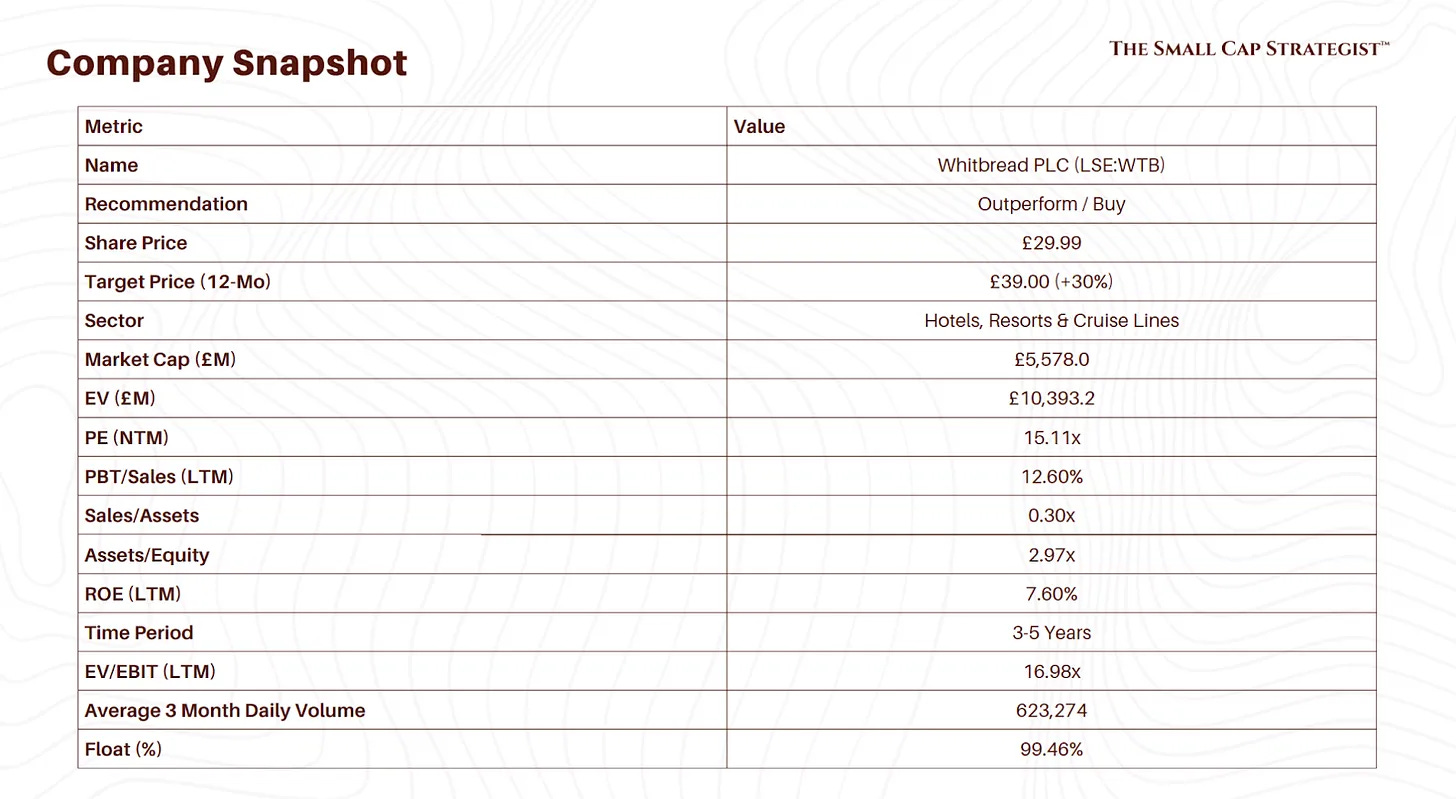

Whitbread PLC - Overview & Highlights

5B Property Margin of Safety, A "Free" Operating Business, With A £250M Share Buyback.

Investment Thesis

Accelerating Growth Plan (AGP): Unlocking value by converting 100+ low-return restaurants into 3,500 high-margin hotel rooms, adding £100M+ incremental Profit Before Tax (PBT) by FY30.

Germany Profitability: The German operation is set to turn profitable in FY26, forcing a market re-appraisal of this hidden growth asset.

Capital Returns: A clear policy of shareholder returns, including a new £250M buyback for FY26, provides a tangible cash return and signals management confidence.

Valuation & Margin of Safety

The stock is deeply undervalued on a sum-of-the-parts (SOTP) basis. The analysis shows the market is valuing the entire global operating business at just £1.06bn, or 1.58x Last Twelve Months (LTM) Earnings Before Interest and Taxes (EBIT). Given that a private market transaction implies the German business alone is worth ~£1.09bn, investors are effectively getting the dominant, cash-generative UK business for free. This provides an extraordinary margin of safety. The author's price target is £39.00 (+30% upside).

Key Risks

A prolonged or deep UK recession depressing consumer and business travel.

Execution risk in Germany (failing to achieve brand resonance or manage operational complexity).

Intense competition from global hotel chains (Accor, IHG), domestic rivals (Travelodge), and disruptive models (Airbnb).

Reverse Thesis (The Short Case)

Property Overvaluation: A severe UK commercial real estate downturn could impair the value of the freehold portfolio, eroding the margin of safety.

Germany is a "Value Trap": The German expansion could fail to achieve profitability and scale targets, becoming a capital sinkhole that destroys value rather than creates it.

UK Business in Secular Decline: The current trading weakness is not a cyclical blip but the start of a structural decline due to permanent shifts in travel (e.g., post-COVID habits) or a superior competitive threat (e.g., Airbnb), meaning the UK operating business is worth very little.

Company & Competitive Analysis

Analysis of Competitive Advantage

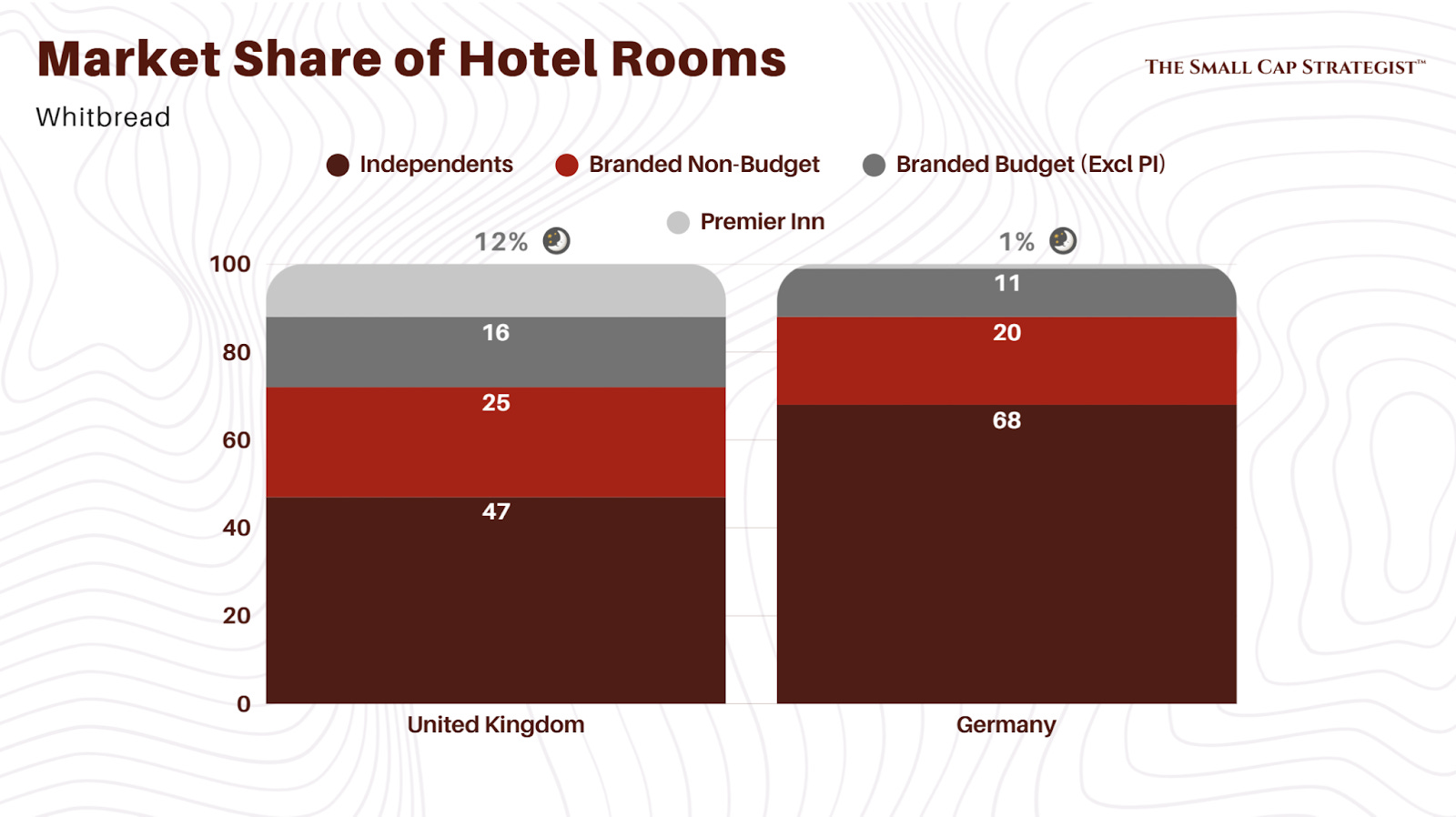

Market Position: Dominant UK market leader with a 12% share. The market is fragmented, so this position provides significant scale advantages. Market share is increasing as weaker independent hotels exit the market. In Germany, Whitbread is aggressively expanding to become a leading player in another fragmented market.

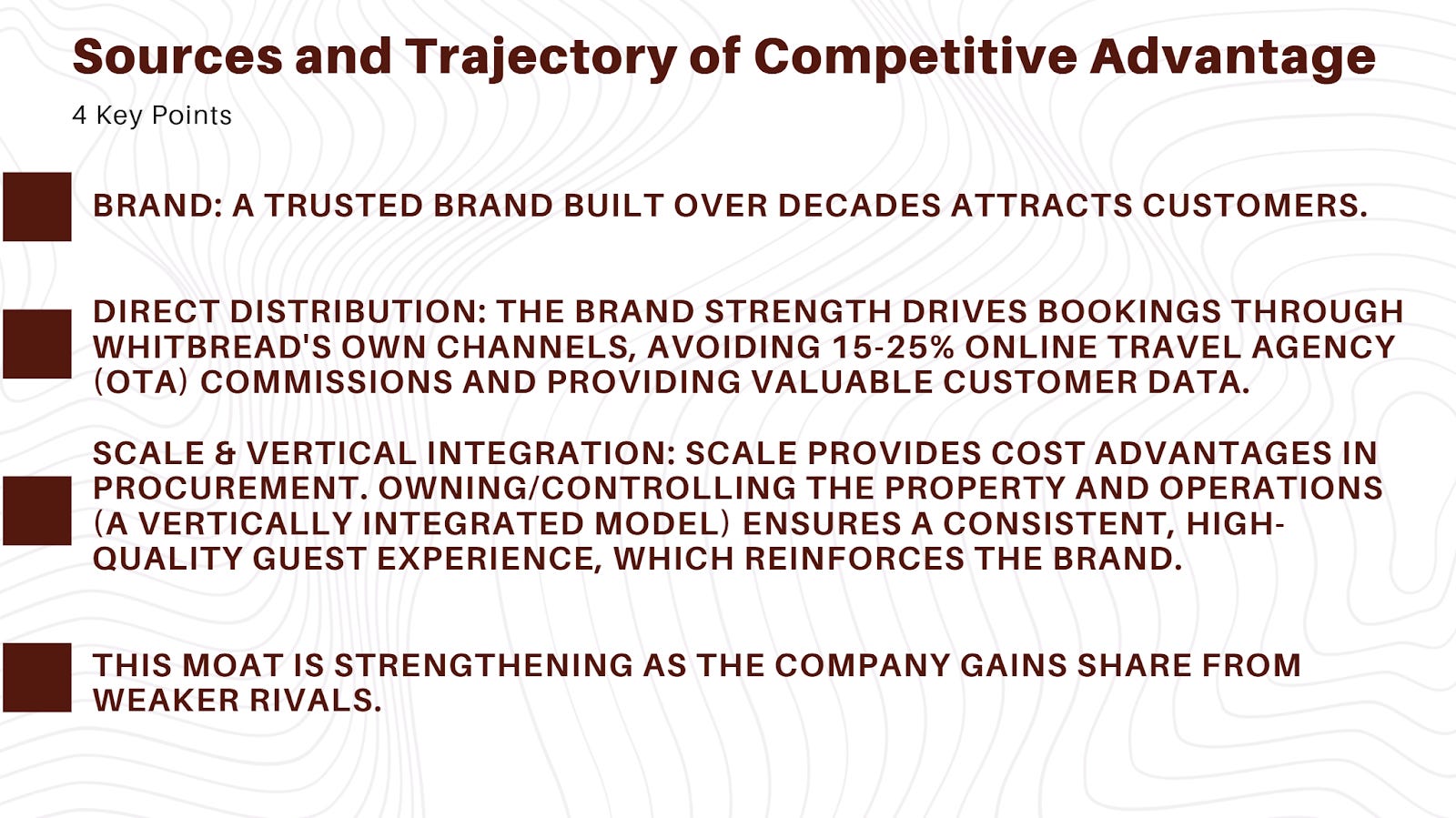

Product Differentiation: The Premier Inn brand is a powerful intangible asset, synonymous with trust, reliability, quality, and value-for-money. This strong brand positioning reduces customer search costs and drives a high degree of direct, loyal bookings.

Sources and Trajectory of Competitive Advantage: The competitive advantage is wide, durable, and derived from a virtuous cycle:

Evidence of Pricing Power: The company has demonstrated the ability to maintain pricing discipline and high occupancy (81% UK) even in a softer macroeconomic environment, a clear testament to the strength of its brand and value proposition.

Evaluation of Business Franchise / “Economic Moat”: The economic moat is wide and durable. It is built on the self-reinforcing loop of brand trust, direct distribution, and operational control. The asset-heavy model, often viewed as a negative, is the key enabler of the quality control that underpins the brand's promise, making the moat difficult for asset-light competitors to replicate.

Key Competitors

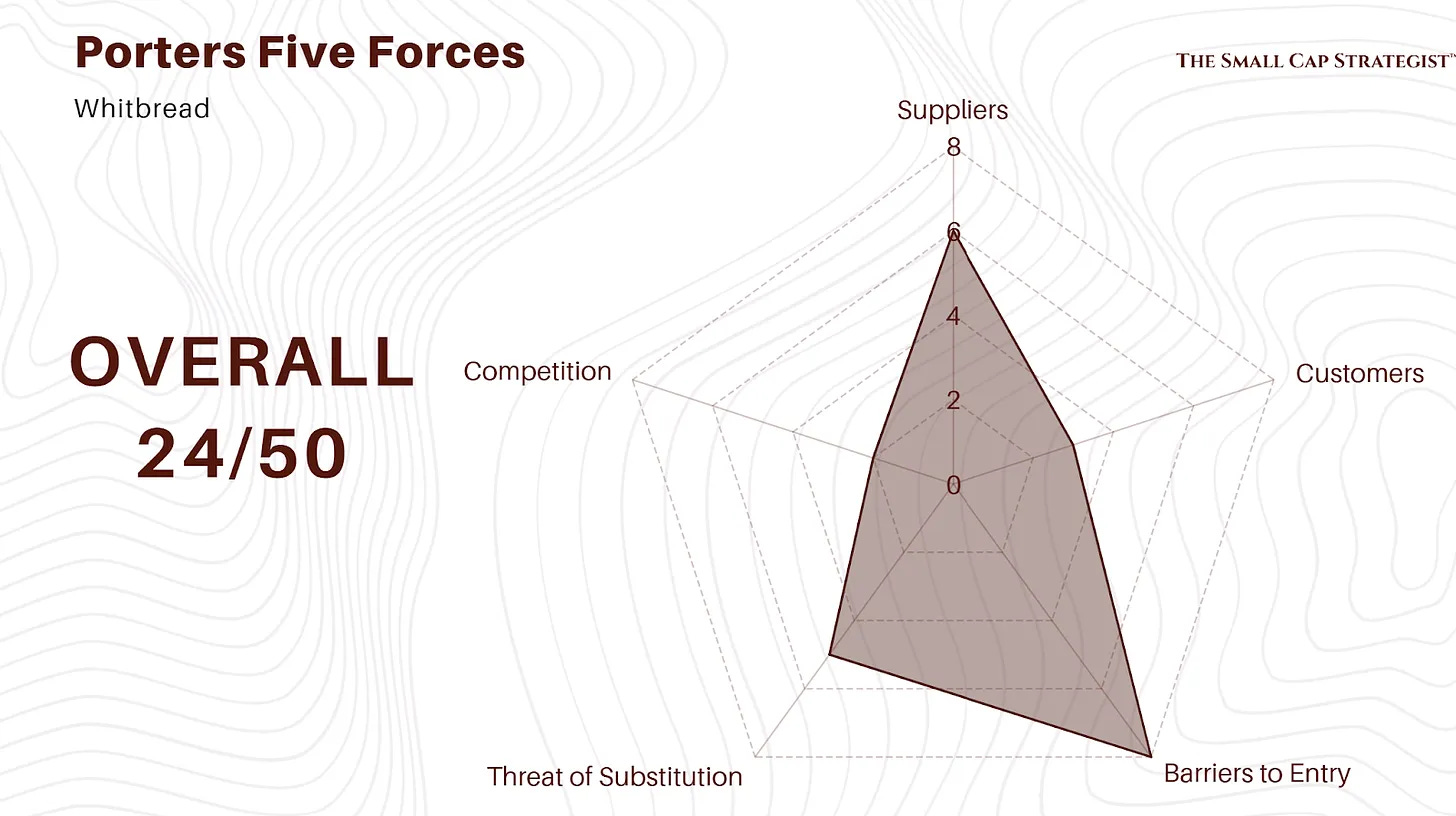

Industry Analysis: Porter’s Five Forces (Overall Score: 24/50)

The budget hotel industry is structurally challenging. Profitability is constantly under pressure from intense rivalry and powerful customers. Sustainable success is therefore contingent on building a durable competitive advantage.

Supplier Power (Score: 6/10): Low to Moderate Power. Key inputs are property, which can be competitive, and labor, which is subject to wage inflation. However, Whitbread’s scale provides significant bargaining power over other suppliers (e.g., food, linens, technology), mitigating cost pressures.

Customer Power (Score: 3/10): High Power. For the end consumer, switching costs are effectively zero. The rise of online booking platforms has created immense price transparency, giving customers significant power to compare options and drive down prices.

Barriers to Entry and Exit (Score: 8/10): High Barriers to Entry. The capital required to build a national hotel network of meaningful scale is immense. Furthermore, building brand recognition and trust on the level of Premier Inn is a multi-decade, multi-billion pound endeavor, creating a formidable barrier for new entrants.

Threat of Substitution (Score: 5/10): Moderate to High Threat. The primary substitute is the private rental market, epitomized by Airbnb, which offers a different value proposition. However, for the core business and short-stay leisure traveler seeking consistency, reliability, and predictability, the branded budget hotel model remains a distinct and preferred choice.

Competitive Intensity of Industry (Score: 2/10): Very High Rivalry. The industry is intensely competitive, featuring global giants, strong domestic peers, and a fragmented base of independent operators all competing fiercely on price and location.

Financial and Operational Deep Dive

Revenue Trends

A strong "V-shaped" recovery post-pandemic. Near-term (FY25) revenue shows a slight dip due to UK softness and planned Food & Beverage (F&B) restructuring. A return to growth is expected from FY26, driven by network expansion in both the UK (AGP) and Germany.

Volume: Robust underlying volumes, with UK occupancy at 81%. Room count is growing organically through the AGP and the German rollout.

Pricing: Average Room Rate (ARR) has held firm, demonstrating pricing power and the brand's strong value proposition.

Mix: The revenue mix is strategically shifting towards higher-margin accommodation and away from lower-return F&B revenue as part of the AGP.

Cost Structure, Margins & Returns on Capital

The business has high operating leverage due to a significant fixed cost base (property, staff). Management has a strong focus on efficiency, targeting £60M in savings for FY26. EBITDA margins are strong (28.6% in FY25) and projected to expand significantly to over 36% by FY27, driven by the shift to higher-margin rooms and German profitability.

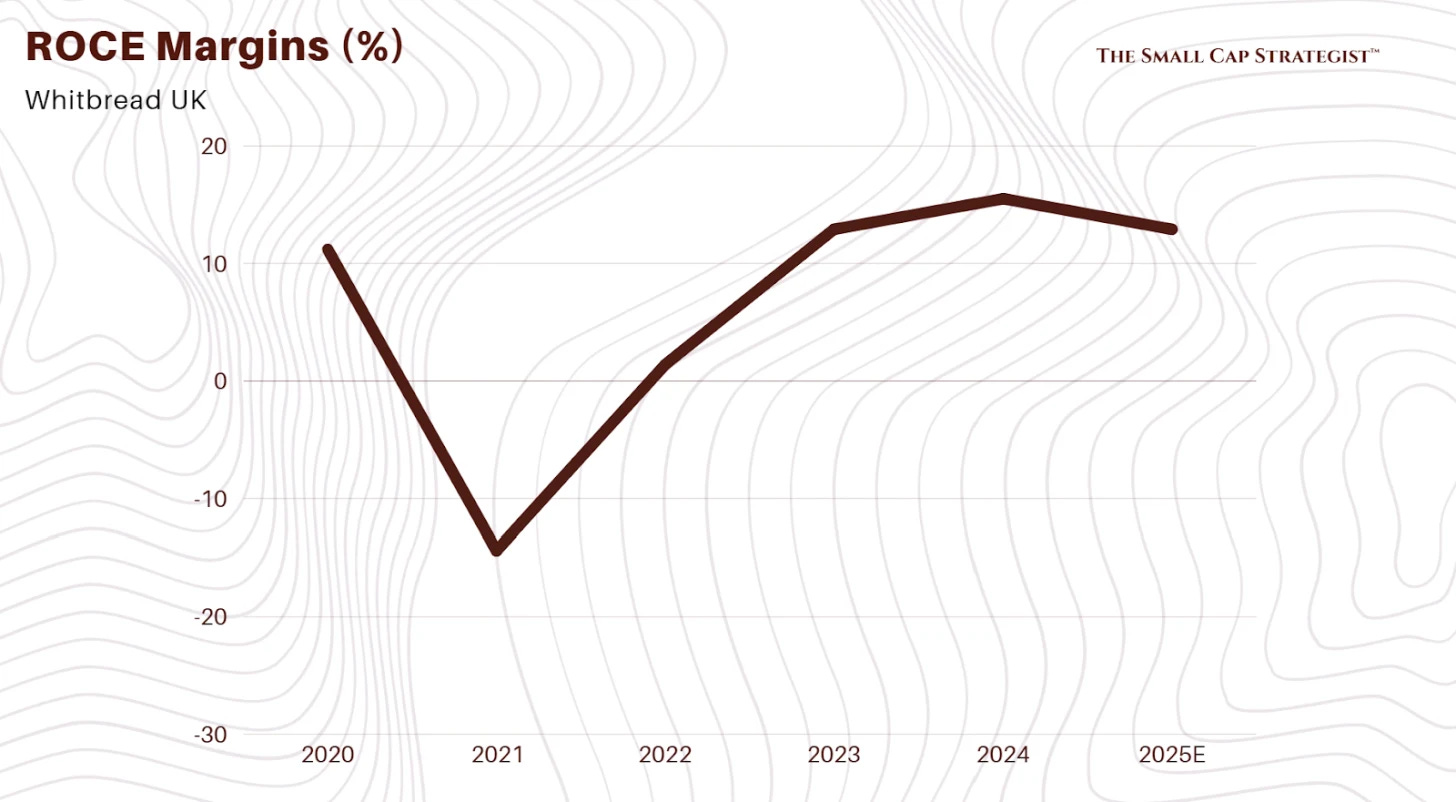

Returns on Capital: Return on Capital Employed (ROCE) is a key metric. UK ROCE was 12.9% in FY25. While down from a post-COVID peak, it remains above the historic average. The core strategy (AGP) is explicitly designed to improve ROCE to a target of 15% by recycling capital from low-return restaurant assets into high-return hotel rooms.

Capital Allocation

Management has a proven and astute approach to capital allocation. The 2018 sale of Costa Coffee for £3.9bn and subsequent £2.5bn return to shareholders is a prime example. The current framework prioritizes reinvestment in high-return growth (Germany, AGP) while returning all surplus cash to shareholders. A new £250M buyback is planned for FY26, supporting a 3.23% dividend yield.

Balance Sheet & Cash Flow Considerations

Balance Sheet: The key feature is the vast freehold property portfolio, valued at ~£5 billion. This provides immense balance sheet strength, strategic flexibility, and a hard asset backing for the valuation. The company operates with a net cash position (ex-leases).

Cash Flow: The business model is capital intensive due to property ownership and expansion plans. Major uses of cash are capex for the German rollout and the UK Accelerated Growth Plan. This investment is funded by strong operating cash flow from the mature UK business and capital recycling from the sale of non-core assets.

Management & Corporate Information

Management

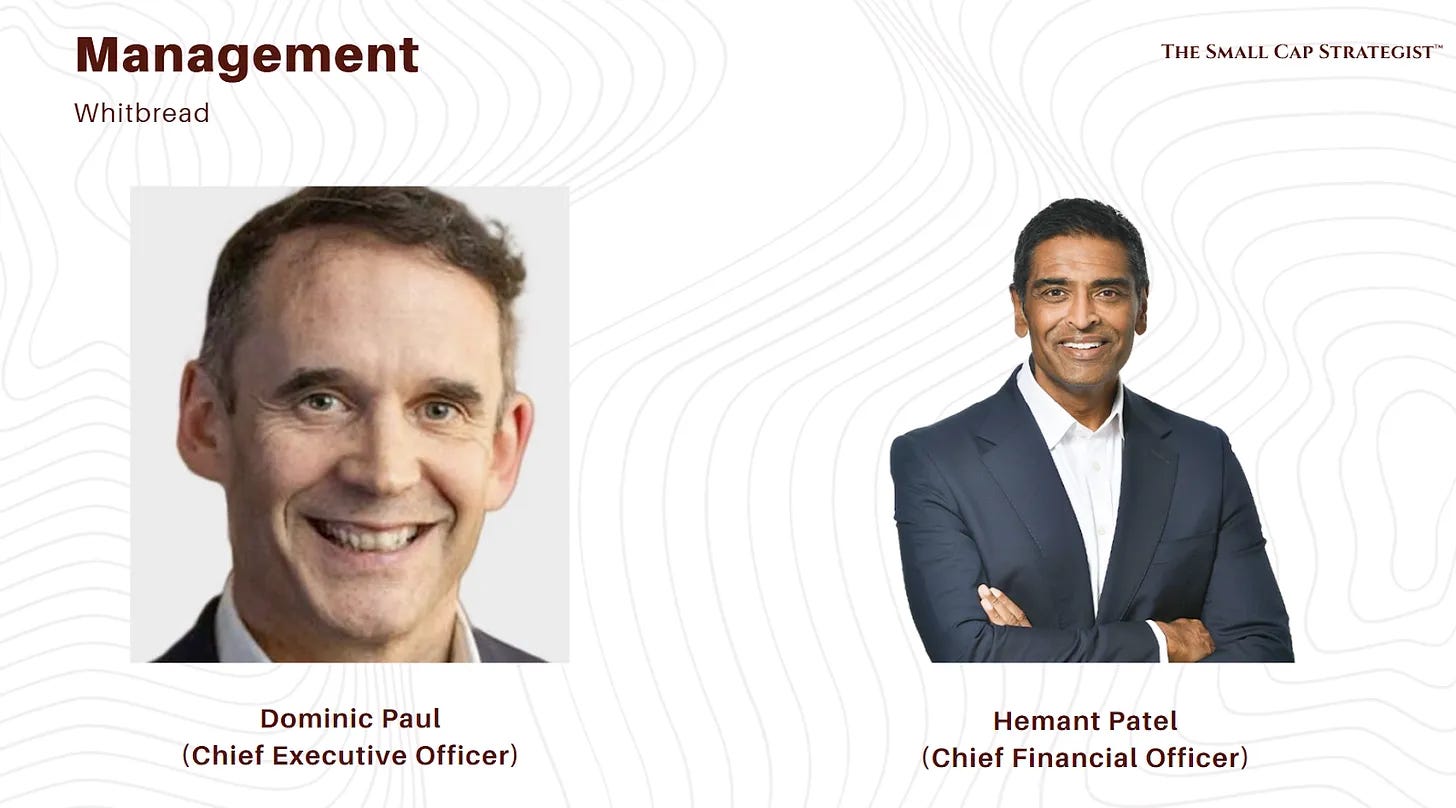

CEO: Dominic Paul (appointed Jan 2023). Brings highly relevant experience as former CEO of Domino’s Pizza Group and MD of Costa Coffee, demonstrating expertise in managing large, brand-driven consumer businesses.

CFO: Hemant Patel (appointed Mar 2022). Has a background in UK leisure and retail with senior finance roles at Greene King and ASDA-Walmart, ensuring financial discipline.

Board: Insider ownership is low at 0.40%, but incentives are aligned via performance-based pay.

Share Ownership & Coverage

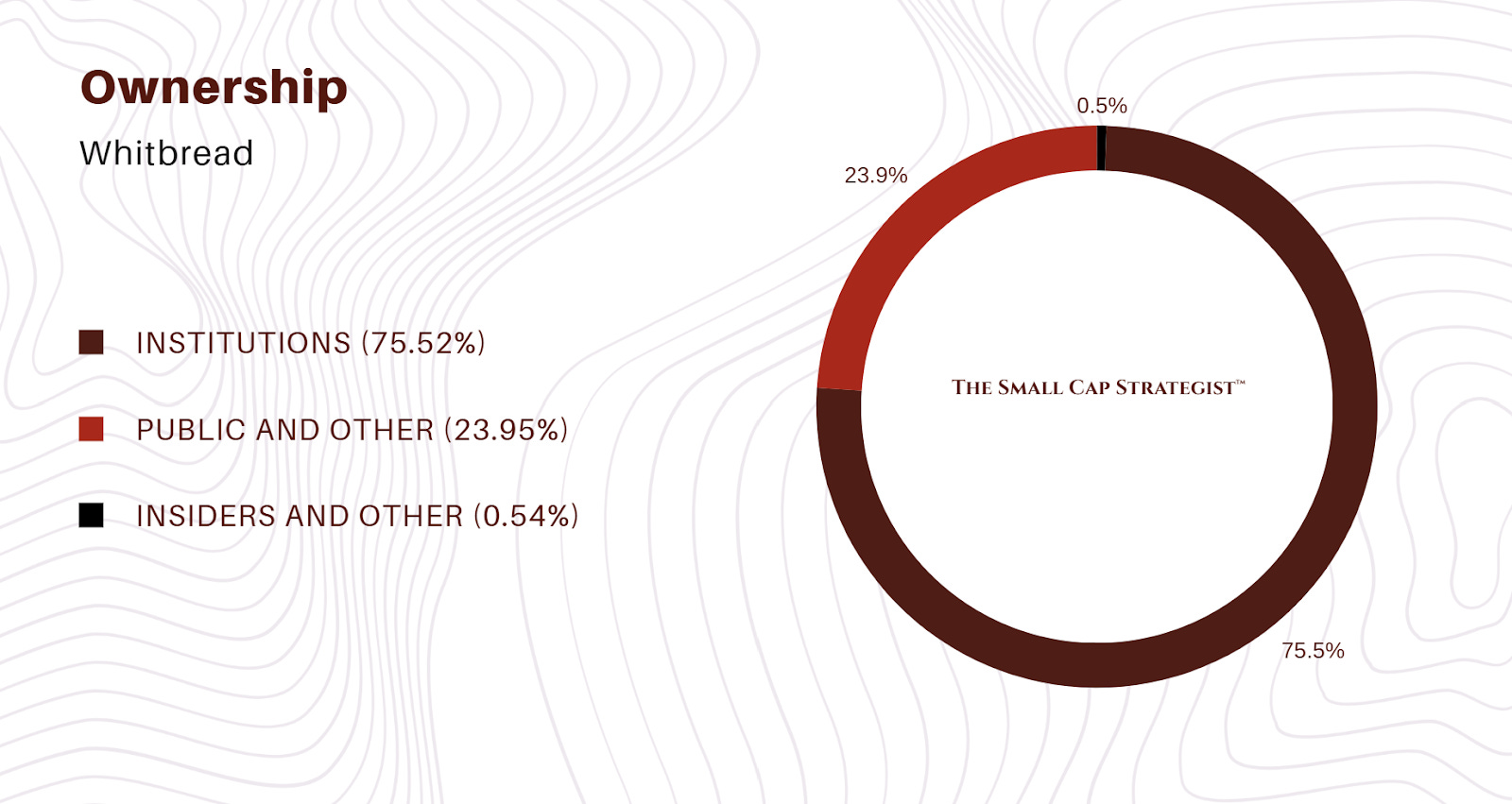

Share Ownership Structure: High institutional ownership at 75.52% indicates significant conviction from sophisticated professional investors.

Broker / Analyst Coverage: The author's recommendation is "Outperform / Buy".

Context & History

Industry Overview: The budget/midscale hotel sector is cyclical and highly competitive. The industry structure is characterized by a few large, branded chains and a long, fragmented tail of independent operators. A key secular trend is the consolidation of the market as these under-capitalised independents are squeezed out, creating a growth opportunity for scaled players like Whitbread.

Operational Overview: Operations are split into two key geographical segments:

UK & Ireland (Core): A mature, highly cash-generative business focused on optimization and enhancing returns via the Accelerated Growth Plan (AGP).

Germany (Growth): A rapidly scaling business aimed at replicating the UK's success in Europe's largest economy. It is on the cusp of profitability.

Ancillary F&B operations are being restructured to support the core accommodation business.

Relevant Company History: The 2018 divestment of the Costa Coffee division to Coca-Cola for £3.9 billion was a landmark transaction that crystallized significant value for shareholders and demonstrated management's capital allocation acumen.

If you enjoyed this post, consider becoming a paid or free subscriber to The Small Cap Strategist.

Disclaimer: This post is for informational and educational purposes only and should not be considered investment advice. The author is not a financial advisor. All investment decisions carry risk, and readers should consult with a qualified financial professional before making any investment choices. The author may or may not hold positions in the securities discussed. This post may not be an accurate reflection of Whitbread PLC or its related companies. Read the full disclaimer in the ‘About Me’ section.

Impressive breakdown. The AGP strategy and the German segment’s path to profitability make the valuation gap hard to ignore.

Your content is gold, keep it coming!