Nobody Wants Gold

Gold miners price the metal a third below spot. The Singapore gasoil crack says why, and June 17 decides when.

Everyone declared the emergency over when crude calmed down. They read the wrong barrel. The signal that tells you whether the dollar scramble that drove the selling is still live sits one step downstream, in a market almost nobody is watching, and it says the driver hasn’t gone away. I’m still long, I’ve been the whole way, and if the flush comes into June 17 it’s the entry, not the exit.

Nobody wants the gold miners. The juniors are leading the whole complex lower, the tourists who turned up at $5,000 gold have gone back to the chip stocks, and the people who spent a year calling the miners the cheapest thing in the market have gone quiet. On Friday the junior miners fell 10% in a single session while bullion fell 3%. That’s not a sector finding a floor. That’s a sector being left for dead.

I'm still long. Gold miners are a fifth to a quarter of my book, they have been for most of a year, and I've sat through every day of this correction without selling a share. I didn't panic into the March lows, I didn't chase the April rally, and haven't flinched through this drift. I'm not writing to tell you I've been right. I'm writing to tell you the one thing the consensus has wrong, because it changes whether this is the moment to give up or the moment to buy.

A framework only discussed when it works is marketing, so the record first. In March, near the lows, I argued in Gold Is Not Failing that the crash was a dollar liquidity event and not a repricing, that the metal was being used and not abandoned, and that the forced selling was finite. That held. In April I gave you five names in Buy The Miners on the thesis that the sector was printing $3,000 margins and trading for a gold price well below spot. In May I marked it to two earnings prints and told you where I was wrong, in public. I weighted Skeena’s de-risking over Rupert’s wider discount, and Agnico bid for Rupert two weeks later. The original Alamos sizing was set before its Q1 costs revealed what they revealed. The hits sit next to the misses. That’s the deal, and it’s the only reason the rest of this letter is worth your time.

One honest update before the tape, because I won’t pretend my read has stood still. In March I weighted this sell off as dominantly mechanical, positioning and gamma and tourist selling doing the work, with sovereign selling at the margin. The evidence since has moved me. Gold held through the ceasefire, held through the reversal, and made new relative highs on its way down, which isn’t how a purely mechanical unwind behaves. So I now weight the marginal driver toward the dollar short energy importer. I hold it as the leading read, not a certainty, and the first thing that would make me wrong is set out at the end.

The signal that says the scramble is still live

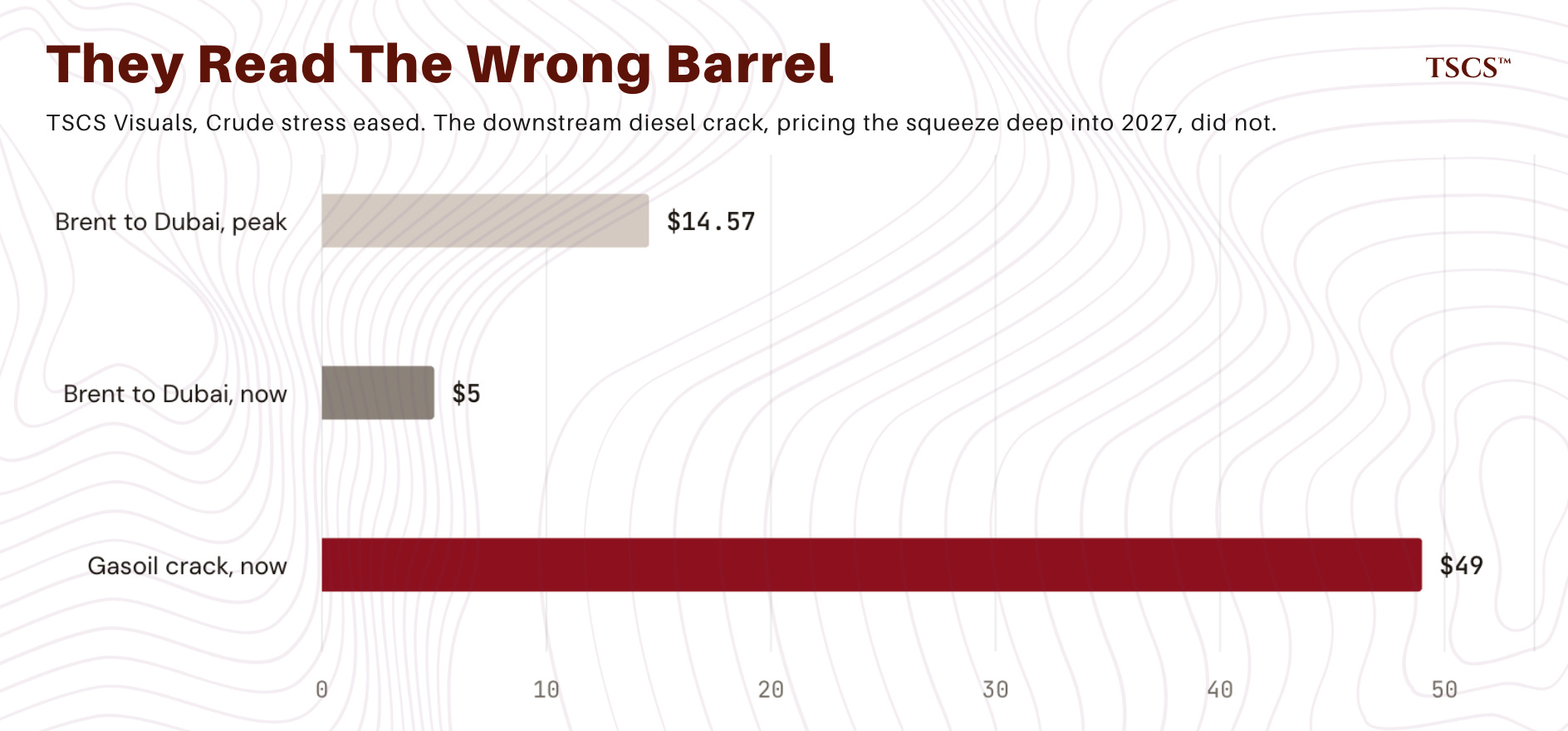

In March I gave you a two part test for when the forced selling ends. Not one signal, two. The acute phase is over only when the Brent to Dubai crude spread and the Singapore gasoil crack compress together. When only the crude spread comes in, you're watching the easy half of the normalisation, not the hard half. Pull both up today and you get the whole story in one picture.

Brent to Dubai, the premium the world pays for a barrel that can actually move versus one trapped behind a closed strait, blew out to $14.57 at the peak of this crisis, a reading you see a handful of times in a generation. It’s back near $5 now. Crude has largely healed, and front month Brent falling 19% in May, its worst month in six years, says the same. The crude panic has passed.

Now look one barrel downstream. The Singapore gasoil crack, the premium an Asian importer pays for diesel over crude, tore out to its highest since August 2022 and remains steeply backwardated, pricing the stress to persist deep into next year. Understand the mechanism, because it’s the whole argument. Crude can be rerouted around a closed strait given enough ships, time and insurance. Refined product can’t, and not for the reason most assume. The binding constraint isn’t the diesel tankers, it’s the refineries. Close to a fifth of the world’s seaborne oil moves through Hormuz, along with a tenth of the diesel and a fifth of the jet fuel that crosses borders, and with Gulf crude logjammed behind the strait the refineries that turn it into diesel are starved of feedstock. Replacement crude from the Atlantic basin takes one to two months to arrive, so refineries cut runs rather than shut down, and product output falls with them. The rerouting only makes it worse, since every tanker sent the long way around Africa burns more of the diesel that’s already short. So the crude spread can heal while the product market tightens, which is precisely the divergence on the screen.

Exxon says US distillate inventories are at their lowest since 2003, down roughly a quarter since the war began, and that once you reach the bottom of the tank prices don’t drift, they shoot. Chevron says the same in gentler language. And you can see who pays: oil-importing economies sold about $86 billion of Treasuries in March, the largest monthly drawdown since 2011, the dollar scramble surfacing in the one account it can’t hide. That’s the chain. A closed strait, starved refineries, a diesel squeeze that crude’s recovery masks, importers funding it by selling reserves, and gold the most liquid reserve asset they hold.

What the crack does and doesn’t tell you is where the consensus, and until recently I myself, muddled the logic. The crack measures the environment. It tells you whether the dollar scramble that drove energy importers to sell their reserve asset has eased. It hasn’t. The importers are still short dollars, the inventory cliff is real, and the condition that fed the selling is still in place. That’s the driver, still live, in a market nobody is quoting because they’re busy watching the crude headline that has calmed. What the crack doesn’t measure is whether the selling itself has run its course. That’s a separate question, with a separate set of signals, and conflating the two is the single most common error in reading this tape.

The signals that say the selling is not done

When a forced sell off exhausts, the tell isn’t in the oil curve. It’s in the tape of the thing being sold. Three of them, and they answer the question the crack can’t.

The first is the juniors. At the bottom of these episodes the most leveraged, most hated, most illiquid end of the complex stops falling before bullion does, and that refusal is usually the first sign the bleeding has stopped. We’re seeing the opposite. Friday: GDXJ down 10%, bullion down 3%, the seniors down nearly 9%. GDXJ is really intermediates rather than true small caps, and one session can be beta off an oversold low rather than signal, so call it colour and not proof. But it points the same way the crack does, toward patience.

The second is positioning. Open interest in gold futures is at a 13 year low and the tourist ETF selling that defined March has slowed. That’s washed out, and washed out is constructive. But it means the downside fuel is largely spent, not that the last of it has burned. A floor forming, not a floor in.

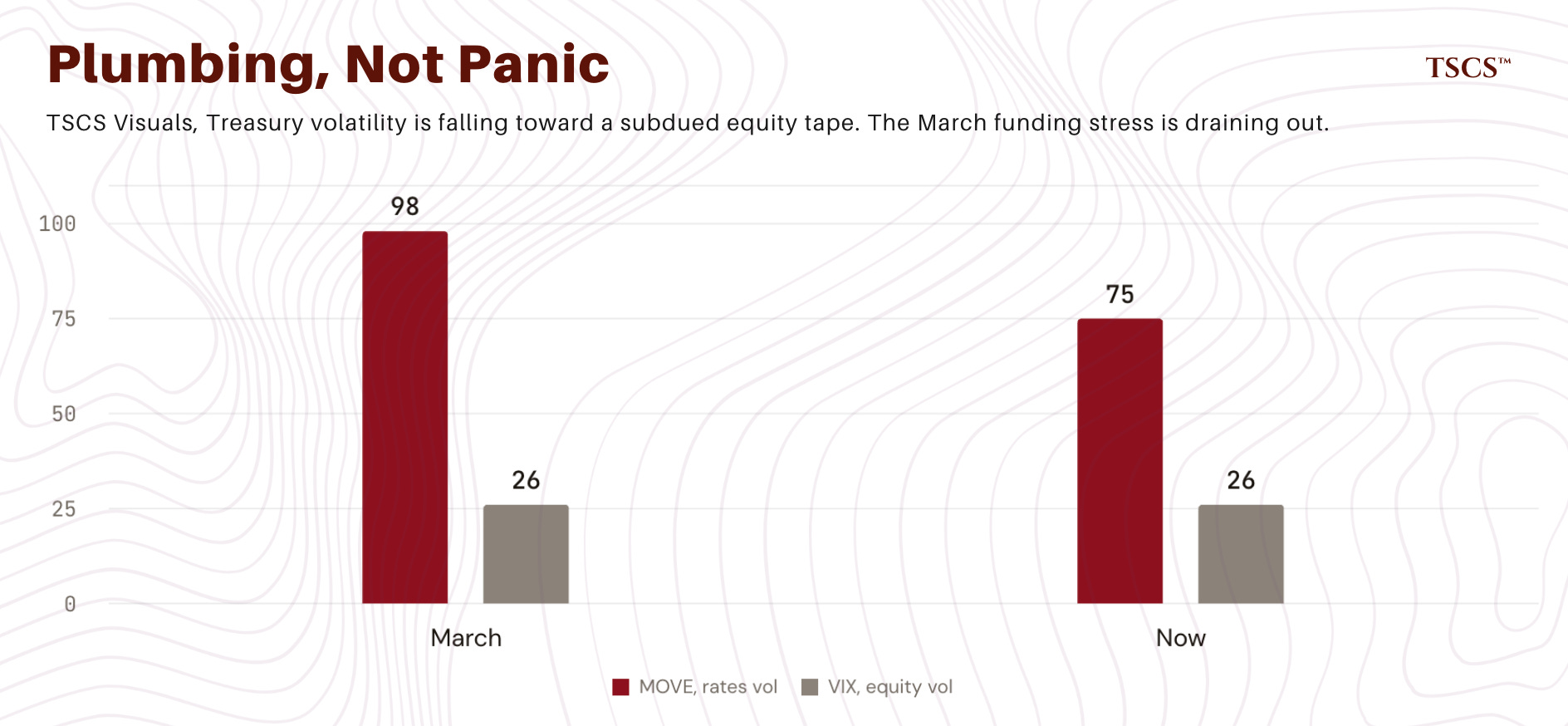

The third is the plumbing, and it cuts both ways. The cleanest March evidence that this was a funding event and not an economic one was the gap between rates volatility and equity volatility. The MOVE index, stress in the Treasury market, sat at 98 while the VIX sat at 26. Bond market screaming, stock market calm, which is isolated plumbing, and plumbing resolves faster than economic stress because it answers to policy. That gap has narrowed, the MOVE is down near 75, and the March stress is draining out. The watch from here is the thing that would change my mind. A VIX that re-spikes and holds in the 20s is the one in four deflationary outcome I keep weighting, the world where the wait is years and not months. A VIX that stays where it is says the stress is still just draining.

Read the two questions together and they point the same way for now. The environment is still stressed, the crack says so, and the selling isn’t yet exhausted, the juniors say so. Neither is a reason to be bearish on the thesis. Both are reasons to be patient with the entry. And the weakness was never gold’s alone. Silver and the mining equities were hit at least as hard, which is what a dollar liquidity event looks like, everything sold at once for the one thing everyone needs.

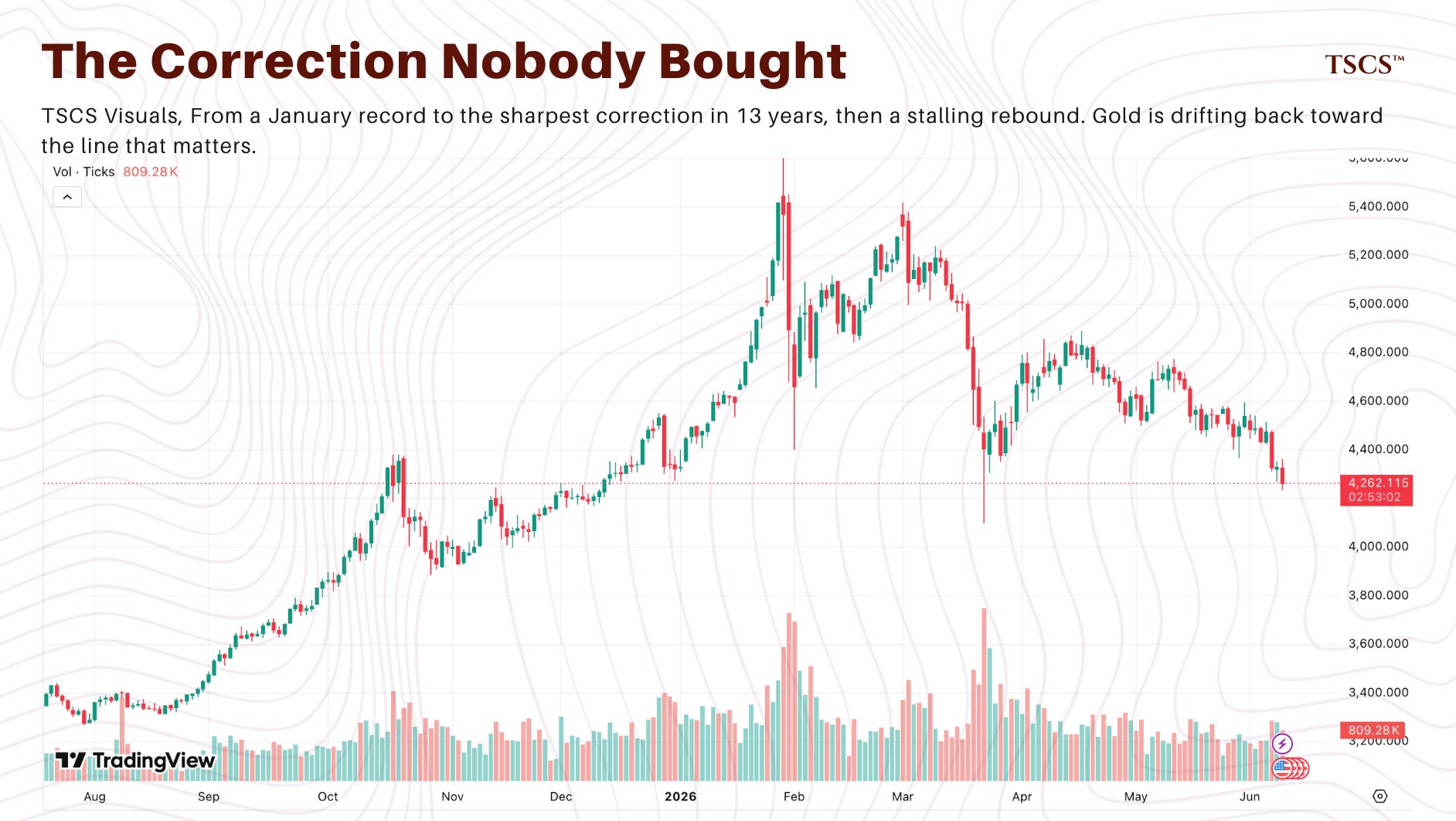

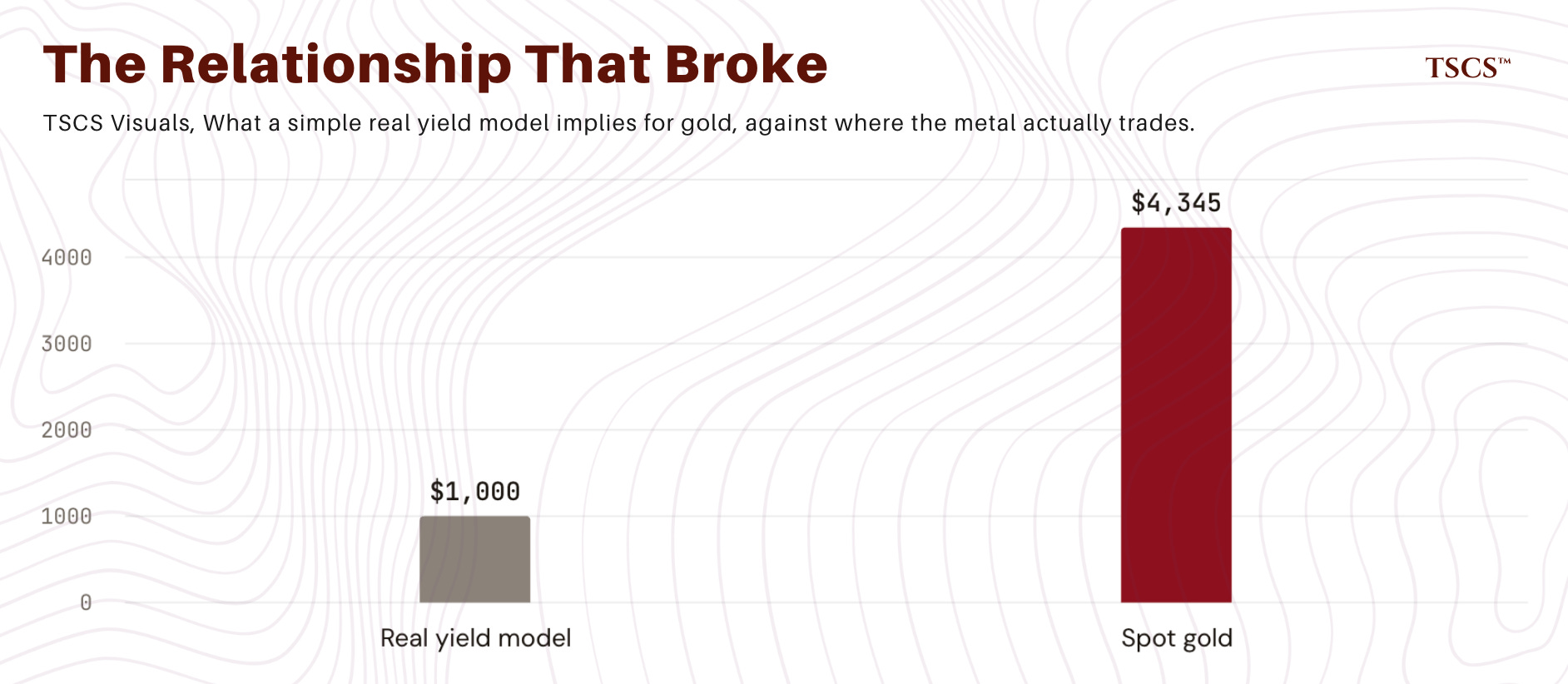

Gold itself is doing what you would expect in the middle of this. It’s around $4,345 as I write, down about $145 on the week with the drop concentrated in Friday, trying to base just above the $4,200 line I’ve called the level that matters. The relationship that supposedly governs the metal, gold against real yields, is still broken. A simple model off a real yield near its highest in 15 years would put gold close to $1,000, not $4,345, and the recent dip hasn’t begun to repair that gap. The thing that should worry a gold bull isn’t a $145 pullback. It’s the day the metal starts tracking real yields again, and that day isn’t here.

Everything above is the free read: what follows, the book itself, where each name sits today, the kill switches, and the exact levels and sequence in which I add my cash, is for paid subscribers. The thesis is free. The trade is not.

Keep reading with a 7-day free trial

Subscribe to TSCS to keep reading this post and get 7 days of free access to the full post archives.