer’s non-public bonds are Level 2; a meaningful tail is Level 3. Level 3 does not mean fraudulent. It means the number is an estimate whose inputs an outsider cannot independently check.

Third, accounting basis. In the statutory filings that drive an insurer’s solvency assessment, most bonds are carried at amortized cost regardless of fair value, so until an instrument is formally impaired, a decline in its market value need not pass through the statutory balance sheet at all. The 10-K’s GAAP balance sheet marks more of the book; the statutory balance sheet, the one that decides whether the company is deemed solvent, marks less.

Stack the three together: a privately placed, Level 3, amortized-cost asset is one that does not trade, is valued by a model the manager influences, and is carried for solvency purposes at a number that does not move when the market’s opinion of it moves. Not every private asset is all three. The ones that are all three are where the gap between carried value and realizable value can widen quietly, for years, before anything forces the question.

This is the same accounting treatment, applied to a portfolio many multiples larger, that allowed Silicon Valley Bank to carry underwater securities at a value that bore no relationship to what they would fetch, right up until the moment it was forced to find out.

Nemeth’s letter established that roughly 72% of Athene’s bond portfolio is privately placed. A large share of those private placements are valued against a model rather than a market price, and a model’s output is, in a sense the public is not invited to examine, an opinion. And the rating that determines the capital charge against that opinion is frequently supplied by a small ratings agency, paid by the issuer, processing private credit ratings at a volume that works out to roughly one rating per analyst per business day.

So when we say the opacity is the product, we mean it almost literally. The inability to see the price is not a side effect of the private credit model. It is a feature the model requires. A marked-to-market book cannot hide a loss. A marked-to-model book can hide a loss for years, and “for years” is exactly long enough for the fees to be collected and the architects to be gone.

Occasionally an instrument inside this opaque universe is forced into the daylight. We have a live one.

7. A Live Fire Test: CDK Global

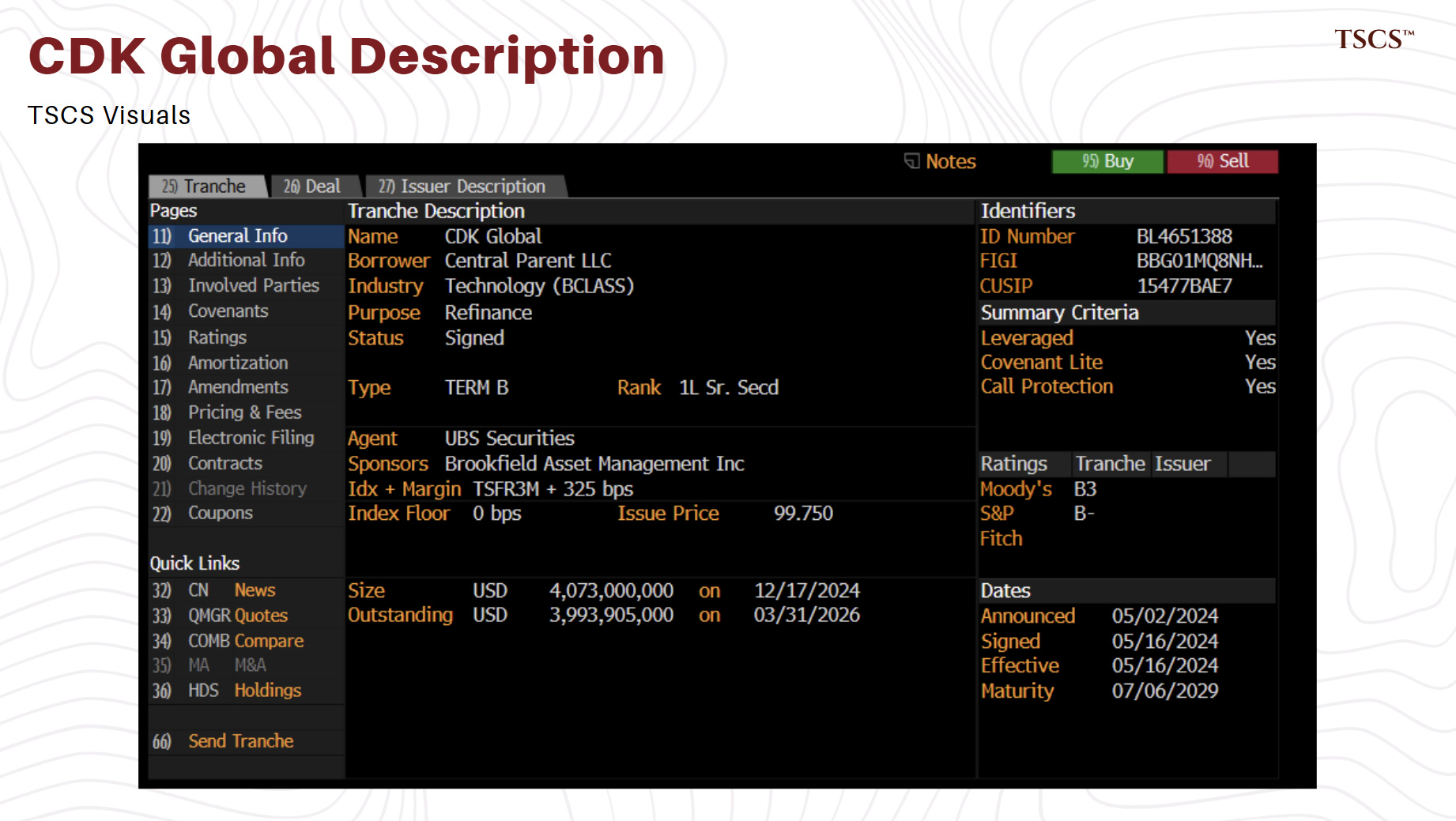

CDK Global is a software company. It provides the systems that car dealerships run on. In 2022 it was taken private by Brookfield, the asset manager, in a leveraged buyout. The buyout was funded, as buyouts in that era were, substantially with a large floating-rate term loan: roughly $4 billion, first-lien, maturing in 2029.

That loan is the kind of instrument that lives, in pieces, on the balance sheets of insurers, private credit funds, and the retail-facing vehicles those firms sell to the public. And right now, that loan is under visible stress.

In April 2026, the ratings agency Fitch added the CDK loan to its list of loans of concern. CDK’s earnings had deteriorated sharply. And then, on 22 April 2026, Bloomberg reported something that does not happen to healthy loans: a group of CDK’s largest creditors signed a cooperation agreement. A cooperation agreement is the choreography that precedes a restructuring. It binds creditors to act as a bloc. You do not sign one unless you expect a fight over the remains. The reported signatories included three of the largest names in credit: PIMCO, BlackRock, and Blackstone.

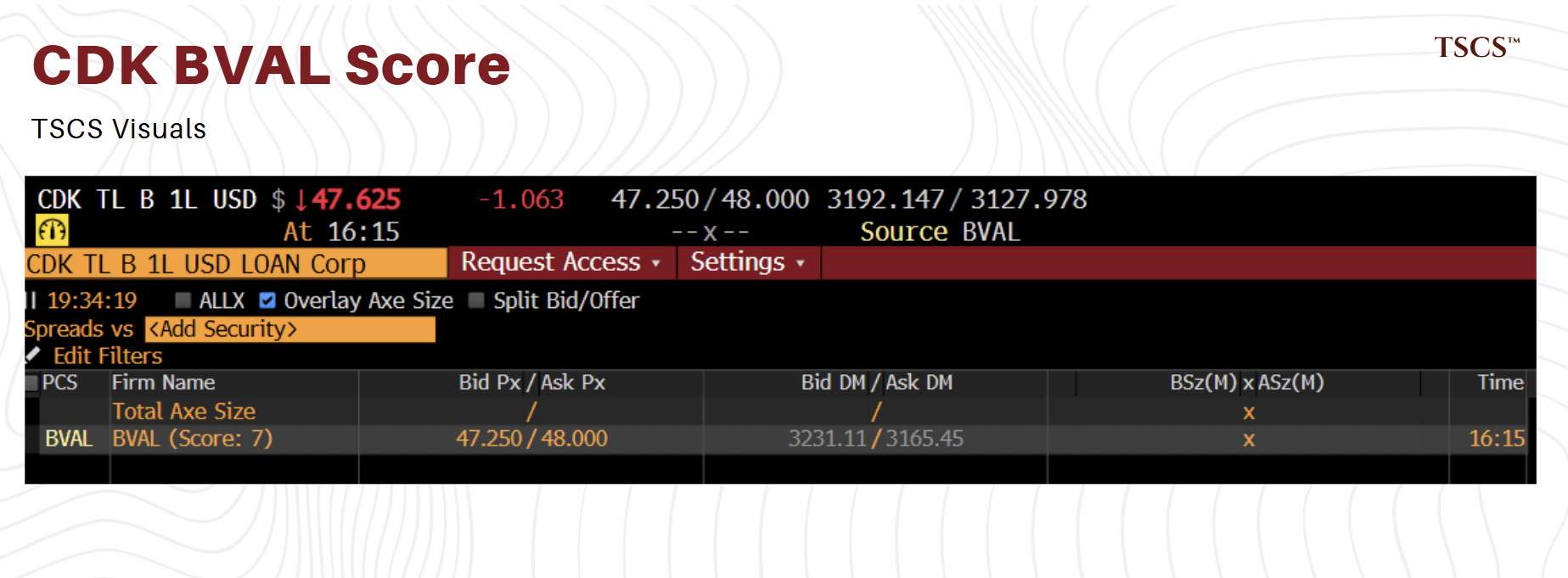

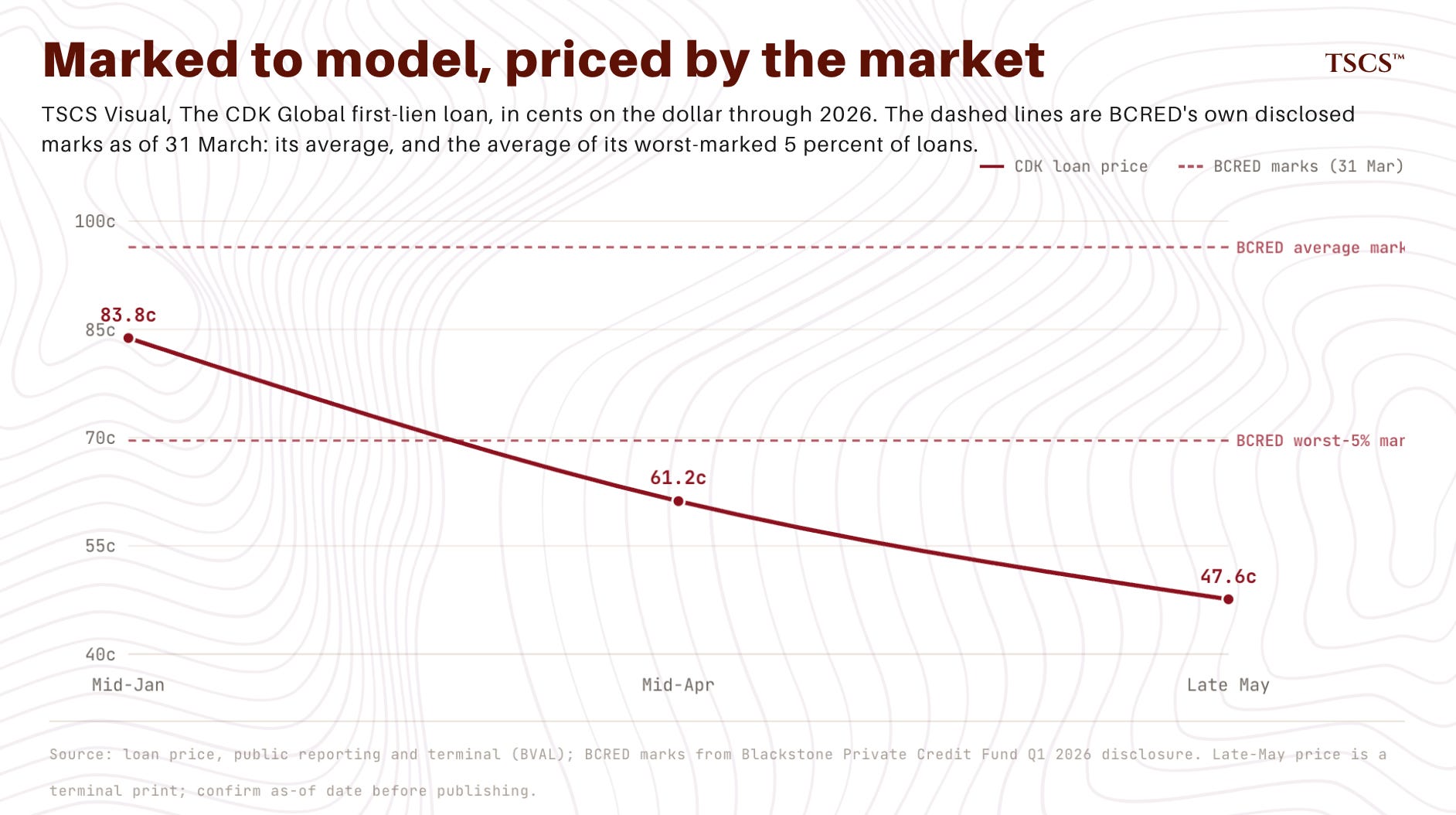

On the terminal, the loan’s composite price, the BVAL print, sits around 47.6 cents on the dollar.

Now hold that 47.6 against a fact from the private credit world. BCRED is Blackstone’s large retail-facing private credit fund, the vehicle through which ordinary investors get access to this asset class. BCRED holds the CDK loan. And BCRED’s most recent valuation marked that loan at a price far above the high-40s print on the terminal.

Sit with the two facts together. Blackstone, through its credit arm, signed the cooperation agreement in April: an institutional action that signals an expectation of restructuring. Blackstone, through BCRED, carries the same loan at its most recent mark, the quarterly valuation struck on 31 March, at a price well above where the loan now trades. That mark predates both the April cooperation agreement and the current terminal print. It is, in other words, a stale number, set before the loan’s most visible leg down, and it is the number BCRED’s retail investors see when they check their account, and the number their management fee is calculated against.

Same parent. Same instrument. Two valuations, struck for two different audiences. One of them, current and institutional, informs a restructuring strategy. The other, older and retail-facing, informs what an ordinary investor believes their holding is worth.

This is the same architecture we found in the insurance filings, surfacing in a different segment of the same firms’ empires. An institutional view of an asset and a retail-facing view of the same asset, maintained by the same parent, that do not agree. Our colleague Leyla Kunimoto goes considerably deeper on the private credit dimension of this in a forthcoming piece, and we will not get ahead of her work. We raise CDK here for the reinsurance angle, and for that, we pulled the full holder list of the loan off the terminal. It is the most interesting document we obtained in the entire investigation.

Two things jump out.

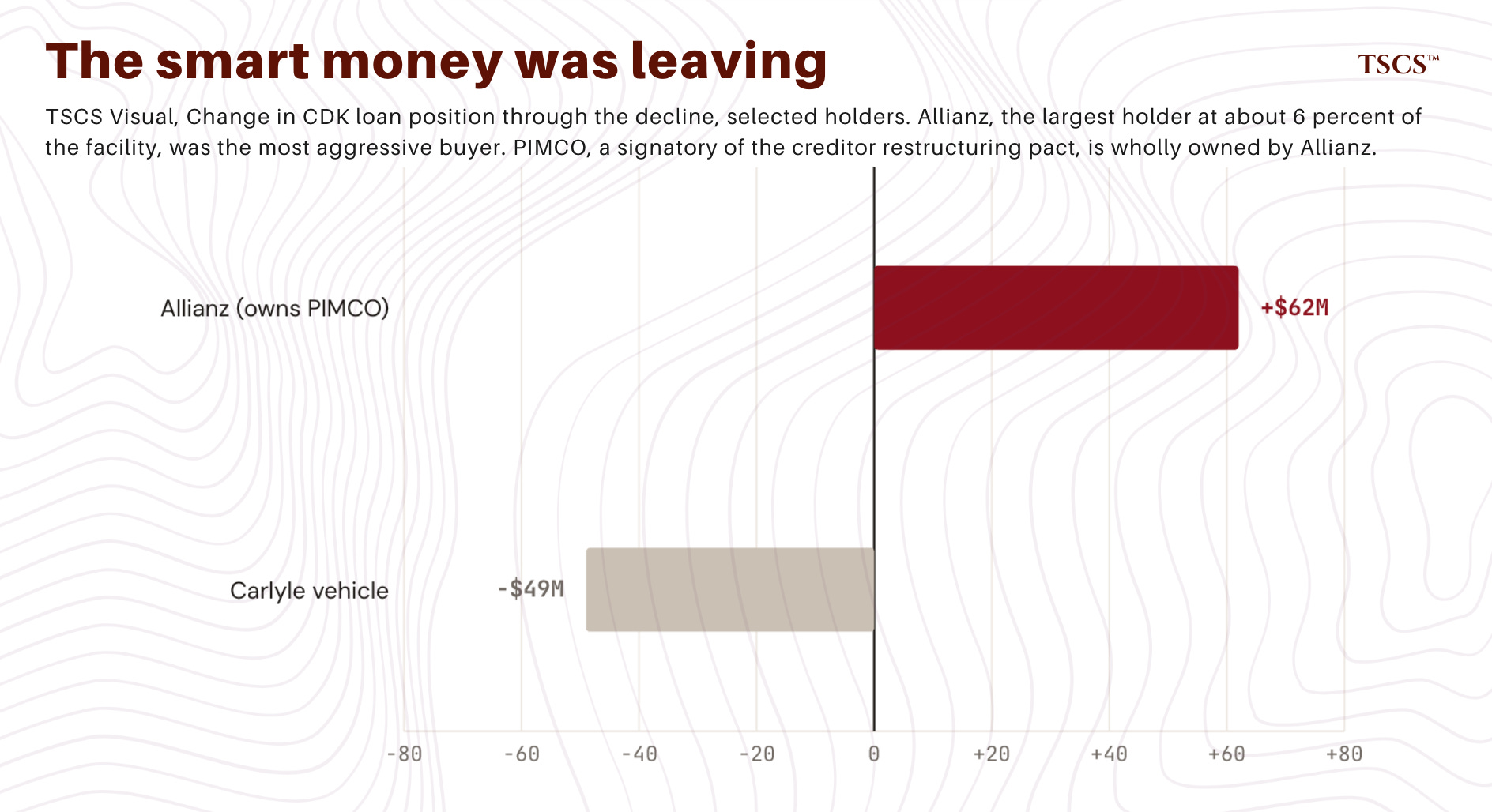

The first. The single largest identifiable holder of this distressed, restructuring-bound loan is Allianz, at roughly $240 million, just over 6% of the entire facility. Allianz is one of the largest insurance companies on earth. And Allianz, alone among the large holders, was not selling. Allianz was the most aggressive buyer in the entire holder list, having added roughly $62 million to its position through the very period in which the loan was deteriorating toward the high-40s.

The second. Around Allianz, the behavior of the other large holders runs the other way. The PE-affiliated credit managers, in aggregate, were net sellers. The single largest seller in the entire list was a Carlyle vehicle, reducing its position by roughly $49 million. The names with the deepest institutional credit franchises were, on balance, heading for the exit. The flow across the whole holder list was net negative: money leaving.

Now the detail that ties it together. Three public facts, in order.

Fact one: PIMCO is one of the named signatories of the CDK creditor cooperation agreement, the restructuring bloc.

Fact two: PIMCO has been wholly owned by Allianz since 2000.

Fact three: Allianz is the largest holder of the CDK loan, and was its most aggressive buyer through the decline.

We’re not going to tell you what that means, because to assert a single interpretation would be to claim knowledge of internal information flows that we do not have, and that no honest outside analyst could have. There are benign readings. A global firm is not a single brain; the left hand and the right hand of a company that size genuinely do act independently, and often should. There are less benign readings. We are showing you the facts, in the correct order, from public sources, and we are leaving the interpretation where it belongs, which is with you.

What we will say is this. The CDK holder list is a photograph of the thing this entire piece is about. A distressed, opaque, model-valued private credit instrument. A web of the largest asset managers and insurers in the world, all holding pieces of it. The sophisticated institutional money, on balance, quietly leaving. And the retail-facing and insurance-facing vehicles, the BCRED investors and the Allianz policyholders, still inside, still carrying it, still being charged a fee on a number a model produced.

That is the structure. CDK just happens to be a corner of it that the daylight reached.

A brief interruption, because this is the kind of work we exist to do.

TSCS publishes institutional-grade research on the structures that move markets, before the structures become headlines. Our Nuclear Primer became a reference document. “Don’t Short SaaS” called the bifurcation of the software selloff while the market was still panicking. Our private credit series, with Les Barclays and now Leyla Kunimoto, has been mapping the marks-versus-reality problem for months. Nick Nemeth’s open letter to Speaker Johnson reframed the insurance debate in Washington.

If you want this kind of work in your inbox, and you want it before the crowd arrives, subscribe.

8. The Market Has Already Voted

Step back. If this trade, buy the insurer, swap the assets, collect the spread and the fees, is so good, who’s been collecting the proceeds?

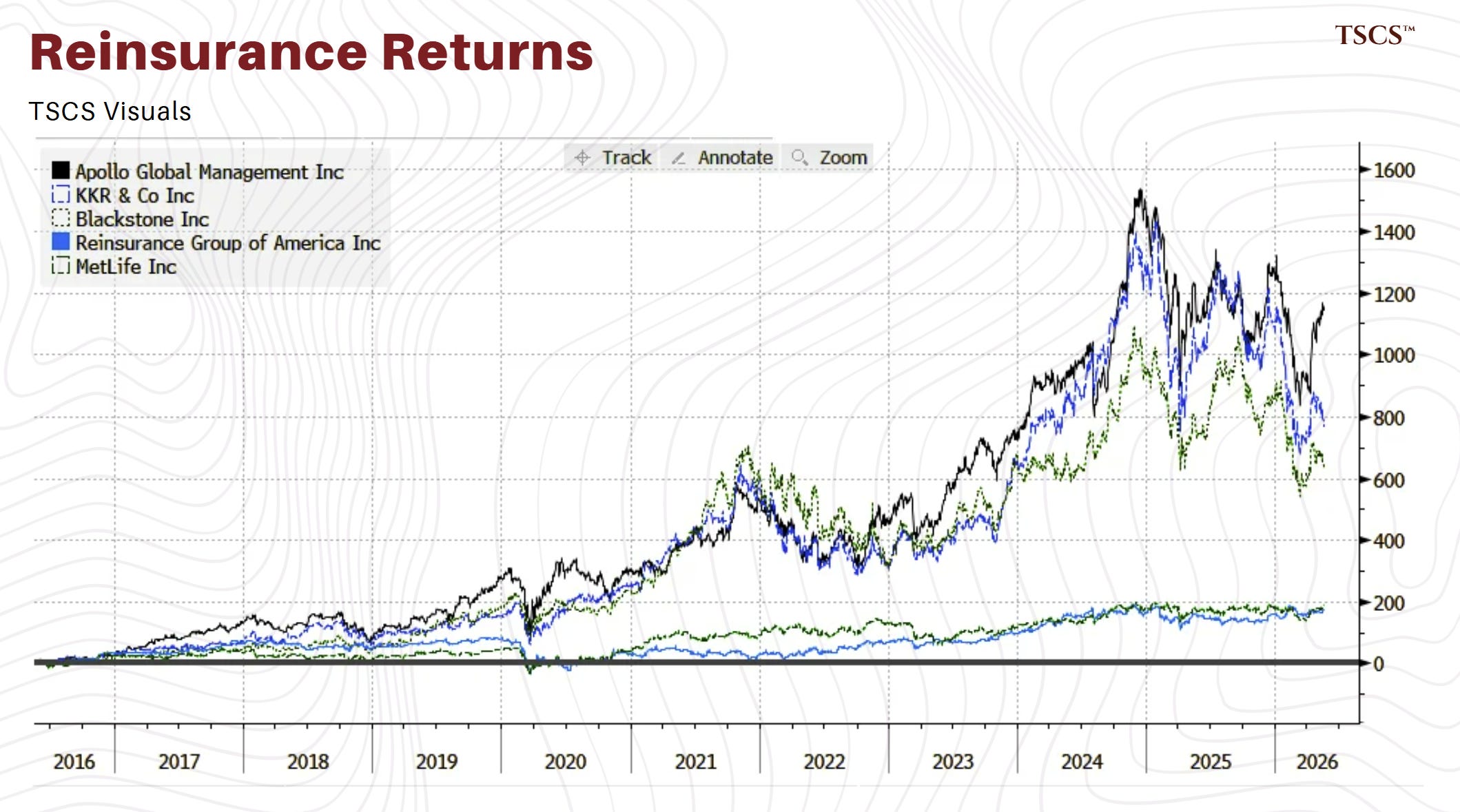

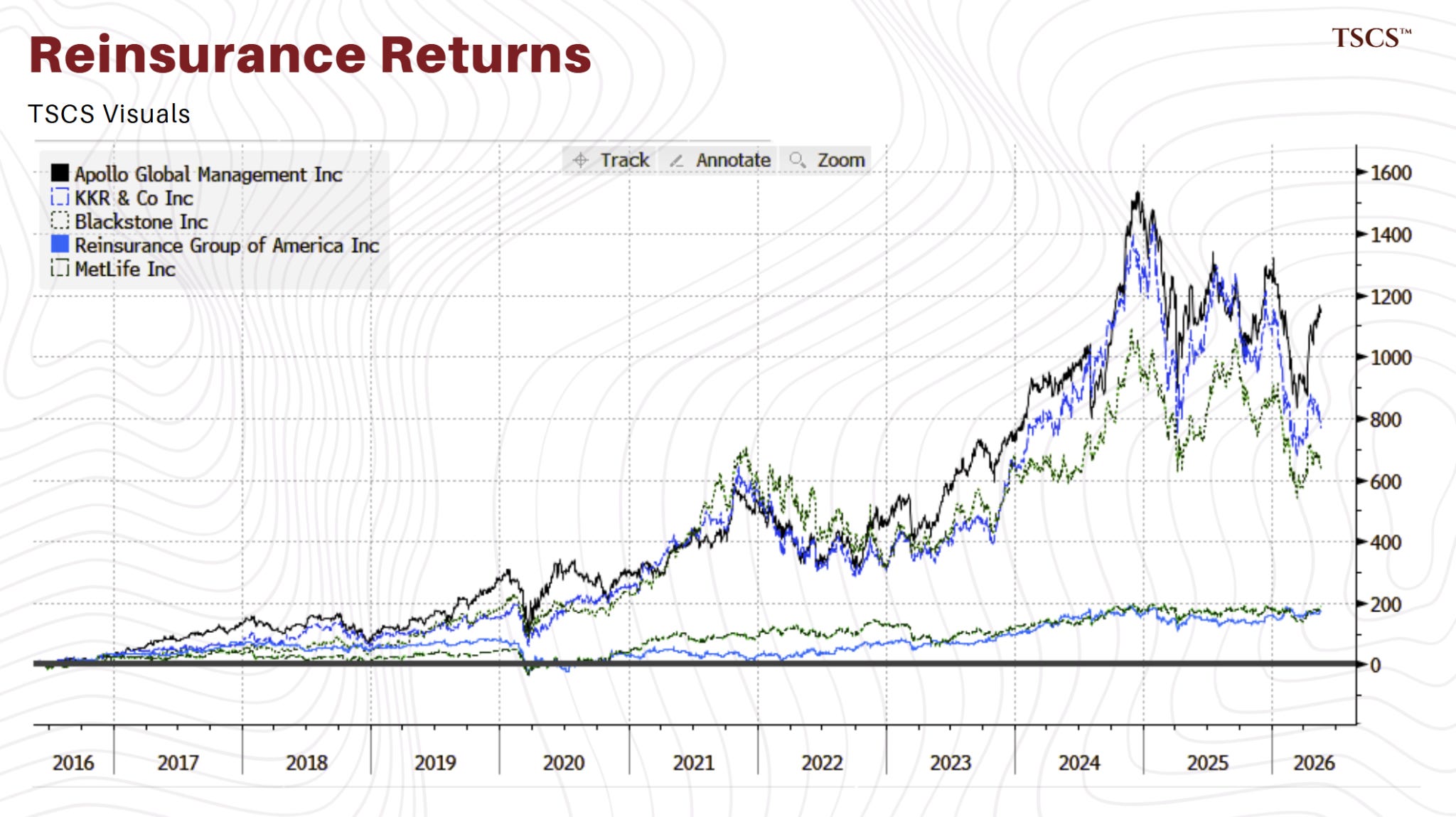

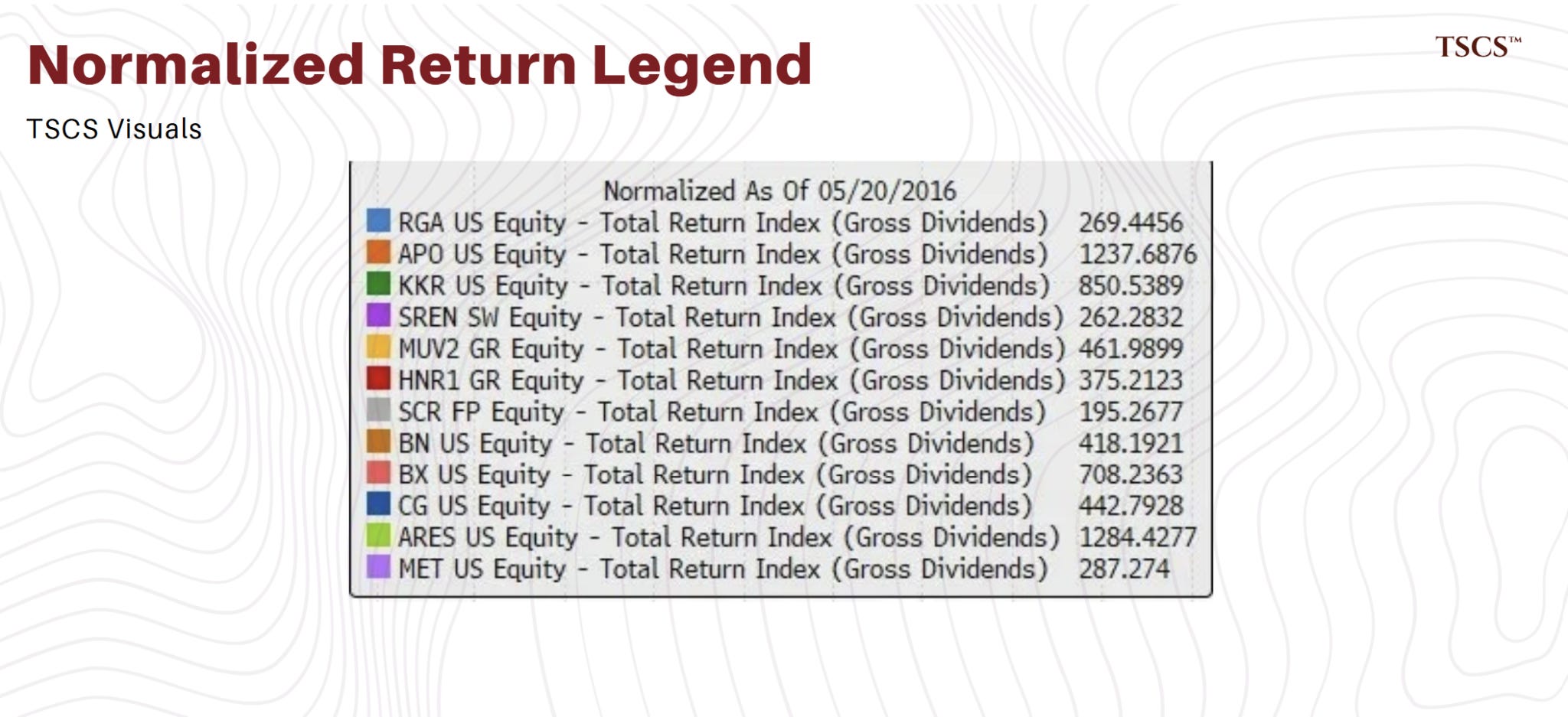

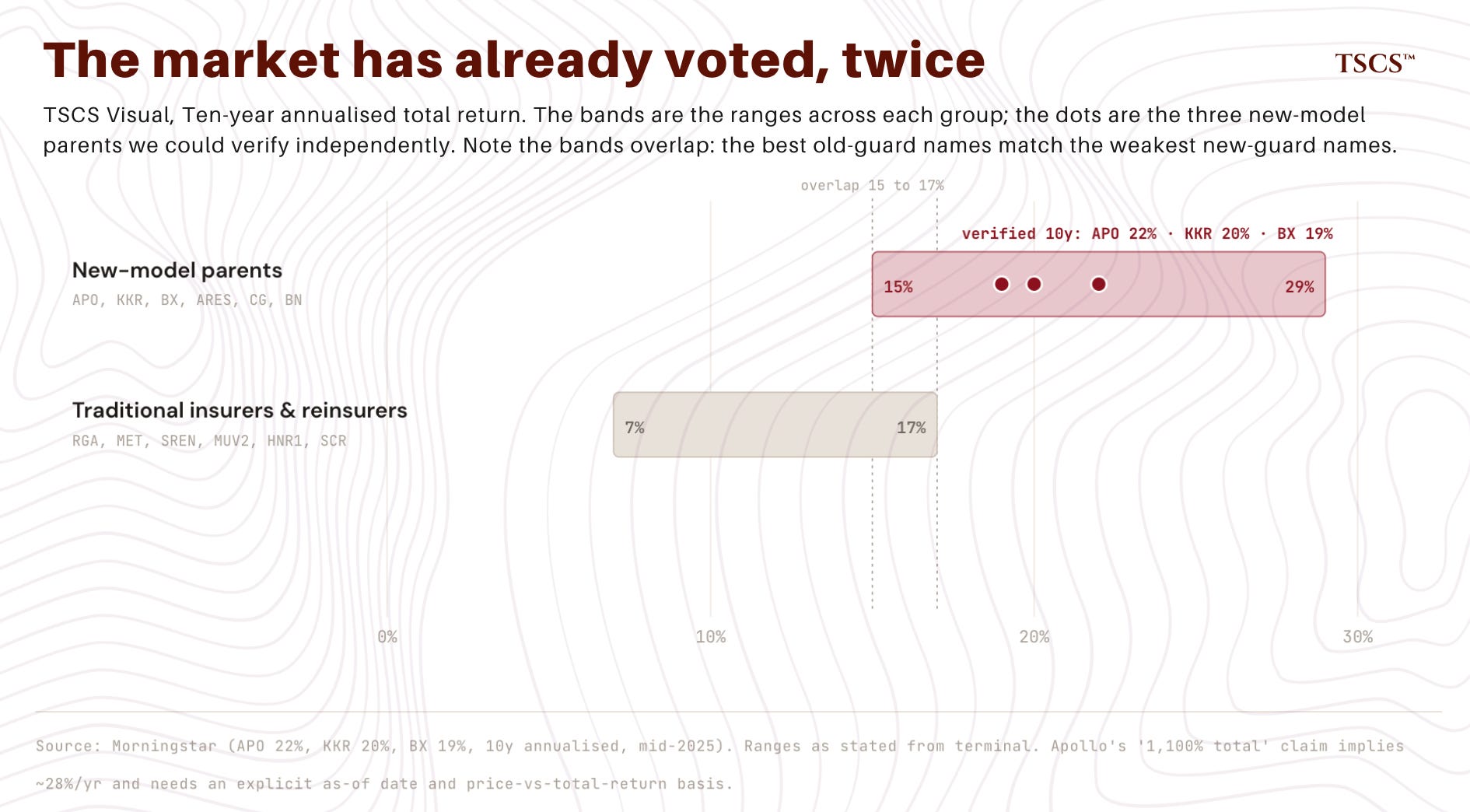

We pulled ten years of total return, indexed, for two groups. The first group is the old guard: the traditional, publicly traded life insurers and reinsurers. Reinsurance Group of America. MetLife. Swiss Re. Munich Re. Hannover Re. SCOR. The second group is the new guard: the publicly traded parents of the new model. Apollo. KKR. Blackstone. Carlyle. Ares. Brookfield.

The result is not subtle. Over the decade, the old guard compounded total return at roughly 7% to 17% a year. Respectable, boring, insurance-like numbers. The new guard compounded at roughly 15% to 29% a year. Apollo’s total return over the ten years was north of 1,100%. Ares’ was higher still. The asset manager parents did not beat the traditional insurers by a margin. They lapped them, two and three times over.

And look at the underlying business growth. RGA, the largest pure life reinsurer in the old model, grew its life premiums from roughly $9 billion to roughly $17 billion over nine years. It roughly doubled. Solid. Apollo’s Retirement Services revenue went from $1.4 billion in 2019 to $27 billion in 2025, though much of that step-up is the accounting consolidation of Athene from 2022, not organic growth. The old guard did not stop working. It got lapped by an institution running a different machine.

The equity market, in other words, has already rendered a verdict, and the verdict is emphatic: the new model wins. The capital has voted.

But that vote measures one thing only: which model is more profitable in a benign environment. It does not, and cannot, measure whether the more profitable model is more robust. Those are different questions, and the equity market, over the last ten years, has only been asked the first one.

There is a second market, and it has rendered a notably more cautious verdict. The credit market, where these same firms borrow, is supposed to be the careful one: the market that prices downside rather than dreams. We pulled a decade of borrowing spreads for the asset manager parents and set them against the traditional insurers.

A decade of spectacular equity outperformance has not bought the new model a credit market endorsement. If the bond market genuinely believed the PE-owned insurance complex were as robust as its equity returns imply, the parents would borrow at a clear premium to the sleepy old guard. They do not. In aggregate they borrow roughly in line with the traditional insurers, and several of them, including the parents of major insurance platforms, borrow visibly wider than MetLife or Prudential, not tighter.

The equity market has priced these firms for a generation of compounding success. The credit market has declined to award them a single basis point of safety premium for it. The two markets disagree this sharply about the same companies. The equity market votes on how good the upside looks. The credit market votes on whether you get your money back. The market that has been less impressed is the one whose job is the question this piece is about.

9. Why You Cannot Opt Out

Everything to this point has been about institutions. Here is where it touches a person.

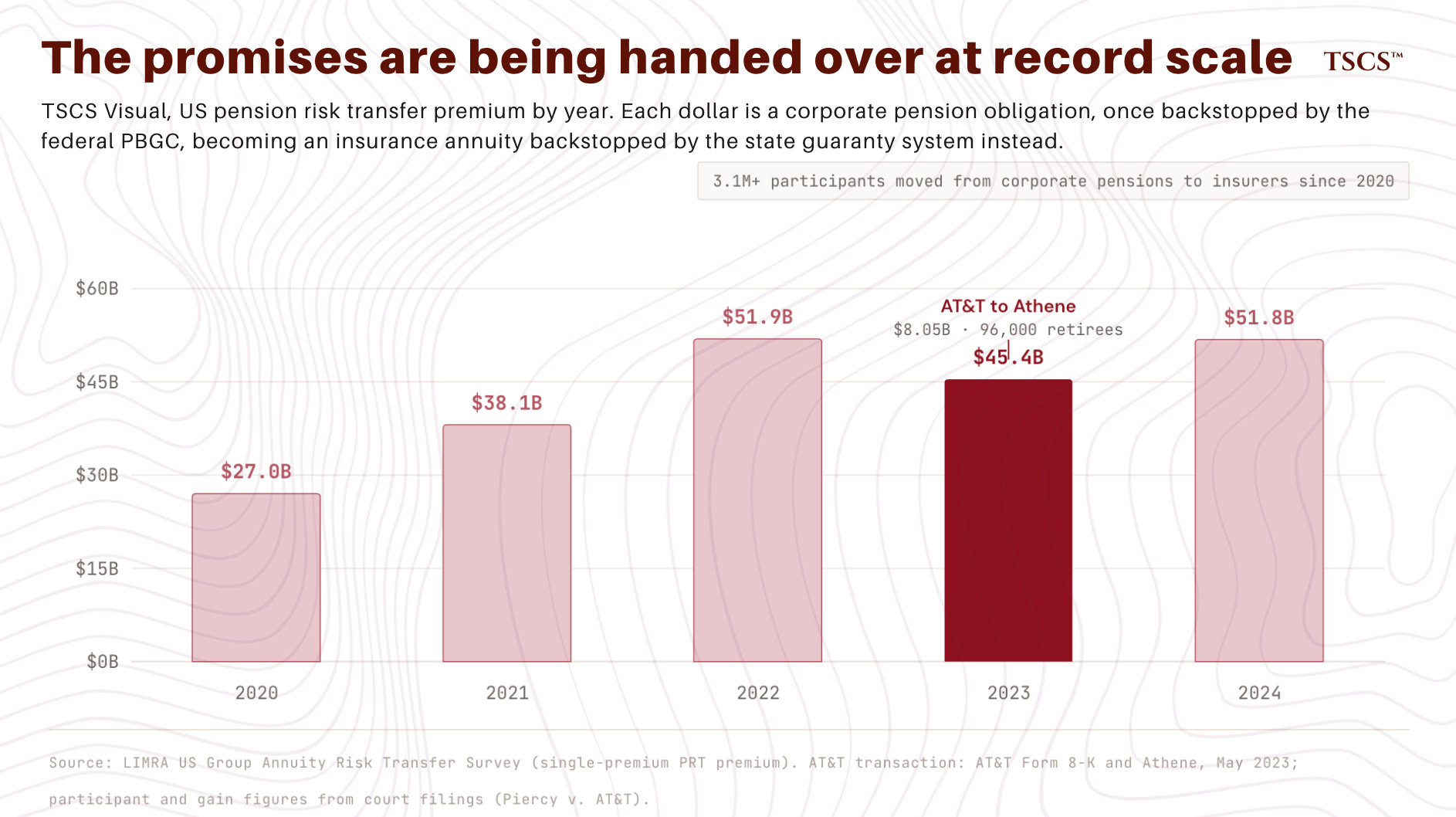

In May 2023, AT&T transferred its pension obligations for roughly 96,000 retirees and beneficiaries to Athene, in a single transaction worth about $8 billion. This is called a pension risk transfer, and it has become one of the busiest corners of the insurance industry. A corporation with a defined-benefit pension plan hands the obligations, and the matching assets, to a life insurer. The insurer issues annuities. The retirees, who used to be beneficiaries of a corporate pension, become annuitants of an insurance company.

The retirees did not vote on this. They were not asked. One day their pension was an obligation of AT&T, backstopped by the federal Pension Benefit Guaranty Corporation. The next day it was an obligation of Athene, backstopped by something else entirely. AT&T, for the record, recognized a pre-tax pension settlement gain of $363 million on the transaction and shed its PBGC premiums. The transfer was good business for AT&T. Nobody asked the 96,000.

And, by the structure we read in Section 2, a substantial majority of those transferred obligations were then reinsured offshore. Athene’s own disclosures indicate the majority of its pension risk transfer liabilities are reinsured to its Bermuda affiliates, consistent with the internal reinsurance structure described in Section 2.

When a corporate pension fails, the PBGC stands behind it. The PBGC is a federal entity, it is pre-funded, and while its coverage has limits, it is a genuine, funded backstop. When an insurer fails, there is no PBGC. There is the state guaranty fund system.

The state guaranty funds are real and they have paid claims. But they are not the PBGC. They are organized state by state. They are not pre-funded in any meaningful sense; they raise money, after a failure, by assessing the other insurers in the state. And their coverage is capped, commonly around $250,000 of present value per individual, with the precise figure varying by state. For a modest annuity, that cap is sufficient. For a retiree whose pension was substantial, it may not be.

The retired teacher we started with cannot escape any of this. She cannot move her annuity to a safer insurer without surrendering it, often at a penalty. She cannot read the Bermuda filing, because there is almost nothing to read. She cannot see the marks on the private credit book, because the marks are models and the holders are undisclosed. She was told, by every signal the system is designed to send, that she had bought the safest thing in finance. She had in fact been moved, without a vote, onto a balance sheet that Apollo’s own filings describe as funded short, invested in model-valued private assets, and capitalized largely offshore.

That is what “you cannot opt out” means. The people with the most at stake in this structure are the people with the least ability to see it, understand it, or leave it.

10. What Would Make Us Wrong

We have built a deliberately alarming case. Here is what would make this piece wrong, and we’re not going to be coy about any of it.

We are punishing the company that showed its work. Athene publishes voluntarily. It puts its US statutory filing on its own investor relations website. The 80% to 100% quota share, the capital-in-Bermuda admission, the affiliated fee disclosures: we were able to build this case largely because Athene disclosed the raw material. The roughly 700 other US life insurers, many smaller, less sophisticated, and less well capitalized, disclose far less, and some are surely running cruder versions of the same structure with worse assets and thinner buffers. There is something genuinely uncomfortable about training the brightest light on the operator that left the lights on. Athene is, by most credible accounts, among the most sophisticated operators in this space. If the best-run version of this structure is the one we have just spent the piece worrying about, that is either evidence the worry is overblown, or evidence the problem is much larger than one company. We think the latter. But the discomfort is real and we will not pretend it away.

The ratings agencies have more information than we do. Athene’s insurers carry an A+ from S&P, Fitch, and AM Best, and Moody’s equivalent A1. Those agencies have access to data, including confidential Bermuda data, that we do not. It is entirely possible they have examined the consolidated structure and concluded it is robust, and that our outside view, built from public filings, is missing capital and protections that are real but not publicly visible.

The consolidated capital number is much larger than the entity number. Nemeth’s letter focused on the modest capital at the US operating entities relative to the obligations they have written. Athene will point out, correctly, that on a consolidated basis, across the US and Bermuda entities and including third-party ACRA capital, the figure is many times larger, and that the internal reinsurance structure is specifically designed to make that aggregate capital available across entities. That is a serious rebuttal. Our answer is the one we gave in Section 2: in a receivership, what protects a policyholder is the capital legally obligated and available at the failing entity, under the jurisdiction that regulates it, and ACRA’s third-party investors have no such obligation. But this is a genuine analytical dispute, not a settled fact, and a fair reader should weigh both sides.

Regulators are already moving. The Bermuda Monetary Authority introduced enhanced disclosure rules for these reinsurers, effective from year-end 2025, with the first detailed asset and liability reporting cycle in 2026. The Financial Stability Oversight Council has explicitly flagged the offshore reinsurance trend. The IMF has raised concerns about life insurers and illiquid assets. The structure we have described is not a secret to the people whose job is to watch it. It is being watched, and the disclosure regime is tightening. The optimistic case is that the system corrects through regulation before it corrects through a failure. We hope that case is right.

This is not a new observation. Academics have studied the underlying maneuver, insurers ceding liabilities to affiliated and more lightly regulated reinsurers, under the label “shadow insurance” for roughly a decade.

Nothing has actually broken. Every alarming sentence in this piece is, strictly, a sentence about a potential. The wall is in 2027; 2027 has not happened. The refinancing market is open; it has not seized. The model-valued assets have not been forced into daylight at scale. A patient critic can fairly say that we have described a structure that has, so far, worked, paid every claim, and made its owners spectacularly rich, and that “so far” has lasted fifteen years.

We hold our view in the face of all of these. But a piece that did not put them in front of you, in their strongest form, would not be research. It would be advocacy. We would rather be honestly uncertain than dishonestly confident.

11. The Translation

Nick Nemeth ended his open letter to Speaker Johnson with a comparison we keep returning to. He showed a risk-based capital ratio that reads like a fortress, sitting on an operating entity whose capital is a thin single-digit slice of the obligations it has written. And the people who will bear the cost of the gap between the headline and the structure did not build it, did not profit from it, and do not know it exists.

This piece has been an attempt to close, slightly, that last gap. Not the financial gap. The knowledge one.

We have not shown you anything that was hidden. That is the entire point. The 80% to 100% quota share is in the 10-K. The capital being held in Bermuda is in the 10-K. Apollo being 84% an insurance company is in Apollo’s own segment reporting. The funding wall is on the terminal. The fee architecture is in the footnotes. The CDK holder list is a function call away for anyone with a Bloomberg login. None of it is leaked, none of it is alleged, and almost none of it has ever reached the people it is actually about.

The life insurance industry spent a century building the most valuable asset a promise-making institution can hold, which is the boring, unimpeachable trust of the people it serves. Over the last fifteen years, a set of brilliant, aggressive, and entirely legal financial engineers worked out how to convert that trust into spread and fees, and they did it in plain sight, in public filings, in a language precise enough to be accurate and dense enough to be unread.

We do not think this ends in a single dramatic morning. The structure is more likely to fail the way Hemingway said you go bankrupt: gradually, then suddenly. A hard refinancing in a bad year. A wave of downgrades through the thin investment-grade tier. A model-valued book that meets a market that insists, finally, on voting. One mid-sized insurer, then a quarter of silence, then another, each failure explained as idiosyncratic until the pattern is undeniable. And underneath all of it, the annuitants. The retired teacher. The 96,000 from AT&T. The people who bought the single thing in all of finance that was supposed to be safe.

There is still time for this to be fixed by disclosure and regulation rather than by failure. Nemeth’s letter laid out what that would take, and we would point Congress and the state regulators back to its five asks: leverage measured honestly rather than through headline ratios, statutory filings made genuinely public and machine-readable, an annual federal report on every insurer that takes pension or annuity money, the filing-exempt ratings backdoor closed, and a review of whether the 1945 statute governing all of this still fits the world it now governs.

We would add only one sentence to his five asks. Require that the person buying the annuity be told, in language she can read, what we have just spent nine thousand words showing you: that the institution holding her retirement is funded short, invested in assets that do not trade, capitalized in a jurisdiction she will never see a filing from, and owned by a firm that earns a fee every time her money moves.

She will likely still buy the annuity. Most people, correctly, will still need one. But she will have bought it knowing. And the entire architecture we have described in this piece depends, in the end, on her not knowing.

We have told her now.

This piece builds directly on Nick Nemeth’s “An Open Letter to Speaker Johnson,” published in March 2026, and is intended as a companion to it. A full layman-to-expert primer on how reinsurance works, “What Is Reinsurance and Why You Should Care,” will follow within the next two weeks.

Nothing in this piece is investment advice. It is structural analysis built entirely from public filings and market data. We hold no position in any security mentioned. Figures are sourced from SEC filings, Bermuda regulatory disclosure, and the Bloomberg terminal as of May 2026; where a figure depends on a methodological choice, we have flagged it. If you believe any fact here is wrong, write to us, because we would rather correct it than defend it.

Subscribe to TSCS for institutional-grade research on the structures that move markets, before they become headlines.

| A guest post by

|

Actually, there is nothing new under the sun. In the late 1980s, a famous go-go growth stock investor, Fred Carr, built Executive Life into one of the fastest growing life insurers in the industry by writing fixed annuities and investing roughly half of its assets in high yield bonds underwritten by Drexel. The higher yield on the junk bond portfolio made Executive Life almost unstoppable — until the 1990-1991 recession, when Executive Life was taken over by regulators. And shortly later, Eli Broad built SunAmerica (first called “Broad Inc.”) into an annuity powerhouse by buying closed blocks of annuities, lowering the crediting rate, and investing the assets aggressively into hedge funds and private equity partnerships. Broad was smart enough to sell to AIG before the music stopped on that one.

The current iteration of “alternative investment” annuity companies have tried to build stability by reducing the surrender option value on the liability side of the balance sheet, and investing in private credit where borrowers don’t default, they just restructure.

Jim Belardi, the cofounder of of Athene, was the CFO of Broad Inc. and SunAmerica. Much of the private credit community traces its origins to Michael Milken, Drexel, and the high yield market …

Wicked good read. Pension funds and life insurance. Two products built on fear of the future and paid for by money earned with years of labor torn into by the dogs of finance. I doubt they will leave any meat on the bone.