Party's Over

The element most people associate with balloons is non-renewable. South Korea sources 64.7% of its helium from Qatar and fabricates two-thirds of the world's memory chips.

The most important satisfies semiconductor manufacturers for advanced chip fabrication is not silicon. It is not copper, cobalt, palladium, or ultra-pure quartz. It is a noble gas that forms underground over geological timescales, escapes permanently into space the moment it is vented, has no synthetic substitute, no futures market, no transparent pricing mechanism, and no way to ramp production in under seven years.

In October 2025, it quietly surpassed MRI machines as the world’s largest end use. Nobody outside the specialty gas industry noticed.

Five months later, Iranian drones shut down the facility that produces a third of global supply.

You have read the panic version of this story. Sherwood ran it. CNBC ran it. Tom’s Hardware ran it. Helium gone, chips disrupted, AI buildout at risk. We are not writing that piece. Not because the disruption is fake, it is real, but because the panic narrative is built on a number that is almost certainly wrong, and the number that replaces it cuts in a direction nobody is discussing.

Here is what we mean. The headline says semiconductors consume 21 to 24% of global helium. That figure is accurate. It is also gross throughput before recycling, and quoting it as net demand is like measuring an oil refinery’s crude intake and calling it consumption without accounting for the fact that most of it comes out the other end as product. Modern advanced fabs recapture 80 to 95% of the helium they use. The semiconductor industry’s actual fresh helium requirement may be closer to 2 to 5% of the global market.

The entire crisis narrative might be anchored to the wrong number.

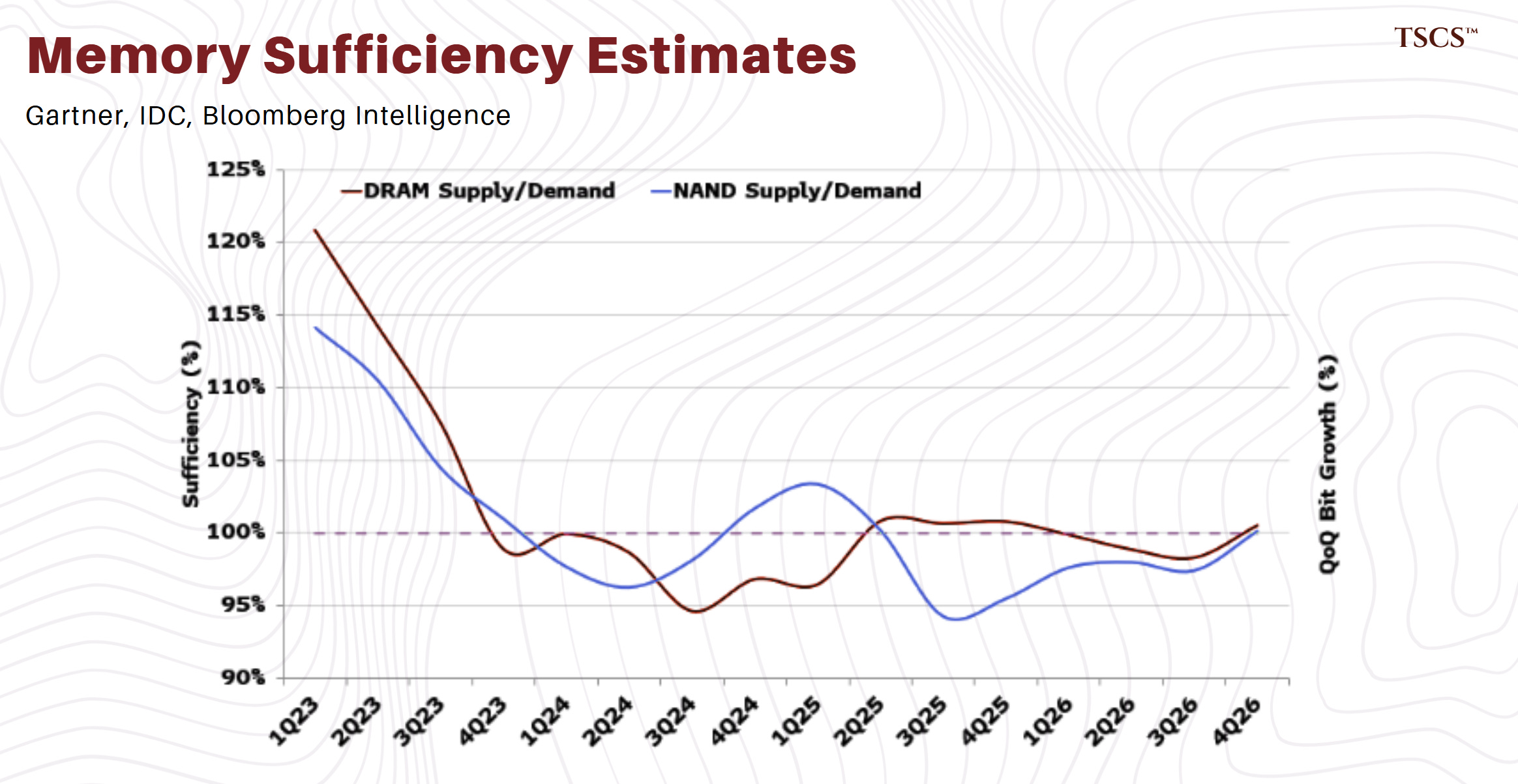

But before the bulls exhale: the right number is still scary enough. South Korea sources 64.7% of its helium imports from Qatar and fabricates roughly two-thirds of the world’s memory chips. The memory market entered this crisis with DRAM prices up 240% year over year, finished inventory at three weeks against a four-week floor, and SK Hynix having presold its entire 2026 output. There is no slack. There is no quiet quarter where this lands softly. And the recycling rate that determines whether this is a manageable inconvenience or a binding production constraint is, to be direct, a number nobody can actually measure.

We built the full transmission model: fab-level helium consumption by process step, the nonlinear yield degradation curve that makes conservation self-defeating past a threshold nobody publishes, the distributor allocation mechanics that determine which fabs produce chips and which ones don’t, the China variable that turns a commodity shortage into a geopolitical allocation crisis, and the natural hedge between energy costs and helium scarcity that almost nobody is modelling.

Our base case: a three-to-five month disruption producing meaningful spot price increases and allocation tightening but not binding production constraints at major Korean fabs. Probability: roughly 50%. Tail risk, six months or longer, forcing allocation triage on top of the steepest memory supercycle in the modern era: roughly 25%. Benign resolution within weeks: roughly 25%.

We think the most probable outcome is that the semiconductor industry navigates this with manageable pain and the narrative overshoots reality.

We could be wrong. Below, we show you exactly how to know if we are.

Why you should be reading TSCS

Everything above is free because you can find some version of it elsewhere.

What follows, the recycling arithmetic that collapses the headline narrative, the nonlinear yield curve nobody is modelling, and the five indicators that will tell you whether this is a footnote or a structural repricing, you cannot.

That is what a TSCS subscription gets you.

Let’s get into it.

Keep reading with a 7-day free trial

Subscribe to TSCS to keep reading this post and get 7 days of free access to the full post archives.