The Paper Strait

Tankers, insurers and a regional trade are one wager on Hormuz. There is no diversification in this note, only the same contingency at four prices.

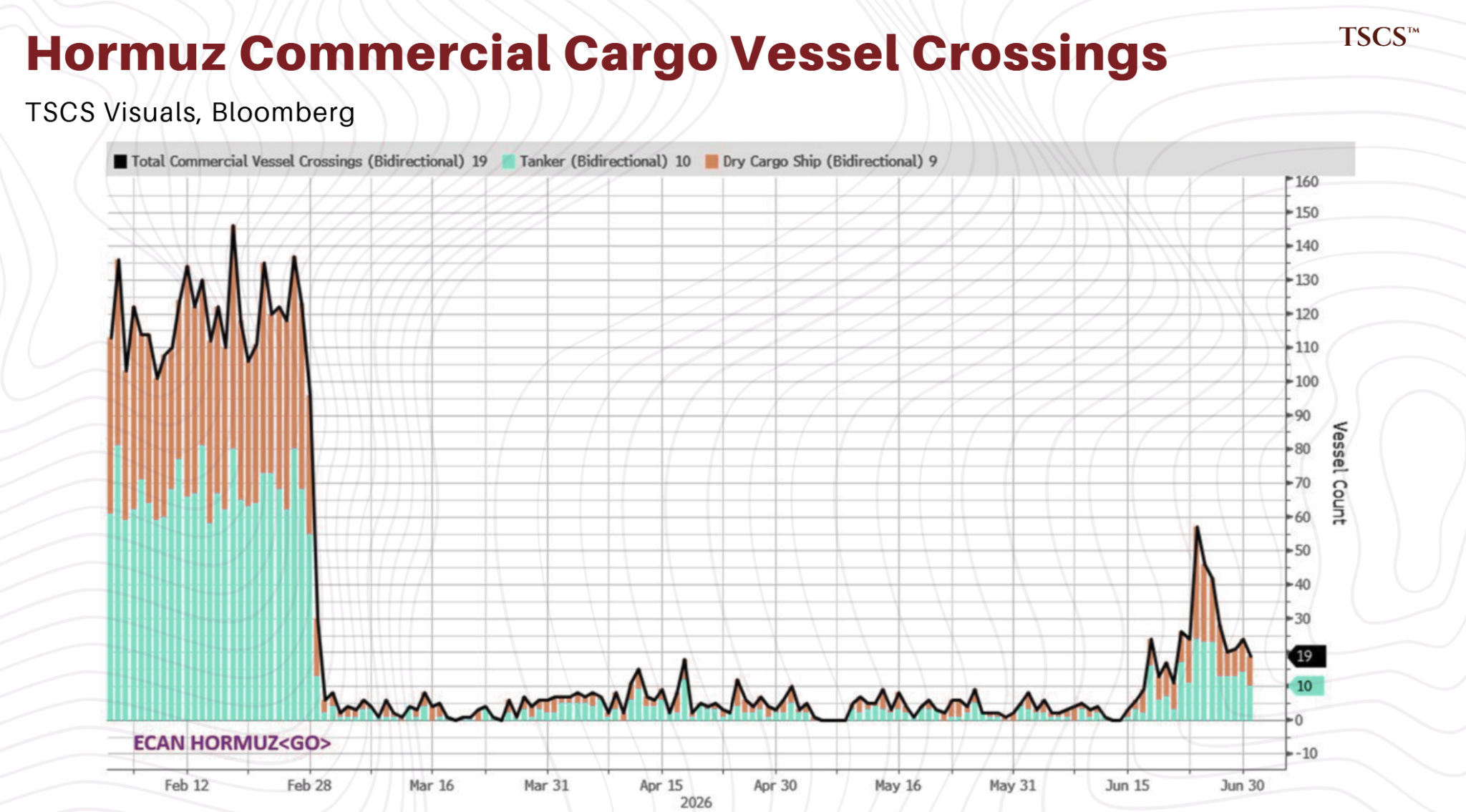

The strait reopened on paper in the middle of June. It stayed ‘reopened’ for about 2 weeks.

In between, the oil market finished its round trip, close to $120 in March, $114 again in early May, back to $72 by the 2nd of July, the futures curve flat at $70 all the way out to 2030, and the listed tanker fleet gave back a 1/5 of its value in 5 sessions.

Then a tanker was hit inside the strait on the 25th of June. Another ship on the 27th.

The escorted southern lane was suspended, the war underwriters put their quotes back up to between 3 and 8% of hull value, and transits, which were supposed to be surging back toward the 130-a-day world of January, stalled at about 40.

At Ras Tanura, the Saudi export complex, loadings resumed on 26 June after a near 4 month halt, and Aramco is ramping hard: 5 supertankers carrying 10m barrels already out through Hormuz, 11 more inbound between 23 June and 1 July, and a switch to spot pricing to move barrels in Asia.

I’m putting the strongest counter datapoint here, because the thesis doesn’t need Saudi barrels to stay trapped. It needs compliant hulls and fixtures to stay scarce, and barrels are recovering faster than hulls: Gulf exports are back to roughly 3/4 of pre war levels while transits still run roughly 70% below, the gap being backlog clearance, AIS dark runs and the dark fleet.

Watch the inbound ballasters. If they normalise and rates print five figures, that is the falsifier arriving on schedule, and this note will say so.

I spent part of this spring in the Gulf, reporting a larger piece that is now in counterparty review. This note is not that article, and none of the people who opened doors for it appear here in any form.

This is where the equity work is, and the views in it are mine alone. I should also put something else on the table before the first balance sheet: I am not a tanker specialist.

Some of you reading this run tanker books professionally, and by the end of this note I hope to convince you that my not being one of you is the least important fact in it, because the mispricing I’m going to describe is not a shipping question. It’s a question about the distance between what gets signed and what gets sailed, and I’ve spent weeks living unusually close to that.

One warning, once, at the top. Everything in this note, the tanker names here, the insurers in the next section, the regional trade at the end, is the same bet wearing different clothes. It all pays if the normalisation of the Strait of Hormuz takes longer than consensus says it should, and it all unwinds together, probably in the same week, if it doesn’t.

There’s no diversification inside this note. There are only expressions of one contingency at different prices. Size like it.

Keep reading with a 7-day free trial

Subscribe to TSCS to keep reading this post and get 7 days of free access to the full post archives.