Underwater at 1%

Negative carry at the Bank of Japan, a 40 year low yen, and the widowmaker stirring." Thirteen words, three hooks, my pick

Japan was the cheapest money on earth for 25 years. Was.

Its central bank is now losing money on its own bonds, the yen is at a 40 year low, and the cheap cash that funded everything from Treasuries to crypto is drying up. If you own bonds, a currency, or anything priced for a world of free money, this is about your book, not Japan’s.

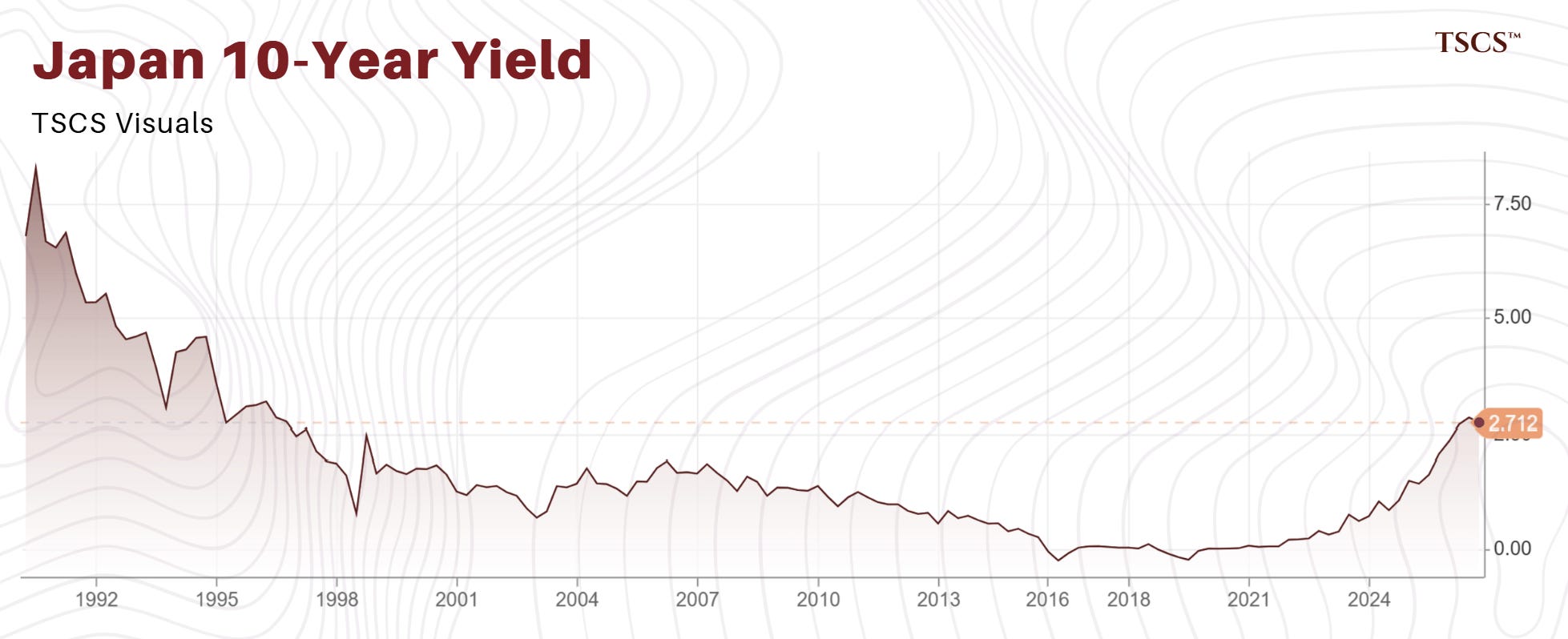

I shorted Japanese government bonds a while ago. It wasn’t some brave contrarian trade. It was the opposite. Everybody wanted it. The debt math looked so broken that shorting it felt like picking money up off the floor. I did it through options, the yield near 60 bp when I put it on. I watched it grind toward 20 while I bled, and in the end I did what everyone does. I gave up near the lows and ate the loss.

They call it the widowmaker for a reason. It kills you because it looks obvious.

Every few years someone works out that Japan cannot go on like this, shorts it, and gets carried out. That crowd is back, and this time they want the yen at 300. I’ve already paid to learn the lesson, so I’m not going to say Japan is finally breaking. I’m going to say something more useful, which is that ‘it’s different this time’, and you can see it in the Bank of Japan’s own accounts. So I went and read them.

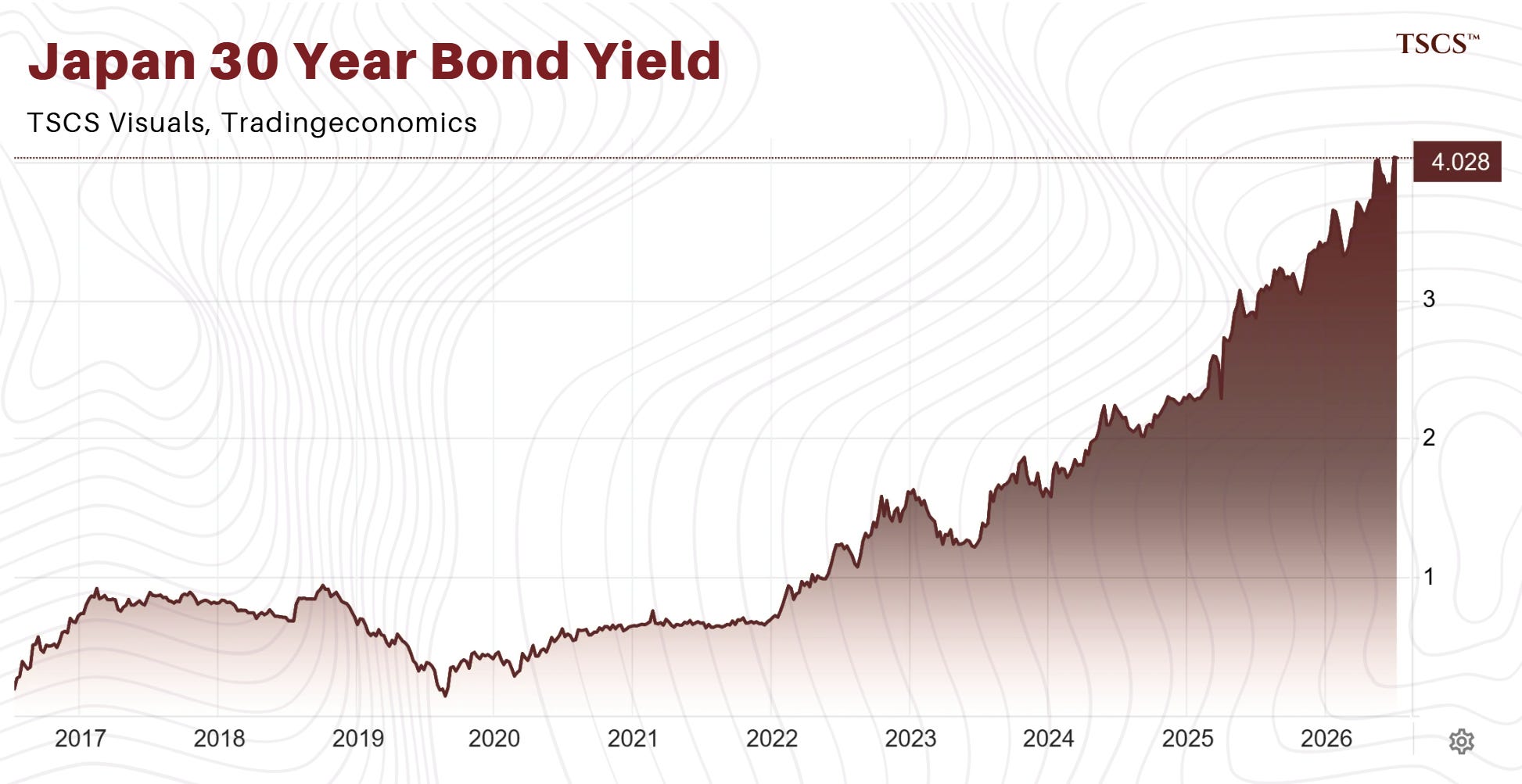

On the 7th of July, Japan sold 30 year bonds at a 4% coupon (now 3.922%), the first time it has ever paid that much, and buyers mobbed the sale, the strongest demand in 7 years. That looks reassuring, right? But look closer. Japan can still borrow. It just has to pay a price it hasn’t paid in a generation.

For 25 years Japan ran the loosest money in the developed world, and that cheap money didn’t stay home. It leaked into everything, Treasuries, credit, emerging markets, the carry trade, crypto. Japan was the quiet lender behind a lot of the world’s risk.

Japan won’t default, it owes the money to itself in its own currency and its central bank holds nearly half the bonds. What we see is something less dramatic.

The argument below is free. The trade, the structure I'd own, the levels that would prove me wrong, and the basket we're building around it, are for paid subscribers.

The reserve leg

The obvious escape I briefly thought of is to cancel the debt. Japan owes it to itself, so merge the central bank into the treasury and let it disappear.

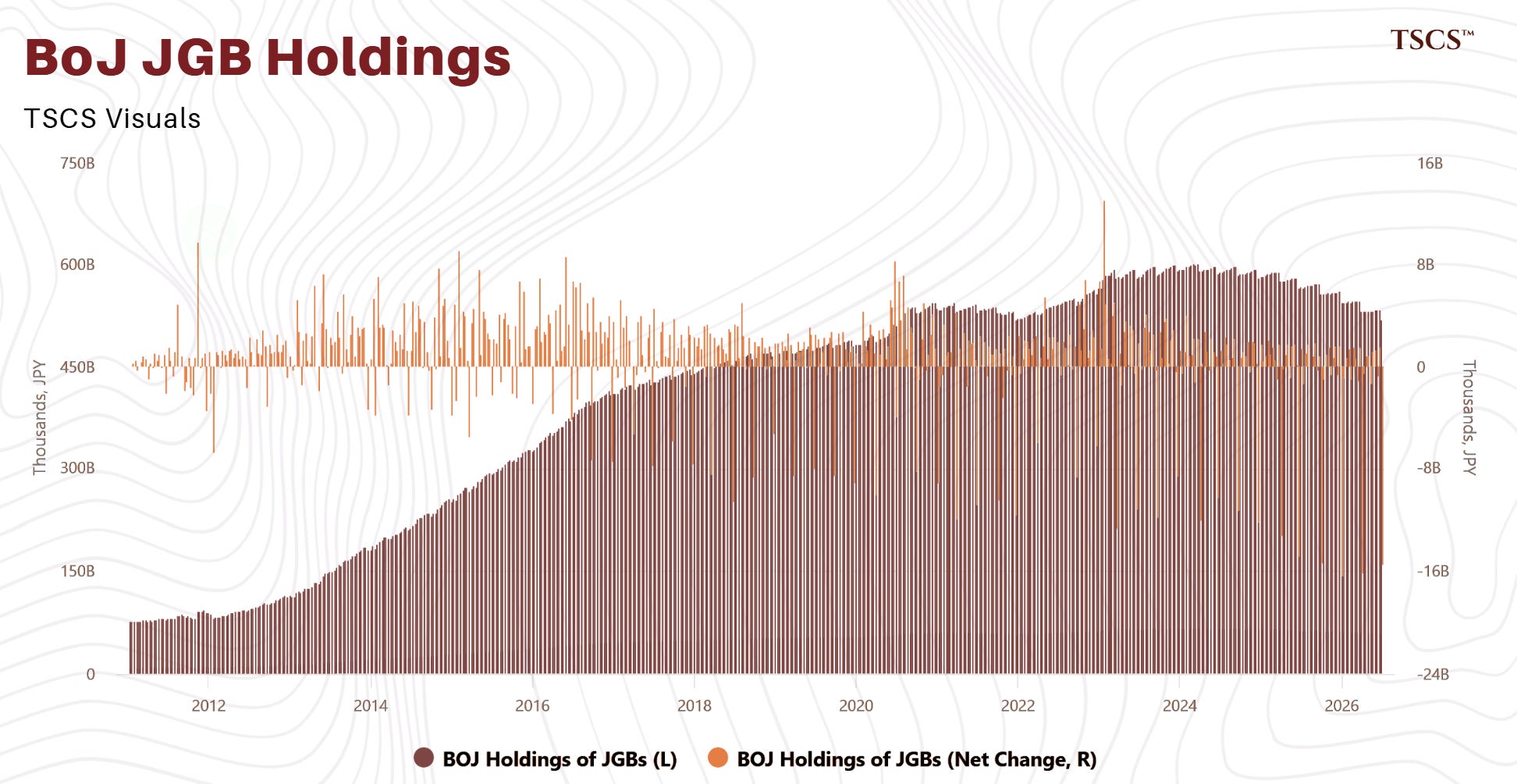

The BoJ holds 518 trillion yen of their bonds, about 48% of it on the Ministry’s latest breakdown, and the Bank is part of the government. That’s what people mean when they say Japan owes the money to itself. Almost half the debt is one arm of the state, the treasury, owing another arm of the state, the central bank. Merge the two and that IOU disappears.

The problem is that this debt already barely counts. When you hear Japan’s debt is 250% of GDP, that’s a gross number. There’s a second number, net debt (takes out the bonds it owes itself) and that’s about 140%. So cancelling those bonds would only make official what the net number assumes (anyone serious about Japan is already working off the 140%).

And even if you cancelled them anyway, the debt wouldn’t really vanish, because of how the Bank paid for those bonds in the first place. It didn’t buy them with nothing. It created reserves to pay for them (440 trillion yen). If you cancel the bond those reserves are still sitting there. All you’ve done is swap a long, fixed rate bond for an overnight, floating rate deposit.

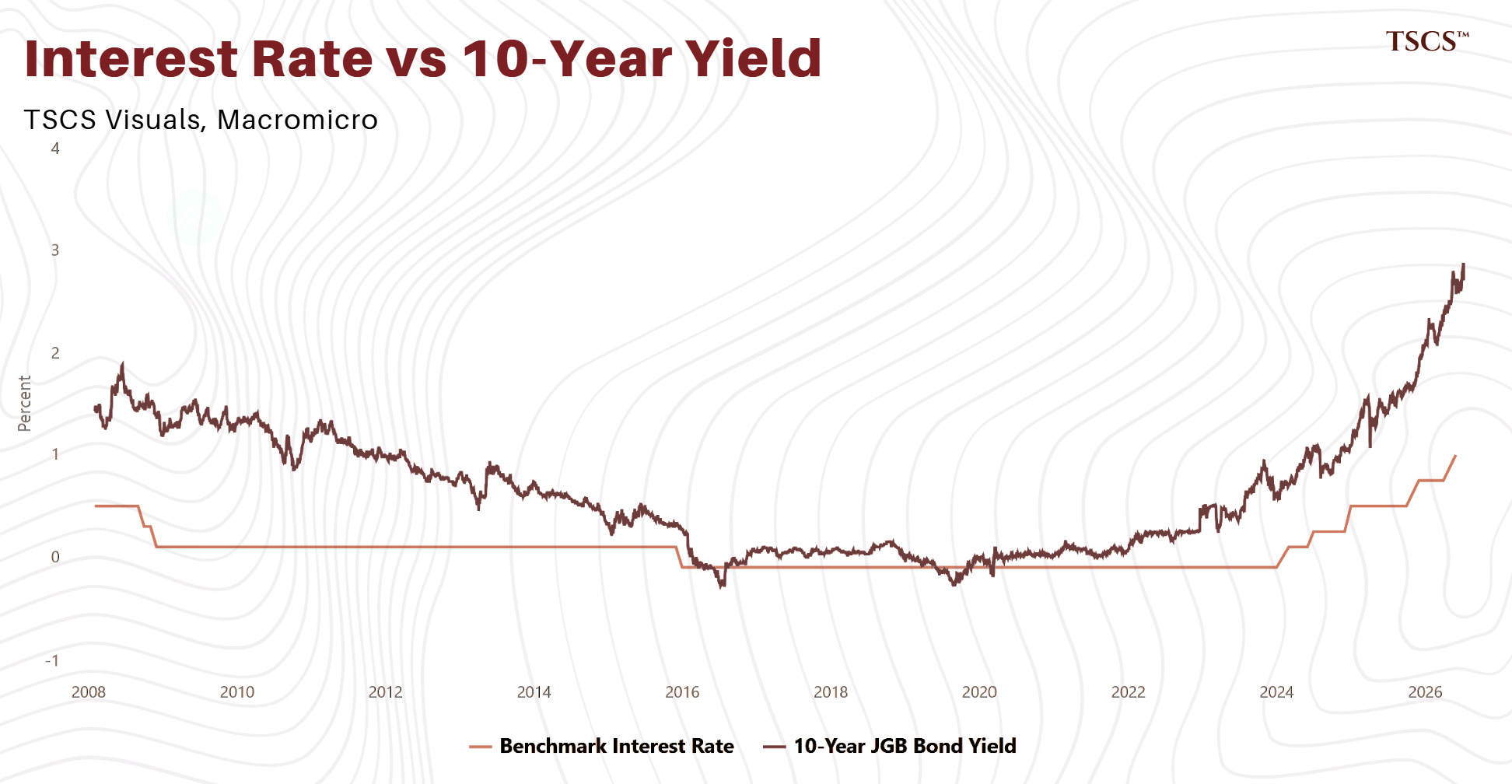

To run a positive interest rate, a central bank has to pay that rate on those reserves. That’s how the policy works, and it’s where the issue lies.

Here are the numbers, from the Bank’s accounts. Last year it earned 2.52 trillion yen on its 518 trillion of bonds, a yield of about 0.5%. At today’s 1% it owes about 4.3 trillion a year on its reserves, more than the entire bond book pays it.

And that bill will obviously climb fast when rates rise, it more than doubled last year, from 1.25 trillion to 2.71 trillion (against 2.52 trillion earned on the book).

The one thing keeping the whole operation out of the red is a quirk of Japanese QE.

Alone among the big central banks, the BoJ spent years buying stocks as well as bonds, a huge pile of equity funds, which pay dividends. That came to 1.63 trillion last year, real and recurring, with a smaller 0.1 trillion from share selling (one off).

They also disclosed over a trillion yen of foreign currency gains last year but it’s mostly the weak yen marking up the Bank’s own foreign assets (that’s cheating!). The Bank’s profit is partly manufactured by its currency weakness. The day the yen turns, that line will clearly turn as well.

Add it up. Coupons of 2.52 trillion plus dividends of 1.63 trillion is 4.2 trillion earnings, against 4.3 trillion going out on reserves. The BoJ is already losing a little on its core business at 1%, and only the one off share sales keep the reported number flat.

The board wants to take rates to 2%. For the government there really is a refinancing schedule, Japan’s bonds average about 9.5 years to maturity, so the treasury only pays today’s rates on the slice it rolls each year. That’s why there’s no cliff for the state. The Bank has no such schedule, reserves aren’t bonds, they’re overnight money. The whole 440 trillion reprices the day the policy rate moves. That’s what QE really did. It took half of a debt that repriced over 9 years and swapped it into a liability that reprices overnight.

So the projection has three moving parts. The rate on reserves rises with policy, fast, on everything. The reserve pile shrinks as QT runs, the Bank let 12.5 trillion of bonds roll off last quarter alone and its own plan has the book down 16-17% by March 2027. And the bond income creeps up, about 2.5 trillion a month and shrinking, now earns 2% and more instead of next to nothing.

Run those together on the way to 2% and the losses peak around 3-3.5 trillion a year, then start narrowing, because the pile they’re paid on is melting underneath them.

Cumulatively that’s maybe 10 trillion of losses against a cushion, provisions plus reserves, of about 14.8 trillion.

A central bank can run on negative equity, it obviously won’t go broke in a currency it prints, and Australia’s has done that since 2022.

There is a real cost, though.

Those reserve payments are actual money flowing from the state to the banks, and if a politician ever tried to make them go away by cancelling the bonds or ordering the Bank to stop paying, the market would not see less debt. It would see a government printing to cover itself, and it would sell the currency.

The only money Japan still gets for nothing is the 115 trillion of banknotes people carry around, which pay nobody. Everything else reprices the moment the Bank raises rates, and no accounting trick reaches it.

The yen

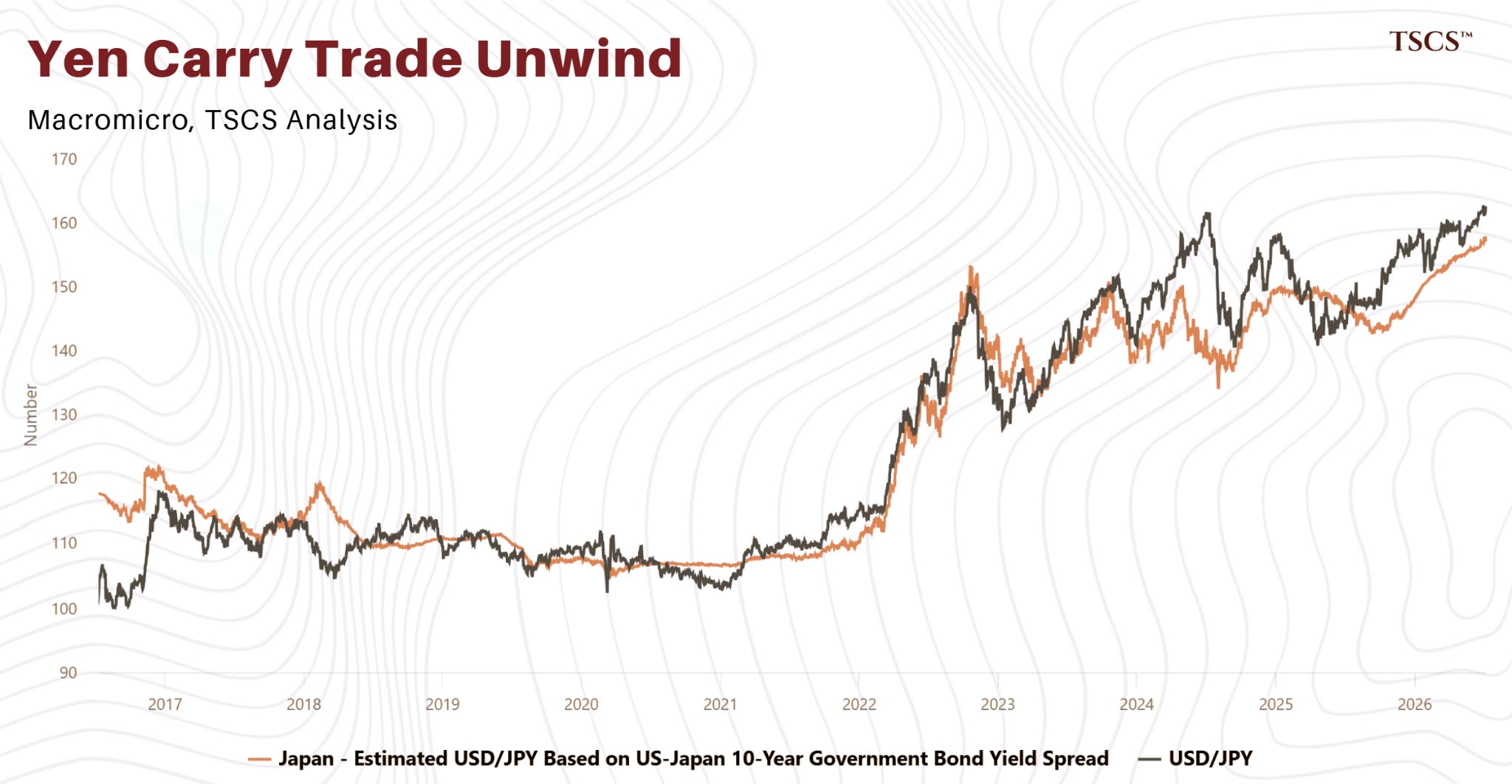

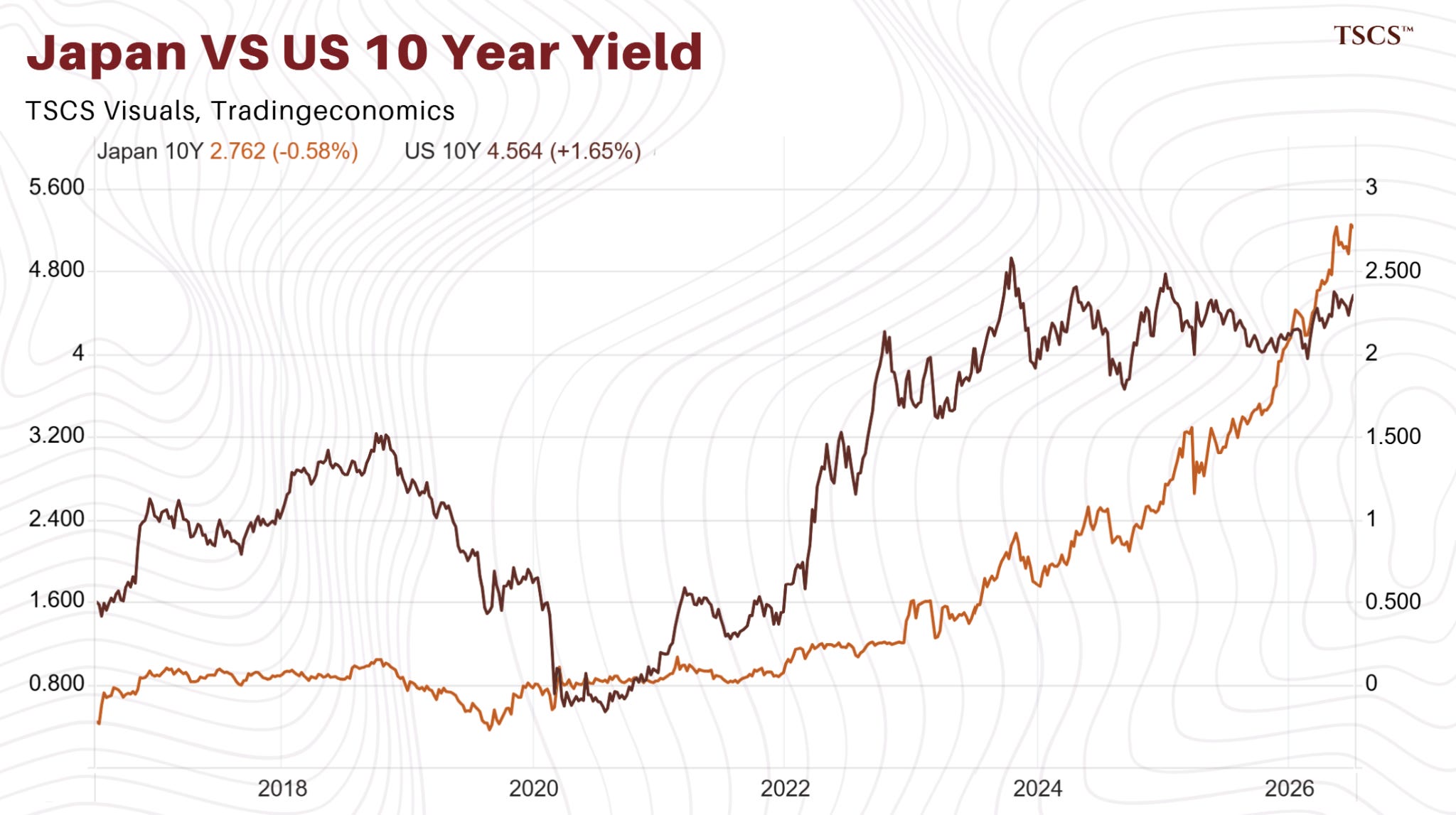

For years the yen moved with the gap between US and Japanese interest rates, the way a carry trade should, wider gap, weaker yen.

That relationship has been dying in stages. The gap peaked in late 2023 and spent the next 9 months narrowing, and the yen weakened all the way to 160 by the spring of 2024. The August 2024 squeeze snapped the two back into line for about a year, which tells you what it took to restore the old relationship, a forced unwind, not a recovery.

Then it broke again. The Bank raised rates toward 1%, the American front end slid, the gap narrowed hard, and on the old relationship the yen should have strengthened.

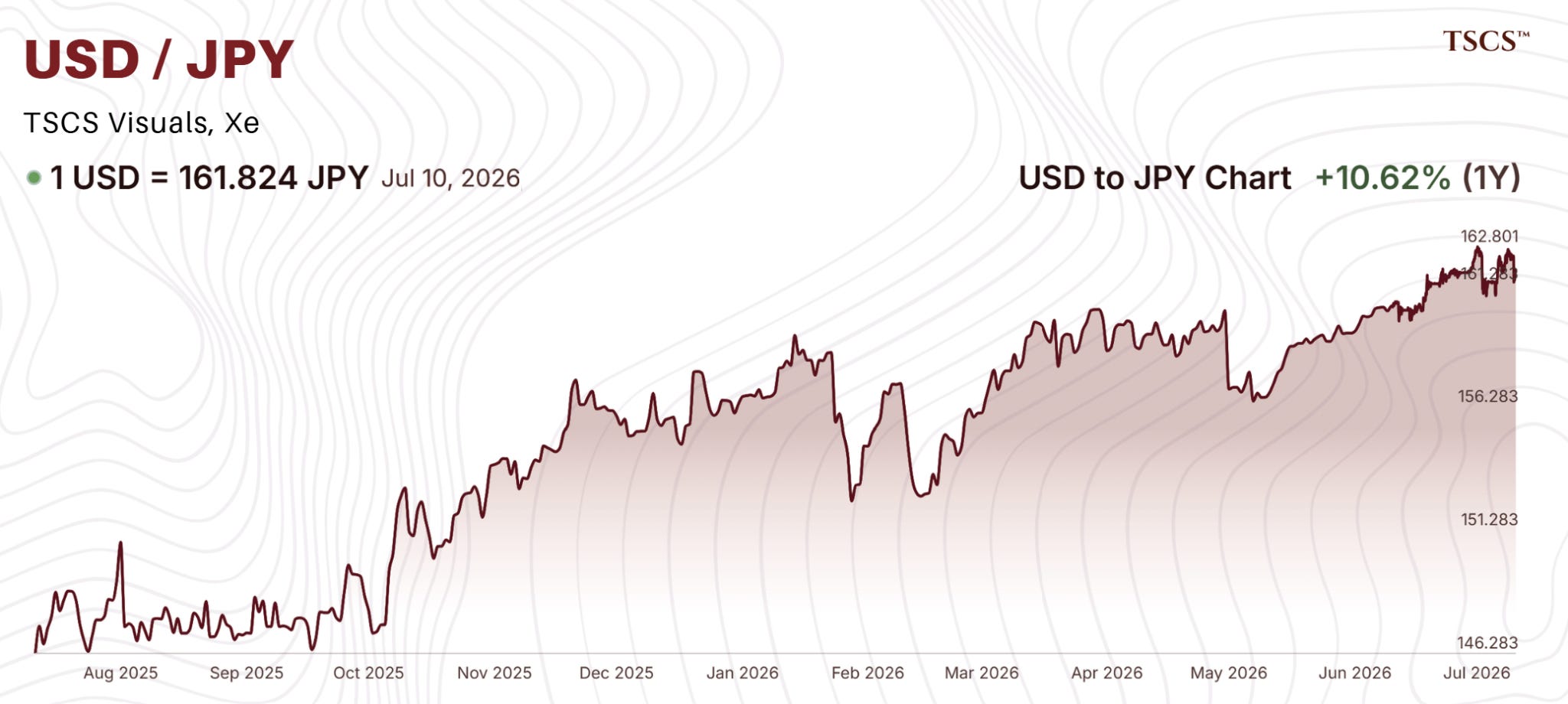

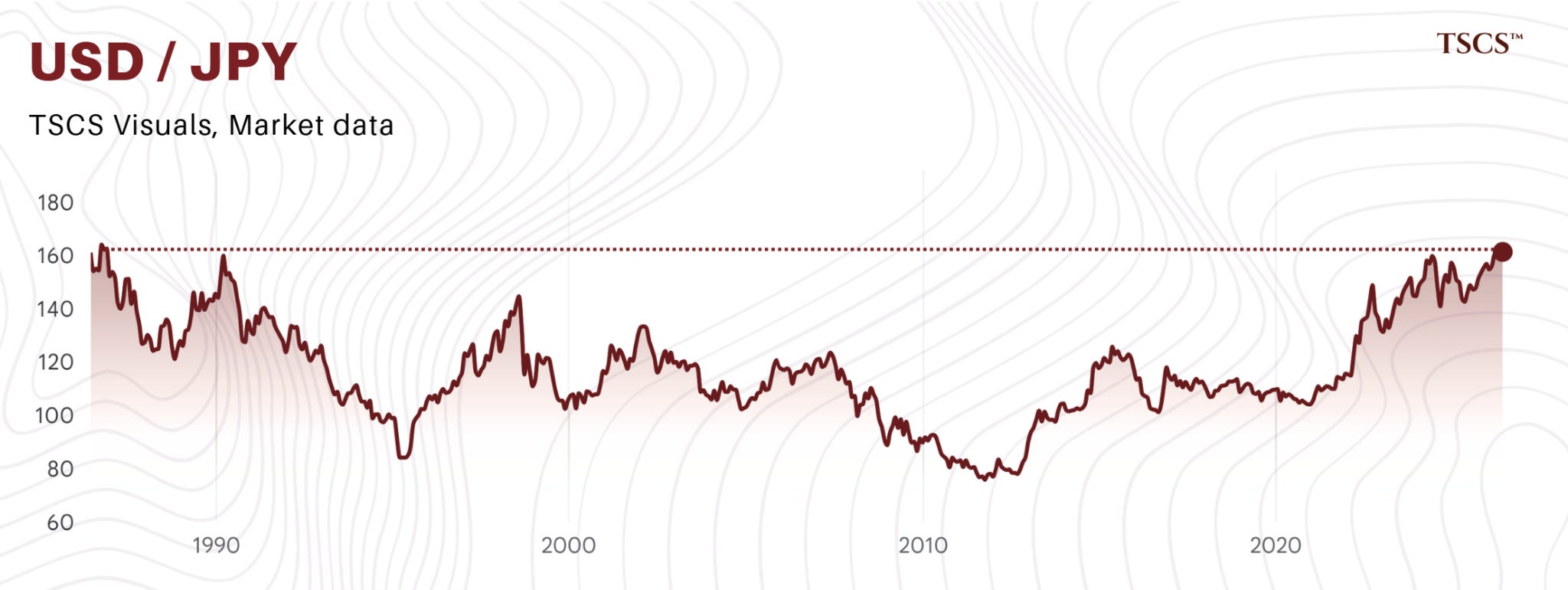

It did the opposite. It fell to a 40 year low and stayed there, around 162, roughly where it sat when the gap was twice as wide.

There are 2 reasons, I’ll explain both.

Japan is still sending money abroad, and the rate gap, even smaller, still pays you to be short the yen. No clever theory required.

But that doesn’t quite explain why a shrinking gap now comes with a weaker yen instead of a stronger one.

The rest is that the market has started charging Japan a small premium, the kind you charge a borrower rather than a carry trade. I’m not going to claim the yen has turned into a credit overnight. But the premium is there and it’s growing.

The repatriation that isn’t

This is where I part company with the doom crowd.

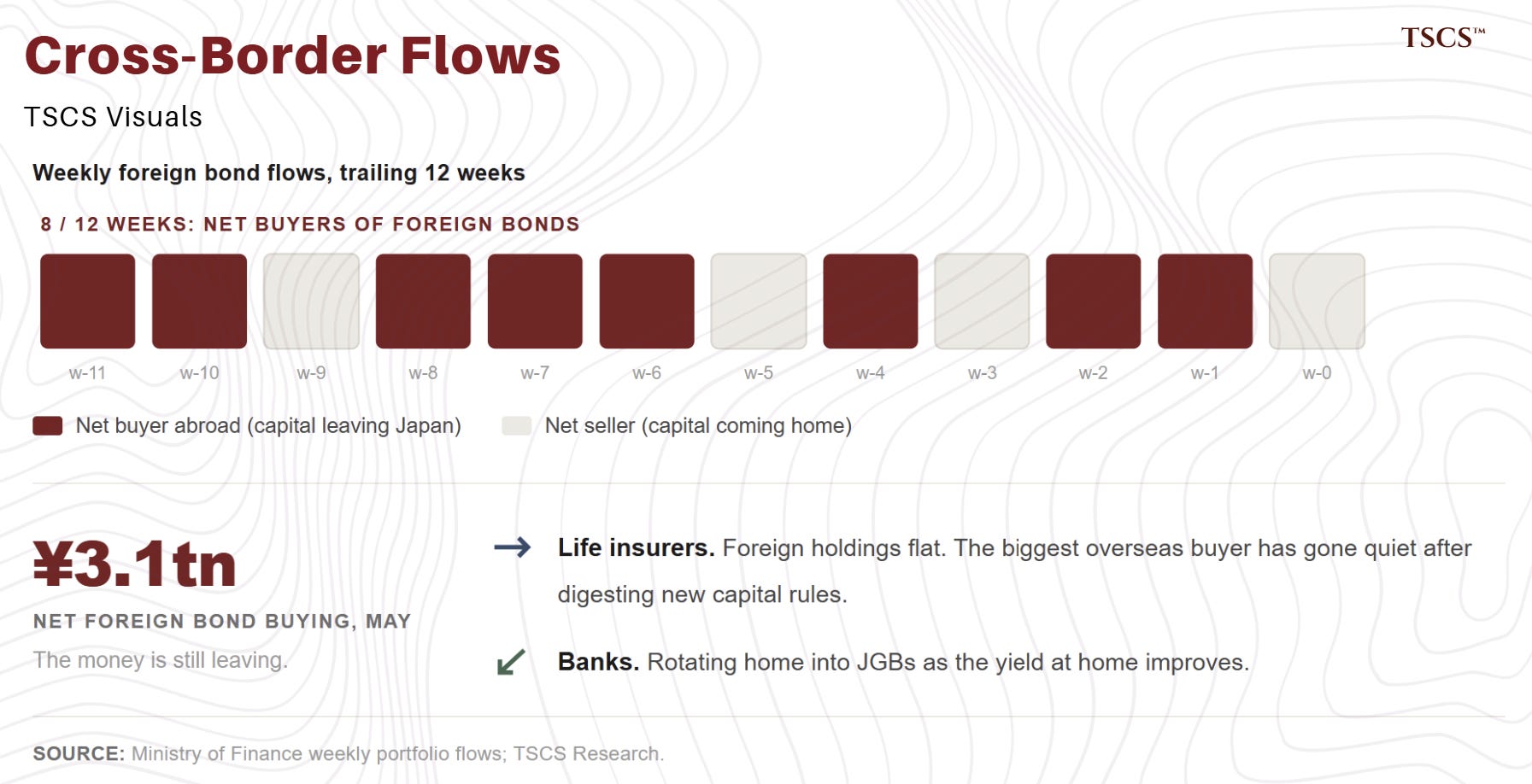

Everyone’s waiting for Japanese money to come flooding home out of foreign bonds.

The Ministry of Finance publishes the flows every week, and Japanese investors have been net buyers of foreign bonds in 8 of the last 12 weeks, 3.1 trillion yen of them in May alone. The money is still leaving.

What’s changed is narrower. The life insurers, who did most of the buying abroad, have stopped adding, they’ve finished adjusting to new capital rules and their foreign holdings have flattened out. The banks are moving cash back into JGBs as the yield at home improves. So the biggest foreign buyer has gone quiet while the country as a whole keeps exporting capital. Nobody is coming home yet.

The war, and the trap it left

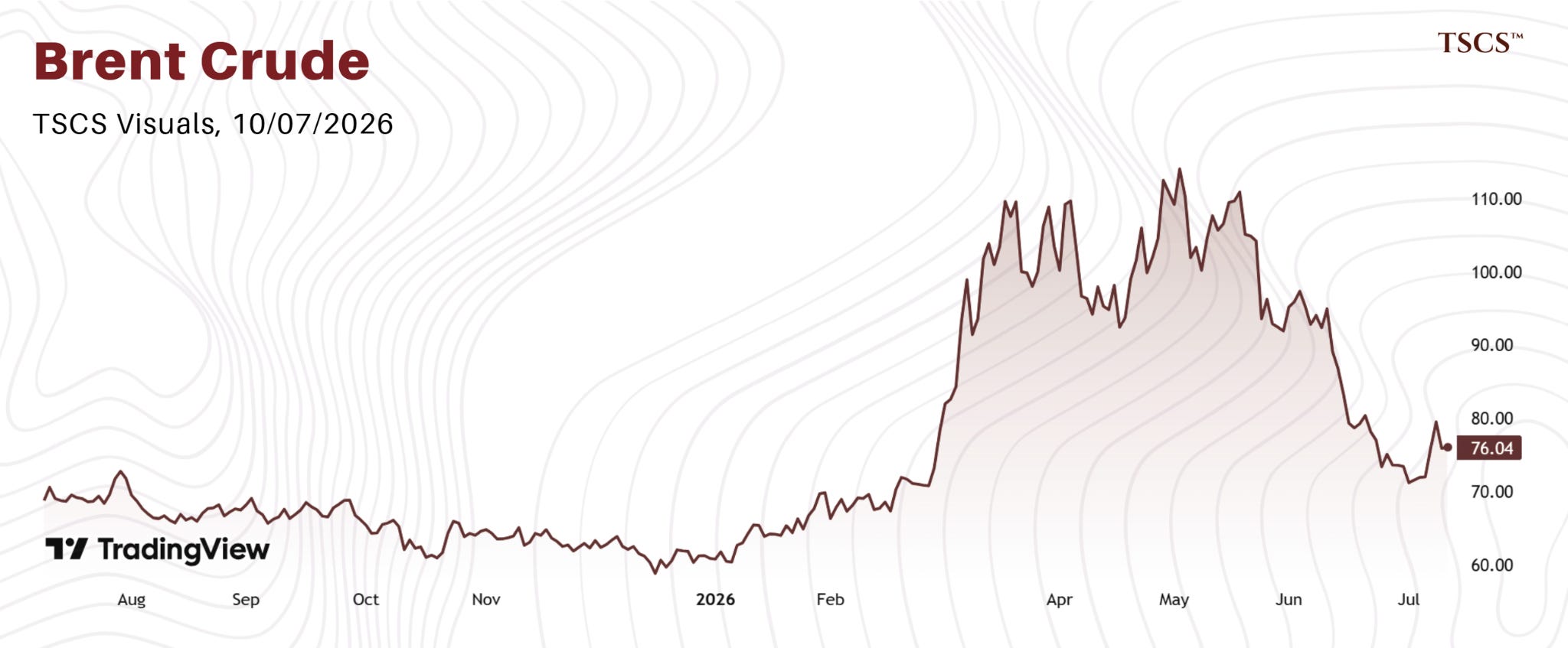

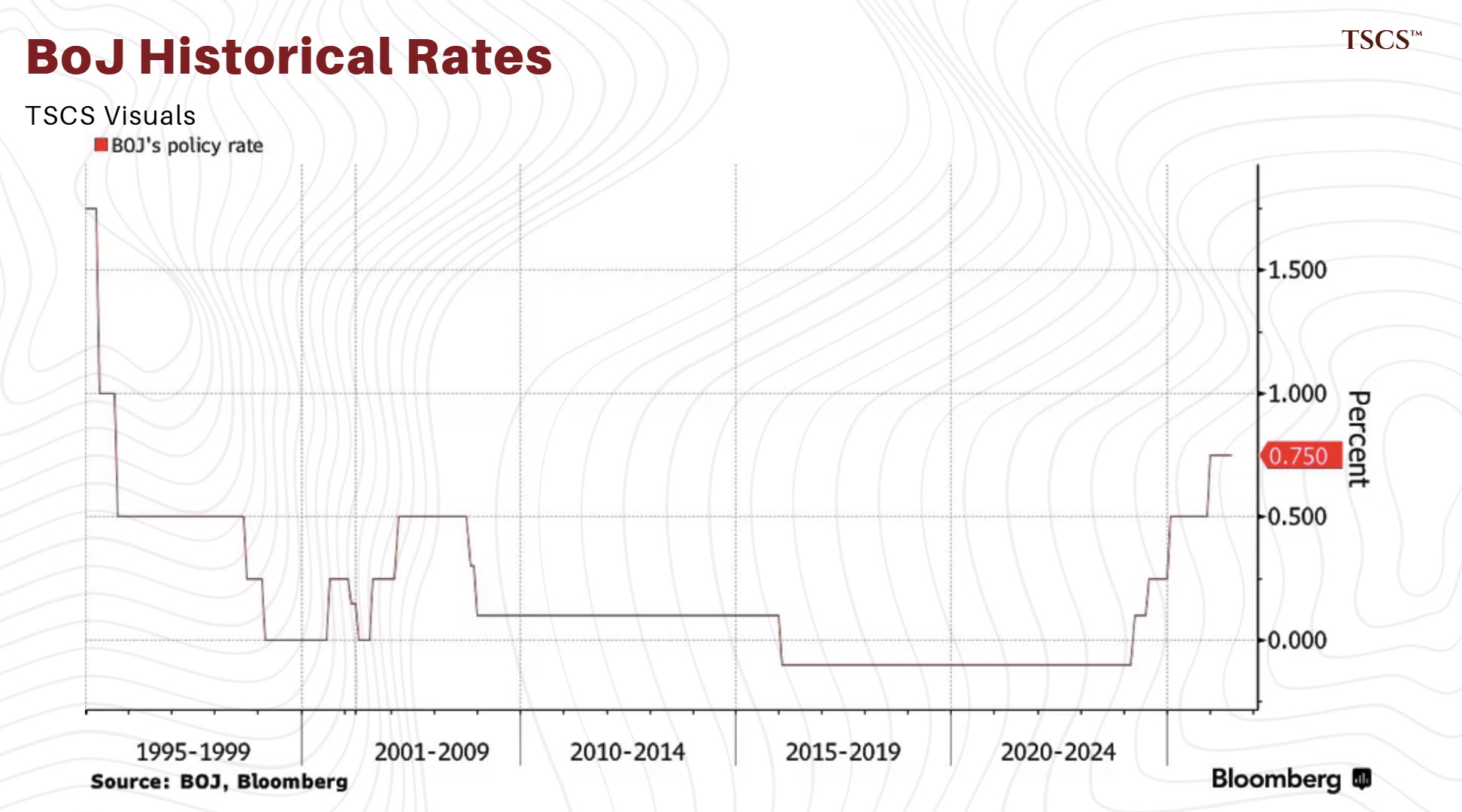

So what pushed the Bank to raise rates? The war between the US and Iran and the closing of Hormuz sent oil to one of its sharpest spikes ever, Brent reached $126 in the spring, into a country that imports nearly all its energy, and a 40 year low yen made every barrel worse. That was the inflation the Bank pointed at when it took rates to a 31 year high in June.

Since then, the ceasefire is coming apart, Iran has hit tankers in the strait again, the US has struck back and pulled Iran’s oil waiver, Trump has declared the interim deal over, and traffic through Hormuz has effectively stopped again.

Crude jumped on the strikes and then went strangely quiet, Brent near $76 as I write, because the market is betting the talks still running in the background will hold. Maybe they will.

But inventories are draining while the strait sits mostly shut, so the pressure builds under the calm. The near term risk for Japan has flipped. Oil going back up would wipe out the disinflation, spring the trap on real wages, and force the BoJ to keep hiking.

The weak yen has not gone anywhere, though.

Real wages in Japan have been positive every month this year through May, 1-2%, the first decent run in years. Pay finally rose faster than prices (wages ~3%, inflation ~1.5%).

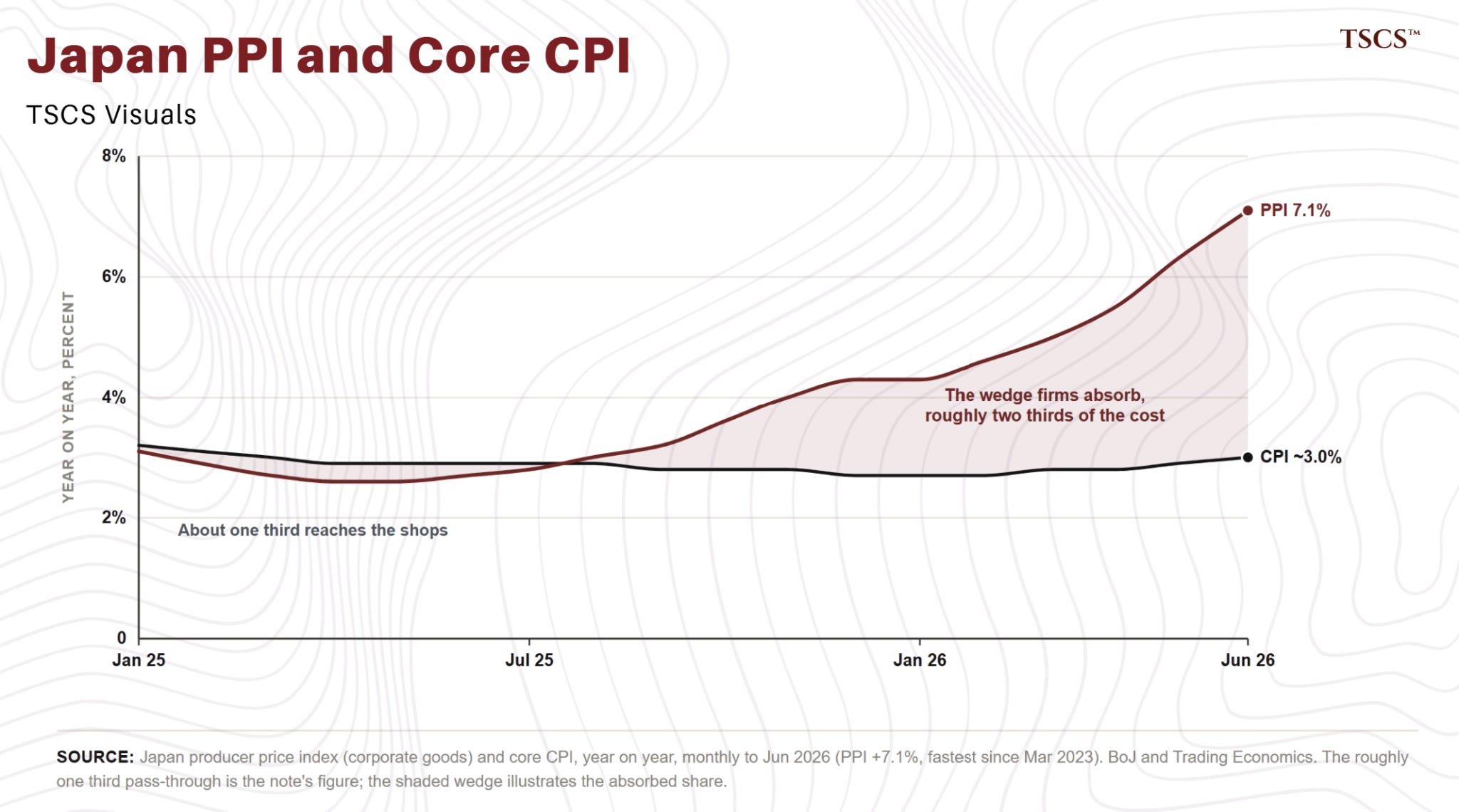

Then why did prices stay down? The Bank’s own import figures show energy costs going from -14% in January to +47% in May, food 6% to 8%. Wholesale prices for June rose 7.1%, the fastest in over 3 years.

So if cost inflation reaches the end consumer, or the yen falls further, the real wage gain in Japan will turn negative again. That’s the trap.

They need the yen to stop falling to protect the one good thing that has happened, and they cannot raise rates fast enough to lift it without paying the reserve bill from the first half of this piece.

What everyone does now

Every player here is doing the only sensible thing their position allows, and the positions are as much about history and habit as about money.

The Bank raises rates slowly and protects the credibility it spent 25 years building. It won’t step in to hold long term rates down, because doing that means buying huge amounts of long bonds, which is money printing in the open and would sink the yen. BoJ got hurt raising rates too early in 2000 and 2006, so caution is wired in. It absorbs the losses and leaves the currency to the Ministry of Finance.

The Ministry leans against the yen to slow it down rather than to defend a line. It has spent close to 12 trillion yen since April, about $73 billion, doing that, and the yen sits near 162 anyway. The finance minister, Katayama, has hinted she might stop announcing intervention in advance to catch the shorts off guard, an admission the old playbook is wearing thin.

Its biggest weapon, about 1.1 trillion dollars of US Treasuries, is also its most awkward, because selling them to buy yen pushes up American interest rates, which Washington doesn’t want, so any intervention happens with a quiet nod from Washington. Yamasaki, who used to run this desk, said they are past warnings now, and on his math the yen is 20% too cheap.

Takaichi is the contradiction at the center. She is an Abe protege who spent her career wanting a weak yen, and she now runs a country where the weak yen and its inflation are exactly why people are angry, which is why she has a supermajority. So she spends, she suspended the food tax and launched a 370 trillion yen investment plan, all while talking about discipline, and she swallows the rate hikes she used to oppose because they are the only thing slowing the currency she helped weaken.

Her mandate lets her spend, her mentor’s ghost tells her to, and the weak yen that was the whole point of Abenomics is now her biggest problem.

The banks are the winners, a steeper curve and positive rates widen their margins, and they are buying JGBs again as the yield improves. The insurers stay cautious on the very long bonds under their new rules. The fast money is crowded into the biggest yen short in 20 years, smart on its own and dangerous all together.

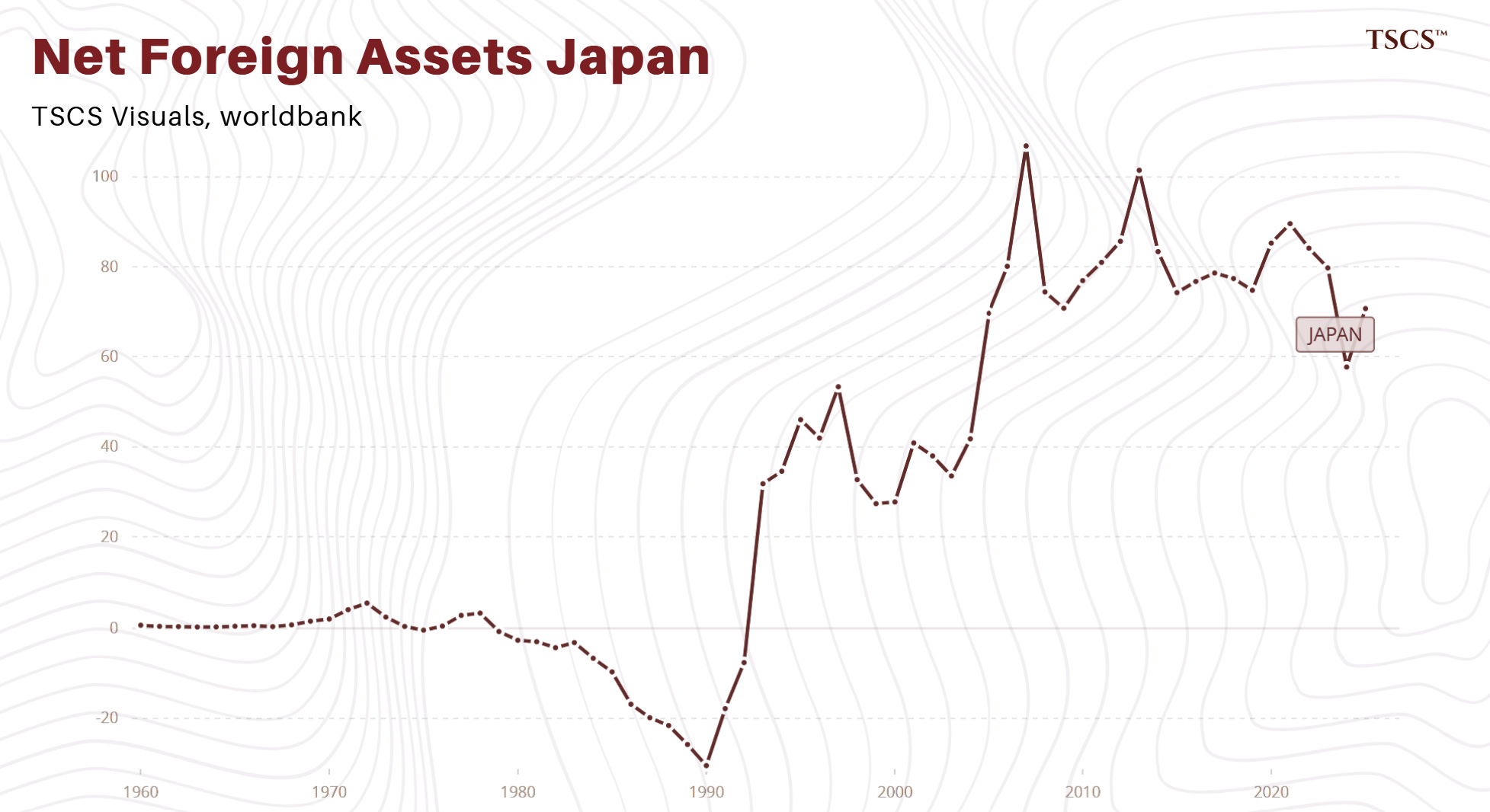

Washington wants a stable yen, because a collapsing yen means a strong dollar and Japanese selling into an already heavy Treasury market, so it tolerates the intervention. And every other heavily indebted government should watch Japan closely, because Japan can print without instant punishment only because it is the world’s biggest creditor, $3.7 trillion of net foreign assets, with a long history of deflation. Britain found out in 2022 how fast that goes wrong when a country that lives on foreign money tries the same.

Why it’s your problem

The tempting story is that Japan is the fuse for a global blowup. That’s too much. The world’s long term interest rates have been climbing mostly for American reasons, a 6% deficit and a rising risk premium, with the loss of America’s last triple A rating a trigger, and the narrowing gap between US and Japanese rates can come as much from American rates falling as Japanese rates rising.

Japan did not cause this. It was one of the beams holding the thing up, and it is being pulled out. For 15 years the automatic bid from a zero rate Japan, and the carry trade it paid for, and the carry trade it paid for, Morgan Stanley put the stock near $500 billion at its peak, held long term rates down everywhere and financed risk. Take that away and the same pile of new debt has to clear at a higher yield.

The bigger point is that Japan is an example of what happens when you hold debt in your own currency. Take notes America.

Where I might be wrong

The best argument against me isn’t the doom crowd, it’s Bill Fleckenstein. For a year he has told anyone who asks that the repatriation and contagion story is overblown, that it’s not a systemic event, that all it really shows is too much debt in both Japan and America. He has been right for that year while the people calling for global liquidation have been wrong. He even thinks higher Japanese rates should lift the yen, not sink it. On his question, is this a crisis, he is right, and I am not arguing with him.

But we are answering different questions. His is whether this blows up. Mine is whether it costs. A central bank losing money on its own bonds is a cost. A currency at a 40 year low while rate gaps close is a cost. Real wages that just turned positive and sit one oil spike from turning back are a cost. Fleckenstein walks right up to that and even opens the door, granting there is too much debt. I’m walking through it. I’m not disagreeing with the smartest skeptic in the room.

Crisis no, cost yes isn’t heresy, it’s close to official doctrine, the Bank itself, the BIS and the IMF all say losses don’t stop a central bank operating and that the cost is fiscal.

What none of them do is put the number on the table and follow it into the currency and the curve, which is the job here. And I’m not the first to circle the number either. Kenzo Yamamoto, a former BOJ executive director, flagged back in 2024 that the trouble starts a little above a 1% deposit rate and that the ETF income was what delayed it. Sayuri Kawamura at the Japan Research Institute warned the Bank was nearing reverse carry and couldn’t lean on ETF income forever. Pictet’s Tokyo desk called the crossover on the bond book outright last year. What I haven’t seen anyone put in print is the clean version, strip out the one off gains and the Bank is already underwater at 1%, so read this as assembly as much as discovery, and credit where it’s owed.

And his disagreement hands you something for free. He and the three hundred crowd are both sharp, both certain, and on opposite sides of the yen. When people that good split that hard on direction, you do not want to own a direction. You want to own volatility.

The base case is a slow grind, so reading this as a crash call is incorrect. The money is still leaving Japan, so the outflow could keep the yen weak far longer than any of this implies, or it could snap home in a rush on the risk Aberdeen flags, where losses on long bonds under the new insurer rules force selling that feeds on itself, the way Britain’s pension funds unraveled in 2022.

I checked the two soft spots in the reserve math against the Bank’s own accounts and both held, the dividend cushion is real and mostly recurring, and the old system where the Bank paid its policy rate on only part of its reserves was scrapped in 2024, so there is no hidden discount softening the bill. But there does exist a hole, it assumes the weak yen reaches the shops, and Japanese firms have been passing on only about 1/3 of their higher costs and eating the rest, so prices may rise less than the mechanism says and the squeeze on wages may be gentler (but ask yourself how long can they eat these costs for). And a turn in the yen is muddy, because with the short this crowded a bounce could be a squeeze that fades. None of this is a default.

The trade

Analysis that never turns into a position is just talk. Let me present you some idea generation.

Let’s first eliminate these awful crowded trades, and yes I know I say that as someone who opened this piece getting carried out of one. The curve steepener has been the consensus play for two years, the 30 year is already at 4%, the very long end is already stretched, and the Ministry is shortening what it issues to flatten your bet, while the Bank still buys around 2.5 trillion of bonds a month and reserves the right to buy more if the long end moves too fast. You would be paying to sit in a crowd while the government works against you.

The plain short yen is worse, the most crowded short in 20 years. Both are the trade that looks obvious, which around here is the trade that hurts you.

The better trade is hiding in the options.

Keep reading with a 7-day free trial

Subscribe to TSCS to keep reading this post and get 7 days of free access to the full post archives.