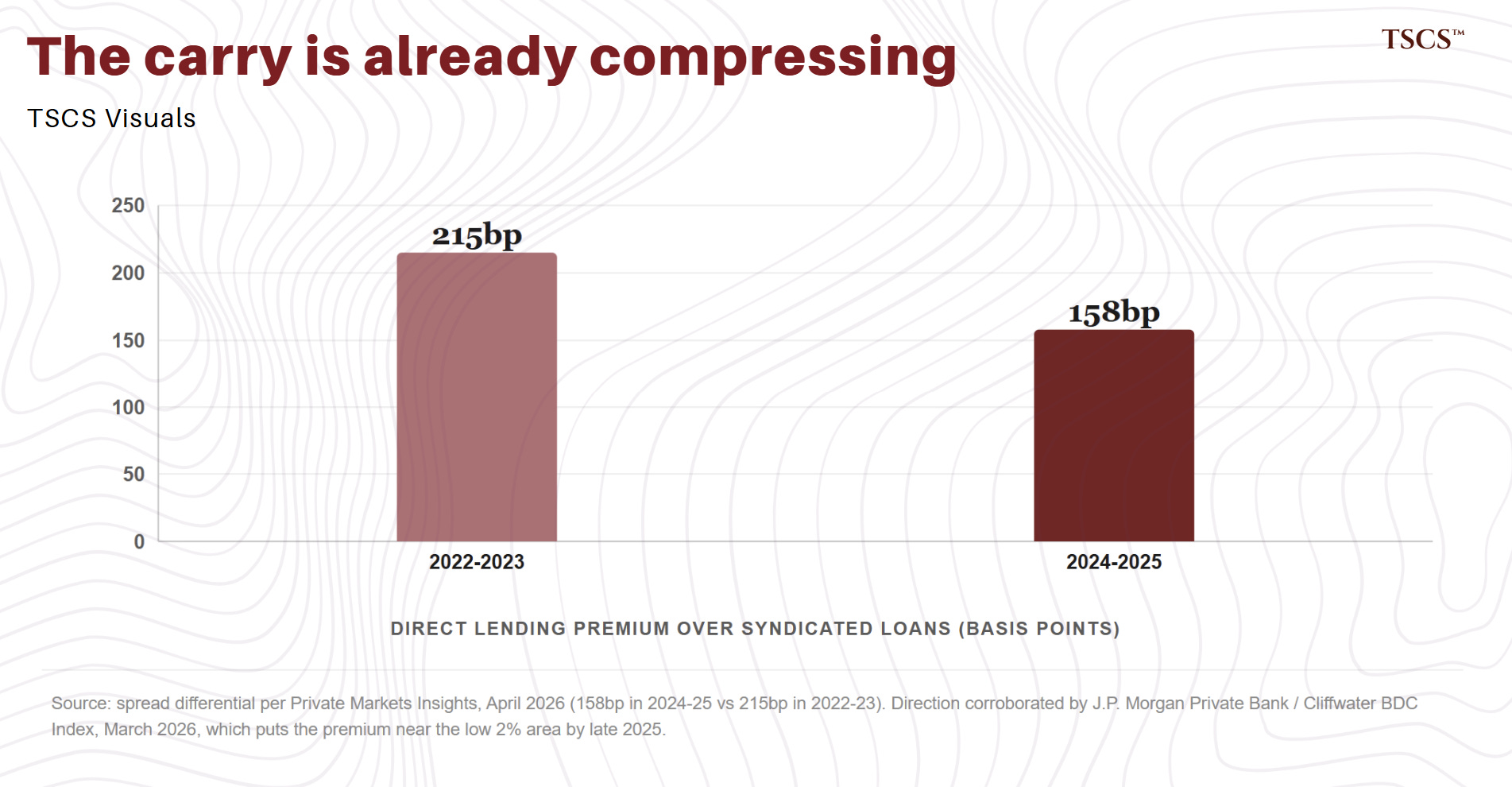

Marked to Faith

For some private credit loans the mark lags the market; for most, there is no market to lag. BDCs, NAV, payment-in-kind, and redemption gates. Blackstone, Apollo, PIMCO, Blackrock, etc.

In the harbor at Piraeus, in the years when Athens fed itself on the trade of the whole Aegean, there was a merchant named Theron who grew rich on jars he never opened.

His trade was olive oil, the good oil of the inland estates, sealed at the press into tall amphorae and stamped at the neck with the mark of the grove that made it.

The stamp was the thing. It told a buyer, without his ever tasting a drop, that the jar held first-pressing oil and not the bitter dregs, and on the strength of the stamp alone a jar could change hands a dozen times between the press and the table.

A jar sealed in autumn might pass through four merchants before spring, each paying a little more than the last, none of them breaking the wax.

To break the wax was to end the jar’s life as a thing that could be sold; you opened an amphora only to pour it, and a poured jar was worth nothing to the next man in the chain.

So the market in oil was, in truth, a market in seals.

Theron understood this earlier and more clearly than his rivals. He saw that the price of a jar had almost nothing to do with the oil inside it, which no one had seen since the press, and almost everything to do with the confidence of the man holding it that the next man would honor the stamp.

He bought sealed jars and he sold sealed jars, he was scrupulous, he prospered, and for years not one jar he traded was ever opened in his presence.

This was not a flaw in his business. It was the business. As long as the wax held, every jar in Piraeus was first-pressing oil, because the stamp said so and nothing said otherwise, and a thousand stamped jars in a thousand storerooms were, by common agreement, a fortune.

It held until a tavern-keeper, careless or thirsty, broke the seal on a jar that had passed through six hands at a rising price, and found vinegar.

One jar.

The keeper cursed and poured it out, and the loss was his alone. But the men in the storerooms did not sleep that night, and not over the one jar.

They lay awake over the others, the sealed ones, still stamped first-pressing and still, by common agreement, worth a fortune.

The opened jar had told them nothing about any particular sealed jar; it might have been the only bad one in the city. What it had told them was worse, and more general. It had told them that the stamp was not the oil. That a seal is a promise about a thing, and not the thing, and that the only way to learn what a jar holds is to break the wax, which no one in the chain can afford to do, because a broken jar cannot be sold.

This is a note about a market in seals. You have already met the jar that got opened.

The Loan You Can See

In our last piece, Eat The Pension, we showed you a single term loan that two arms of the same firm valued two different ways. Blackstone’s BX 0.00%↑ institutional credit business sat inside a creditor coalition organizing around the loan. Blackstone’s retail private credit fund carried that same loan on its books at a price the coalition’s existence made difficult to defend. Same loan. Same parent. Two numbers.

The loan was CDK Global’s. We raised it there for one reason. We raise it here for another. In the reinsurance piece, CDK was an illustration, the seam where the insurance balance sheet and the private credit balance sheet meet. Here it is a doorway. Because the interesting thing about the CDK loan isn’t that it’s mispriced. It’s that it can be priced at all.

Start with the loan itself. CDK Global makes the software that car dealerships run on. Brookfield took it private in 2022, funding the buyout the way buyouts of that era were funded, with a $4.07 billion first-lien term loan B, floating at three-month SOFR plus 325 basis points, maturing July 2029, rated B3 and B-minus. In April 2026 a majority coalition of CDK’s creditors, including PIMCO ALV 0.00%↑, BlackRock BLK 0.00%↑ and Blackstone and advised by the law firm Gibson Dunn, signed a cooperation agreement, the instrument creditors use to bind themselves together before a restructuring fight. Later that month a dissident faction tried and failed to assemble a rival group. Fitch added the loan to its Top Loans of Concern list in its April default monitor. CDK’s fourth-quarter pro forma EBITDA came in near $127 million, down roughly 18% year on year.

Now the numbers.

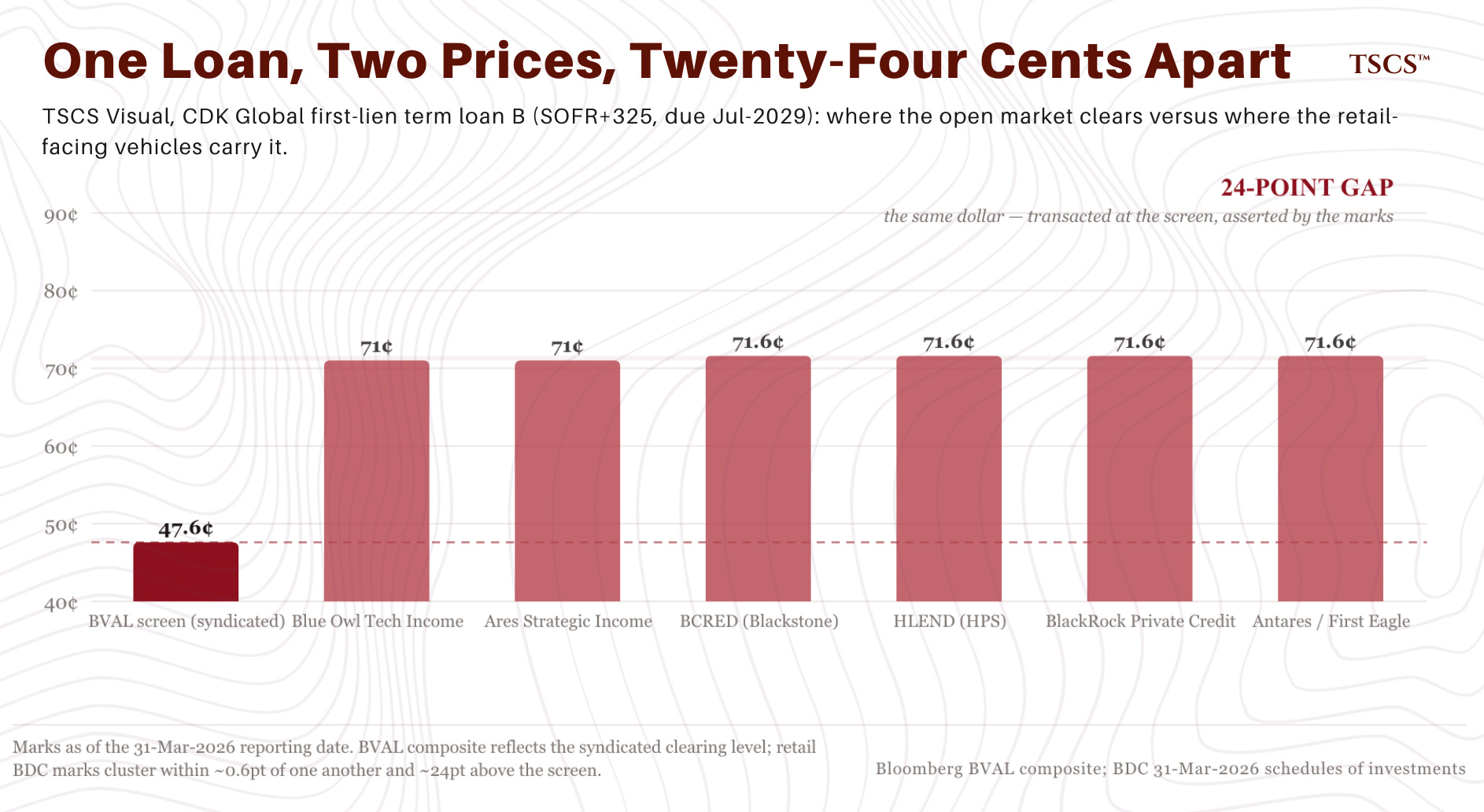

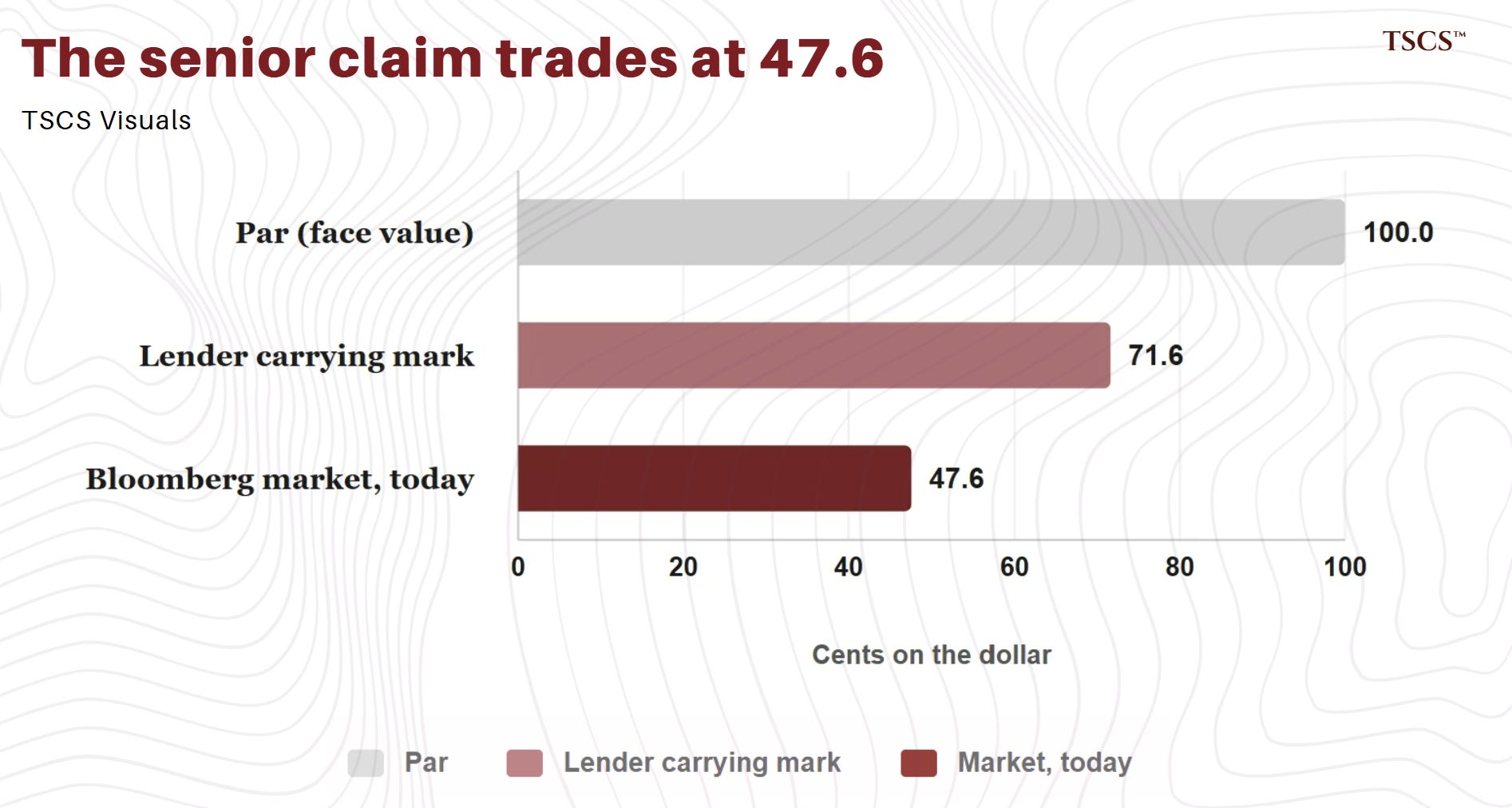

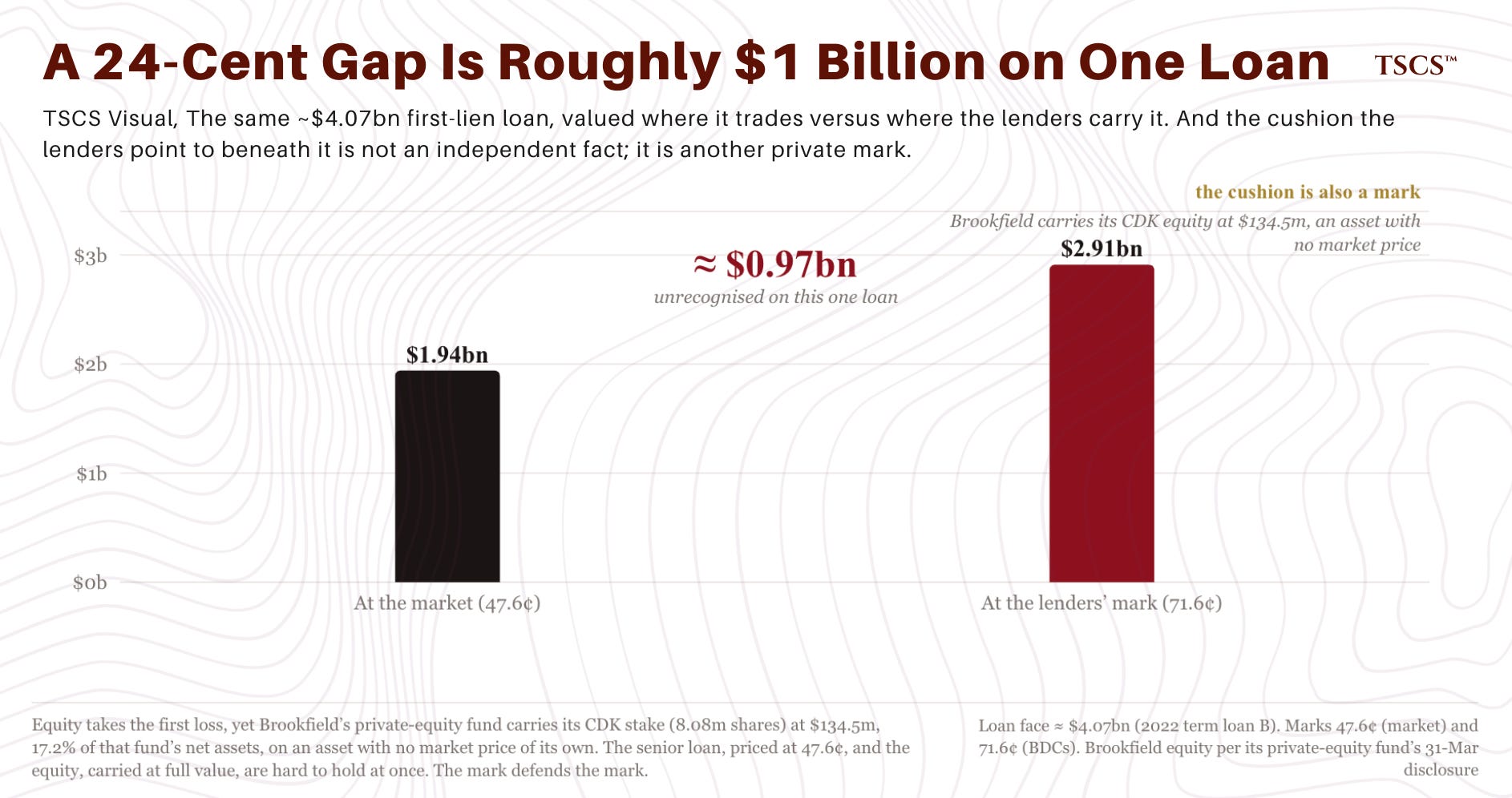

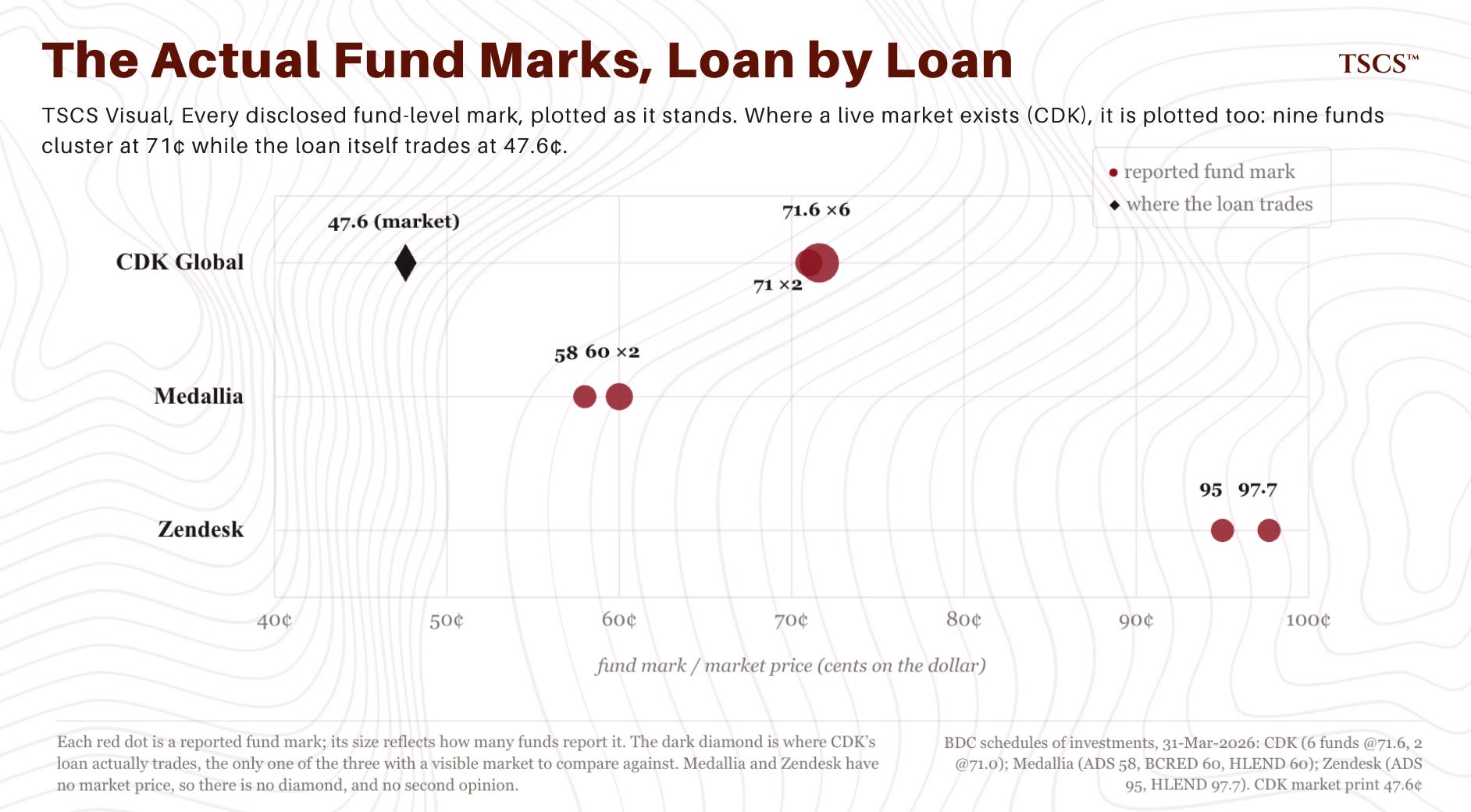

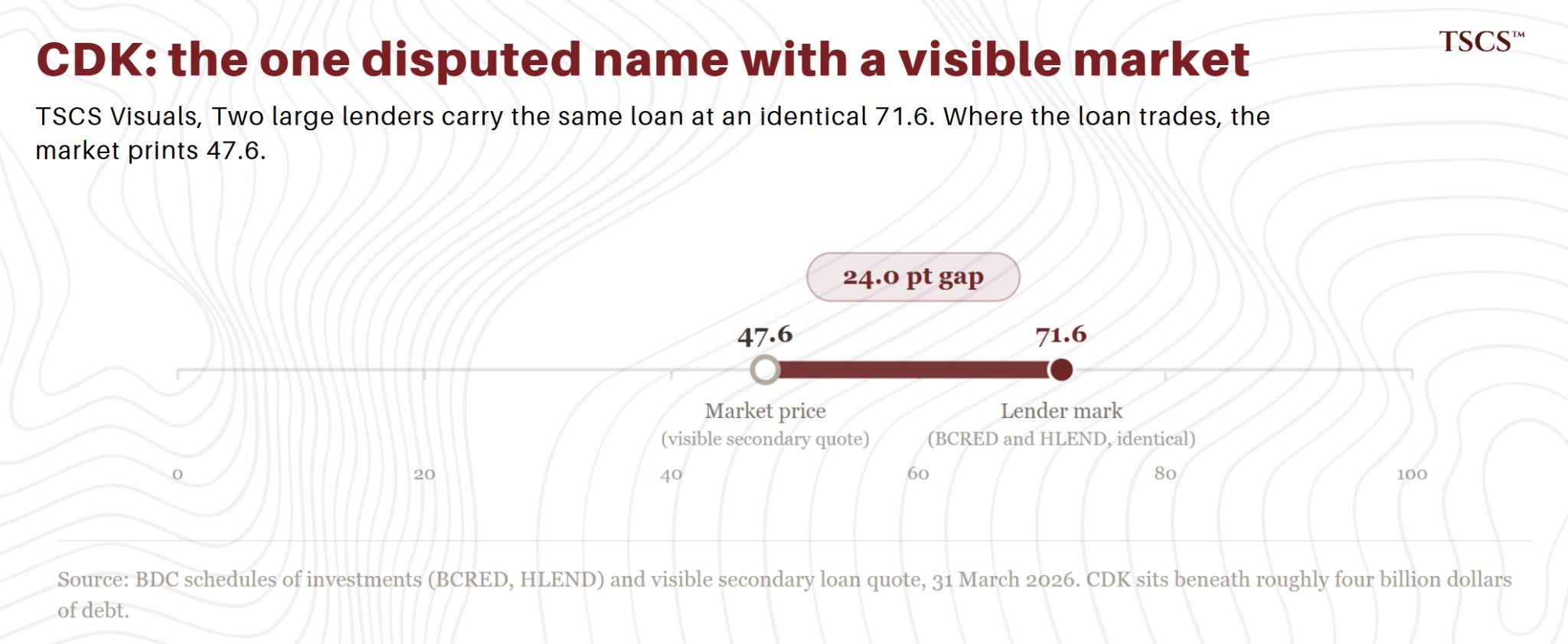

On the Bloomberg terminal, the loan’s composite price, the BVAL print, sits around 47.6 cents on the dollar. That figure is not a model output. CDK’s is a roughly $4 billion broadly syndicated term loan that trades in the secondary loan market, and the composite is built from the quotes dealers are making on the actual paper, so 47.6 is the price the market puts on the loan, not an estimate of where it might sit.

Across the retail-facing BDCs that hold the loan, the marks tell a strikingly uniform story. BCRED carries it at 71.6 cents of par as of the 31 March schedule. HPS’s HLEND fund at 71.6. BlackRock’s private credit fund at 71.6. Through Antares, First Eagle and most of the rest of the syndicate, the number barely moves off that line. Two outliers, Blue Owl’s Technology Income BDC and Ares’s Strategic Income Fund, sit slightly lower at 71.0. The retail vehicles, all of them, agree with each other to within roughly half a point. They disagree with the market by twenty-four.

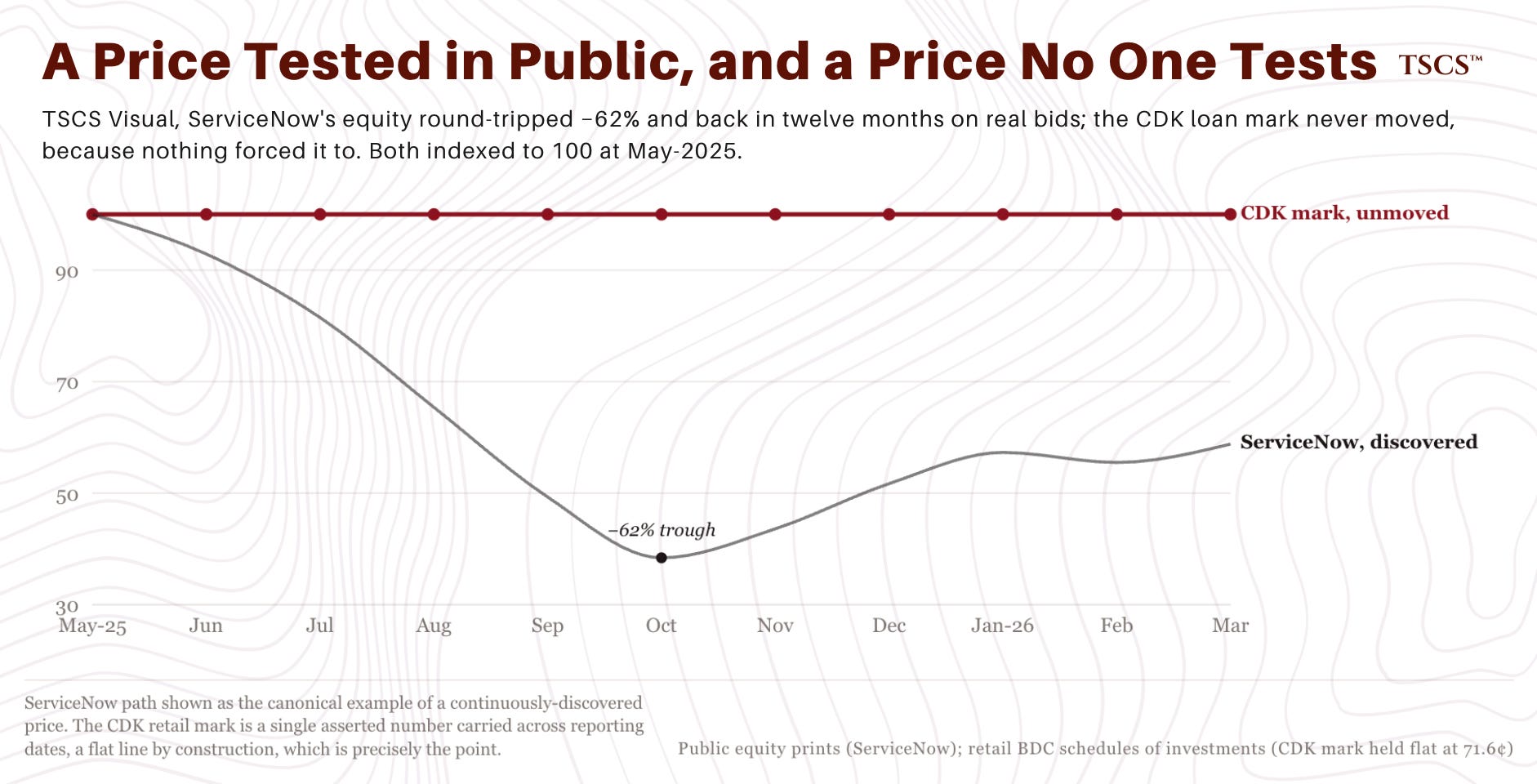

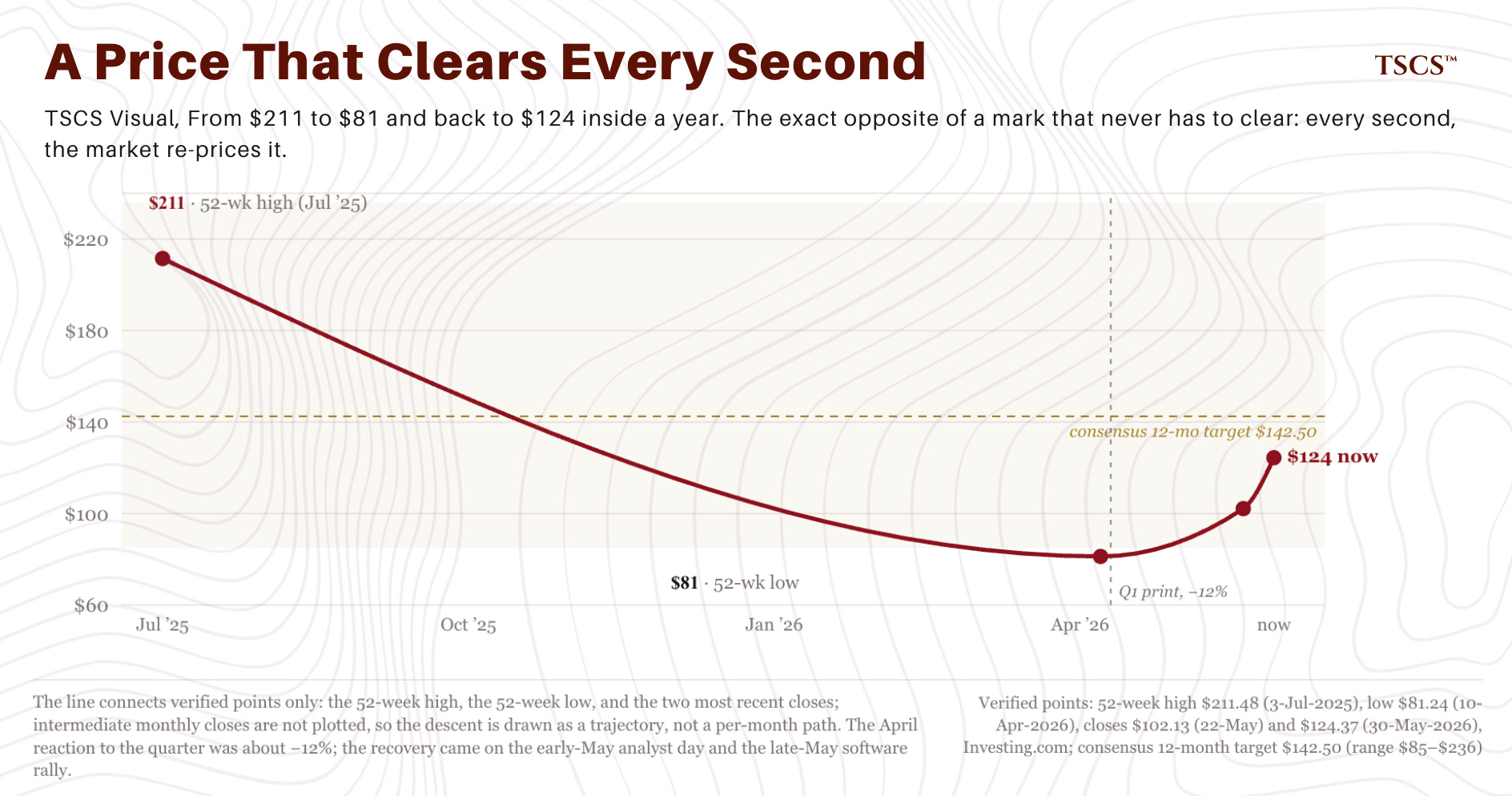

It helps to look at the other end of the spectrum. ServiceNow is one of the most-watched prices in the market, a profitable, growing, cash-generative company. Over the past year the public market took it from $211 to $81 and back to $124, a brutal round trip, because every tick is a real bid that someone has to stand behind. Nobody decided ServiceNow was worth $81. The market discovered it, then discovered it was wrong, in public, with money. CDK’s loan never goes through that. The screen says 47.6 because that’s where the syndicated piece would clear. The BDCs carry it at 71.6 because no one’s forced to test the number. The same dollar of value is treated as a transaction at one end of the spectrum and as an opinion at the other, and the further a position sits from a public market, the more the price is something a manager asserts rather than something a buyer pays.

CDK isn’t the anomaly. It’s the part of the problem that happens to be visible.

It’s visible because it’s breaking. The cooperation agreement, the Fitch listing, the falling earnings, all of it dragged one private credit loan into the daylight where its price could be checked. The 24-point gap looks shocking only if you assume the rest of the cohort is fine. So we went and looked at the rest of the cohort.

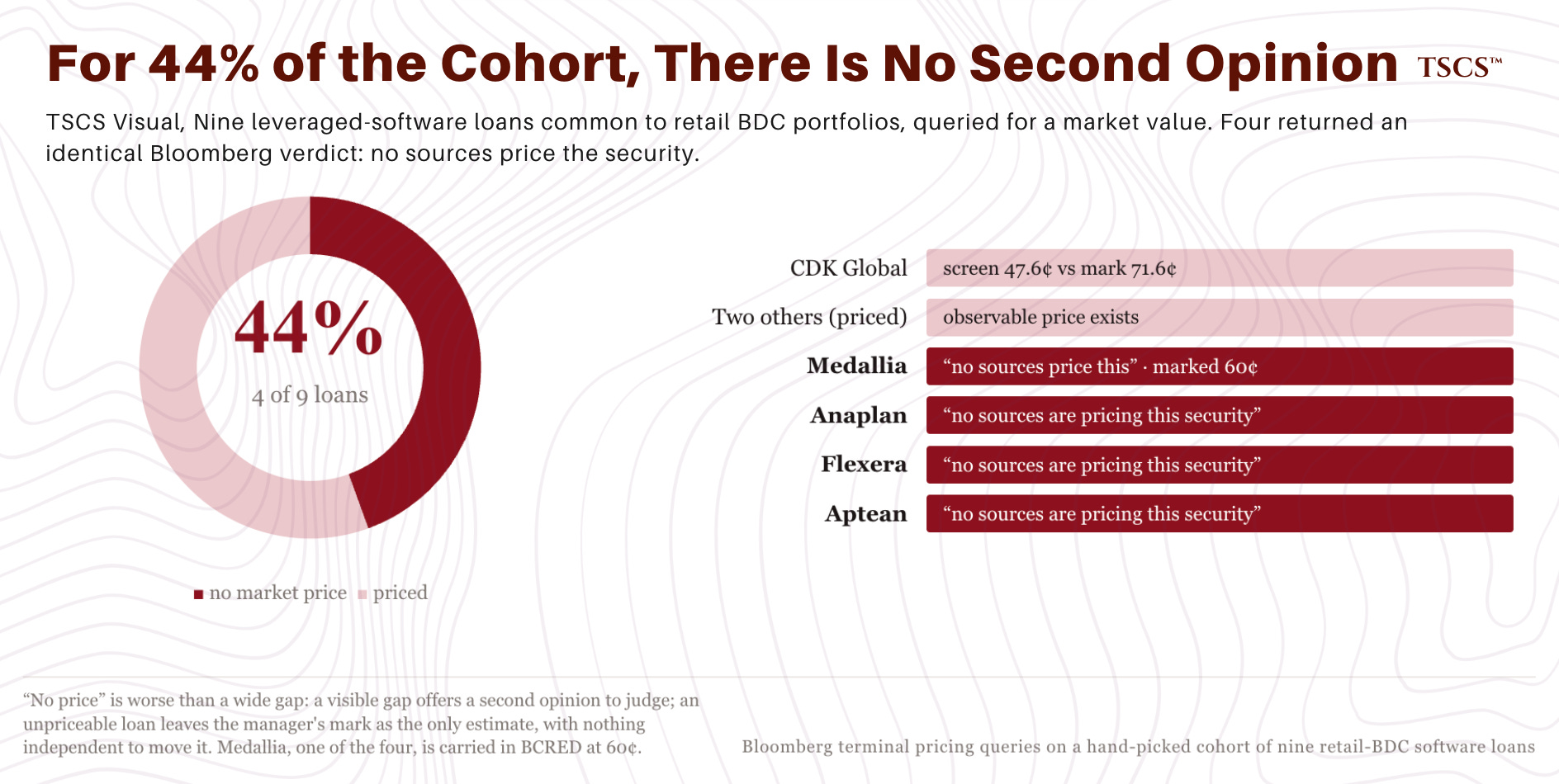

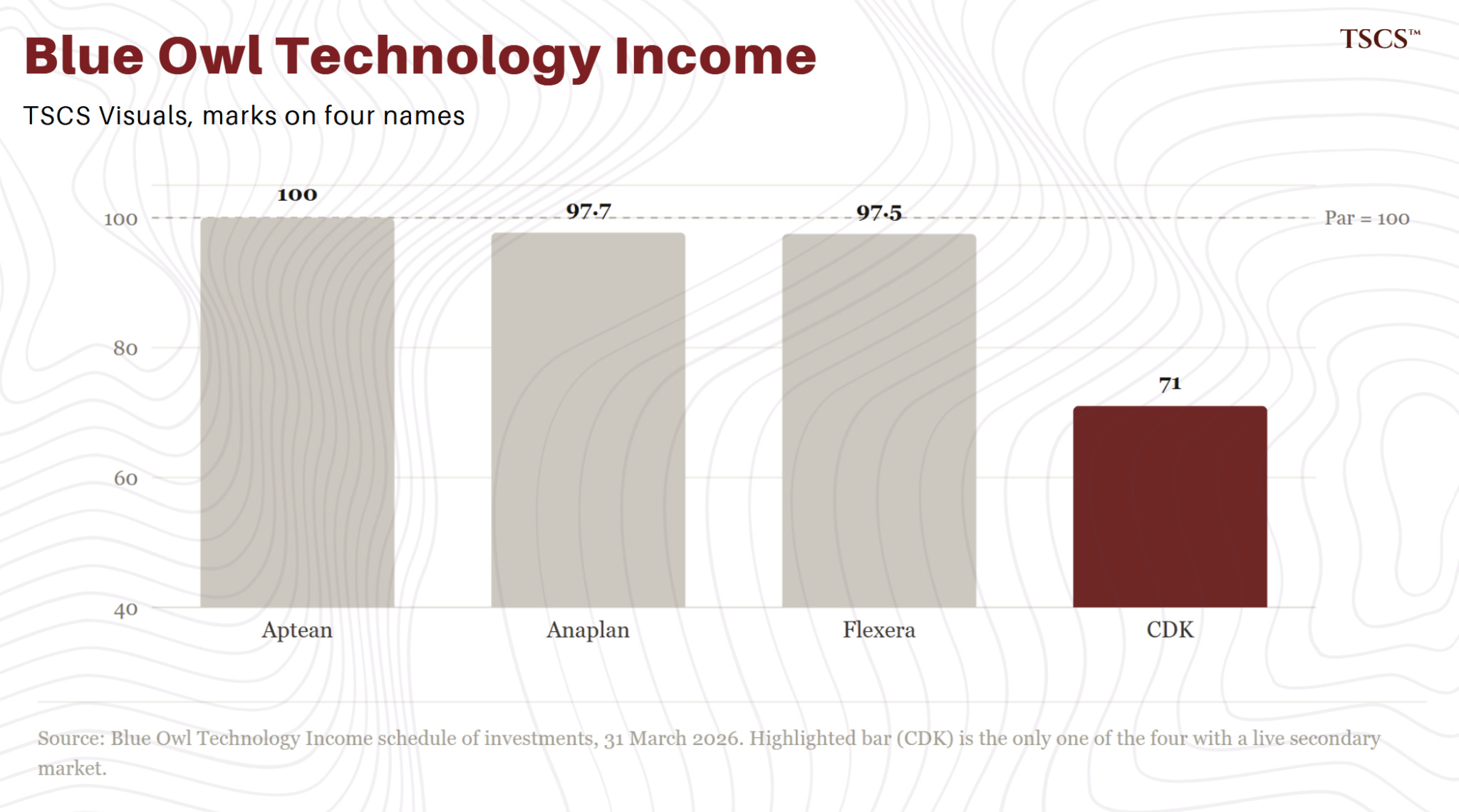

We took the leveraged software loans most commonly found in retail BDC portfolios and asked the terminal a simple question: what is this loan worth? For CDK, however uncomfortable, there was an answer. For four of the nine names we tested, Medallia, Anaplan, Flexera and Aptean, the terminal returned the identical sentence: No sources are pricing this security.

Not a stale price. Not a wide bid-ask spread. No price. For 44% of a hand-picked cohort of loans sitting inside funds sold to the public, there is no observable market value at all. The only number that exists is the one the manager writes down.

This is worse than the CDK gap, not better. A loan with a visible 24-point gap at least has a second opinion you can see and judge. A loan with no market price has no second opinion. The manager’s mark isn’t the high estimate or the low estimate. It’s the only estimate. Nothing independent checks it, and nothing forces it to move.

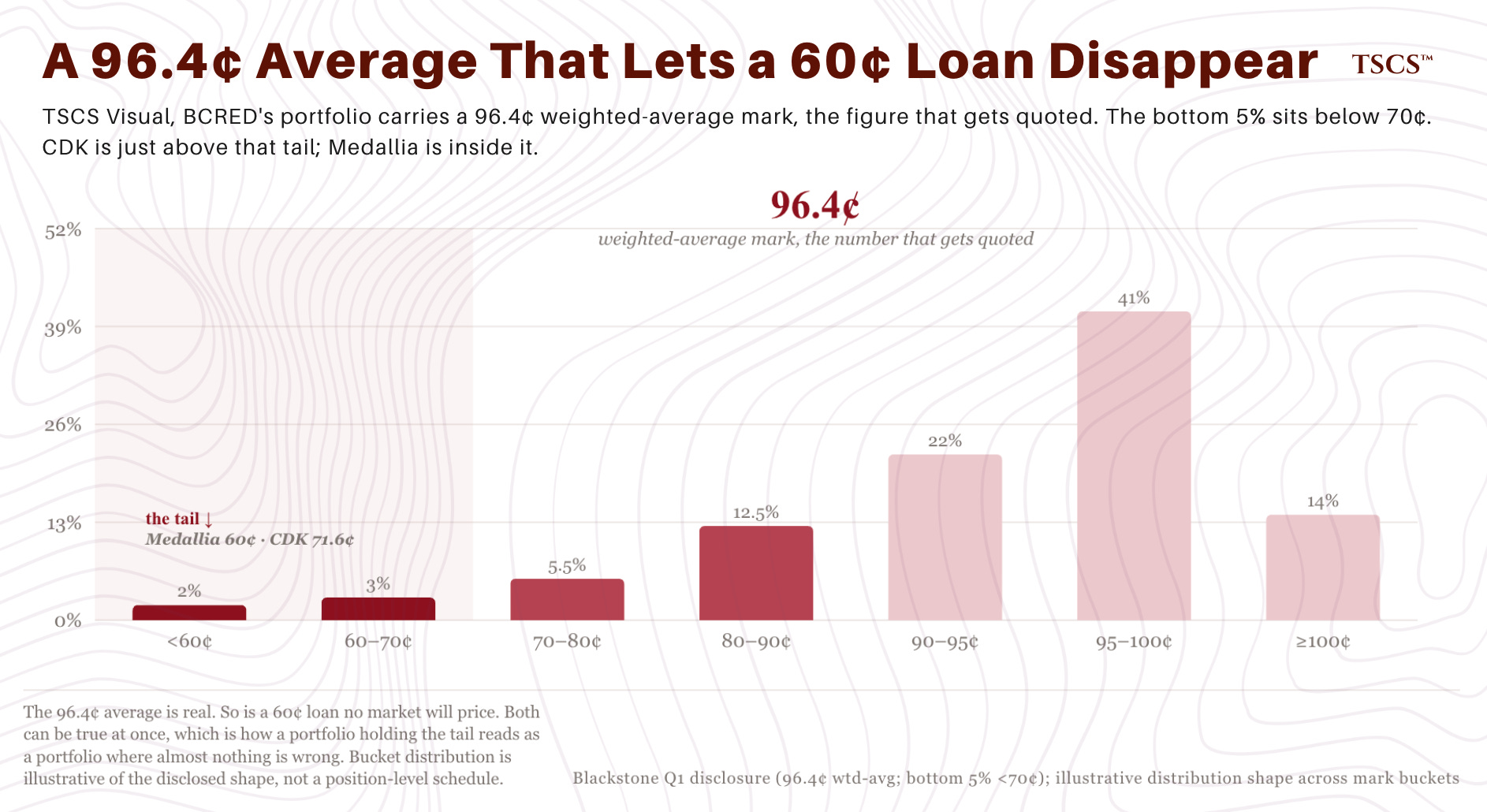

Blackstone, to its credit, has shown the shape of this. On its first-quarter earnings call the firm disclosed that BCRED’s portfolio carries a weighted average mark of 96.4 cents, with the bottom 5% of its loans marked below 70. The 96.4 is the number that gets repeated. The tail below 70 is the number that does not. CDK, at 71.6, sits just above that tail. Some of the unpriceable names sit inside it: Medallia, one of the four loans the terminal would not quote, is carried in BCRED at 60. The 96.4 average is real. It’s also the number that lets a portfolio holding a 60-cent loan, a loan no market will price, read as a portfolio where almost nothing is wrong.

This piece is a collaboration with Leyla Kunimoto, who writes Accredited Insight and has spent the past year taking these vehicles apart fund by fund. The terminal work on the loans is ours. The vehicle-level analysis, which BDCs hold the most of this, how the marks behave from fund to fund, and what the rising use of payment-in-kind interest signals underneath them, is hers.

This problem has two halves, and the loan view without the fund view is half-blind. So we are each sending our readers to the other. If you own any of these vehicles, or advise someone who does, subscribe to both: TSCS here and Accredited Insight here. Today you get the loans and the marks from us; the fund-by-fund companion runs on her side.

The conclusion is shared, and it is this. Across a large and growing slice of the private credit market sold to individuals, the manager’s mark isn’t lagging reality. For much of it there is no observable reality to lag: no market price, no second opinion, and no mechanism that forces the number to move. CDK is the loan you can see. This piece is about the loans you cannot.

What Moves a Mark

A price is a vote. When a syndicated loan trades, a dealer quotes it, a buyer and a seller settle on a number, and a service like Bloomberg’s BVAL turns those quotes into a daily price. The number moves because people with money are forced to act on their opinion. If you think the loan is worth less, you sell, and the price you accept becomes the new mark. The market never asks the lender how it feels. It takes the lender’s transaction and prints it.

A private credit mark isn’t a vote. It’s an opinion, produced once a quarter by the manager, reviewed by a third-party valuation firm that the fund itself engages and pays. The inputs are real enough: comparable spreads, public-company trading multiples, the borrower’s financials, a credit rating. But there’s no transaction at the center of it. Nobody’s forced to act. The manager weighs the inputs, applies judgment, and writes a number, and that number stands until the next quarter, when the manager looks again.

This builds in an asymmetry. A syndicated mark moves continuously, in both directions, because trading is continuous. A private mark moves in steps, and it moves down for essentially two reasons: the public comparables the manager benchmarks against have fallen far enough to drag the model, or the borrower has hit an event, a missed payment, a covenant breach, a restructuring, that the manager cannot decline to recognize. In the space between those two triggers, a private mark can sit still for a year while the business underneath it weakens, and nothing in the machinery is built to stop that.

We don’t have to theorize about the machinery. The managers described it themselves, on their own first-quarter earnings calls.

Apollo was the most explicit, and the most useful, because in describing its own discipline it drew the contrast for us. Marc Rowan said that for Apollo’s direct-lending fund, ADS, the rule is mechanical: when Apollo holds a loan alongside other lenders, it takes the lowest mark anyone has, whether it agrees with that mark or not, because the lowest mark is where someone might actually sell. Apollo maps its book to the syndicated loan index sector by sector, and when a sector falls, the model follows. Rowan’s phrase was that Apollo marks “to current information, not to hope.” He was then blunt about the rest of the industry: marking positions up on day one, common in evergreen funds, “makes no sense” and “leads to mispricing,” and across Apollo’s whole platform such markups “round to zero.”

Now CDK. The loan is carried by BCRED at 71.6 and by HLEND at 71.6, and the market, where it can be seen, is at 47.6. Apollo’s own stated rule, take the lowest mark when others hold the loan, applied to CDK, doesn’t produce 71.6. We’re not refereeing Apollo against the field. One of the largest managers in the business has publicly described a marking discipline the CDK marks don’t appear to meet.

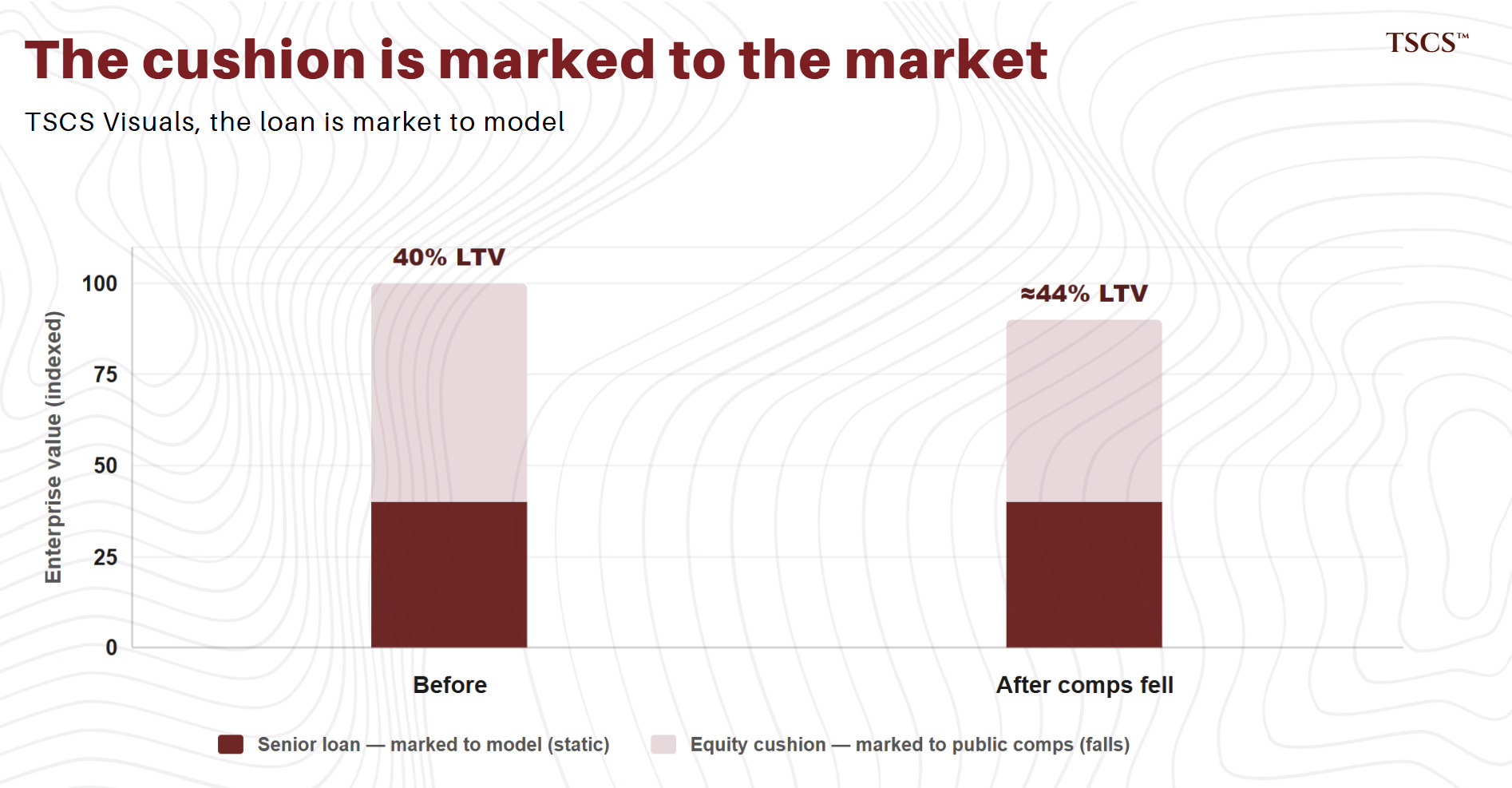

The more revealing comments came from Ares and Blue Owl, and neither was framed as a confession. Both firms were asked about software exposure, and both reached for the same reassurance: loan-to-value in their software books sits around 40%, with billions of dollars of sponsor equity beneath the loan as a cushion. Then both volunteered the same detail. Ares said it had marked the equity value in its software portfolio down, in line with public markets, and that as a result loan-to-value “actually went up slightly.” Blue Owl said its loan-to-values had “ticked up modestly, incorporating moves in public comps.”

The equity beneath these loans is benchmarked to public software multiples. Public software multiples fell. So the equity was marked down. The loan sitting on top of that equity is marked to a model, and the loan didn’t move. The cushion shrank. The thing the cushion exists to protect didn’t. By the managers’ own account, the part of the capital structure tied to a market repriced, and the part tied to a model held still. That’s not a theory of how the gap opens. It’s the gap opening, narrated on an earnings call.

And the cushion itself is a mark. CDK’s sponsor is Brookfield, and Brookfield’s private equity fund carries its CDK equity, 8.08 million shares, at $134.5 million, 17.2% of that fund’s net assets, on the same 31 March date. That’s the equity the lenders point to as their protection. It sits beneath roughly four billion dollars of debt that the market prices at 47.6, and the people who own it carry it at a full, meaningful value. Those two numbers are hard to hold at once, because equity takes the first loss. Either the senior loan is cheaper than the lenders mark it, or the equity is dearer than the sponsor marks it, or the public market is simply wrong about CDK and the insiders are right. We can’t resolve which from the outside. What we can say is that the cushion the lenders lean on isn’t an independent fact. It’s another private mark, set by the sponsor, on an asset with no market price of its own. The mark defends the mark.

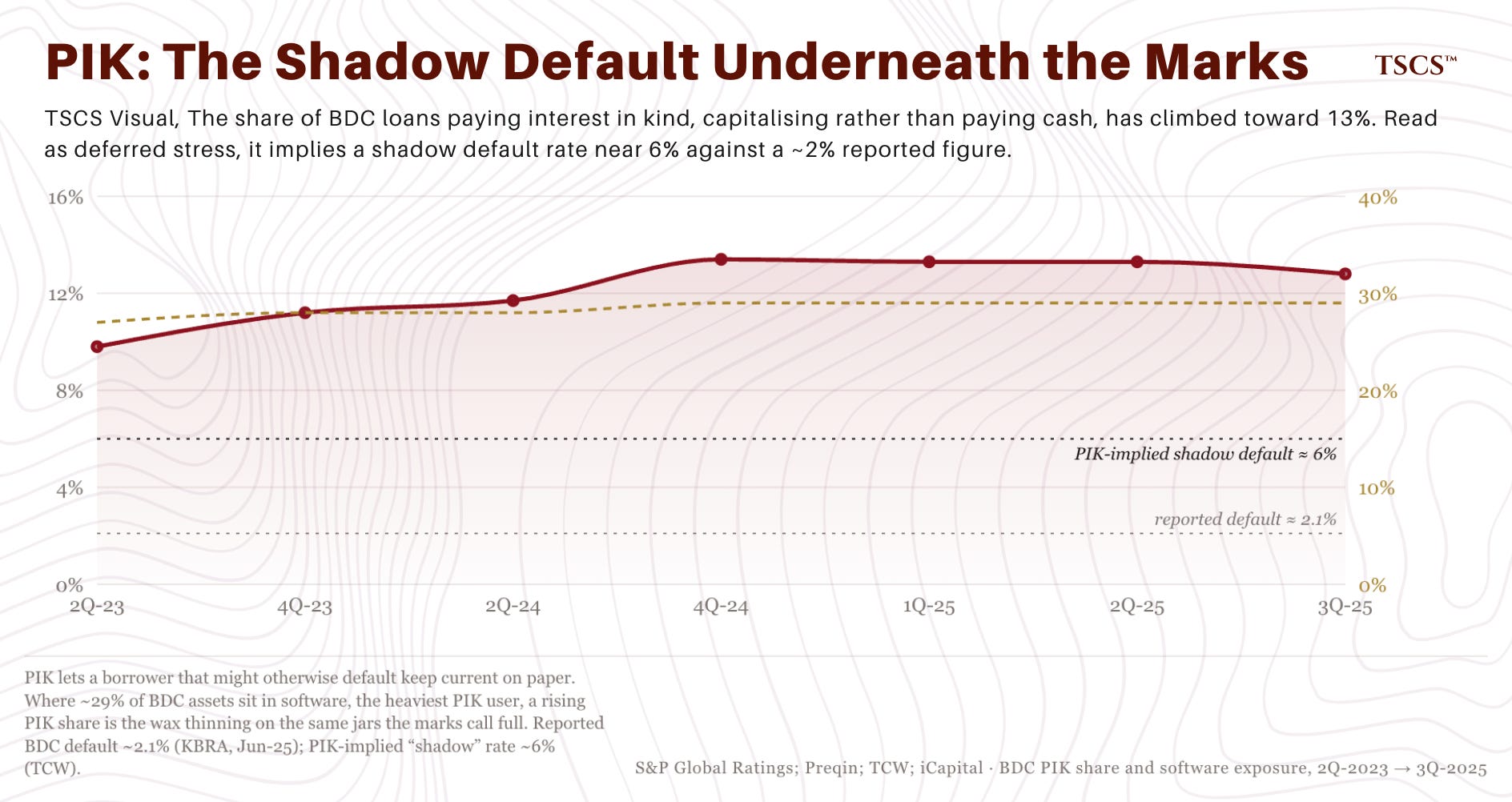

There’s a second mechanism that keeps a mark from moving, and we’ll only flag it here, because Leyla Kunimoto takes it apart properly later: payment-in-kind interest. When a borrower can no longer comfortably pay cash interest, many private loan agreements let it pay in kind instead, folding the interest into the principal. The loan keeps accruing. It keeps counting as performing. The mark stays up. Nothing about the borrower has improved. It has simply stopped paying cash, and the structure absorbs that without registering it. What’s been happening to the use of payment-in-kind across these funds, and what it signals, is Leyla’s subject.

Here’s the strongest case against us, and it’s serious. A private mark isn’t supposed to equal a distressed secondary print. A lender that can hold a loan to maturity, that isn’t a forced seller, isn’t a desk dumping paper into a thin market, and it’s legitimate for that lender to carry the loan above the panic price. A mark estimates recoverable value, not today’s exit price, and for a healthy loan those are different numbers. All of it is true.

It doesn’t dissolve the problem, for two reasons. First, it explains a level, not a direction. It can justify why a mark sits above the market on a given day. It can’t justify why a mark sits still for a year while the borrower’s earnings fall, its leverage climbs, and its interest payments quietly turn into IOUs. Second, the defense rests on the holder not being a forced seller. For a loan held by a closed-end institution, fair. For a loan held inside a semi-liquid retail vehicle that offers its investors quarterly redemptions, that’s precisely the assumption that fails under stress, which is the rest of this piece.

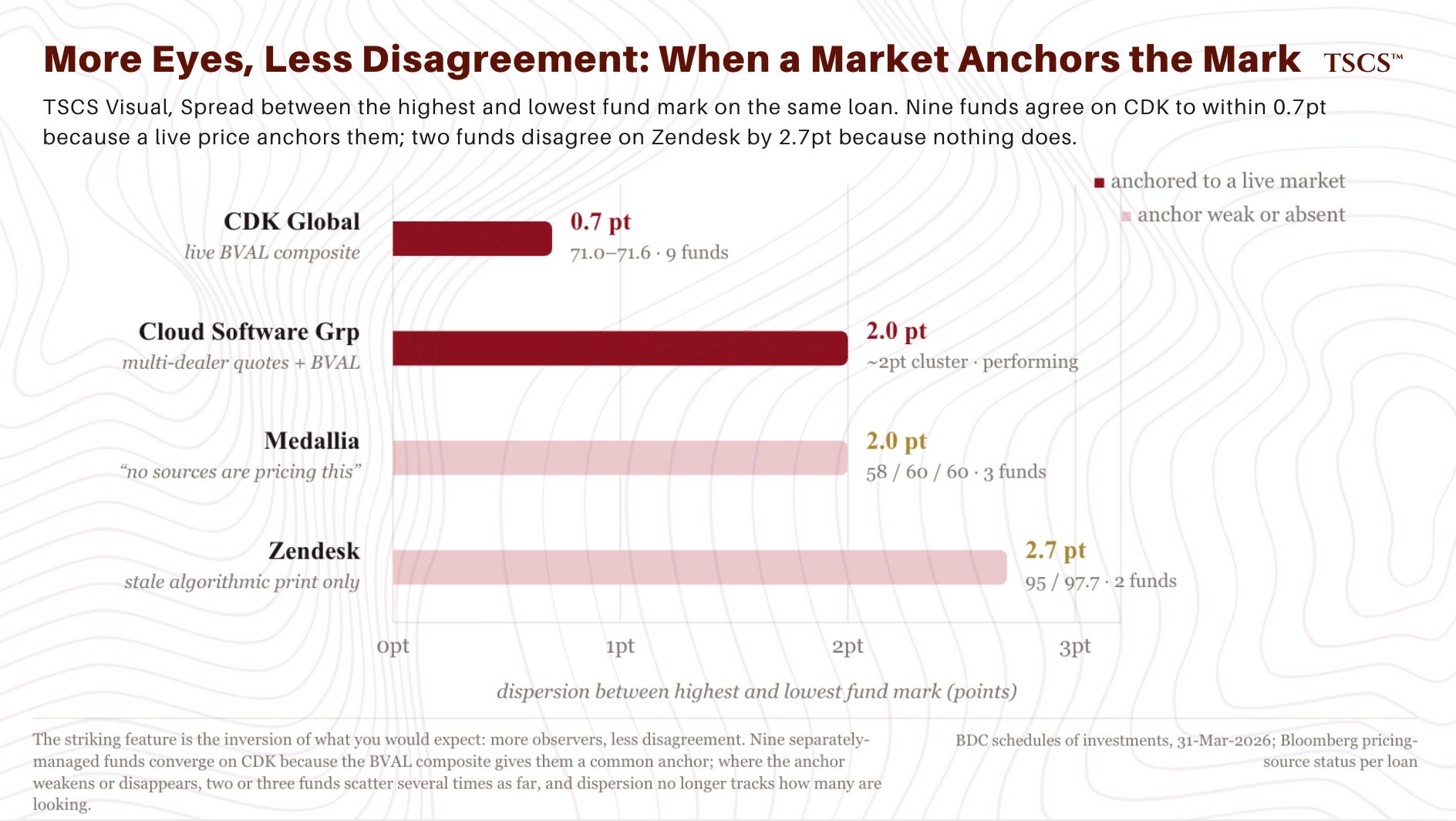

So this isn’t a claim that every private mark is wrong. Where a loan still has a market, the machinery works. Cloud Software Group is the clean case: a performing borrower whose loan draws live quotes from more than one dealer, a BVAL composite, and BDC marks, all clustering within roughly two points of one another. When liquidity exists, the marks converge on it. The right question is never whether the mark is too high. It’s whether anything would force the mark to move, and for a large and growing share of the loans sitting in funds sold to the public, the honest answer is no.

Down in Lockstep

For most of the loans in this universe, nothing forces the mark to move. For some of them, like CDK, something does, and the way it fell is the tell.

Across the BDC syndicate that holds the CDK term loan, nine funds disclose the position consistently enough to give a clean quarterly mark history back to the end of 2023. Those nine are drawn from Prism’s BDC analytics database (prismalts.com) and spot-checked against the underlying filings. They’re the funds we work with here.

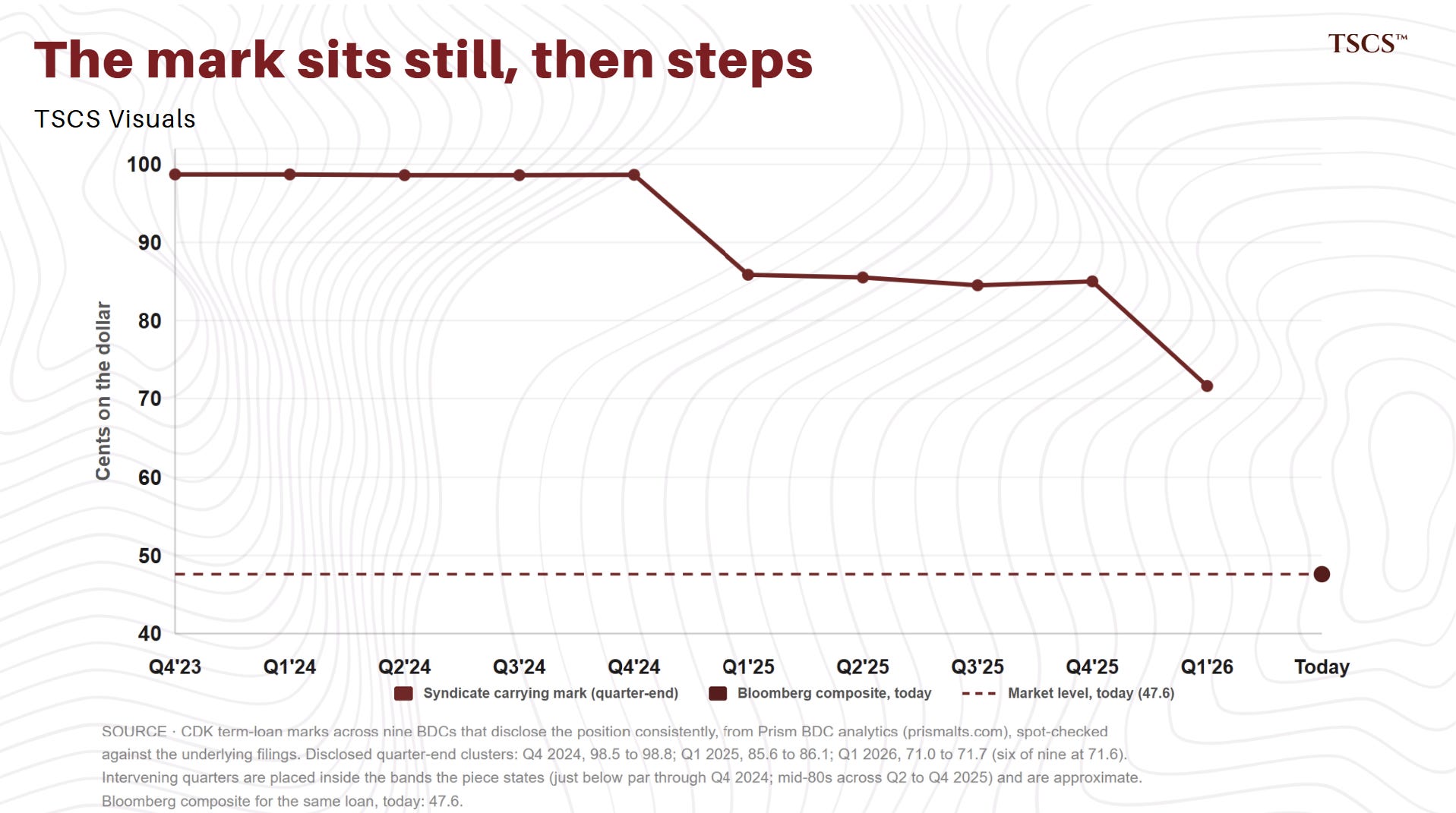

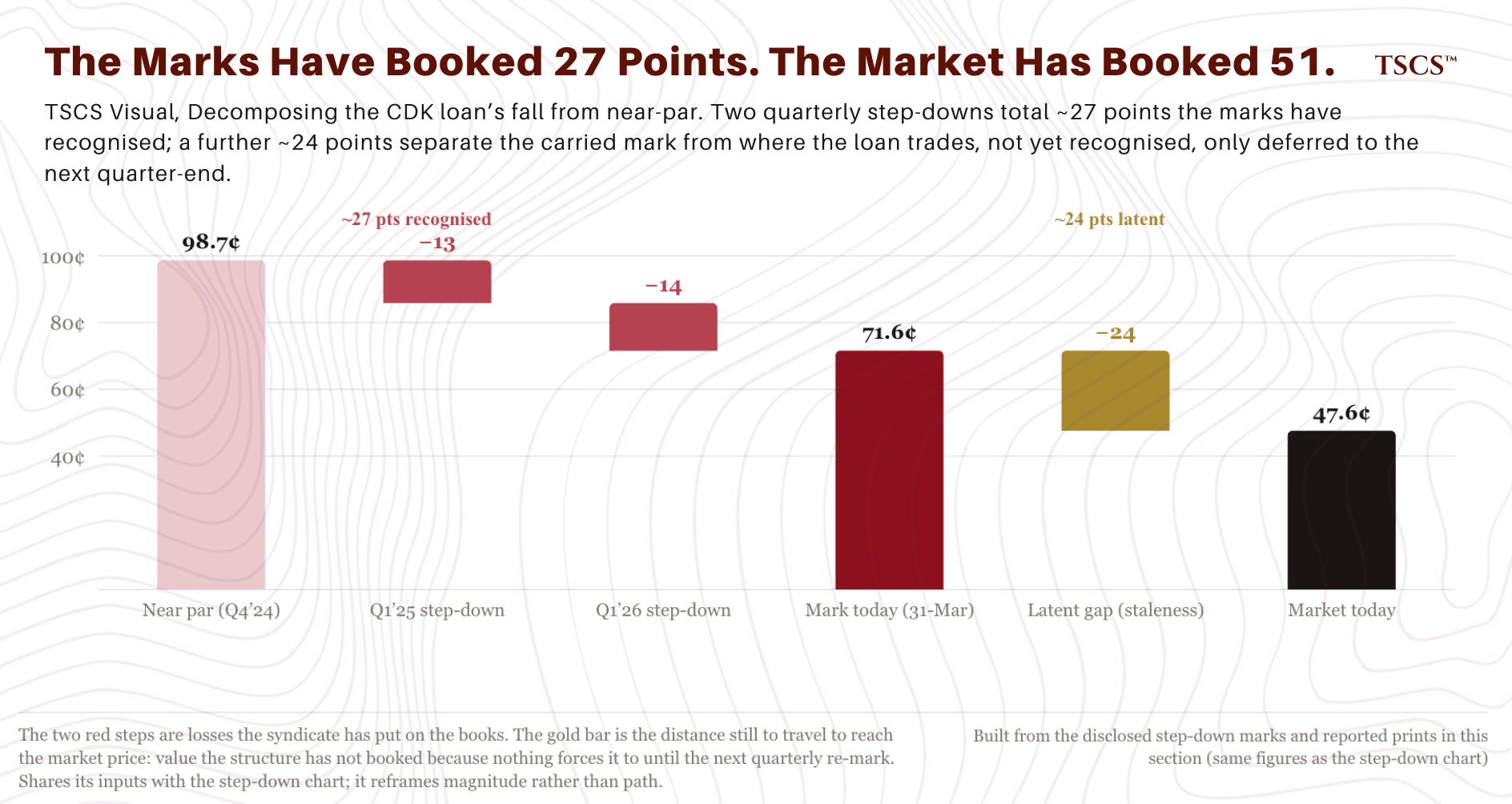

From the fourth quarter of 2023 through the fourth quarter of 2024, every fund in the syndicate of nine carried the loan in a narrow band just below par. BCRED, HLEND, BlackRock’s private credit fund, the Antares funds, the HPS funds, Blue Owl Technology Income, Ares Strategic Income, First Eagle. The Q4 2024 marks ran from 98.5 to 98.8. Five quarters of effective stasis.

Then, in a single quarter, every fund in the syndicate marked the loan down to roughly 86. Not a drift. A step. Nine separately managed funds, with nine separate boards and nine separate valuation processes, agreed in the same quarter to drop CDK by roughly thirteen points. The Q1 2025 cluster landed between 85.6 and 86.1. The dispersion, across nine funds, was less than a point.

Then three quarters of drift within a band. Through Q2, Q3 and Q4 of 2025 the marks stayed in the mid-80s, moving up and down by a couple of points but reverting to the same range each quarter. The cooperation agreement hadn’t yet been signed. The EBITDA decline hadn’t yet been reported. The Fitch concern listing hadn’t yet happened.

Then a second step. In the first quarter of 2026, every fund in the syndicate, again at the same time, marked the loan down by another fourteen points. The Q1 2026 cluster sits between 71.0 and 71.7, with six of the nine funds reporting 71.6 and the two lowest, Blue Owl Technology Income and Ares Strategic Income, at 71.0. Two coordinated step-downs, totalling roughly twenty-seven points, with three quarters of drift between them.

The convergence itself is partly explicable on innocent grounds. Nine funds estimating the fair value of the same loan, using similar inputs, the BVAL composite, public-company software comparables, the borrower’s reported financials, ratings, ought to produce similar marks. Some of these funds may share the same third-party valuation firms, which would mechanise the convergence further. None of that is by itself evidence the process is failing.

What’s harder to dismiss is the shape of the moves and the absence of any divergence during the deterioration. Across nine funds and the three quarters between the two step-downs, no fund marked CDK ahead of the syndicate, none marked it down before the other eight, and none pre-empted the second step despite the credit weakening continuously underneath them. The system has a particular property: it doesn’t move until something forces all of it to move at once. The level the syndicate arrives at may be defensible. The path it takes to get there is stasis and synchronized jumps.

That shape has two consequences. The first is that a private mark sits still and then steps. The Q1 2025 and Q1 2026 moves arrived as single-quarter drops of more than ten points, not as gradual repricings spread across the months in between. The cumulative magnitude over a year may be similar to what a syndicated loan would produce. The path is not. The signal arrives in different shapes.

The second is that the mark reacts to a quarterly information set, not to the continuous deterioration of the underlying credit between quarter-ends. The syndicate marked CDK down in Q1 2025, then sat at the new level for the rest of the year while the loan’s BVAL composite drifted lower and the borrower’s earnings weakened. The second step came at the next quarter-end, on the next set of inputs. Whether the trigger was the borrower’s reported Q4 2025 results, a fresh look at public software multiples, a sector-spread move, or some combination isn’t knowable from this data alone. What is knowable is the cadence: marks move when the model is forced to move, on the quarter, and not before.

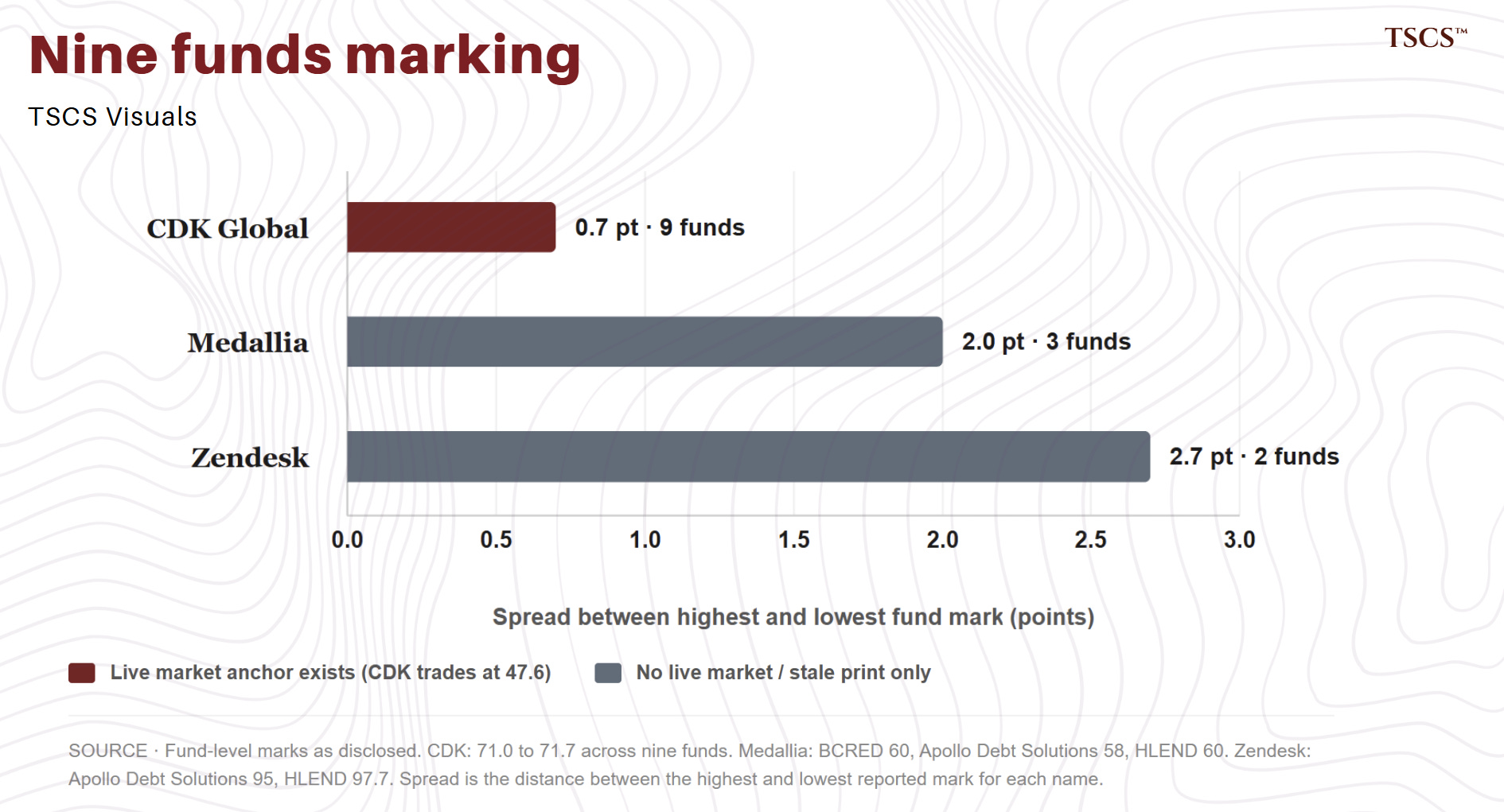

Now the other half. The same nine funds, looking at the same loan, on the same quarter-end date, agree to within half a point. The same funds, looking at loans where no public market exists to drag the model, disagree by more. Medallia, the loan the Bloomberg terminal returned “No sources are pricing this security” against, is carried by BCRED at 60, by Apollo Debt Solutions BDC at 58, and by HLEND at 60. Two points of dispersion. Zendesk, with only a stale algorithmic print, is carried by ADS at 95 and HLEND at 97.7. 2.7. The gap is small in absolute terms, but it’s several times the half-point the syndicate agrees on for CDK, and it opens precisely where the anchor disappears. When the model has a market to anchor on, the marks converge. When it doesn’t, they drift apart.

One last piece, and it sets up everything that follows. Blue Owl Technology Income holds about $39 million of the CDK loan at par. In absolute size it’s one of the larger positions in the cohort, though once you count BCRED’s holding through its Emerald JV, BCRED’s is larger. What makes Blue Owl Technology Income the one to watch is concentration. It’s the BDC built explicitly around the thesis that sponsor-backed software lending offers superior risk-adjusted returns, and as a share of its own book it’s the most exposed of any vehicle here, to CDK and to the wider set of disputed names. Its CDK mark, 71.0, sits at the bottom of the syndicate range. Which vehicles hold the most of this, and what that means, is where Leyla’s analysis begins.

The evidence reduces to this. The marks fall in coordinated steps, lagging the market, all moving together. Between the steps they sit still while the credit underneath them weakens. Once they’ve stepped, they’ve agreed, all to within half a point of each other. The most recent disclosure, the 31 March quarter-end, has the syndicate at roughly 71.6. The Bloomberg composite for the same loan today is 47.6. Some of that 24-point gap is the natural staleness of a quarterly mark, and that staleness is itself the point: the number on the retail investor’s quarterly account statement is, by design, a number from a quarter ago, and at the next quarter-end it’ll move, and at the one after that it’ll move again, in the same coordinated step as the rest of the syndicate. CDK, the loan we can see, is the data point. For the loans we cannot see, the same machinery is running on a longer leash, and the only number the public has is the manager’s.

The next section, who actually holds the most of this, is the half of the work that is Leyla’s, and it is what Accredited Insight does every quarter as the schedules land. If the fund-by-fund view is the one you want kept current, that is her beat: Accredited Insight. The loan-and-macro side you have been reading is ours, and it does not stop: TSCS, if you are not already on it

Which Vehicles Hold the Most

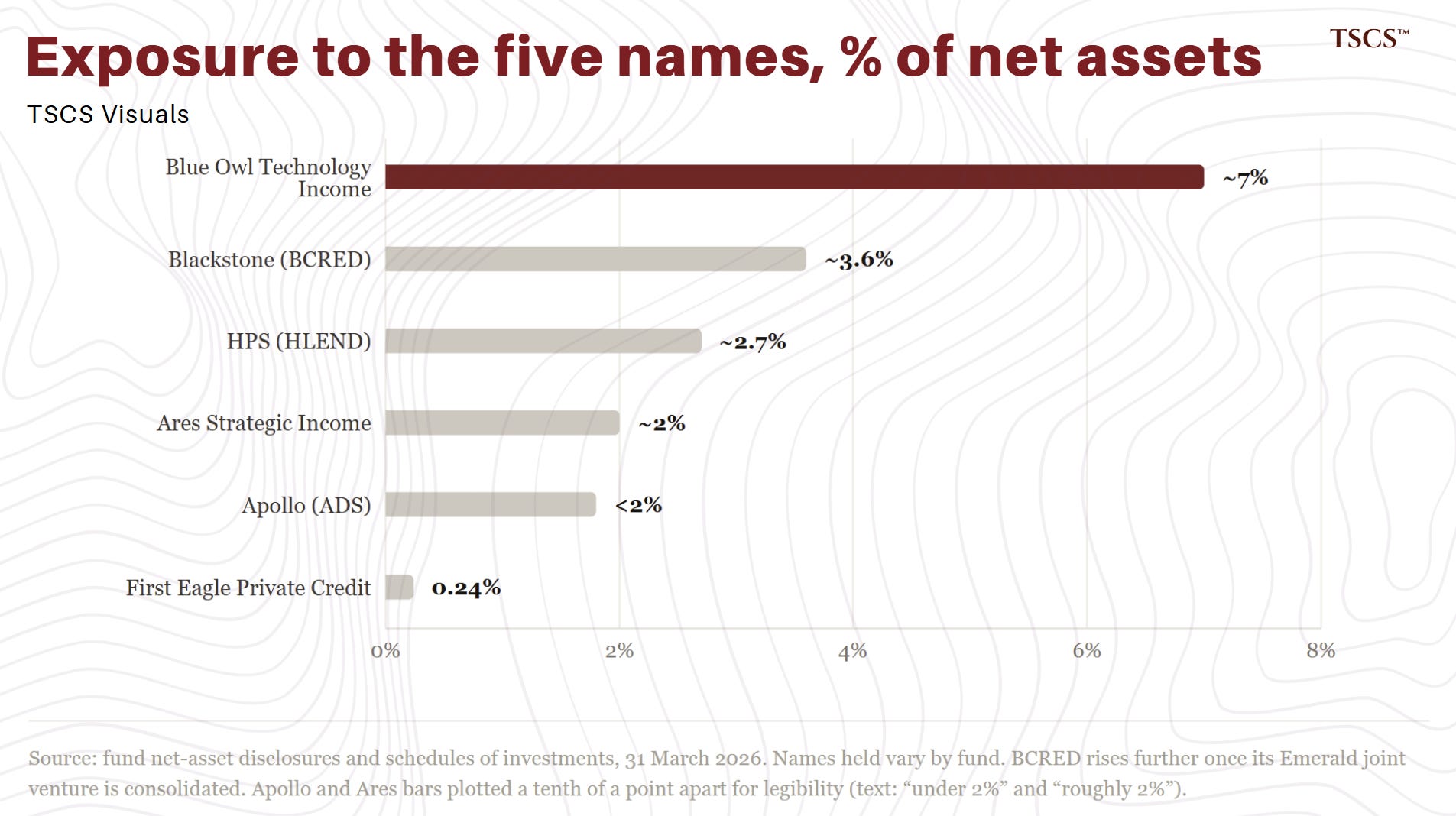

So we did for the vehicles what we did for the loans. We took the five disputed names, CDK and the four the terminal wouldn’t price, and asked, fund by fund, how much of each book they account for. This isn’t a forecast of losses. It’s a map of where the unpriceable risk actually sits, and it isn’t evenly spread.

Measured as a share of net assets, the spread runs from trivial to material. First Eagle’s private credit fund holds only CDK among the five, at 0.24% of its book. Apollo’s ADS holds Anaplan and Medallia among them, and $230 million of Anaplan alone, but it’s a $14.5 billion fund, so the total comes to under 2%. Ares Strategic Income, holding CDK, Flexera and Aptean, comes to just under 2%. HPS’s HLEND, holding CDK, Medallia and Flexera, to roughly 2.7%. BCRED holds all five and lands around 3.6% in its main fund, more once its Emerald JV is folded in. And at the top, by a clear margin, sits Blue Owl Technology Income: the same names run to nearly 8% of its net assets, close to twice BCRED and several times the larger diversified funds. The vehicle built around software lending is the vehicle most concentrated in the software loans no market will price. That’s not a coincidence. It’s the strategy working exactly as designed, in both directions.

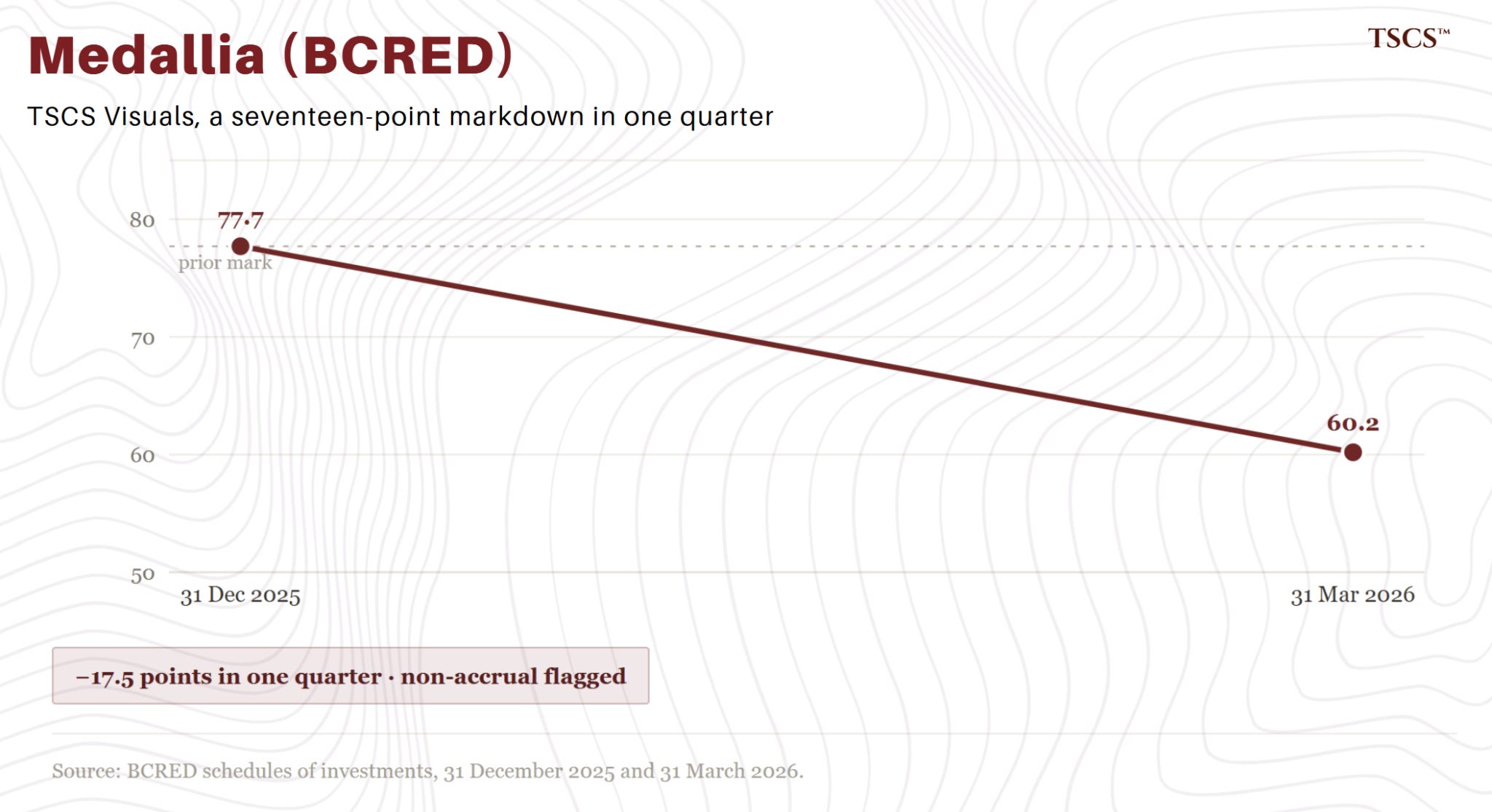

Inside a single book, the marks on these names tell the story in miniature. In Blue Owl Technology Income, Aptean is carried at par, Anaplan at 97.7, Flexera at 97.5, and CDK, the one with a visible market, at 71.0. In BCRED the same pattern holds, and one name breaks it: Medallia. BCRED marked Medallia at 77.7 at the end of December and 60.2 three months later, a seventeen-point drop in a single quarter, and added a non-accrual footnote alongside it.

The other unpriceable names didn’t move. Medallia moved because it stopped paying, and a loan that stops paying is the one event a manager cannot decline to recognize. Strip Medallia out, and every name with no market price sits at or near par. Nobody has tested those values. Nothing has forced them off par. That’s the whole mechanism, visible inside one fund’s schedule.

Which brings us to the quiet version of the same problem: payment-in-kind. The reflex is to read rising PIK as hidden distress, a borrower that can no longer pay cash. That reflex is mostly wrong, and the accurate version is worse.

Take Blue Owl Technology Income again. Its PIK interest income rose 27% year on year, from $6.2 million to $7.9 million, and climbed from 4.4 to 5.8% of total investment income, while total investment income itself fell. A larger share of what the fund books as income is now paper it isn’t collecting in cash. The fund’s own filing heads off the distress reading directly: substantially all of its PIK, it says, was structured that way from inception, not switched on because a borrower hit trouble. Take that at face value. It’s true of a great deal of sponsor-backed software lending, where a company in a growth phase is meant to plough cash into the business rather than service interest, and the loan is written to allow it.

But structured PIK isn’t reassuring in the way the disclosure implies. It’s the same disease as the marks. A loan that was always going to pay in kind can never miss a cash payment, because it was never going to make one. The single event that forces a manager to recognize trouble, a missed cash coupon, has been contracted out of existence at signing. Medallia is what it looks like when that tripwire still exists and gets tripped: a markdown to 60 and a non-accrual flag. Structured PIK removes the tripwire entirely. The borrower can weaken for years, and the loan will keep accruing, keep counting as performing, and keep its mark, because the structure was built so that paying in kind is normal rather than a signal. The cushions are a private mark. The marks have no market. The income is increasingly paper. One number, moving only when something forces it, inside a structure designed so that less and less is able to.

How This Resolves

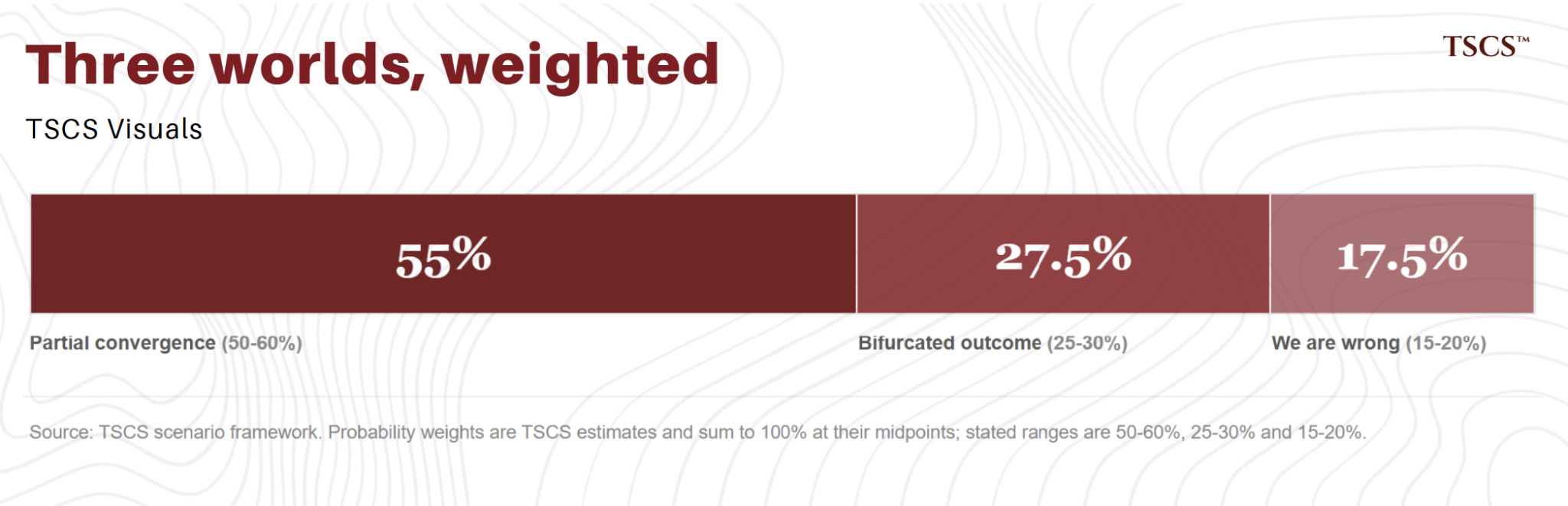

We’ve shown you a gap and a mechanism. We haven’t shown you a catalyst, and without one a gap can stay open for years. So we hold this as a distribution of outcomes over the next eighteen months, with rough weights we’ll state plainly and expect to be argued with.

The first, and the one we think most likely at something like fifty to sixty percent, is partial convergence. The lockstep we traced on CDK continues across the cohort. Over four to six quarters a subset of the names, call it a third to two fifths by exposure, takes the kind of coordinated step-downs CDK has already taken, forced by the things that force them: year-end auditor sign-off, a named default, a redemption wave that makes a manager sell. The rest hold within a few points of where they are. The aggregate markdown lands somewhere around eight to twelve points. At the cohort level the thesis is broadly right. At the level of the worst names, and the vehicles that hold them, it’s very right.

The second, at twenty-five to thirty percent, is the bifurcated outcome. The worst names, CDK and the vacuum names with deteriorating borrowers underneath, take thirty points or more. The rest hold roughly flat. The spread closes from the bottom rather than the top. The aggregate damage looks similar to the first case, but it’s concentrated, and that makes the vehicle ranking the whole game: the only question that matters becomes which funds hold the bottom of the distribution. The section above is the map for this one.

The third, at fifteen to twenty percent, is that we’re wrong. The marks hold, broadly, within five points of where they sit today. Some combination of the things the bulls point to does enough work: the equity cushions turn out to be real, the liability management exercises repair the credits rather than deferring the reckoning, rate cuts open refinancing windows, the borrowers grow into their leverage, and the valuation process we’ve treated as toothless, the paid agents, the auditors, the boards, turns out to be doing more than we credit it for. We don’t think this is the base case, but it’s a real outcome and we’re not going to pretend otherwise. A mark that never has to clear can stay wrong in our direction as easily as in theirs.

One rebuttal deserves a direct answer here, because the managers lead with it. Blue Owl sold $1.4 billion of senior secured loans at 99.7 cents on the dollar this year, and points to that as proof the marks are real. It’s proof that the salable names were salable. It says nothing about CDK, or Medallia, or the four names no one will quote. You don’t test a mark by selling the paper that was never in question.

So watch the things that would move us. What would tell us we’re wrong, and push us toward the third case. The gap on the names that do have a market, CDK first among them, compresses rather than widens at the next quarter-end. The public software comps the marks lean on recover. Aggregate non-accruals stay flat, and the next two names we’d expect to break don’t break within a year. What would tell us we’re right. CDK steps down again at the 30 June quarter-end, on the cadence we traced. Two or more cohort names take twenty-point markdowns in the next two quarters. The discount to NAV on the software-heavy BDCs widens past where it’s traded before. Reorganized-security disclosures, the quiet tell that a loan has stopped pretending, start showing up in the cohort filings.

The convenient thing about a quarterly mark is that it tells you when to look. The next set of schedules lands in August. The cadence we’ve shown you says the lockstep either steps again or it doesn’t. We’ll be watching the same filings you can.

Positioning

We size to the distribution, not to the case we think is most likely. If there’s a fifteen to twenty percent chance we’re simply wrong, nothing here is a position for conviction money. These are asymmetric expressions, sized to survive the third scenario.

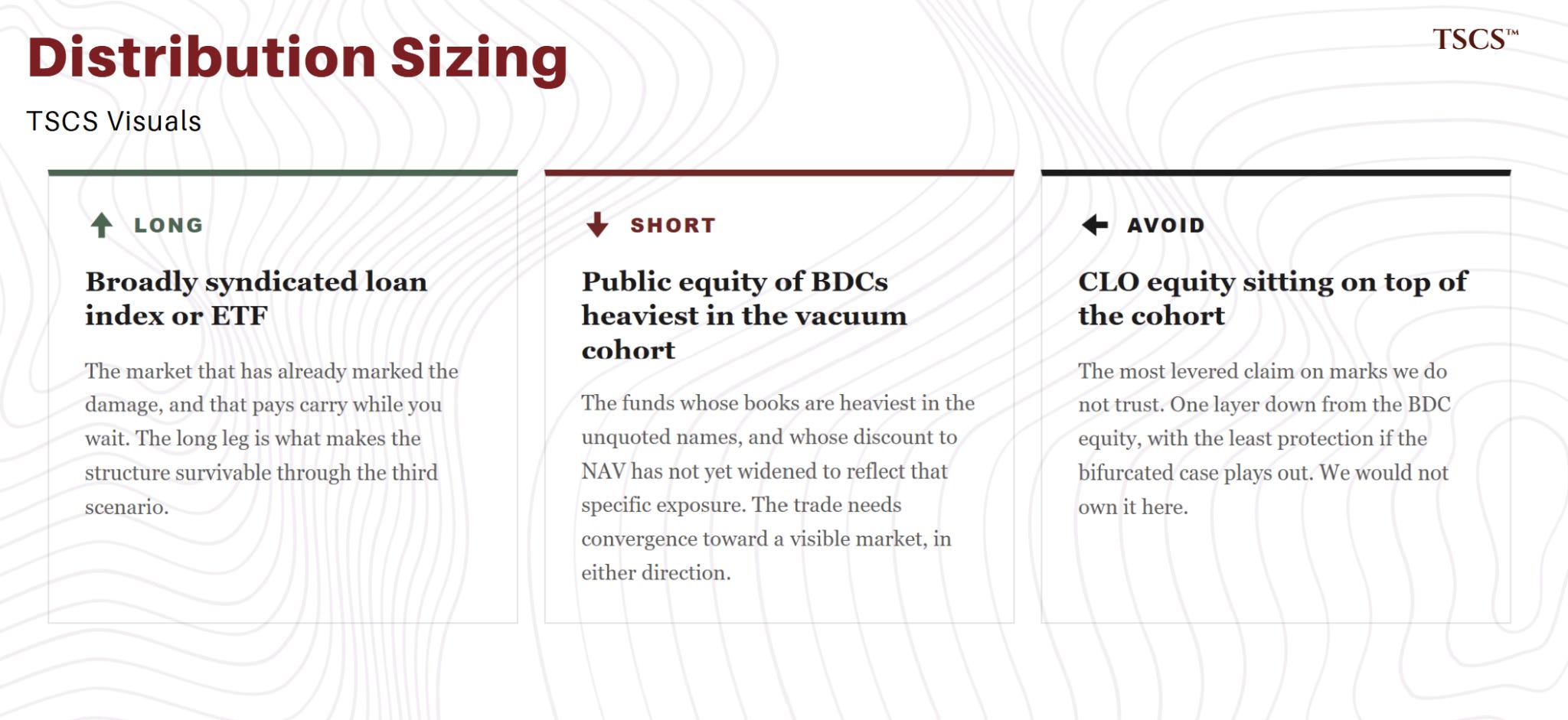

For an institution, the cleanest expression is relative rather than directional.

Long the syndicated loan market, which has already marked the damage, against short the public equity of the BDCs that haven’t. The funds whose books are heaviest in the vacuum cohort, and whose discounts to NAV haven’t yet widened to reflect it, are the short. A liquid loan index or ETF is the long.

The trade doesn’t need the marks to collapse.

It needs them to converge, in either direction, toward a market that’s already visible, and it carries, because the loan side pays.

One layer down, CLO equity sitting on top of this cohort is the most levered claim on marks we don’t trust, and we wouldn’t own it here.

For an accredited investor sitting directly in one of these vehicles, the position is simpler and more uncomfortable: know what you own, and know how to leave. Pull the schedule of investments for your fund. Find the software names. Cross them against the cohort in the section above.

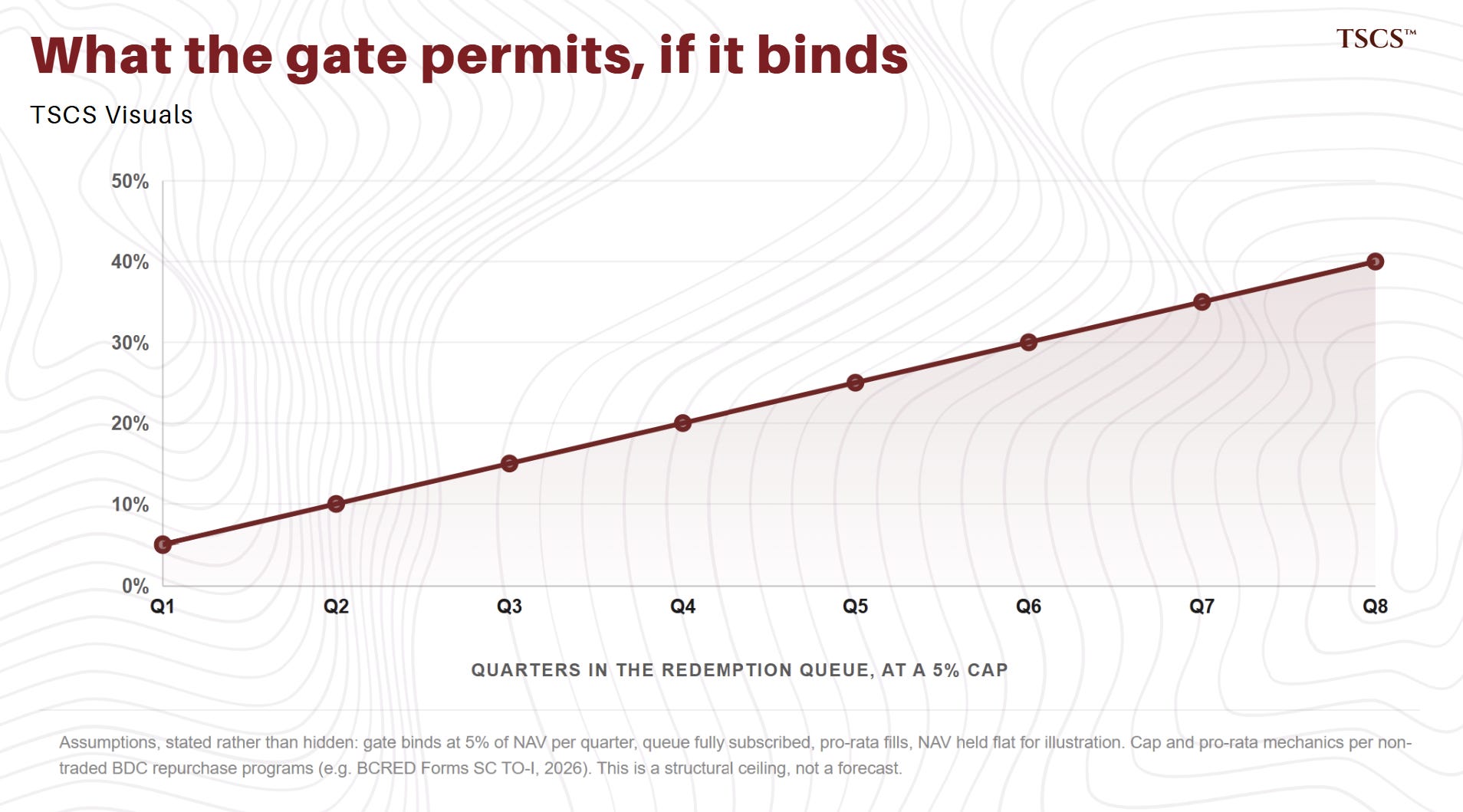

If your fund ranks high on exposed gap, the question is no longer whether the mark is right today. It’s whether you’d rather act before the next quarterly mark steps or after. These wrappers are semi-liquid by design. Redemptions are capped, usually near five percent of net asset value a quarter, and filled pro rata, so that the manager is never forced to sell into a thin market to meet them.

That protection cuts both ways. It was built for exactly the scenario where everyone reaches the same conclusion at the same quarter-end, which is the scenario the lockstep makes more likely rather than less, and in that scenario you don’t get out.

You get a fraction out, at a net asset value the manager set and the market hasn’t yet caught, with the rest of your request rolled behind everyone else’s. The word “semi-liquid” carries a lot of weight in the pitch, and most of that weight is bullshit when it counts. BCRED alone ran $1.4 billion of net outflows last quarter as repurchases rose.

You can’t beat this by being early. The exit is rationed, on the manager’s number, exactly when you’d most want to leave.

None of this is a forecast that the worst happens. It’s a recognition that you’re being asked to hold an asset at a price nobody is forced to defend, in a wrapper that lets you out only on the manager’s terms, for a yield that hasn’t, so far, compensated for either.

The Stamp and the Oil

Return to Piraeus. The danger in those storerooms was never the vinegar. Bad oil is an ordinary misfortune; some jars go off, and a market that can price oil absorbs a bad jar the way it absorbs a bad harvest. The danger was the seal, and the comfort the men took in it, the quiet conviction that a stamp they could not test was the same as oil they could not see. The wisest man in Piraeus was not the one who knew which jars were good. No one could know that. The wisest was the one who knew he did not know, and held his storeroom accordingly, not as a counted fortune but as a wager on every wax seal he had never broken.

A large and growing part of the private credit sold to individuals is a storeroom of sealed jars. CDK is the one that got opened. Its holders carry it near 71.6; in the market where it actually trades, it changes hands near 47.6. That broken seal proves nothing about Medallia or Anaplan or Flexera or Aptean, which sit in the dark at their holders’ marks and may well be sound. It proves only what the tavern-keeper proved: that the stamp is not the oil, and that the part of the book where the wax has never been broken is not a measured fortune. It is a position held on faith, marked by the people who sold it, and worth exactly what the next buyer will pay to take it sealed.

So invert it, as Munger said to. Do not ask which of these marks are right. Ask which of them could ever be shown to be wrong, and by whom, and when. For most of this book, the honest answer is: no one, by nothing, until the jar is opened.

A companion note on ServiceNow

Separate from the piece above, and under my byline rather than Leyla’s. Several of you asked where we stand on ServiceNow after the quarter, and I said it would land with this post. Here it is, a single-name update by request rather than a cohort piece.

The private credit piece above is about prices that never have to clear. ServiceNow is the opposite, and that’s the reason it sits in the same note. Its price clears every second, which is why the stock could fall from $211 to $81 and recover to $124 inside a year. The question is what the recovered price is worth.

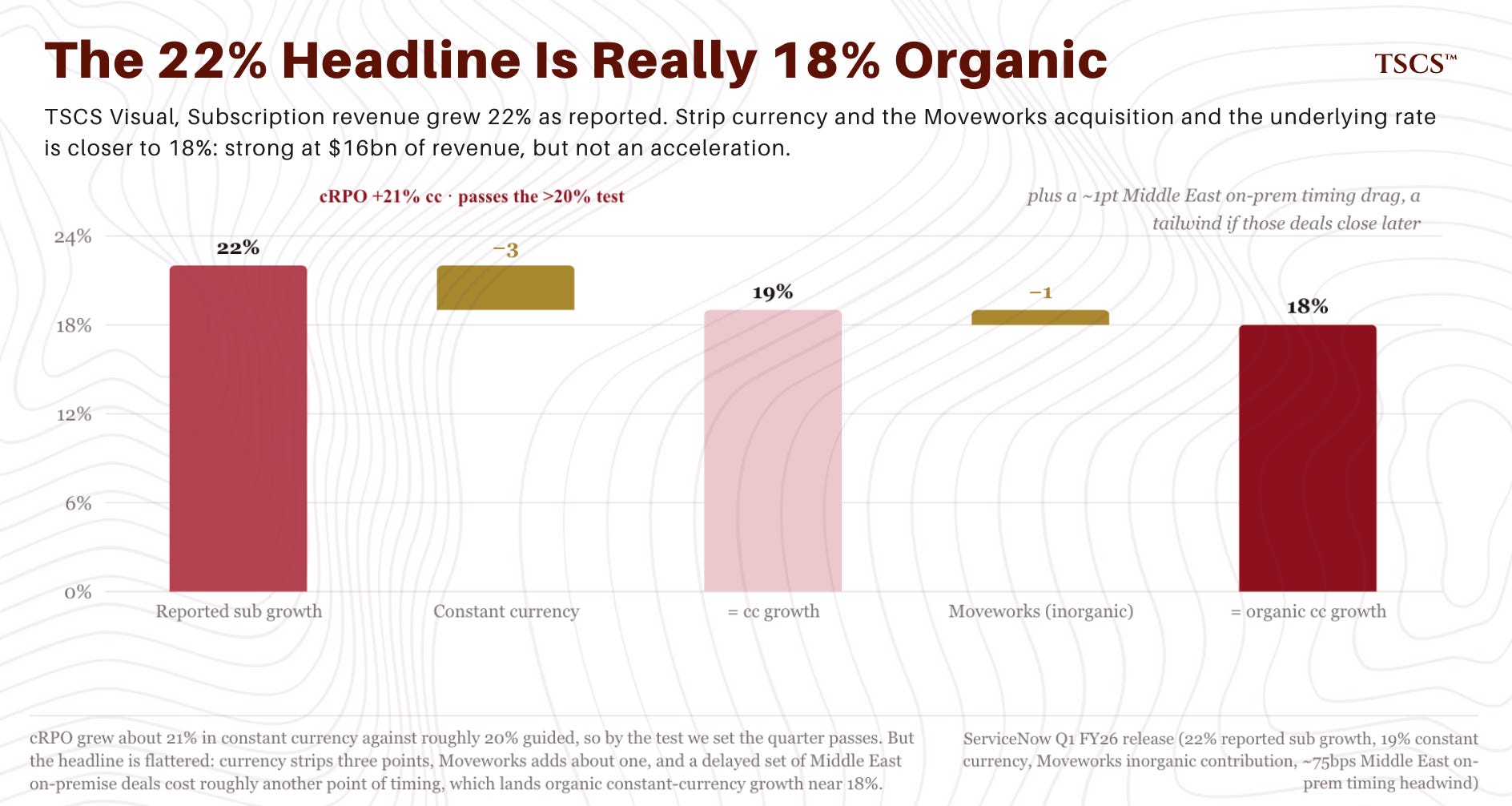

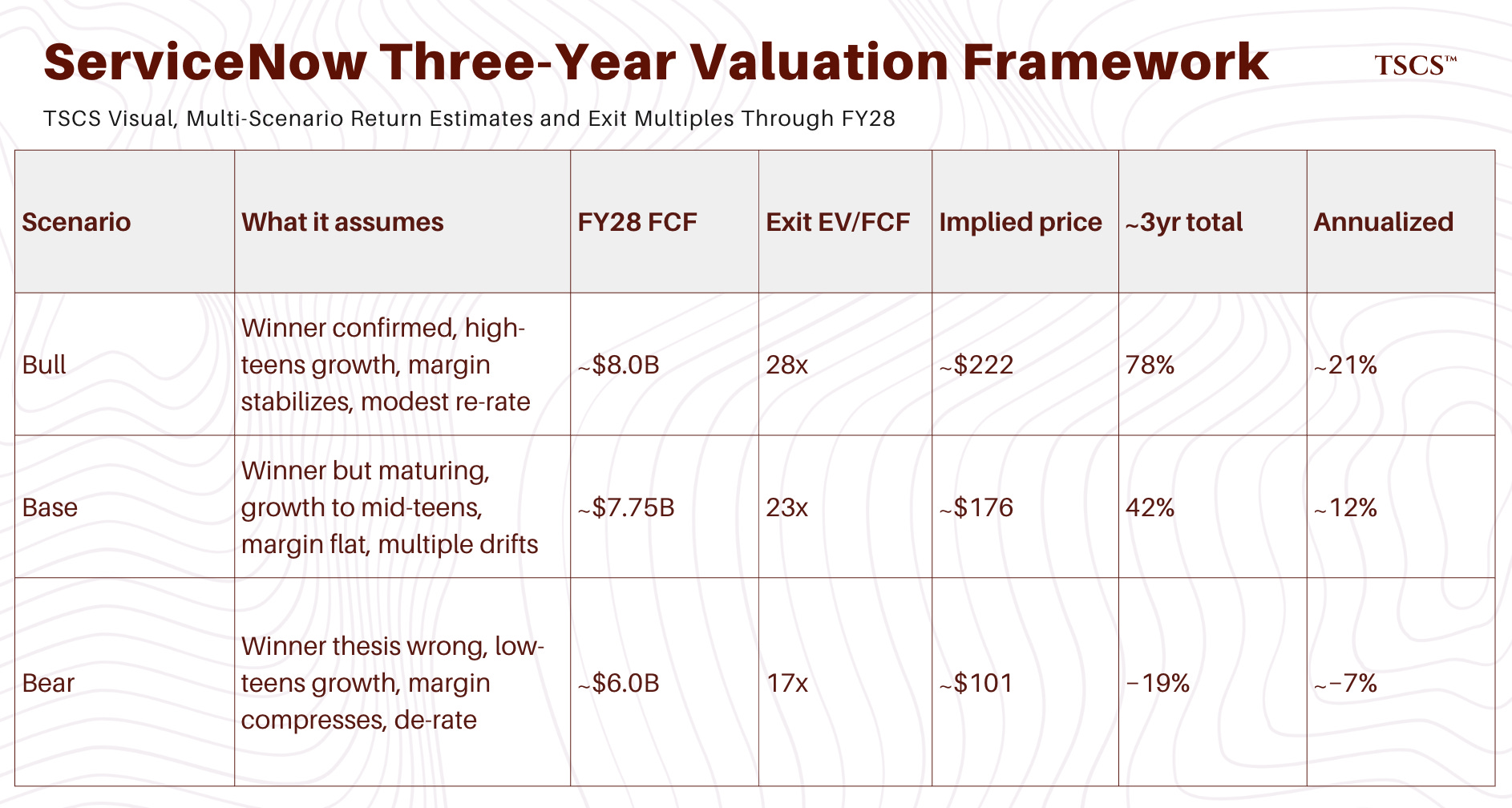

Start with what confirmed. ServiceNow reported the March quarter on April 22 and beat the high end on growth and profitability. Current remaining performance obligations, the cleanest read on near-term bookings, grew 21 percent in constant currency, ahead of the roughly 20 percent guided. Subscription revenue grew 22 percent, 19 percent in constant currency. Non-GAAP operating margin was about 32 percent. The AI line is becoming legible rather than promissory: customers spending over a million a year on Now Assist grew more than 130 percent, and the company lifted its AI target to $1.5 billion. By the test we set in the earlier work, cRPO above 20 percent confirms, and it printed 21. The quarter passes.

Now the part the headline hides. The 22 percent is flattered from two directions. Constant currency strips it to 19 percent, the Moveworks acquisition adds about a point, and a delayed set of Middle East on-premise deals cost roughly another, so organic constant-currency growth is closer to 18 percent. Strong at $16 billion of revenue, and not an acceleration. The full-year guidance raise is almost entirely Armis, which closed early in the year, so the organic raise is small. Free cash flow margin fell about 350 basis points to 44 percent. Subscription gross margin slipped from 81 to 78 percent, part acquisition amortization and part, plausibly, the cost of serving AI. GAAP earnings rose only 2 percent, an artifact of the tax rate normalizing rather than a demand signal. The buyback is doing less than it looks: $2.2 billion spent in the quarter, share count down only 0.7 percent, because stock compensation issues most of it back. The market’s first reaction was minus 12 percent, and the recovery came on the early-May analyst day, on the raised AI target. The market re-rated the narrative more than the quarter.

Is it an AI winner. Probably, with two open questions. The reframe that matters: ServiceNow is building the AI specialists that do the work of the human users who were its seat-license base, so this isn’t a question of whether AI helps or hurts. It’s a value-capture question, whether revenue per customer rises as human seats fall. That reduces to two lines you can watch every quarter. Net expansion, where the proxies are positive. And subscription gross margin, which is sliding and is the single most important number in the model, because a growth winner at a structurally lower AI-compute margin is a mediocre investment. Add the unresolved question of whether ServiceNow owns the agentic orchestration layer or the model companies do, and you’ve got a probable winner that’s taken the early rounds without closing them out.

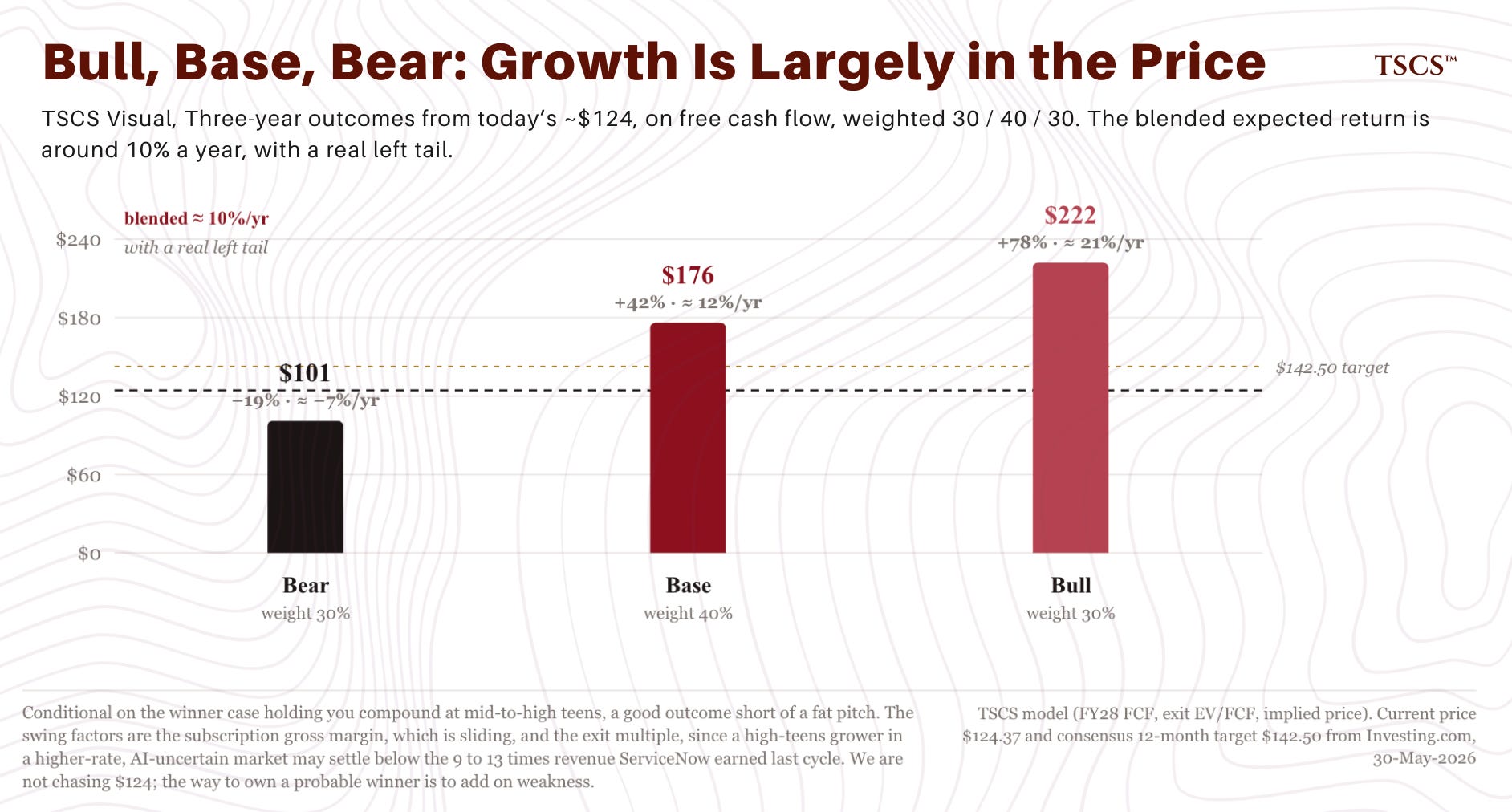

What it’s worth over three years, conditional on the winner case holding. Using free cash flow, since GAAP is distorted by the deals, and anchoring to consensus revenue near $22.8 billion by FY28 at a 34 percent free cash flow margin:

Conditional on the winner case, you compound at roughly mid-to-high teens, a good outcome and short of a fat pitch. Weighting the cases something like 30, 40, 30, the blended expected return is around 10 percent a year with a real left tail. Growth is largely in the price, so the swing factors are the gross margin and the exit multiple, since a high-teens grower in a higher-rate, AI-uncertain market may settle at a structurally lower multiple than the 9 to 13 times revenue ServiceNow earned in the last cycle.

Where we stand. We’re not chasing $124. The dislocation that made this a fat pitch at $102 is closed, and at a fair multiple after a 30 percent run there’s no margin of safety left if the two open questions break the wrong way. The way to own a probable winner without overpaying is to add on weakness, and the cleanest setup is another credit-driven software selloff, the kind a fresh redemption flare in the semi-liquid private credit complex could produce, which is the thread back to the piece above. Hold, accumulate on those dips, don’t back up the truck here. What would raise conviction: a second-quarter cRPO print that holds 21 percent against the 19 the company guided, and a gross margin that stops falling. What would lower it: the reverse.

| A guest post by

|