Peak Silver Demand

Copper substitution, a 19% demand cut, and a deficit rotting from the inside. The bull case for silver might have a problem.

On July 9, Bloomberg reported that LONGi’s copper metallization facility in Shaanxi province is operational.

Pilot lines and roadmap slides have promised copper metallization for a decade.

What Bloomberg described is a running factory, and its product is a solar cell whose conductive grid is copper instead of silver. LONGi is one of the largest solar manufacturers on earth, and photovoltaics has been the largest line in silver’s industrial demand.

I’ve looked at Hecla, Skeena, and Pan American. I published the entry logic, the sizing, and the kill switches in Silver Bugs Were Right. This piece is the best bear case I can build against these positions and any silver positions. If the argument survives your scrutiny, it should change how you weight silver against gold for the rest of the decade. If it doesn’t, the comments are open and I will engage.

The timeline that made me write it reads best backwards.

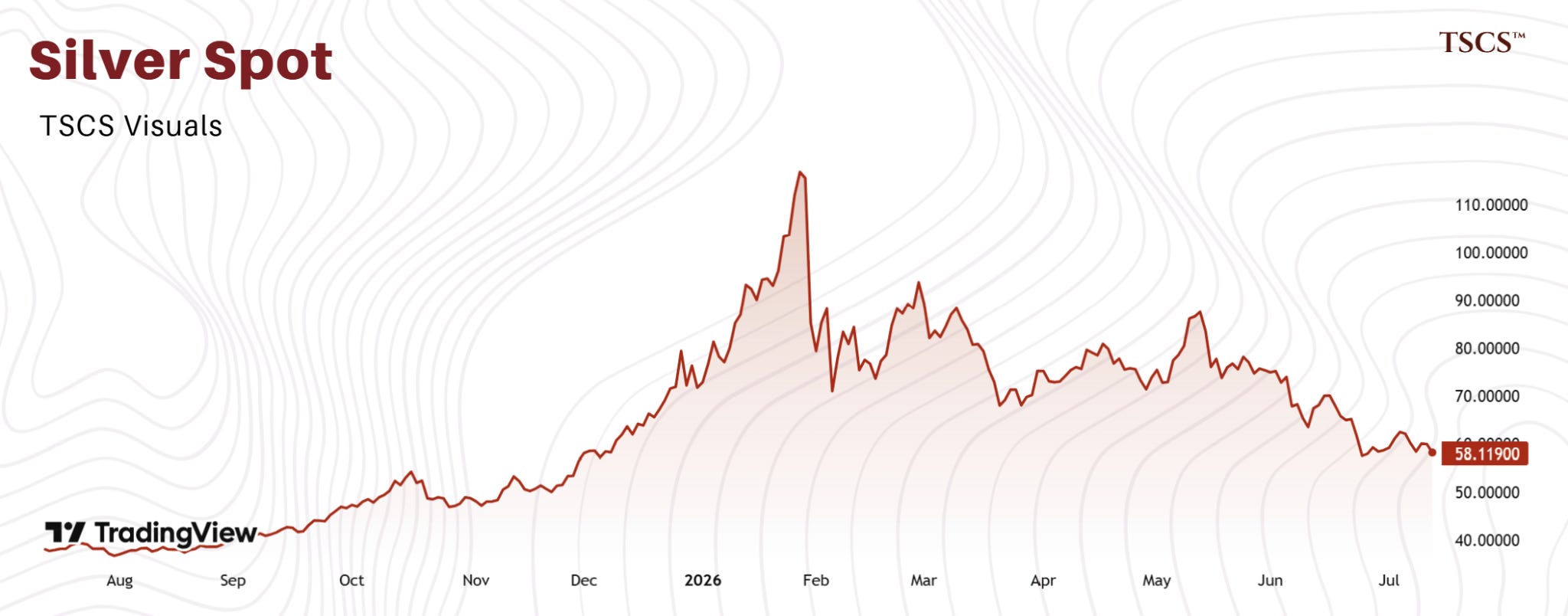

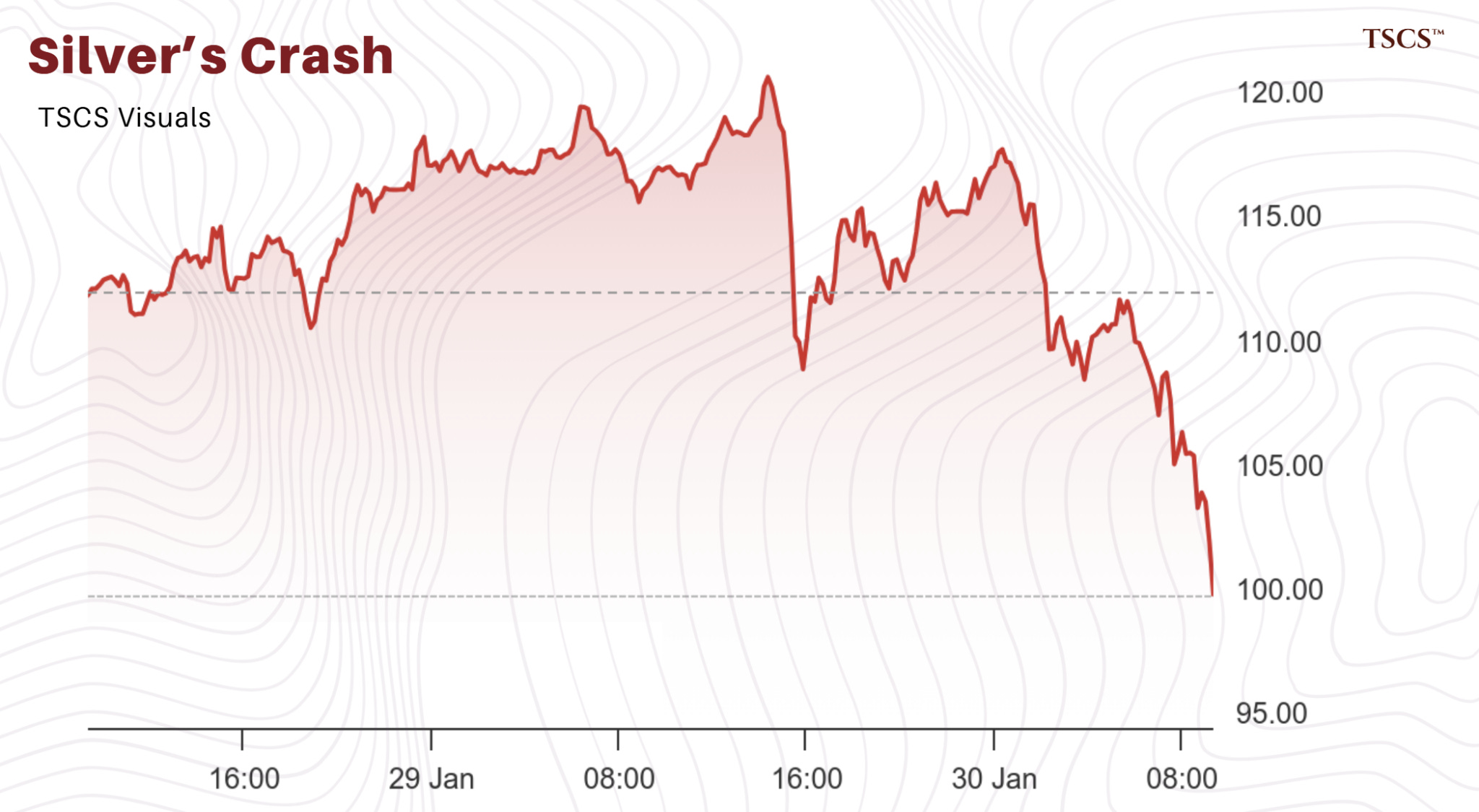

January 29, 2026. Spot silver prints $121.67, an all time nominal high, capping a January run the market had not seen since the Hunt era. 30 hours later it settles at $78.53, the worst single session since March 1980. I covered this in The 31% Silver Crash, and the consensus explanation, then and now, is Warsh.

Trump nominated an inflation hawk to the Fed on January 30 and the leveraged longs got carried out.

Now rewind to January 5, 2026. Silver is around $75, having just pulled back from its December peak of $84. LONGi files with the Shanghai exchange: it will replace silver with base metals in its back contact cells, mass production from the second quarter. Jinko had said in December it could reach large scale output of copper based panels within the year. Aiko was already shipping silver free cells from Zhuhai, with 6.5 GW of initial capacity and copper interconnection it says has 4 years of production validation behind it.

So the sequence is this. The industry’s substitution decision was made at $75 to $84 and disclosed on January 5. The all time high came 3 weeks later, made almost entirely by investment flows (Indian and Chinese retail priced out of gold, ETP money, momentum funds). The mania bought a demand story the customer had already abandoned in writing. The crash on January 30 was margin calls arriving. The change was filed on January 5.

TLDR

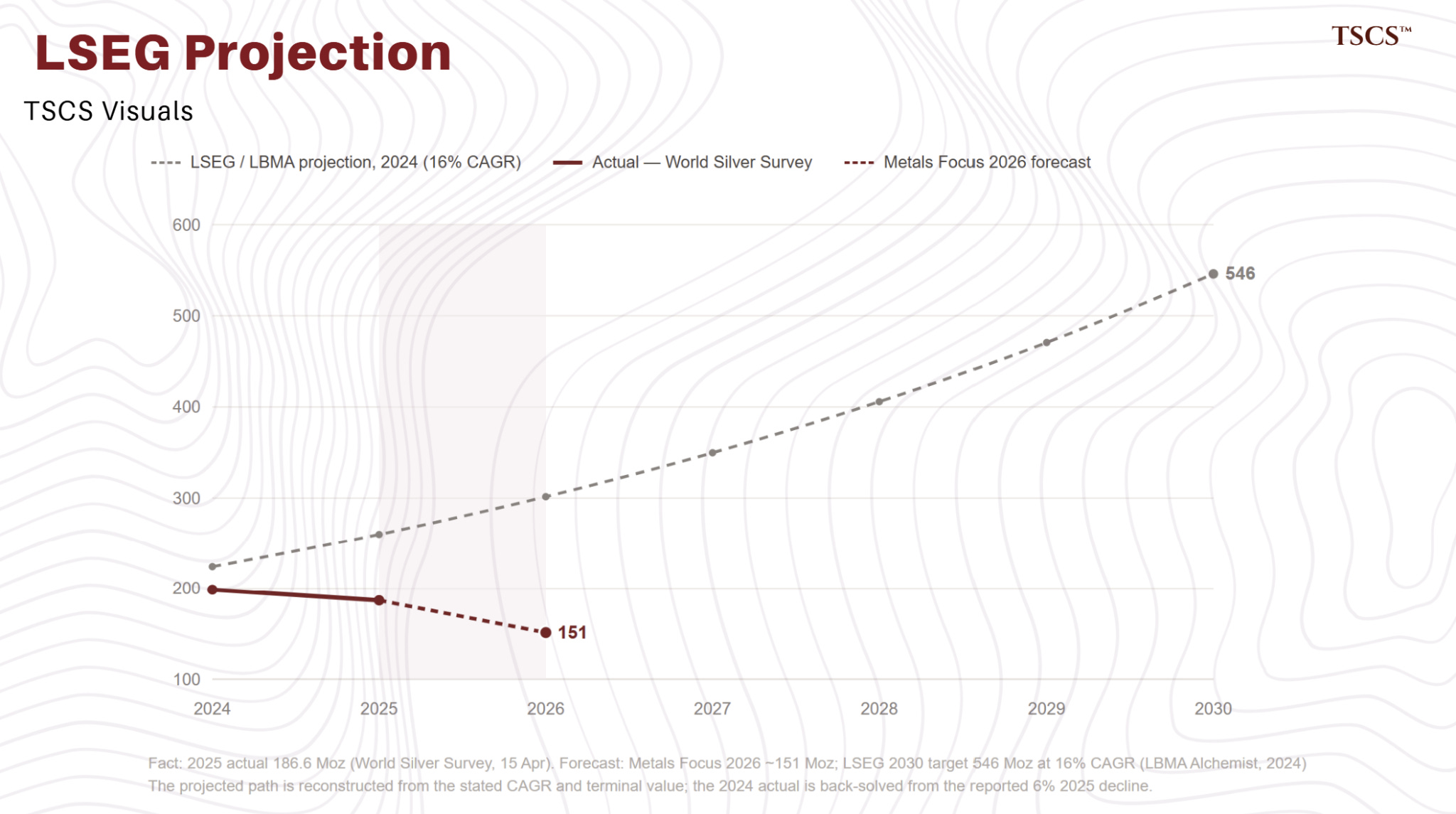

The solar industry cut its silver demand 6% in 2025 and Metals Focus forecasts a further 19% cut in 2026, to roughly 151 Moz, while global cell production held roughly flat. The decline is intensity, silver per watt, and history says intensity losses of this kind do not come back.

The copper trade everyone reached for on this news is a rounding error and I‘ll show why. The real trade is relative: silver is gold with an embedded short position in metallization technology, and I am repricing my own published scenarios accordingly. The deficit is real and I am not shorting into it. The reverse thesis, with dates, is at the bottom.

The copper trade dies in one paragraph

The tweet that started half the recent commentary said LONGi is replacing silver with copper, interesting, copper thesis.

How does it work? Photovoltaics consumes roughly 6,000 tonnes of silver a year. If you replace all of it with copper at 2-3x the mass, since copper conducts worse and the features run thicker, you add perhaps 12,000 to 18,000 tonnes of copper demand to a refined market of roughly 28 to 29 million tonnes.

That’s 0.04% to 0.06% of the market. Copper won’t feel this at all. The copper bull case still rests where I put it in Copper Miners Are Too Cheap, on the incentive price of the marginal tonne, and the cyclical balance just moved against the bulls anyway.

ICSG revised its 2026 forecast in April from a 150,000 tonne deficit to a 96,000 tonne surplus.

The number that moved while nobody was looking

The World Silver Survey landed on April 15 and the market read the headline: a sixth consecutive deficit of 46.3 Moz, wider than last year.

I read it too, and I wrote in Silver’s Quiet Squeeze that the structural thesis survived the crash.

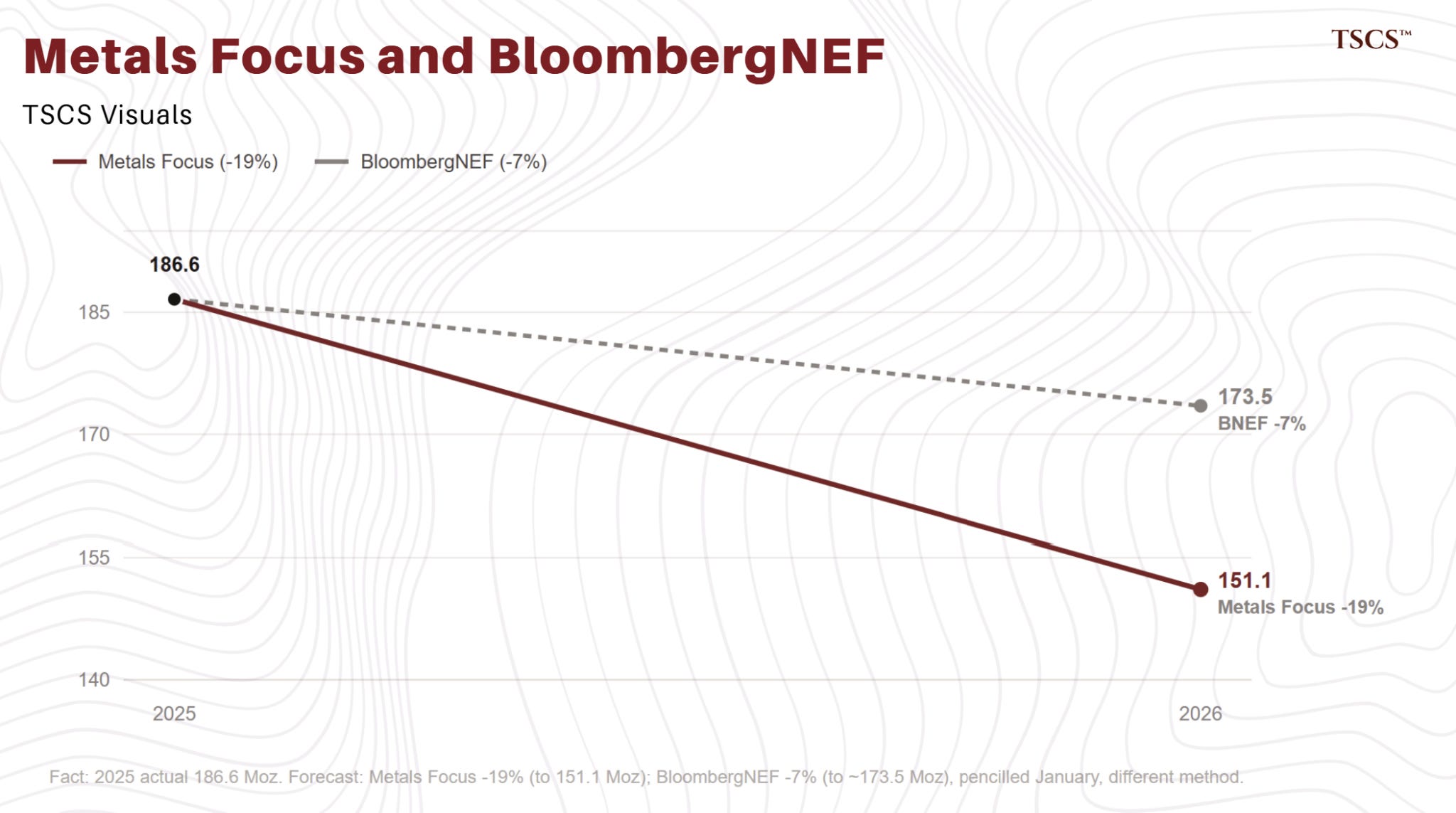

What I underweighted was the demand table 2 pages down. PV silver demand fell 6% in 2025, to 186.6 Moz. Metals Focus forecasts it falls a further 19% in 2026, to around 151 Moz. That’s a forecast obviously, not an actual, and Metals Focus revised its own February outlook within 2 months, so would hold it relatively loose.

But BloombergNEF, independently and with a different method, had already pencilled a 7% decline in January. Interpret that as you will.

Now if you put that next to the volume data, the story will make a little more sense. Chinese domestic installations collapsed in early 2026, down 51% January through April, down 79% in April alone.

The bears quoted it, the bulls countered that exports absorbed the hole ahead of the April 1 removal of China’s export VAT rebate, and the bulls are right: on the best reconstruction from official Chinese output and customs data, global cell production through the first half was roughly flat. No official global series exists. So I can’t be certain about quarterly figures, but I’m quite confident in the direction.

Production was flat and silver demand fell 19%.

The entire decline came out of intensity and the industry achieved that in a year (before the substitution wave).

For scale, in 2024 the LBMA’s Alchemist carried an LSEG projection of PV silver demand reaching 546 Moz by 2030, a 16% compound growth rate.

For your information, it’s still falling.

Consensus on silver’s largest industrial growth engine was wrong by a factor of 4x in two years, and I’ve not seen a single sell side note mark that forecast to market.

How the intensity is being cut, and which part never comes back

Three things are cutting demand. I think they have different priorities so I would try to read it one at a time.

If TSCS pays for one idea this year, this is the one I would pick. It’s imperative to know.

Keep reading with a 7-day free trial

Subscribe to TSCS to keep reading this post and get 7 days of free access to the full post archives.