How To Trade Warsh

In four weeks the market killed the easing cycle and started paying to tighten. The energy math and the one gauge the new Chair trusts both say it overpaid. Fade the hike premium.

Kevin Warsh is an inflation hawk. He has been one for two decades, through his years as a Fed governor and every year since, a consistent critic of easy money and of a central bank he has long argued runs too loose. When a hawk of that reputation took the Chair this month, the market did the logical thing. It repriced the Federal Reserve for tightening.

One fact that repricing has not reconciled.

If you’ve been around long enough, you know Warsh also has a known preference about rulers, the measuring kind.

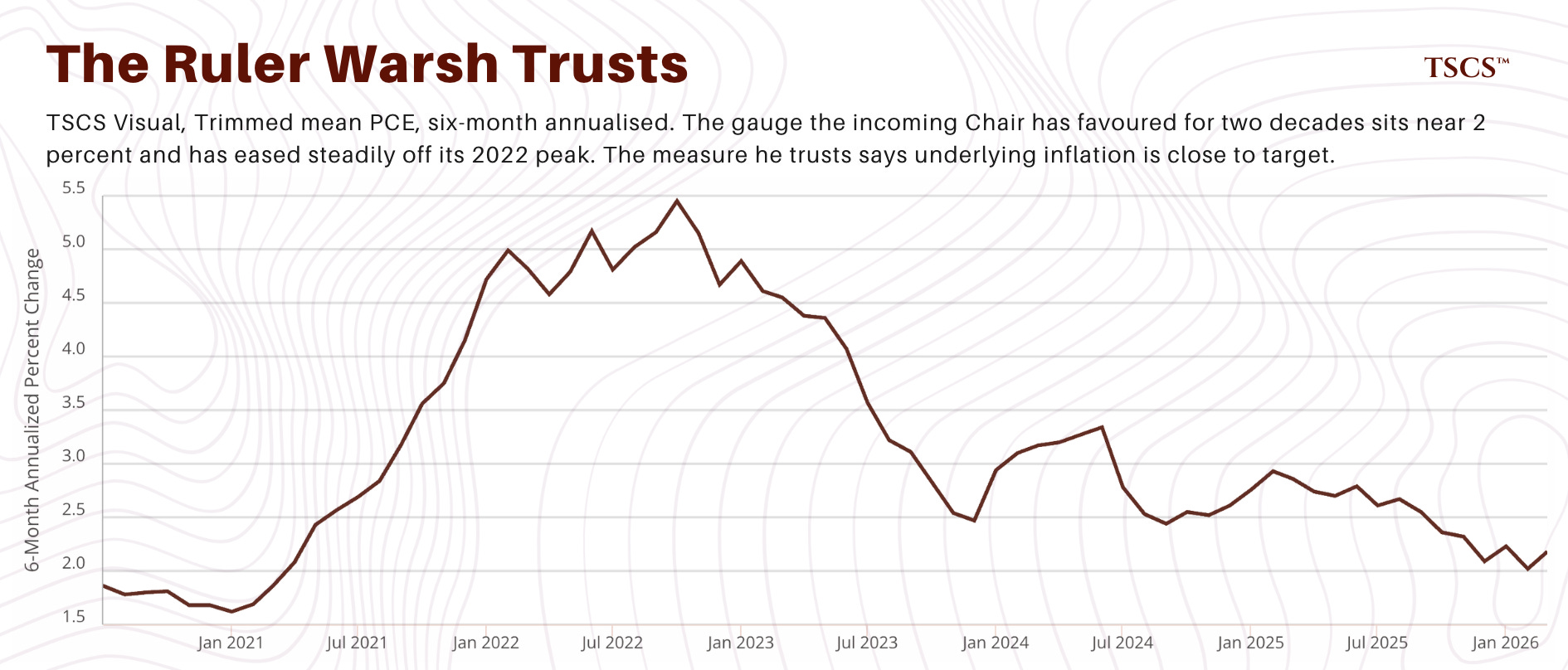

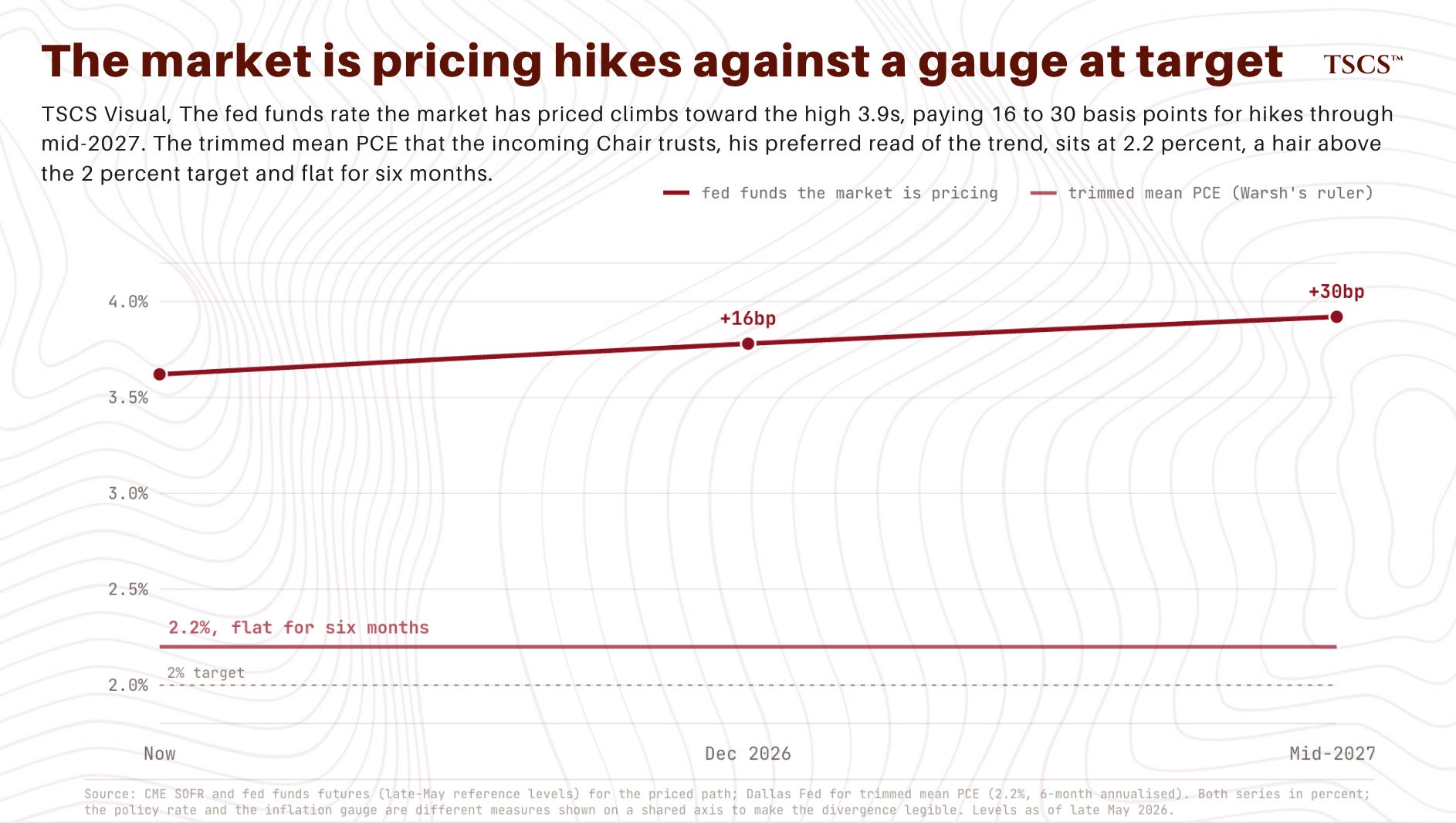

He has long favoured trimmed mean PCE, the measure that sorts every component of the inflation basket by how fast its price moved and discards the extremes at both ends, over the core PCE index, the gauge the Fed itself has leaned on as its preferred read of the trend for the better part of a generation. At his Senate confirmation hearing in April he dismissed that core gauge as a “rough swag,” his term, a scientific wild guess, and pointed to the trimmed measure as the cleaner signal. He picked it because he believes it reads the trend correctly, not because it is convenient. Today that gauge reads 2.2 percent on a six-month annualised basis, and it has sat in a narrow band around 2 percent for six straight months. The measure the incoming Chair trusts most says underlying inflation is close to target.

The man’s reputation says hike. The man’s ruler says hold. The market priced the reputation. The ruler is right, the arithmetic of the energy shock backs it, and the trade is to fade the hike premium the market has built into the 2026 and 2027 strip.

The consensus spent six months asking whether Warsh was a dove or a hawk. The market settled it, priced him hawk, and moved on. That settled view is the mistake. A hawk does not hike when the measure he himself trusts reads 2.2 percent and the inflation shock is already ageing out of the data. The hikes the market has paid for are not coming.

Below the line: the four week repricing in basis points, the committee’s two unpulled triggers, the base-effect arithmetic that fades the headline on flat oil, and the full trade with entry, sizing and kill switches. The market priced the headline and skipped the work. The structure makes it cheap to be wrong. The work is what turns cheap into a positive edge. Paid subscribers get to read it.

1. The Market Has Paid for Hikes

Four weeks ago, at the April FOMC, the New York Fed’s Open Market Desk survey still carried a median modal path of two 25 basis point cuts over the coming year. The same survey window had options pricing roughly a 30 percent probability of a single hike by the first quarter of 2027. A low-probability tail.

Keep reading with a 7-day free trial

Subscribe to TSCS to keep reading this post and get 7 days of free access to the full post archives.