Silver Bugs Were Right

Silver bugs were right. The basket is dead anyway. Silver -8.48% today. M&A took out four primary names. Hecla, Skeena, PAAS left. Vizsla killed after Panuco.

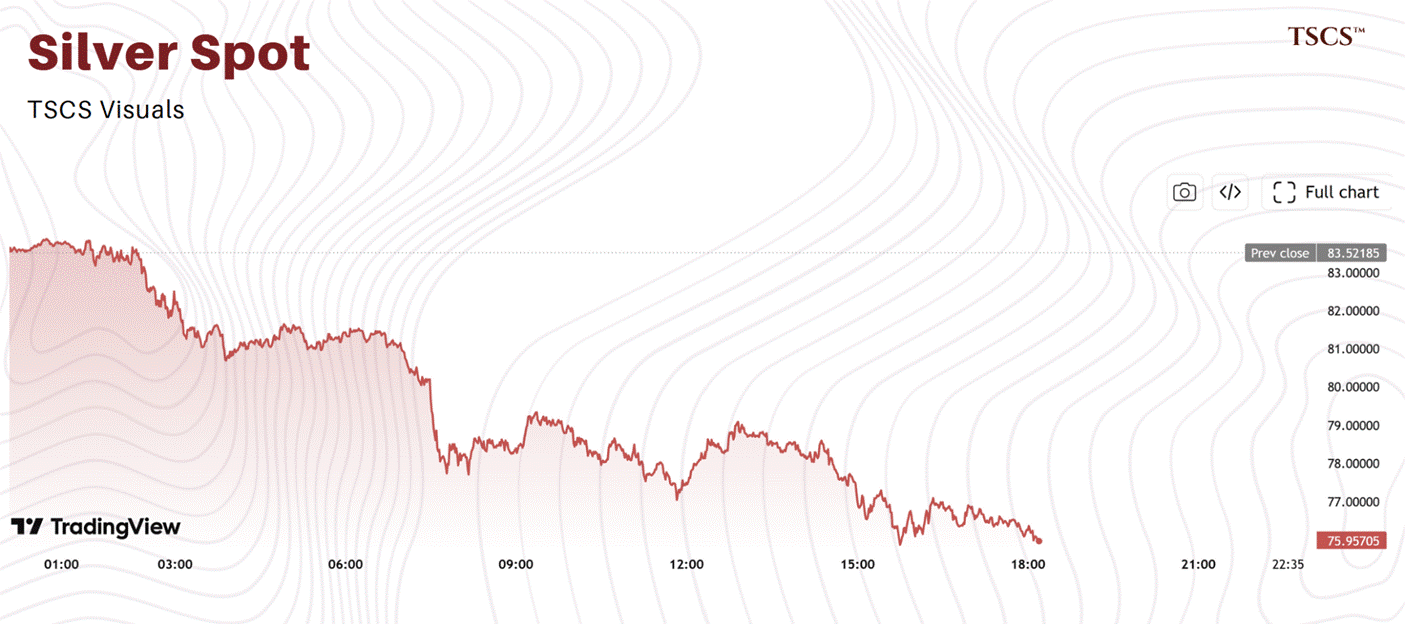

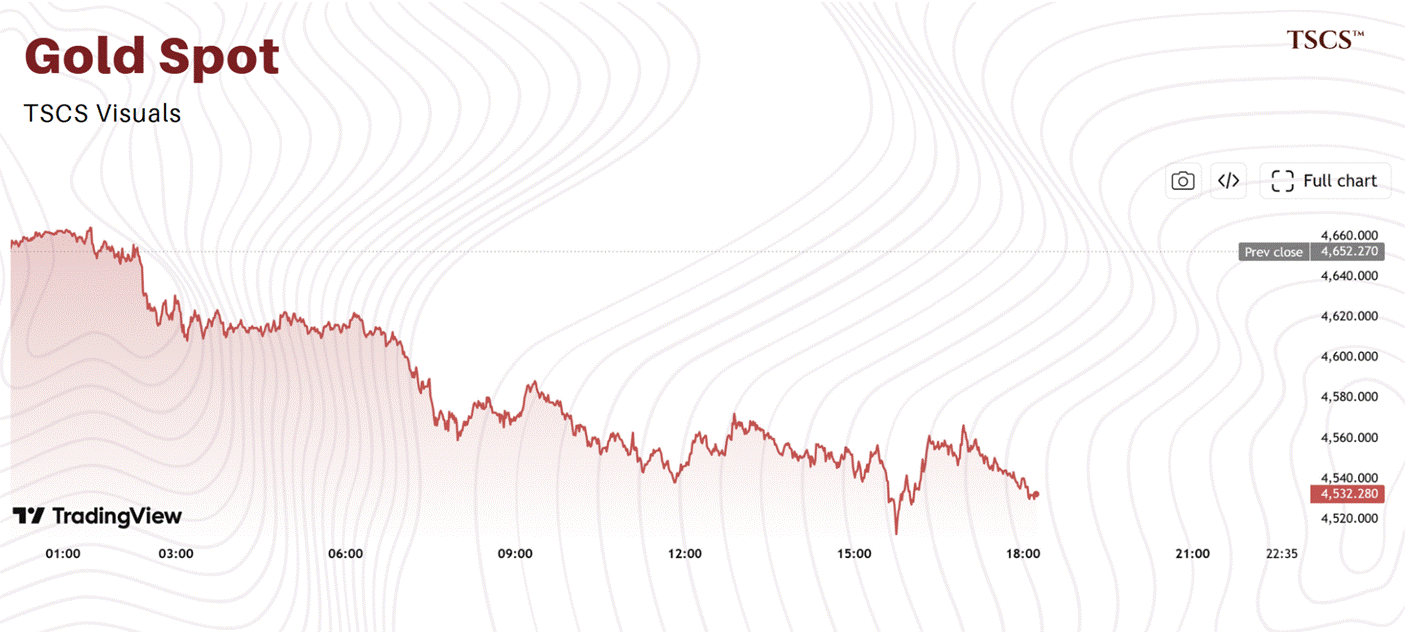

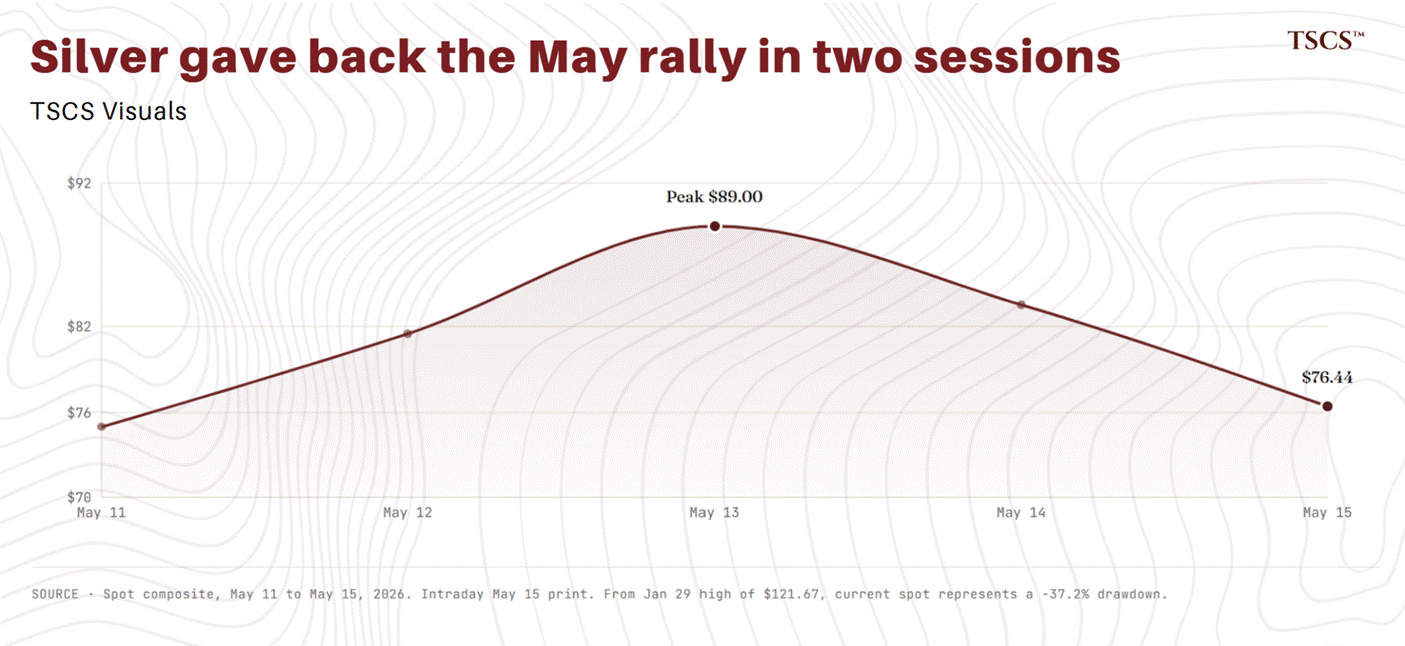

Silver is $76.44. Down 8.48% on the day as I write. Gold is $4,547. The gold to silver ratio blew from 57 yesterday to 59 today in a single session. Yesterday’s close was $83.52. Silver has given back the entire May rally in two sessions and is below the May 11 starting point of $75. Twenty-two years of inverse correlation between silver and real yields said today should happen eventually. Eighteen months of 2024 to 2026 price action said it would not. Real rates at 1.99% and the textbook is finally pulling silver down the way correlation said it should. I am still holding. Here is why.

The single way this piece is wrong is being stress-tested on the tape as I write. The post-2024 correlation flip was rate-cut-narrative dependent, not structural. The May 12 to 14 inflation prints took the rate-cut path off the menu. Today the textbook mechanism is reasserting in full. If that read holds for the next twelve months, silver mean-reverts toward $50 to $60 and the cohort takes a 25 to 40% drawdown with it. The structural deficit, the COMEX warehouse drawdown, the Shanghai premium, the convenience yield gap, all of it explains the reset from $25 to current levels. None of it explained why silver should hold $80 plus with real rates at 2% and no path to lower. Today’s tape proved that. The question now is whether the structural floor holds at $70 or breaks toward $50 to $60. Every other kill switch in this piece is downstream of that question. I am holding because the physical decoupling is real and material. If today is the start of the structural floor breaking too, the whole construction breaks at once.

I called the squeeze in “Two Silver Curves, 200 Basis Points Apart.” The 200bp convenience yield gap, the COMEX warehouse drawdown, the Shanghai premium, the physical decoupling from paper. All of it. Still running as of yesterday’s close. None of it priced in sell-side models, which are still carrying silver at $40 to $50 for 2026 against realised YTD averages in the mid-$80s. The structural setup did not break in the last six hours. The price did.

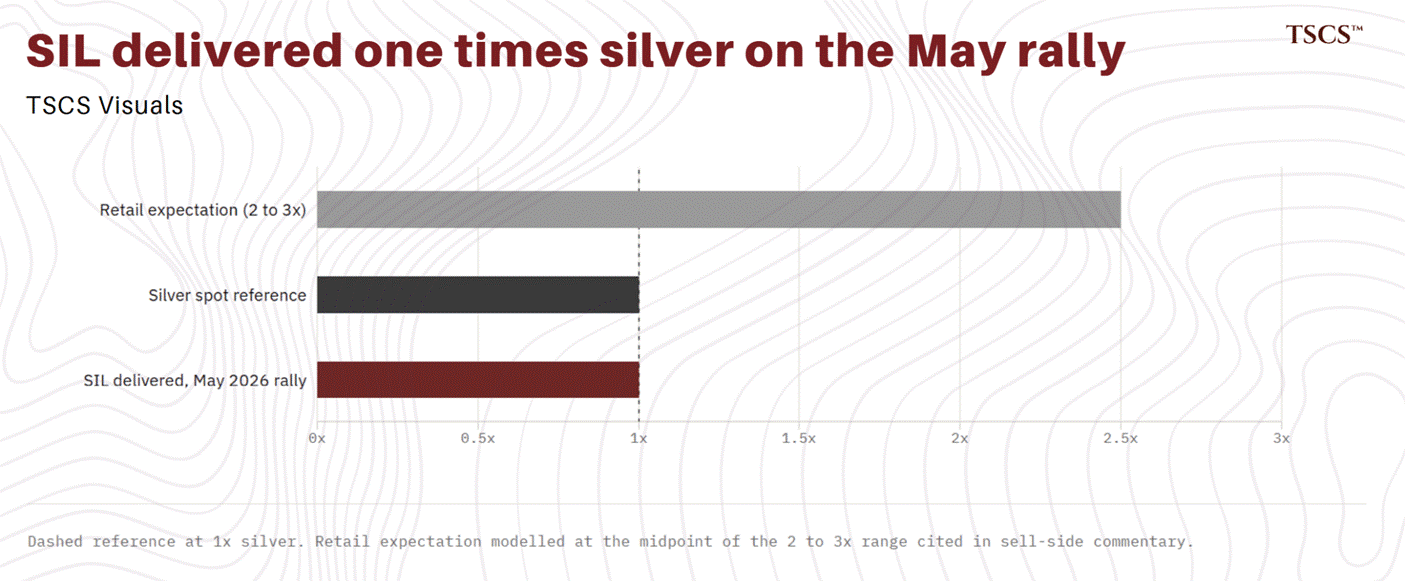

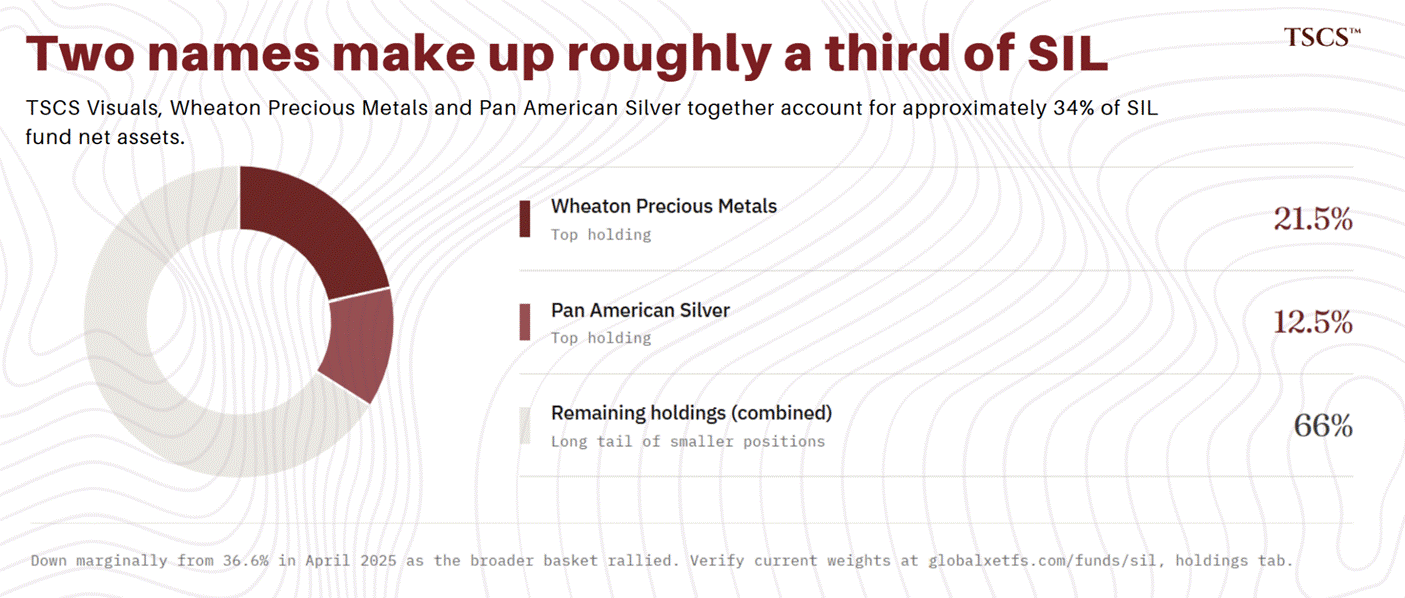

What is not working is the basket trade in the equity. SIL captured 1x silver beta on the May rally. Not 2x. Not 3x. One. Everyone is paying for torque the basket cannot deliver because the basket got gutted in eighteen months. Four primary silver names taken out by M&A. Top two holdings are a third of the fund. The lost torque people want in this cycle is not in SIL. It might be in a handful of curated names. That is the work.

This piece is that work. Three names I am holding. One name I covered, sized, and dropped after a security event in Sinaloa, with the rule discipline that decision required. Kill switches, position sizing, NPV math anchored at the May 13 peak deck ($89 silver, $4,698 gold). Live spot is 14% below that. Caveats explicit in the methodology section. If you cannot take a name-level view and update on each catalyst date, the alternative is PSLV or SIVR at 1x beta with no operator risk. That is a defensible construction. It is not the construction in this piece.

Below the paywall: the three names, the math, the rules I am running them against, and the evidence that says this sleeve is one concentrated silver equity bet expressed across three positions, not three independent ones. The basket is dead. The work is what is left.

TLDR

The basket bet on silver miners is dead. SIL captured 1x silver beta on the May rally, not the 2 to 3x retail commentary keeps quoting. Four primary silver names were taken out by M&A in eighteen months. Top two SIL holdings are a third of the fund. What is left is a curation problem.

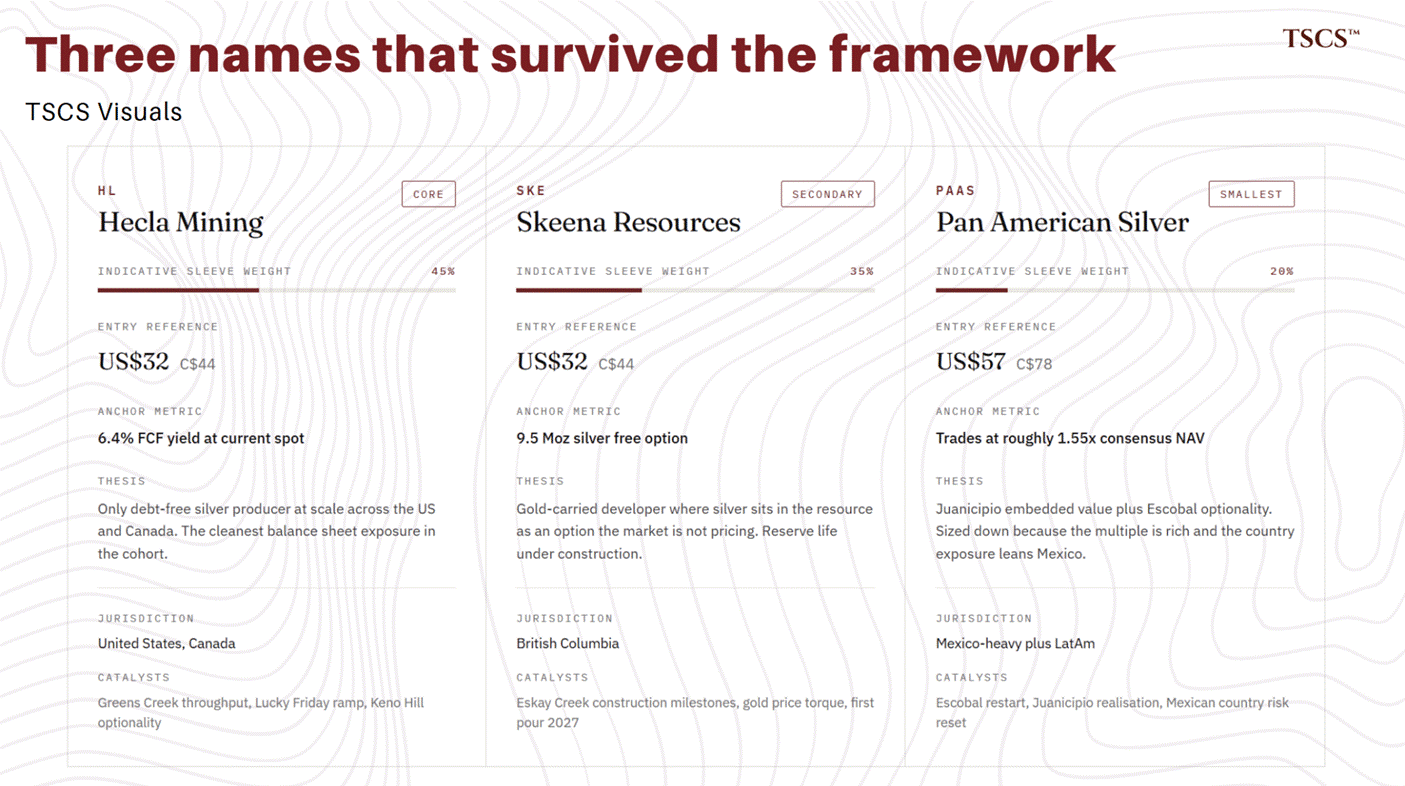

Three names form the active sleeve. Skeena (SKE) as gold-carried developer where silver is a 9.5 Moz free option the market is not pricing, entry around C$44 / US$32. Hecla (HL) as the only debt-free US and Canada silver producer, 6.0% FCF yield at spot, entry around $18. Pan American (PAAS) as Juanicipio embedded value plus Escobal optionality, smallest position because the stock trades at roughly 1.52x consensus NAV, entry around C$78 / US$57.

Vizsla (VZLA) is covered, not recommended. The January 23 abduction at Panuco (nine confirmed dead) triggered my pre-set security kill switch. Re-entering now would soften the rule retrospectively. I am not.

The real rates correlation flipped. Pre-2024 silver-TIPS correlation was minus 0.62. Post-2024 it is plus 0.48. The trade is a bet the inversion sticks. If the historical mechanism reasserts at 1.99% real rates, silver mean-reverts to $50 to $60 and the cohort goes with it.

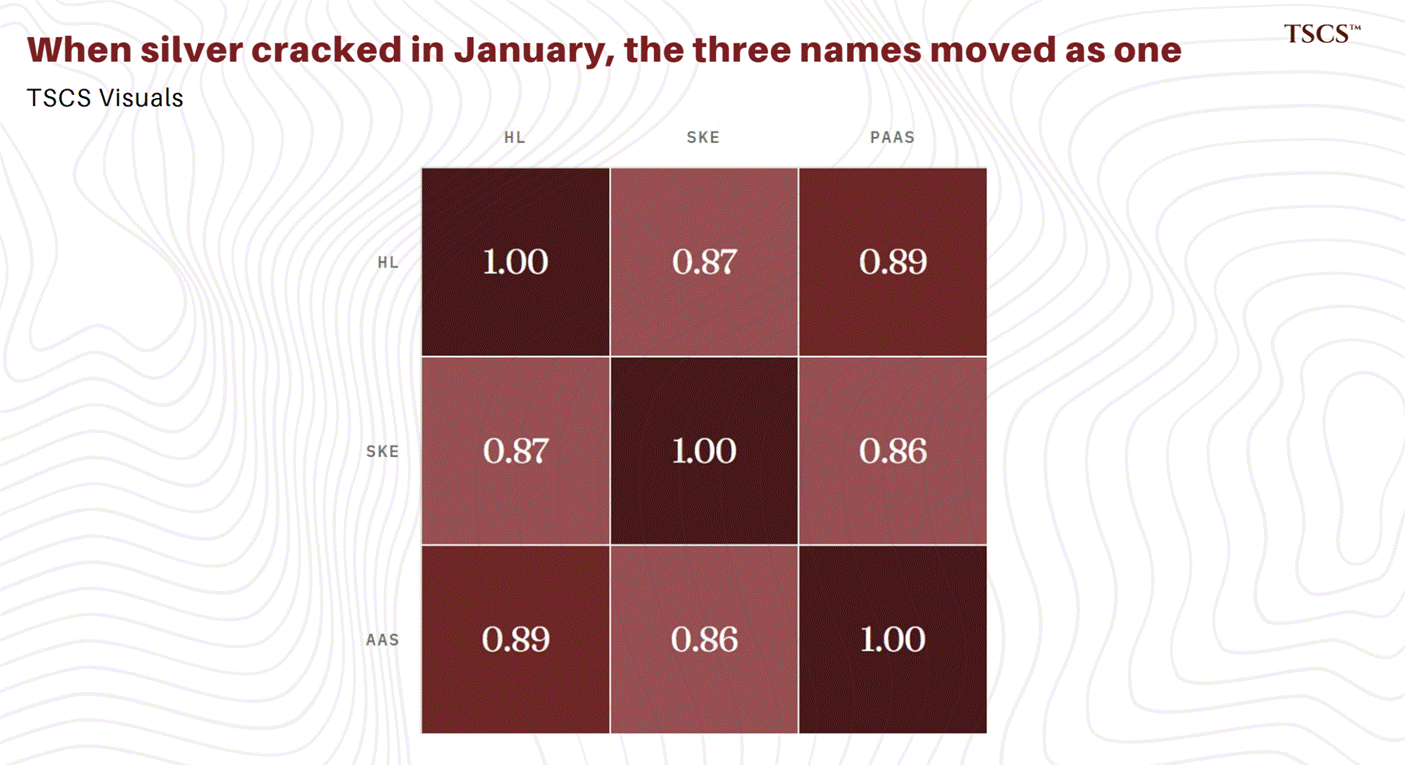

The sleeve is meaningful but bounded. Daily correlation across the three names exceeded 0.85 for two weeks during the January crash. This is not a diversified basket. It is one concentrated silver equity bet expressed across three positions. Hecla core, Skeena secondary, PAAS smallest.

The basket got worse, faster than the beta math suggests

One fact about this sleeve before going to names. Across the three active positions (Hecla, Skeena, Pan American), daily correlation during the late-January to early-February silver crash exceeded 0.85 for two consecutive weeks. This is not three diversified positions. It is one concentrated silver equity bet expressed across three names. The benefit of holding three rather than one is reduced name-specific tail risk (one Mexican regulatory event, one grade reconciliation surprise), not portfolio diversification. Total sleeve size should reflect that. My own sizing landed on meaningful but bounded, with Hecla as core, Skeena secondary, Pan American smallest.

Run Hecla and Skeena only if you weight tail risk more heavily. Push higher if you accept the correlated bet. A Kelly or Sharpe-optimized construction concentrates into Hecla and trims Pan American.

The three-name structure trades quality-adjusted returns for cycle coverage and Escobal optionality.

Now the basket. Everyone is watching silver versus SIL beta. The 0.95 to 1.2x basket capture is the cleanest evidence that the gold miner 2009 to 2011 analog binds: rising AISC, declining grades, consensus models lagging spot, byproduct credit dependency. The standard interpretation is that miners are a worse trade than the metal at any sizing.

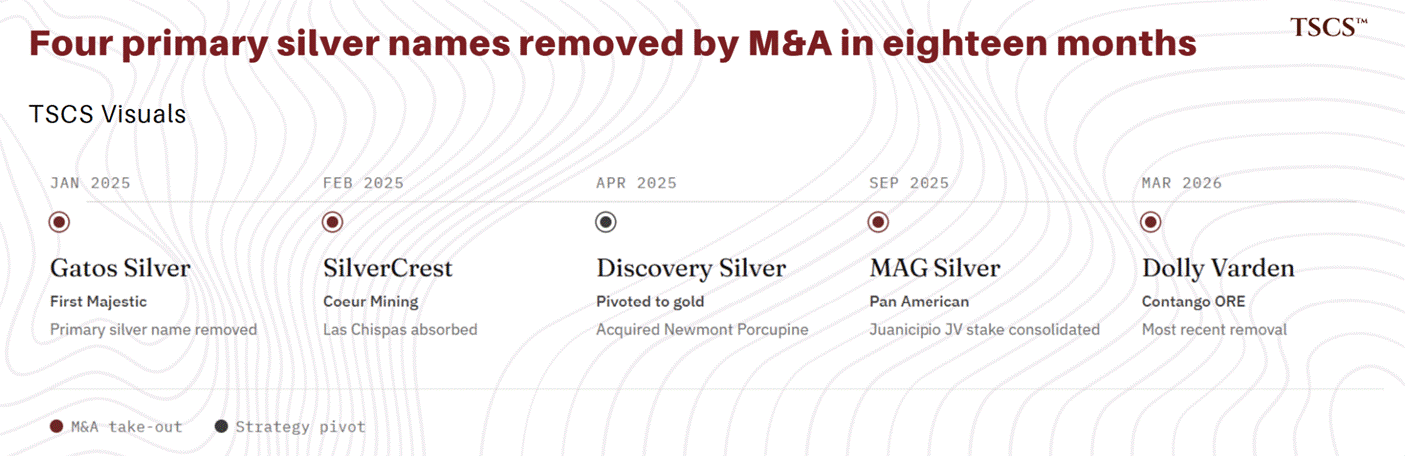

SilverCrest (Coeur, Feb 2025), Gatos (First Majestic, Jan 2025), MAG (Pan American, Sep 2025), and Dolly Varden (Contango, Mar 2026) all left the basket via acquisition. Discovery Silver pivoted to gold by acquiring Newmont’s Porcupine complex in April 2025. The companies left in SIL did not generate the 0.95 to 1.2x figure. Per the Global X N-CSR filing as of October 31, 2025, the top two holdings (Wheaton Precious Metals and Pan American Silver) account for approximately 34% of fund net assets, down marginally from 36.6% in April 2025 as the broader basket rallied. PAAS weight oscillated between 11% and 13%, not monotonic expansion. The structural point holds. Top-heavy basket concentrated in two names, more concentrated than the historical SIL profile.

The drift shows up in the disappearance of names that used to dilute it. Four primary-silver names gone via M&A in eighteen months, plus the Discovery pivot to gold. The basket bet does not just deliver disappointing beta. It delivers it from a portfolio that has been gutted. Hickey has been flagging this acquisition-driven thinning in successive High-Tech Strategist letters across 2022 to 2026, and his framework converges on curation as the value-add. The curation argument does not depend on Hickey. The M&A wave is public record. The conclusion follows from the data.

Three names made it through my framework as the active sleeve. A fourth (Vizsla) I cover but do not recommend. The January 23 abduction at Panuco (nine confirmed dead) triggered my pre-set kill switch. Reinstating after the event would soften the rule retrospectively. I am not doing that. Full reasoning in the Vizsla section.

Skeena as gold-carried developer where silver is a 9.5 Moz free option the market is not pricing. Hecla as the only debt-free US and Canada silver producer, 6.4% FCF yield at spot. Pan American as Juanicipio embedded value plus Escobal optionality, against the rich consensus NAV multiple. All three carry gold revenue. That is intentional. The pure-play primary silver name in a tier-1 jurisdiction with operational reliability is extinct as a category.

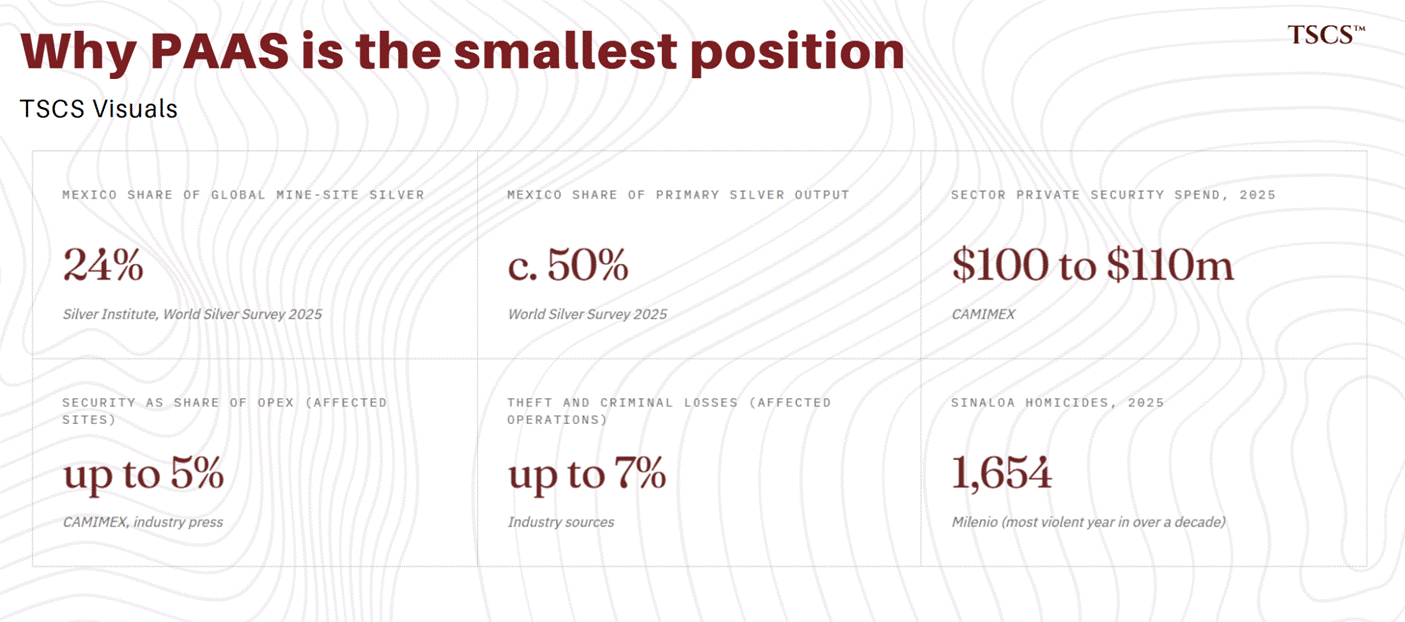

On Mexican country risk. Mexico accounts for approximately 24% of global mine-site silver supply per the Silver Institute’s World Silver Survey 2025, on national production of roughly 186 to 200 Moz against 819.7 Moz of global output. Mexico also accounts for roughly half of dedicated primary silver mine output. The 28% figure sometimes cited in silver coverage is the primary silver share of total global silver production, not Mexico’s country share. Both are large, both matter, neither is interchangeable. CAMIMEX has reported sector-wide private mining security spending in the area of $100 to $110 million for 2025, with industry sources citing security costs running up to roughly 5% of operating expenses and material losses from theft or criminal assault running up to 7% of operational costs at affected operations. Press coverage puts the protection-fee rate at approximately 3% of revenue. Milenio reporting puts Sinaloa homicides at approximately 1,654 in 2025, the most violent year in over a decade. Treat as directional, not audited.

The Vizsla incident is the most visible recent event. It is not isolated. The Mexican jurisdictional discount applies more aggressively than I was modeling. The PAAS sizing reflects that.

Methodology, sourced upfront

What I am relying on, what I am modeling against, where the data comes from. The caveats apply throughout.

Silver at $76.44 intraday May 15 after a -8.48% single-session move from yesterday’s $83.52 close. May 11 close was $75, May 13 peak was $89, May 14 close was $83.52. Silver has given back the entire May rally in two sessions. Down from the $121.67 high on January 29.

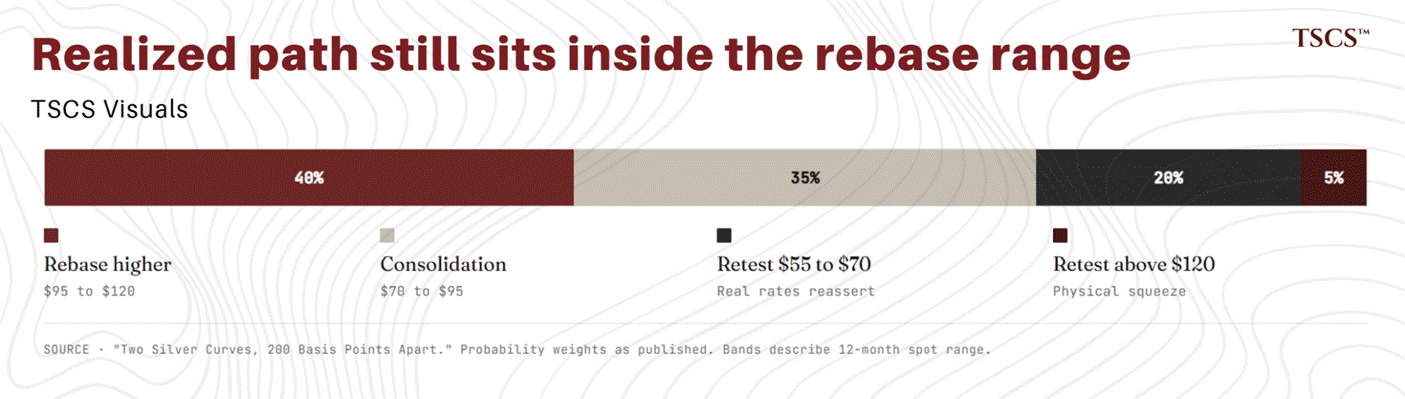

Gold at $4,546. NPV math in the name sections below uses the May 13 peak deck ($89 silver / $4,698 gold) as the analytical anchor. At current $76.44 / $4,547 spot, dollar figures scale roughly 14% lower; structural conclusions unchanged. Scenario distribution from “Two Silver Curves, 200 Basis Points Apart” (40% rebase higher, 35% consolidation, 20% retest of $55 to $70, 5% retest above $120). Realized path sits inside the rebase range. I am not unilaterally revising the published probabilities.

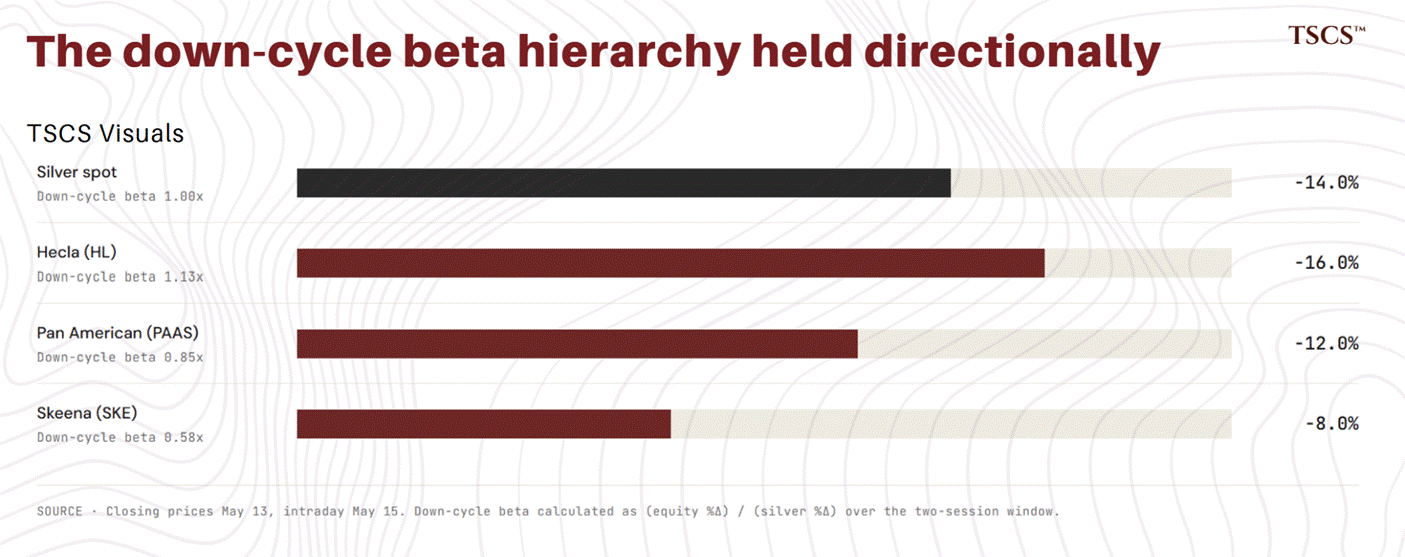

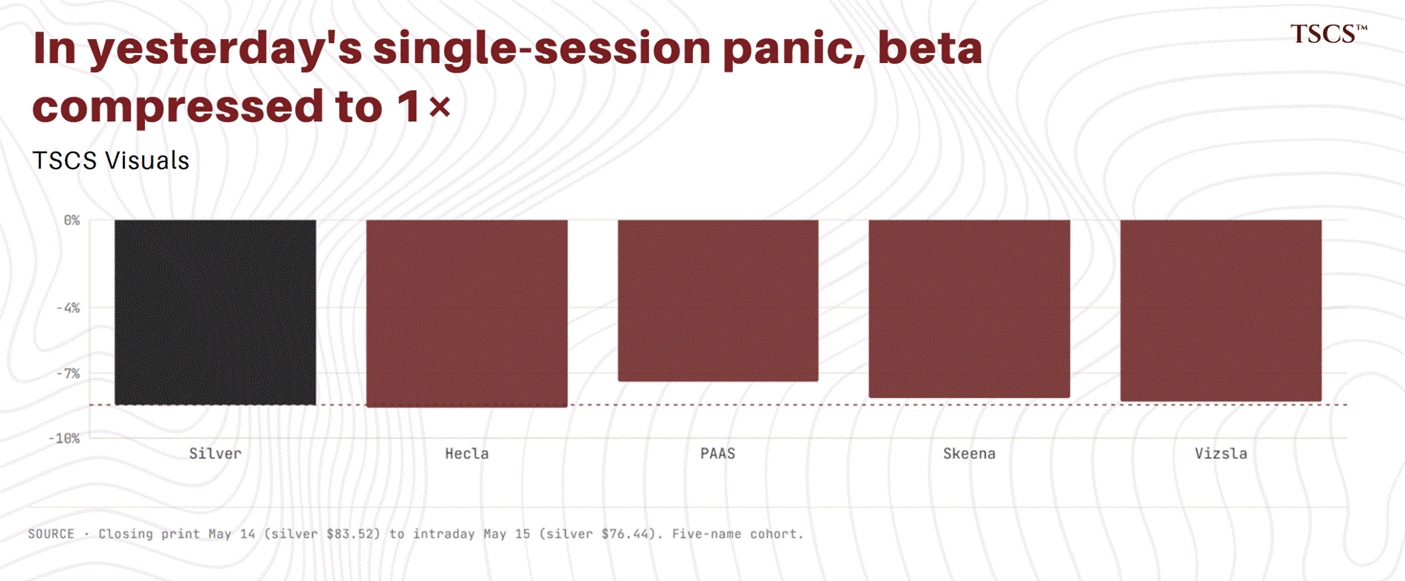

Cohort prices, intraday May 15: Hecla (HL) $17.78 NYSE, Skeena (SKE) C$43 / US$31.17, Pan American (PAAS) C$78 TSX / $56.59 NYSE, Vizsla (VZLA) C$4.75 / approximately $3.44 USD. From the May 13 peak to current: silver fell 14%, Hecla fell 16%, PAAS fell 12%, Skeena fell 8%. The down-cycle beta hierarchy held directionally: HL 1.13x, PAAS 0.85x, SKE 0.58x. Lower silver content, more share-price protection, exactly as the gold-carry thesis predicts. From yesterday’s May 14 close alone: silver -8.48%, HL -8.61%, PAAS -7.39%, SKE -8.17%, VZLA -8.33%.

Today’s single-session panic compressed the cohort to roughly 1x silver beta across the board.

Five things to flag upfront.

Q1 2026 prints are not steady state. Hecla’s Greens Creek AISC of negative $8.39 and Pan American’s silver-segment AISC of $6.63 are byproduct credit artifacts. Strip the gold, zinc, and lead credits and both move up by $15 to $25 per ounce. I model on full-year 2026 guidance midpoints. Q1 figures appear as markers of where the byproduct stack currently sits, not as forward estimates.

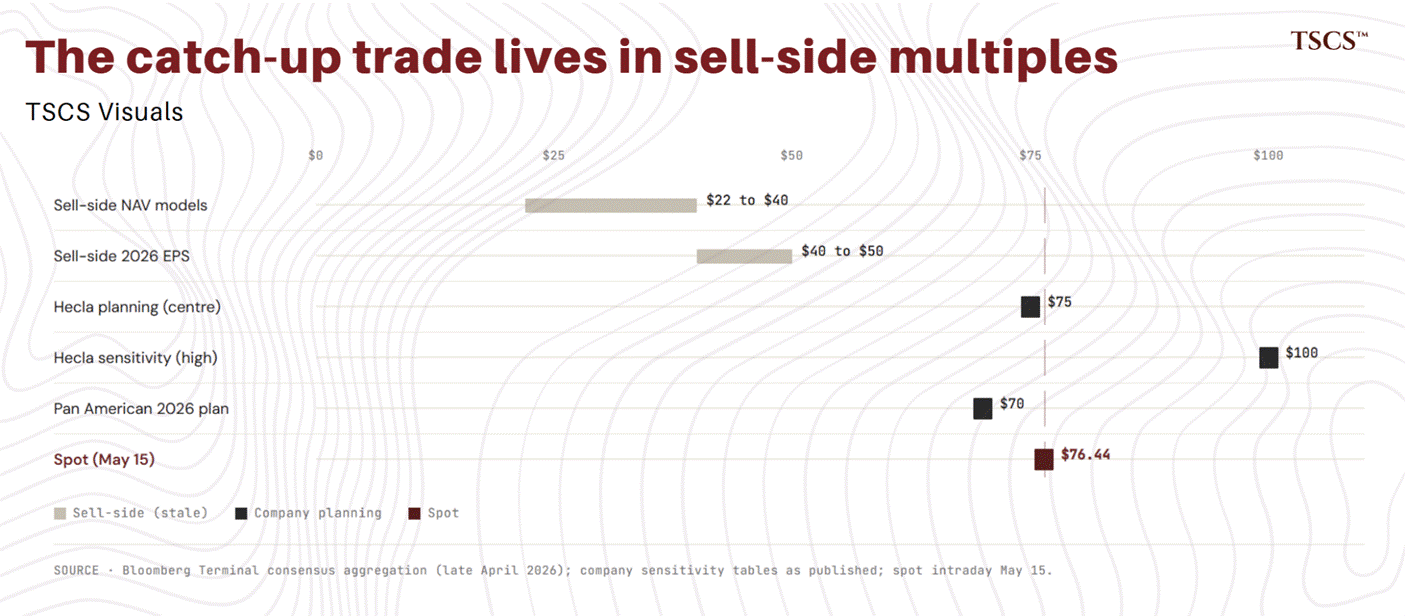

Sell-side models embed silver below spot. Bloomberg Terminal consensus aggregation in late April had the cohort modeling silver at $40 to $50 for 2026 against realized averages closer to $90. Company-level planning is higher: Pan American’s 2026 outlook uses $70 silver and $4,200 gold, Hecla’s sensitivity tables centre on $75 and $100 cases. The catch-up trade lives in sell-side multiples. Company guidance has already caught up. Catch-up is the load-bearing assumption in the PAAS bull case. If it does not happen, PAAS breaks first.

AISC is not standardized. Allocation methods differ, some companies include corporate G&A, some attribute at economic interest versus full ownership. Cross-name AISC comparison is hard. I cite consolidated guidance midpoints where they exist and flag where I am estimating.

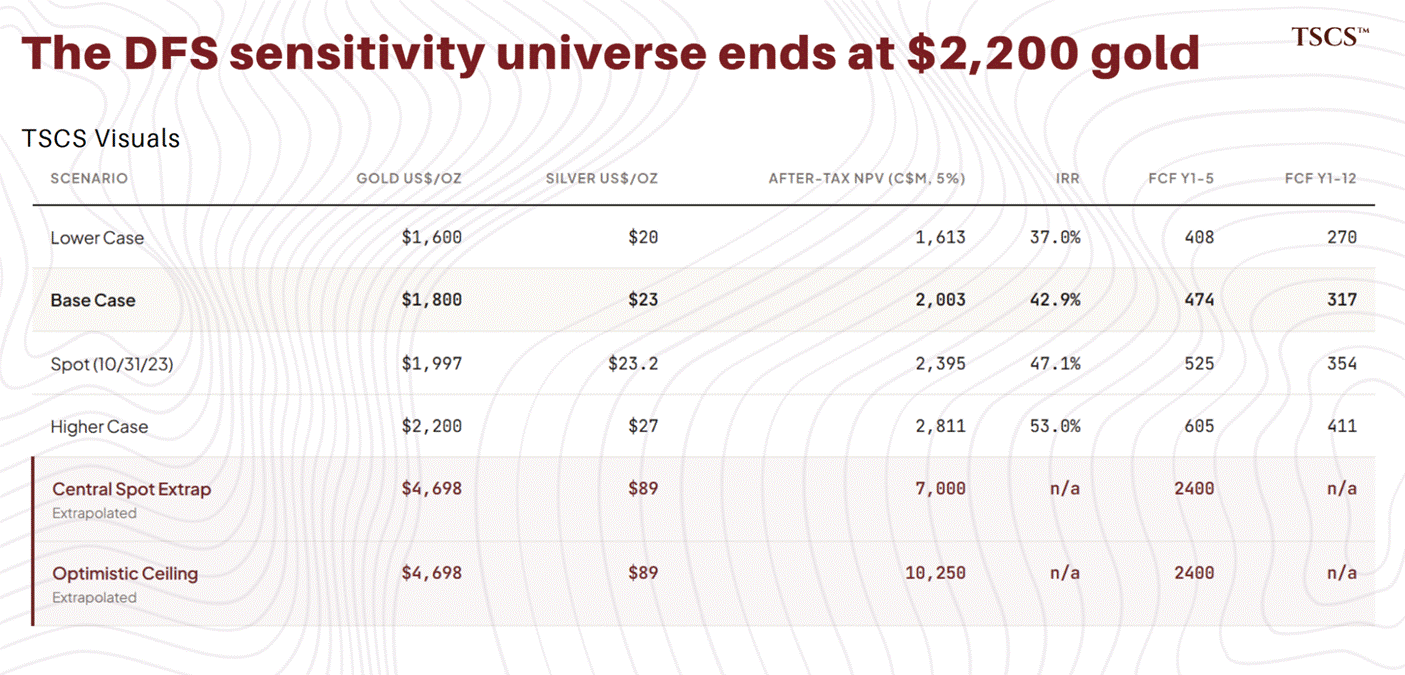

NPV extrapolation is methodologically heavy at current spot. Skeena’s DFS sensitivity envelope tops out at $2,200 gold and $27 silver. Spot is 2.6x and 3.3x outside that. MAG’s Technical Report tops at $1,750 and $22, with spot 2.7x and 4.0x outside. Vizsla’s FS sensitivity tops at +50% from basecase, with spot 2.5x or more outside. Linear extrapolation does not capture cost inflation at higher prices, tax stack changes, royalty step-ups, or grade-recovery non-linearities. I run an optimistic ceiling figure and apply a 25 to 35% conservatism discount for the central case. The central case is the anchor figure. The optimistic ceiling is the upside band. November 2026 (Skeena) and Q2 (PAAS) updates will replace these extrapolations with company-modelled economics at updated metal-price decks.

Bloomberg Terminal is the institutional standard for sell-side consensus aggregation. Where I cite a 1.55x consensus NAV multiple or an 8-analyst sample, the figures are terminal-verified. Macro framing (real rates correlation, gold-silver ratio) uses annual averages from FRED and LBMA. Monthly Bloomberg data tightens magnitudes. Direction holds either way.

I do not disclose position details in published research. Treat the analysis as independent of any position I may hold.

Why the gold analog binds partially

The 2009 to 2011 gold miner analog binds, less tightly than the headline suggests.

During the 2009 to 2011 gold bull market, the HUI Gold Bugs Index delivered approximately 1x gold’s return. The 3 to 8x operating leverage that simple cost-spread arithmetic predicted did not materialize. Costs ate part of the leverage, grades ate more, consensus lagged throughout. The same mechanisms operate in silver miners 2024 to 2026.

SIL’s rolling 1-year beta to spot silver has run between 1.2x and 1.8x across post-2010 history, not the 2x to 3x figure that shows up in retail commentary. The “lost torque” framing in this piece is most accurate against the upper end of that band (1.6x to 1.8x sustained beta), not against an aggressive 2x to 3x baseline. The basket-level compression toward 1.0x holds either way. The magnitude of the compression is smaller than the 2x to 3x baseline implies. The defensible version: the basket used to deliver 1.5x to 1.8x and now delivers 1.0x to 1.2x. The aggressive framing does not survive audit.

The analog binds less tightly than the historical baseline for three reasons.

First, the magnitude of the silver price move (from $25 in early 2024 to a peak above $120 in January 2026) is larger in percentage terms than the gold move in 2009 to 2011. Margin expansion is genuinely greater. The catch-up trade has more room because the gap between modeled silver price and realized silver price is wider for most names than the comparable gap was for gold miners in 2009 to 2011.

Second, the silver miner universe consolidated. Four primary-silver names gone via M&A in eighteen months. SIL is now roughly 22% Wheaton plus a much shorter list of primary producers. The basket effect that diluted gold miner outperformance in 2009 to 2011 (where hundreds of names were available) is meaningfully reduced. Concentrated positions in 4 names out of an 8-name primary silver universe carry much higher tracking error to the basket than concentrated positions in 4 of 80 names.

Third, the structural physical scarcity thesis from the prior piece (200 basis point convenience yield gap, 312 Moz COMEX warehouse drawdown, Shanghai premium) is more acute than the 2009 to 2011 setup, which was primarily an investment demand story. If physical scarcity sustains silver above $100, the equity catch-up trade gets sharper because consensus models embed silver well below current spot.

None of the three is a guarantee. They are arguments for why the analog binds less tightly. The base case remains that silver miners deliver close to 1x silver beta over the next twelve months. Alpha, if it exists, is in concentrated names that score on consensus model lag, operational reliability, and jurisdictional discount.

The three active names in this piece are my best attempt to identify that alpha. Skeena through embedded silver in a gold-economic project. Hecla through jurisdictional safety in a debt-free portfolio. Pan American through Juanicipio cash flow translation. I could be wrong on any of these. Most likely on Pan American, because Hickey publicly disagrees and his track record is meaningfully better than mine, and because Mexican country risk has now demonstrated itself as something more material than a tail event in pricing. Most likely right on Skeena, because the project economics are gold-carried and the silver contribution is option-like, and because British Columbia is structurally insulated from Mexican-style risks. Hecla sits between: the multiple is not contrarian but the jurisdictional cleanliness is rare in this cohort and worth its premium.

At $89 silver and $25 AISC, the typical mid-cost silver producer generates $64 per ounce of gross margin. That margin was zero eighteen months ago. The expansion is real. It has not flowed through to equity returns at the basket level because of the four headwinds the prior piece walked through: rising costs, unstable production, lagging consensus models, equity discount for jurisdictional risk.

The trade I am recommending requires three things to hold per name. Consensus 2026 EPS must embed silver meaningfully below spot (most do). Operational profile has to be stable enough that margin expansion actually flows through. Jurisdictional discount has to be either appropriately priced or actively narrowing. Names that score on all three are the trade. Names that look cheap on operating leverage but fail on country risk or operational reliability are value traps.

Why three names and not a more concentrated two-name (Skeena + Hecla) bet? Two answers.

Skeena is pre-revenue. The position works structurally but generates no cash flow until Q3 2027. A 100% allocation to pre-revenue through 2026 misses the silver miner income Pan American and Hecla deliver.

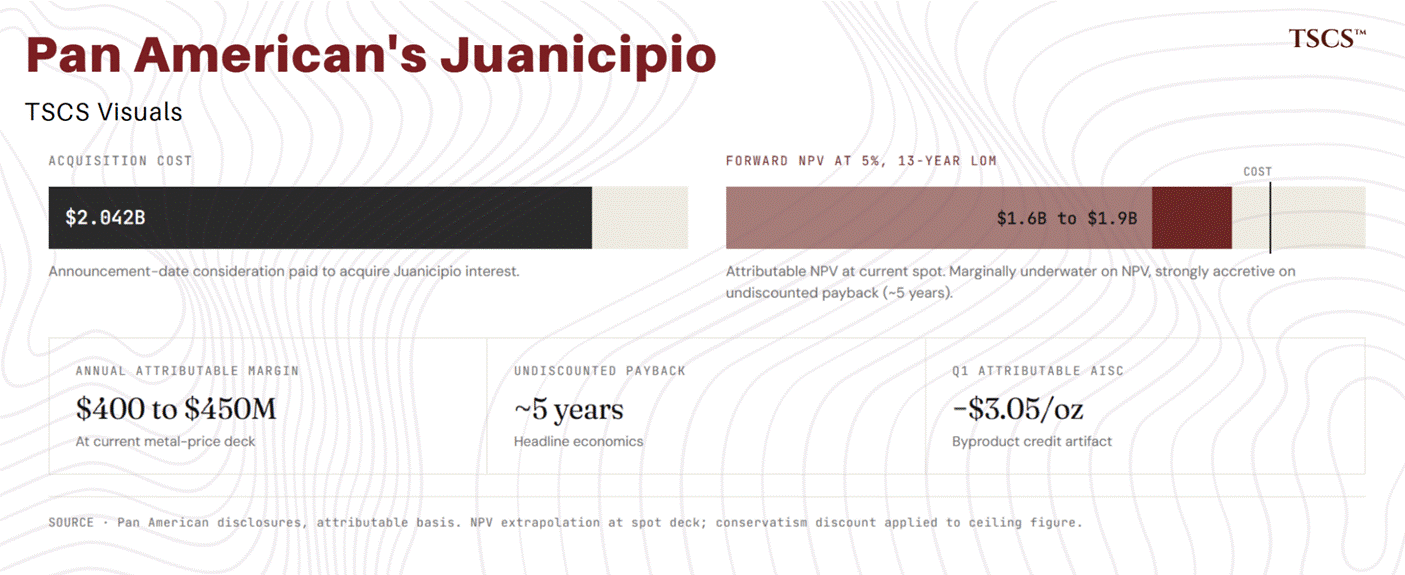

Pan American’s Juanicipio embedded value is real even if not as cheap as it looks. Q1 2026 attributable AISC of negative $3.05 per ounce is not permanent, but the underlying mine economics generate $400 to $450 million per year of attributable margin at current metal prices. Pan American paid roughly $2.042 billion in announcement-date consideration. Undiscounted payback is approximately five years. On a strict 5% NPV basis with a 13-year LOM, forward attributable NPV at current spot is approximately $1.6 to $1.9 billion, modestly below the $2.1 billion cost. The asset is strongly accretive on a payback basis and marginally underwater on NPV. Worth taking. Not the bargain the headline economics imply.

The three-name structure trades concentration for cycle coverage. A two-name structure would generate higher quality-adjusted returns through a Scenario 3 but miss the operating leverage in PAAS. A reader who weights Scenario 3 above 25% should run Skeena and Hecla only.

Real rates and the gold-silver ratio

The mechanism that should be working is not working. Silver has historically traded inversely to 10-year real yields, rolling correlation of minus 0.5 to minus 0.7. The classical mechanism: silver yields nothing, real rates are the opportunity cost, when rates rise silver falls. The 22-year history is clean enough to anchor a position.

Through 2024 to 2026 the correlation flipped. Pre-2024 silver-TIPS correlation runs minus 0.62. Post-2024, plus 0.48. They move together now. The trade in this piece is a bet that the inversion sticks. If the historical mechanism reasserts with real rates at 1.99%, silver mean-reverts to $50 to $60 and the cohort goes with it.

Sell-side consensus NAV models embed silver at $22 to $40 per ounce per Bloomberg Terminal aggregation as of late April. Spot is $76 today. Sell-side 2026 earnings decks separately sit at $40 to $50. Company-level planning is closer to spot: Pan American’s 2026 outlook assumes $70 silver and $4,200 gold, and Hecla’s published sensitivity tables centre on $75 with a $100 case. The catch-up trade is narrower than the stale-deck framing suggests. The mispricing is in sell-side multiples. Companies have already updated. The wider question is whether either anchor survives if the correlation reasserts.

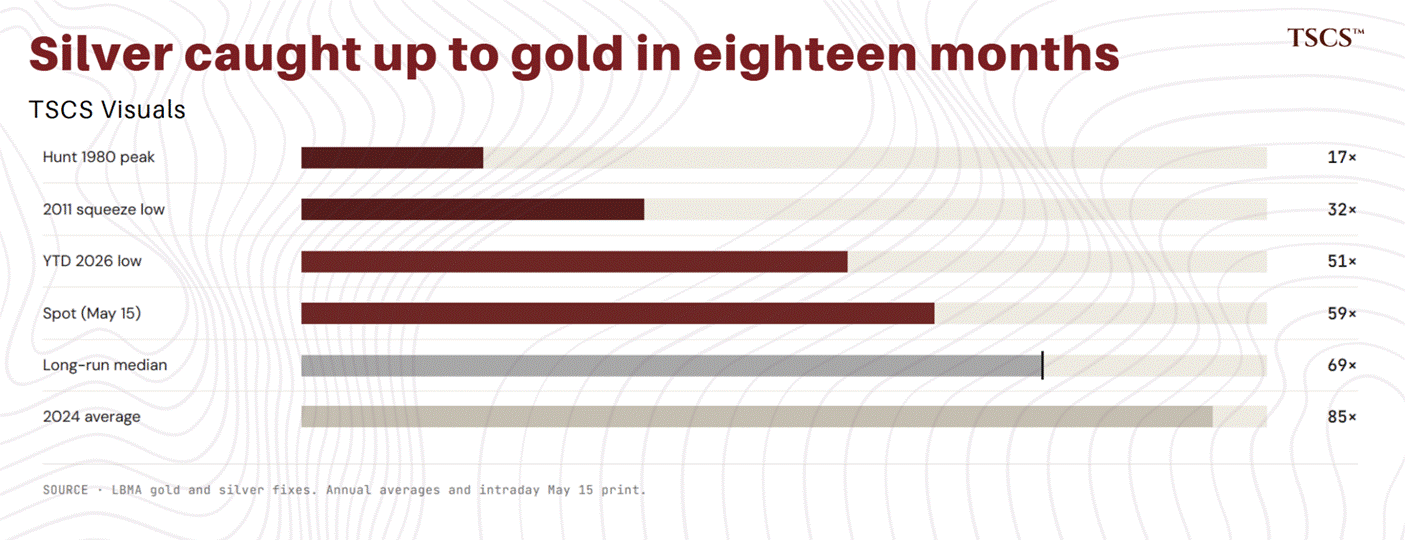

The gold-silver ratio compressed from 85 in 2024 to 51 YTD, 59 at spot. The long-run median is 69. Silver caught up to gold in eighteen months. Below 50 has marked silver tops twice: Hunt 1980, 2011 squeeze. Two data points is not a signal. Tactical context. Whichever framing you bring (rich versus gold, or new regime), the easy phase of the catch-up is priced in.

Below the paywall: NPV math at peak deck and current spot for each name, position sizing across the three-name sleeve, named kill switches per position with the exact triggers that exit the trade, entry levels, the Pretium Brucejack case study every BC developer holder should read before Skeena commercial production, the Vizsla rule discipline and what it cost, scenario analysis on what breaks first in a $50 silver retest, and the full Q2 2026 to Q3 2027 catalyst calendar.

Silver crashed 8.48% in a single session today. The Q2 print cycle starts in eight weeks. The basket is dead. The work is what is left.

Subscribe to read the rest.

Where consensus disagrees, name by name

Keep reading with a 7-day free trial

Subscribe to TSCS to keep reading this post and get 7 days of free access to the full post archives.