Bitcoin is Built to Fail.

BTC's scarcity is its weakness: An investor's look at why the mathematical certainty of scarcity is its greatest economic weakness.

“I can calculate the motion of heavenly bodies, but not the madness of men.”

- Sir Isaac Newton

There’s far more than meets the eye when it comes to our beloved Bitcoin.

Over time we had built a view of Bitcoin’s scarcity that was, quite frankly, wrong. We had accepted the simple, elegant narrative that has become the bedrock of the entire crypto movement: a fixed supply of 21 million coins makes Bitcoin a pristine, incorruptible store of value, the perfect antidote to the profligate money-printing of central banks.

It’s "digital gold," a safe harbor in a world of fiat debasement.

Instead of making you go through the hundred pages of academic papers, financial reports, and expert interviews we’ve gone through in prep for today, we put all the good stuff into this post.

Our curiosity was sparked by a deep, challenging analysis from Du Charme Wealth Management and CFA Mike Green, whose work forced us to question the very foundation of the "digital gold" narrative.

Their arguments sent us digging, and the more we dug, the more the entire scarcity thesis began to unravel.

This post covers everything you need to know about why Bitcoin’s absolute, programmatic scarcity is not its greatest strength, but a catastrophic, system-level flaw. It’s split into a few main sections:

An executive summary,

a deconstruction of the digital gold myth,

the dire consequences of a deflationary system,

the fragile mechanics behind Bitcoin’s price,

the dangerous new layer of financial engineering being built on top of it.

Today, we’ll clear the misconceptions around digital scarcity and move one step closer to becoming objective, clear-thinking investors.

If you want to build a portfolio of unique, high-conviction ideas and gain an edge by understanding the powerful forces shaping global markets, subscribe to The Small Cap Strategist and join a community of discerning investors.

We have already done over 12 company deep-dives, and half a dozen sector researches using institutional quality research. Today we’re looking at Bitcoin.

Executive Summary (The TL;DR)

For those in need of a quick takeaway, here’s the core of the argument:

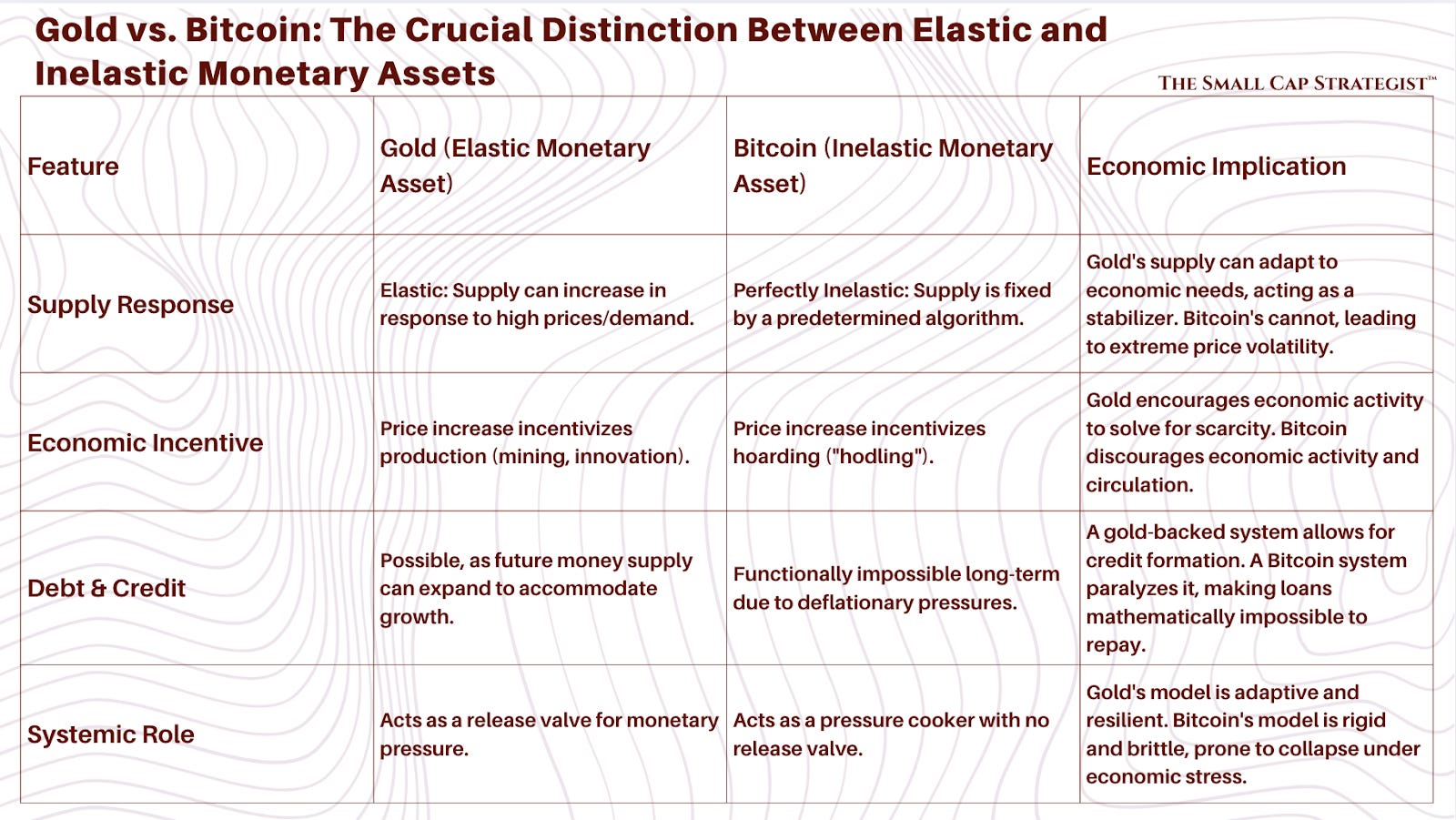

The "Digital Gold" Analogy is Fatally Flawed. The comparison to gold is the most powerful and most misleading narrative in crypto. Gold’s supply is elastic; when it becomes too scarce and its price rises, society is incentivized to produce more of it, acting as a crucial economic pressure-release valve. Bitcoin’s supply is perfectly inelastic. Its rigid, programmatic nature makes it a brittle, not a resilient, monetary system.

Absolute Scarcity Creates a Deflationary Death Spiral. A global economy running on Bitcoin would be trapped in a state of permanent deflation. This sounds great if you already own Bitcoin, but it’s disastrous for a functioning society. It paralyzes credit markets, makes debt mathematically impossible to repay, and systematically transfers wealth from the young and productive to a new aristocracy of early adopters.

Price is a Mechanical Function of Fund Flows, Not Value. Bitcoin’s price action is not a process of fundamental value discovery. It is an almost perfect, mechanical function of new money (like ETF inflows) chasing a fixed number of units. This creates a powerful reflexive loop where inflows drive the price up, which attracts more inflows. This is a classic Ponzi-like dynamic, not a sustainable economic model.

Financial Engineering is Creating "Bitcoin-Squared." A new class of companies, led by Strategy Inc. (formerly MicroStrategy), are issuing billions in real-world debt and equity to buy a non-cash-flowing asset. They are creating leveraged, synthetic exposure to Bitcoin, analogous to the Collateralized Debt Obligations (CDOs) and "CDO-squared" instruments that amplified systemic risk and triggered the 2008 financial crisis. They are a "Ponzi scheme upon a Ponzi scheme".

In short, Bitcoin's most celebrated feature is a bug, not a feature. It is a design principle that makes it fundamentally incompatible with a dynamic, credit-based economy and dangerously fragile as a global store of wealth.

The Digital Gold Myth - Bitcoin is Nothing Like Gold

To understand why the "digital gold" narrative is so misleading, we have to start not with Bitcoin, but with gold itself.

For centuries, we’ve given gold a mystical quality, but at its core, it’s just a shiny, dense metal. As Mike Green explains, gold is simply periodic element number 79 on the periodic table. Its adoption as money wasn't magical; it was practical. It's chemically stable, easily divisible, and (most importantly) its density and elemental nature made it a fantastic anti-counterfeiting tool.

You could weigh a coin and know you weren't being cheated.

But the most crucial property of gold, the one that makes it a viable (though imperfect) monetary anchor, is the very thing Bitcoin was designed to eliminate: its supply is elastic.

The Bitcoin faithful love to remind us that you “can’t print more BTC.” Yet as we watched new crypto millionaires high-five each other, we couldn’t shake the parallels to other financial manias – from gold rushes to mortgage CDOs – where scarcity drove euphoria right up until reality hit.

The Critical Difference: Elastic vs. Inelastic Supply

This is the single most important concept to grasp.

If a society operates on a gold standard and money becomes too scarce, meaning the price of gold rises relative to everything else, a powerful economic signal is sent.

That high price creates a massive incentive for society to devote its resources to making more gold. People rush to mine it, as they did in the 1849 California Gold Rush. Companies invest in new technologies to extract it more efficiently. Scientists might even pursue fusion to create it from other elements like mercury.

This is a vital, self-correcting feedback loop. Scarcity creates a high price, and a high price incentivizes production that alleviates the scarcity. It’s an adaptive system.

Bitcoin, by contrast, is built on the principle of perfect inelasticity. Its code dictates that only 21 million coins will ever exist, released on a predictable, unchangeable schedule. There is no mechanism to respond to the economic needs of society. If the price of Bitcoin goes to $1 million, $10 million, or $100 million, not a single extra coin can be created beyond what the algorithm allows.

It has no feedback loop. It cannot adapt.

Why does scarcity matter? In basic economic terms, a limited supply asset tends to hold its value. Bitcoin’s pioneers and proponents saw the 21-million cap as a way to create “sound money”: an asset that governments cannot debase by printing more.

In the wake of the 2008 financial crisis and subsequent money-printing sprees by central banks, this idea had powerful allure. Bitcoin was portrayed as “digital gold” – a safe store of wealth that would appreciate over time as demand increased against a fixed supply. To believers, each coin is like a plot of digital land: no more can be made, so over the long run it should only become more valuable.

This narrative has been so compelling that by design, Bitcoin’s scarcity isn’t just a feature; it’s the brand. “21 million or bust,” as some hodlers like to say.

What the Bitcoin community hails as a revolutionary feature (the prevention of debasement) is, from a macroeconomic perspective, a catastrophic flaw.

Gold's variable supply is the true feature. It acts as a societal pressure-release valve, allowing the monetary base to expand in response to population growth, technological innovation, and economic need. Bitcoin has no such valve. It’s a pressure cooker with the lid welded shut.

The fundamental disconnect is this: Bitcoin proponents see the ability of governments to expand the money supply as a bug (inflation) and have designed a system to eliminate it.

However, they've thrown the baby out with the bathwater. A flexible money supply is not just a tool for government spending; it is an essential feature for a dynamic, credit-based economy. By creating a system with a perfectly rigid supply, they have designed a monetary system that is inherently brittle and hostile to economic growth.

The table below summarizes this crucial distinction. It moves the discussion from a simplistic comparison of "scarcity" to a more nuanced analysis of how each system responds to economic signals.

Deflationary Death Spiral

If Bitcoin's inelastic supply makes it fundamentally different from gold, what are the real-world consequences of adopting such a system?

The outcome is not a mystery; it is a well-understood economic certainty: a permanent, grinding deflationary spiral that would bring a modern economy to its knees.

In a world where the supply of money is programmatically fixed but the population grows and technology makes us more productive, the value of each unit of money must constantly increase relative to goods, services, and labor.

Everything gets cheaper over time.

While this sounds wonderful to an individual holding the asset, it is poison for a functioning economy for one simple reason: it destroys credit.

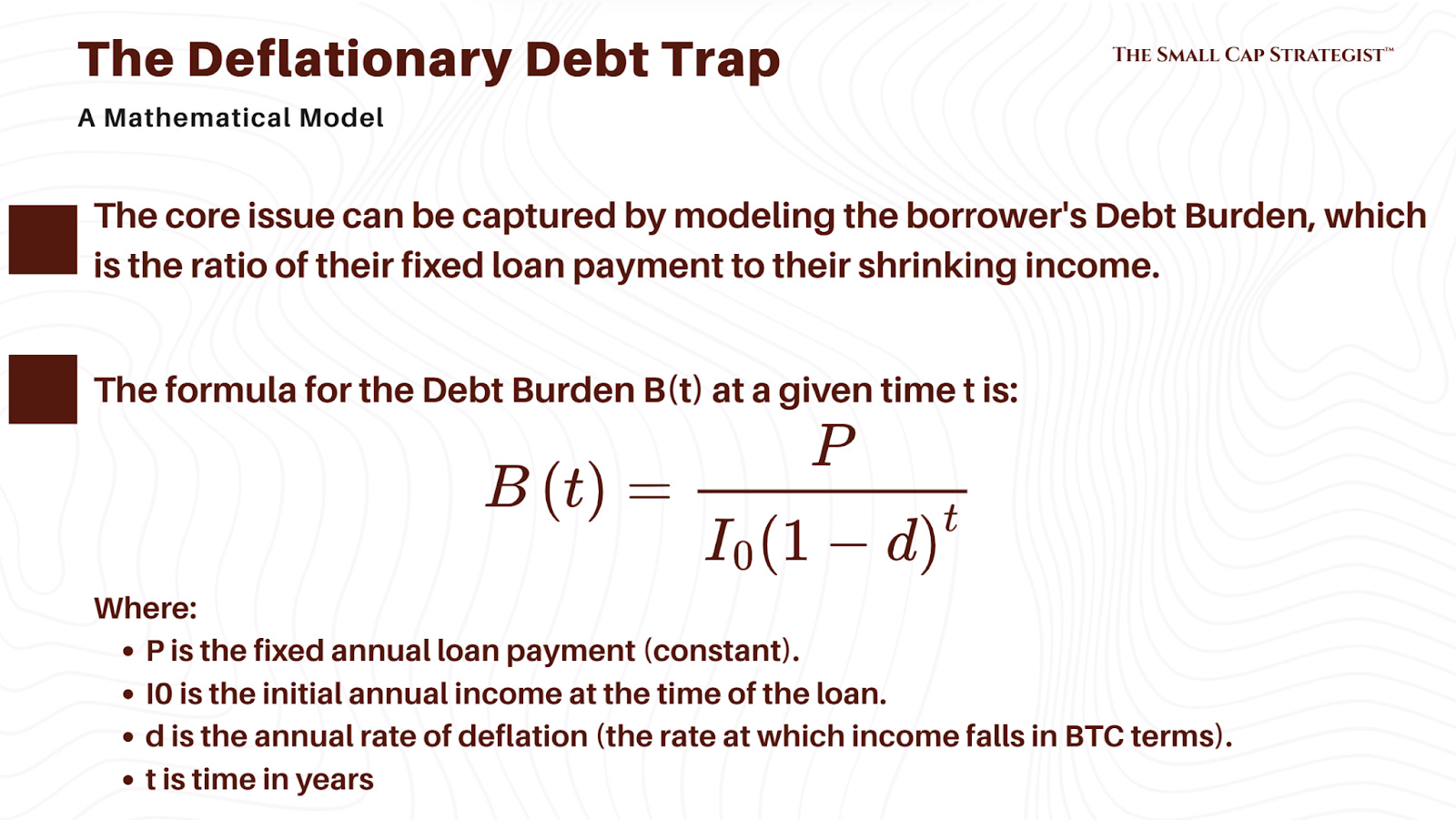

The Paralysis of Credit

Credit is the lifeblood of economic growth.

It allows individuals and businesses to pull future consumption into the present to invest in productive assets - a house, a factory, an education. This entire system is predicated on the assumption that the borrower will be more productive in the future and that the currency they use to repay the loan will be worth roughly the same, or slightly less, than when they borrowed it.

A mild inflationary environment "greases the wheels" of the economy by encouraging investment and making debt burdens manageable over time.

Bitcoin's permanent deflationary nature turns this entire model on its head, creating a trap for any would-be borrower.

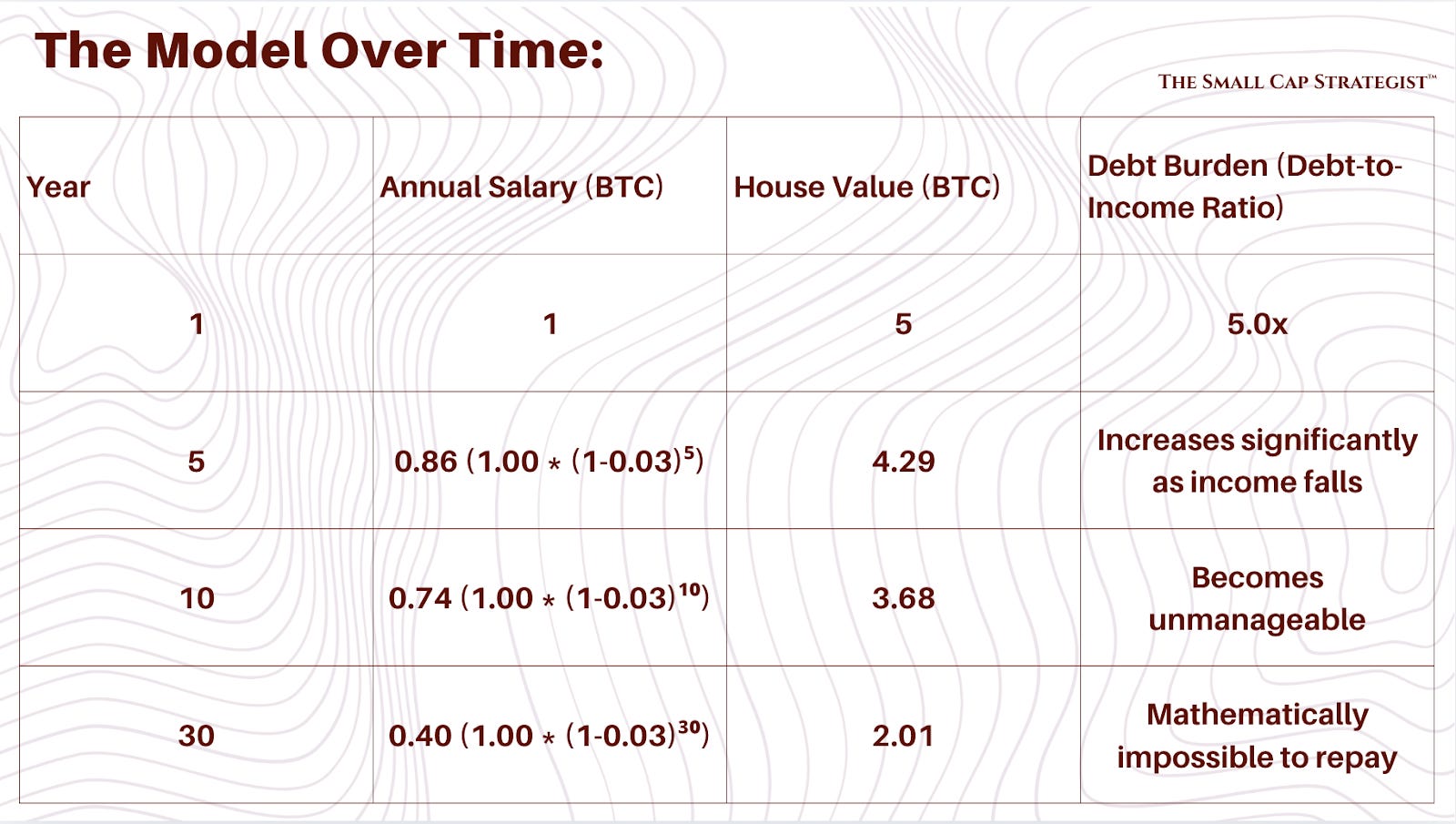

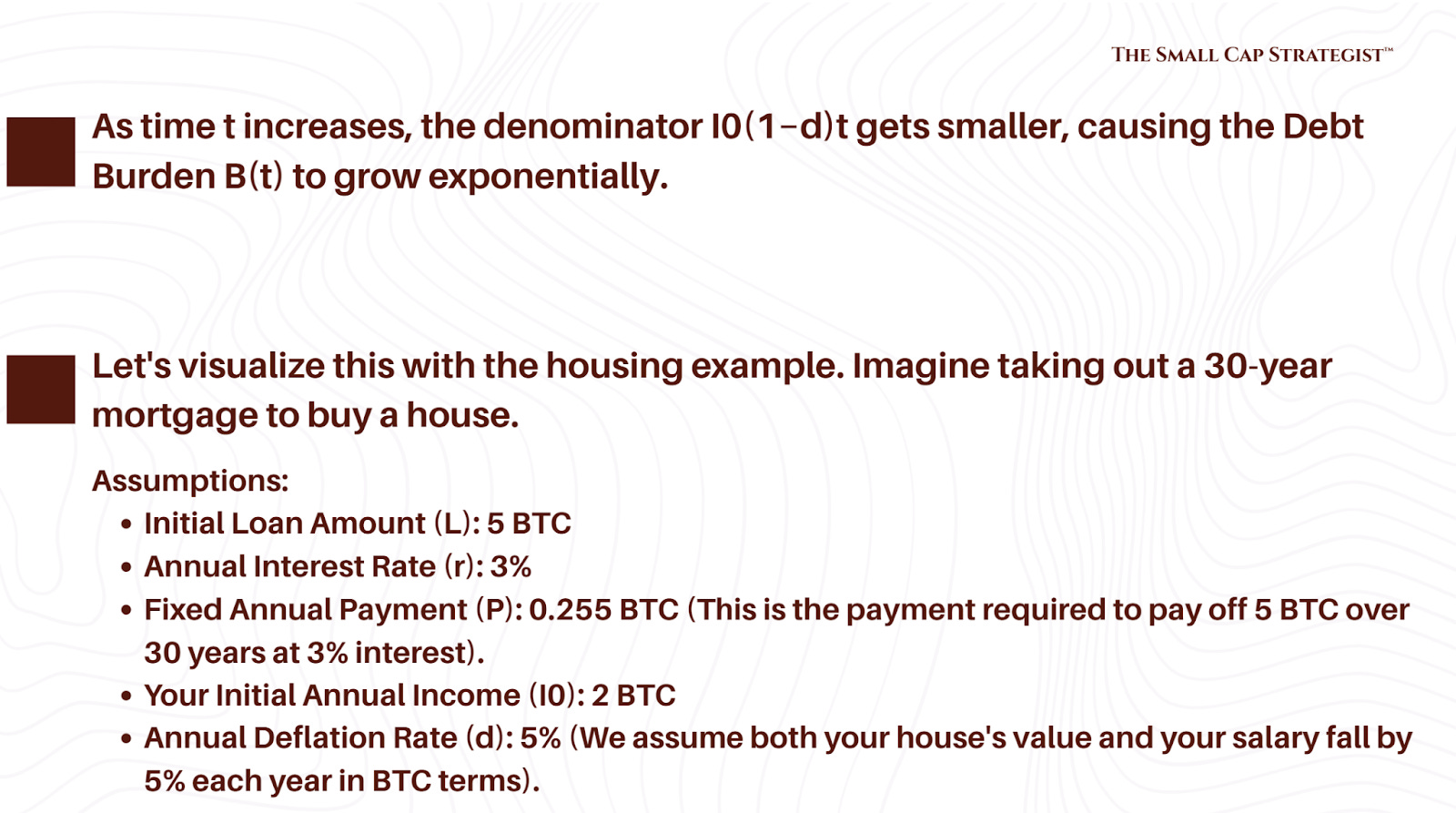

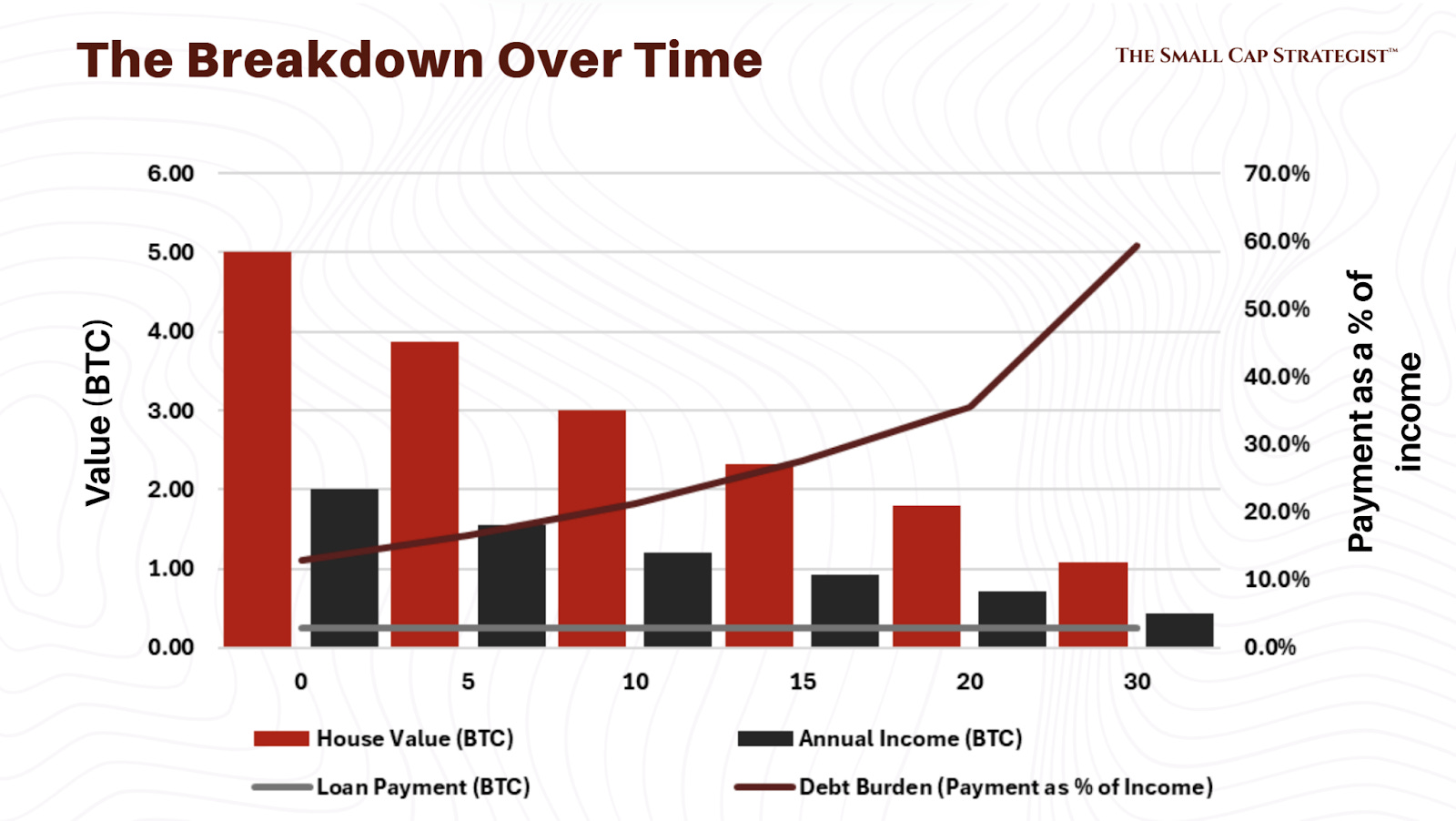

Let's walk through Mike Green's powerful example of trying to buy a house in a Bitcoin-denominated world.

Imagine you want to buy a house that costs 5 Bitcoin. You go to a lender and take out a 30-year mortgage for 5 BTC.

In a deflationary system, the value of that house, priced in Bitcoin, will fall over time. In a few years, it might only be worth 2 BTC. But you don't owe 2 BTC; you still owe the original 5 BTC, plus interest.

The problem is even worse than it appears.

It’s not just the price of your house that is falling in Bitcoin terms; the price of your labor is falling too. Your salary, denominated in Bitcoin, will shrink over the years. You are now contractually obligated to repay a loan of 5 BTC with a salary that is worth fewer and fewer Bitcoin each year, to pay for an asset that is also worth fewer and fewer Bitcoin.

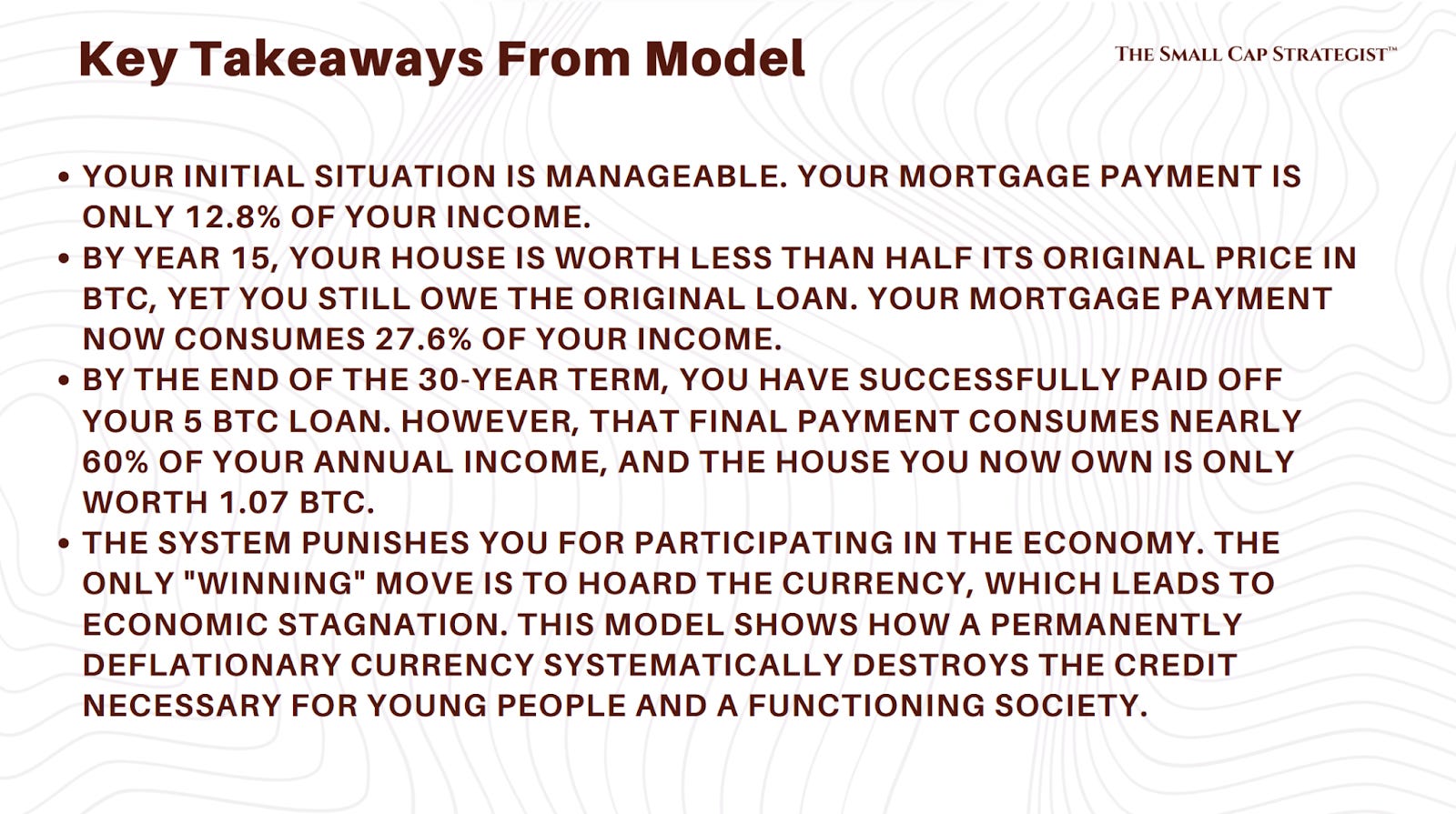

Repayment becomes mathematically impossible, and the only rational decision is to default.

This dynamic would instantly freeze the credit markets. No rational person would borrow, and no rational lender would lend, in such an environment. The tools that young people, in particular, rely on to build capital and participate in the economy, mortgages, car loans, student loans, small business loans, would cease to exist. Economic activity would grind to a halt as the incentive structure shifts entirely from productive investment to hoarding the monetary asset itself.

Why would you risk starting a business when you can generate a guaranteed real return by simply holding your Bitcoin as everything else gets cheaper around you?

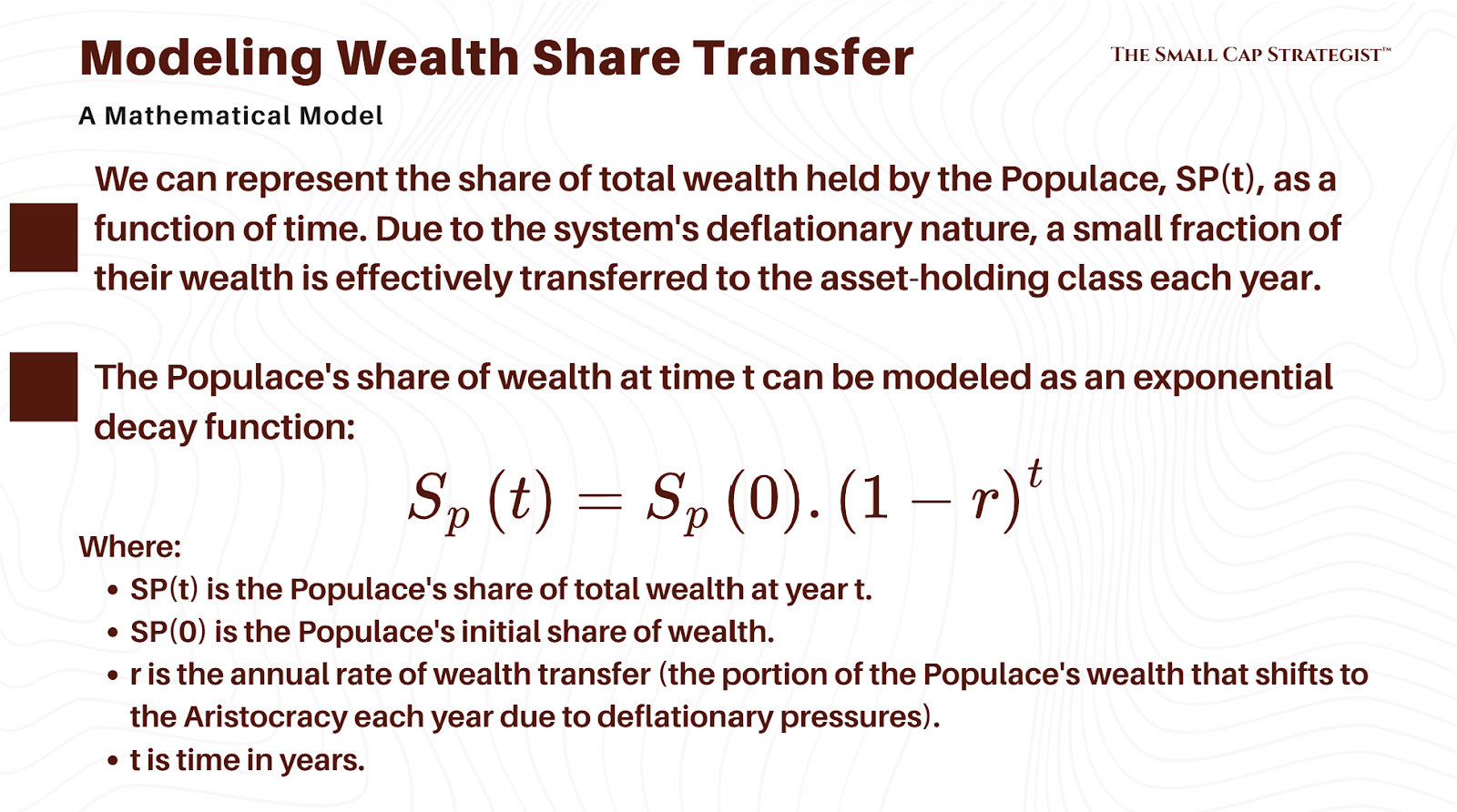

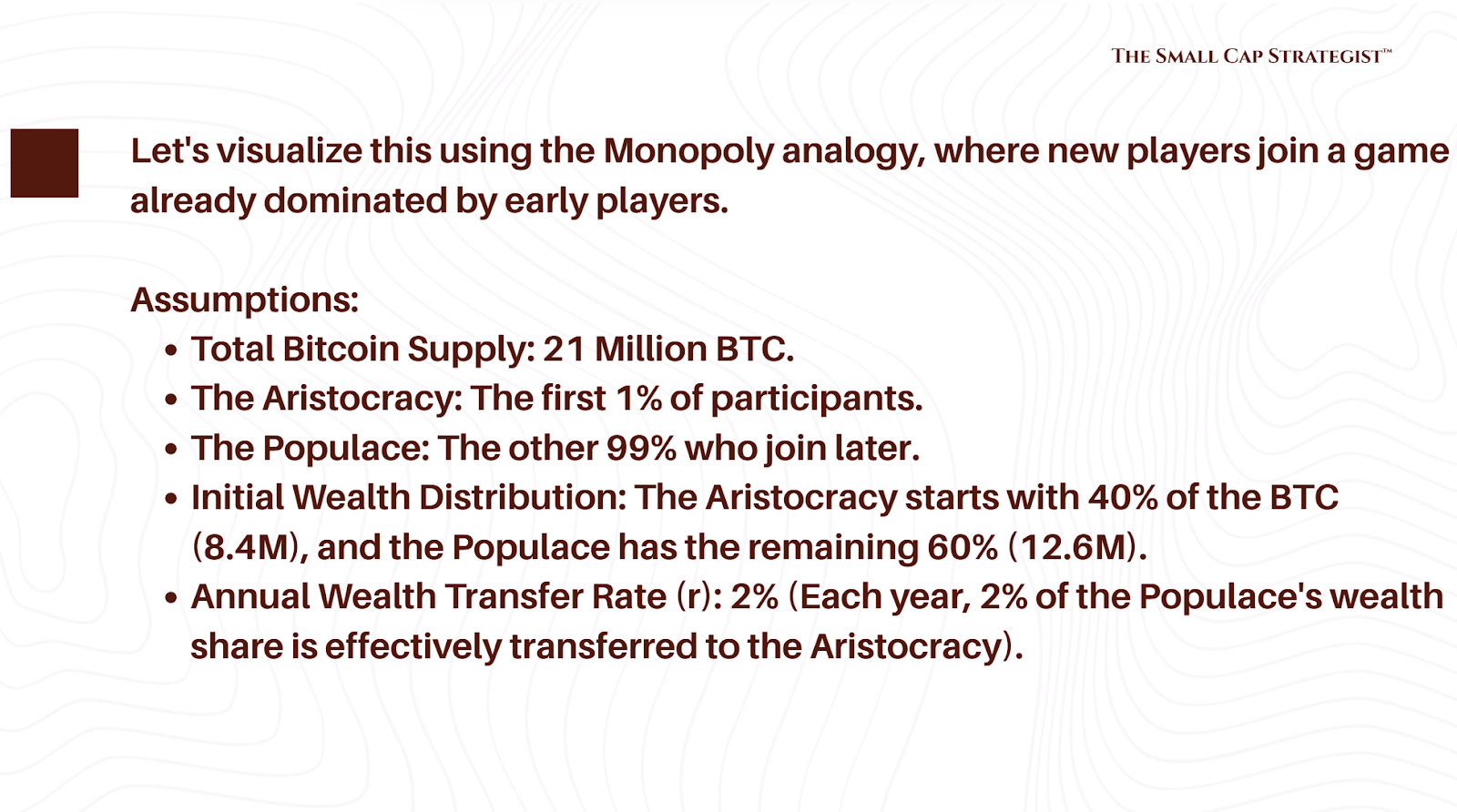

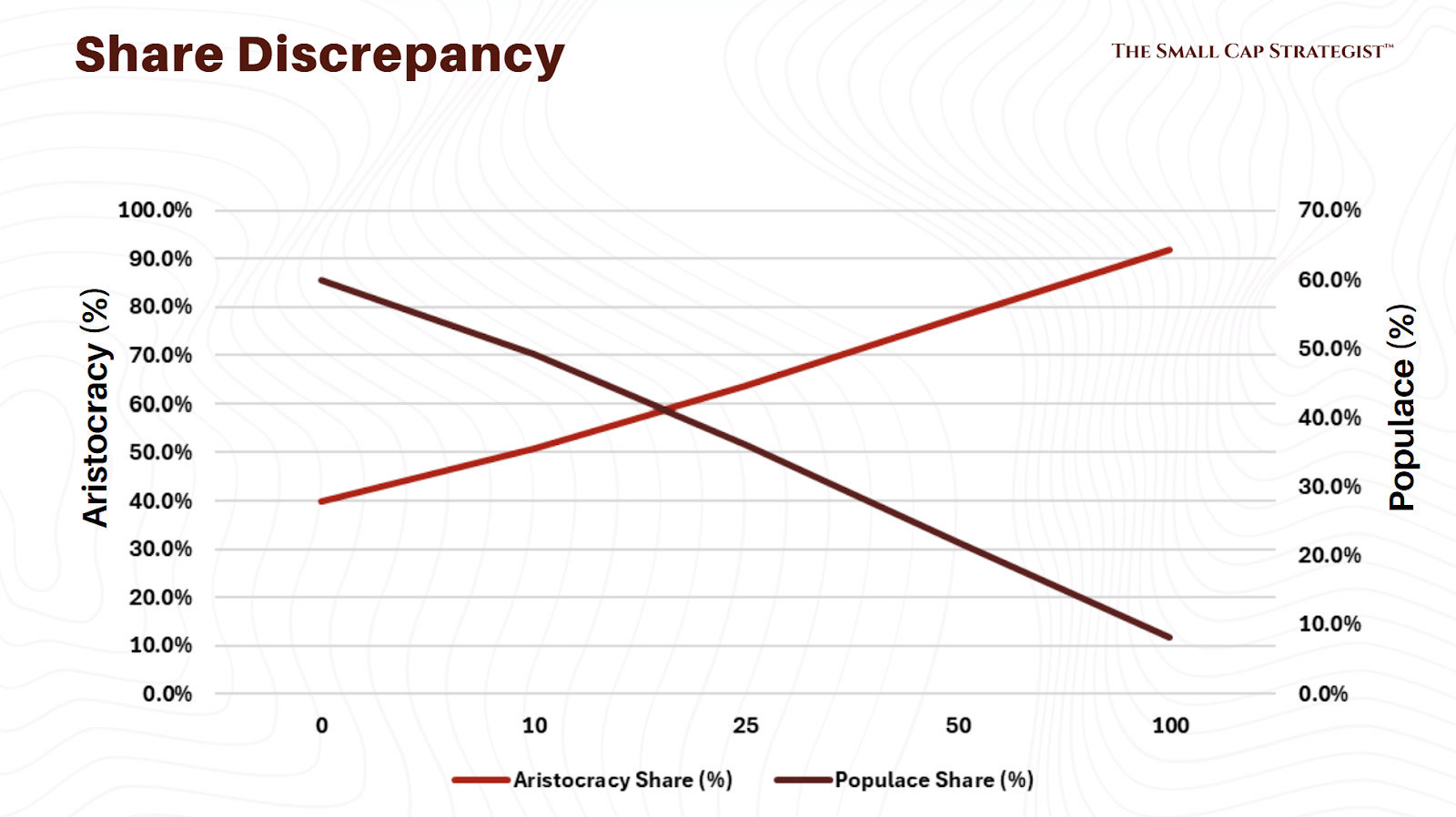

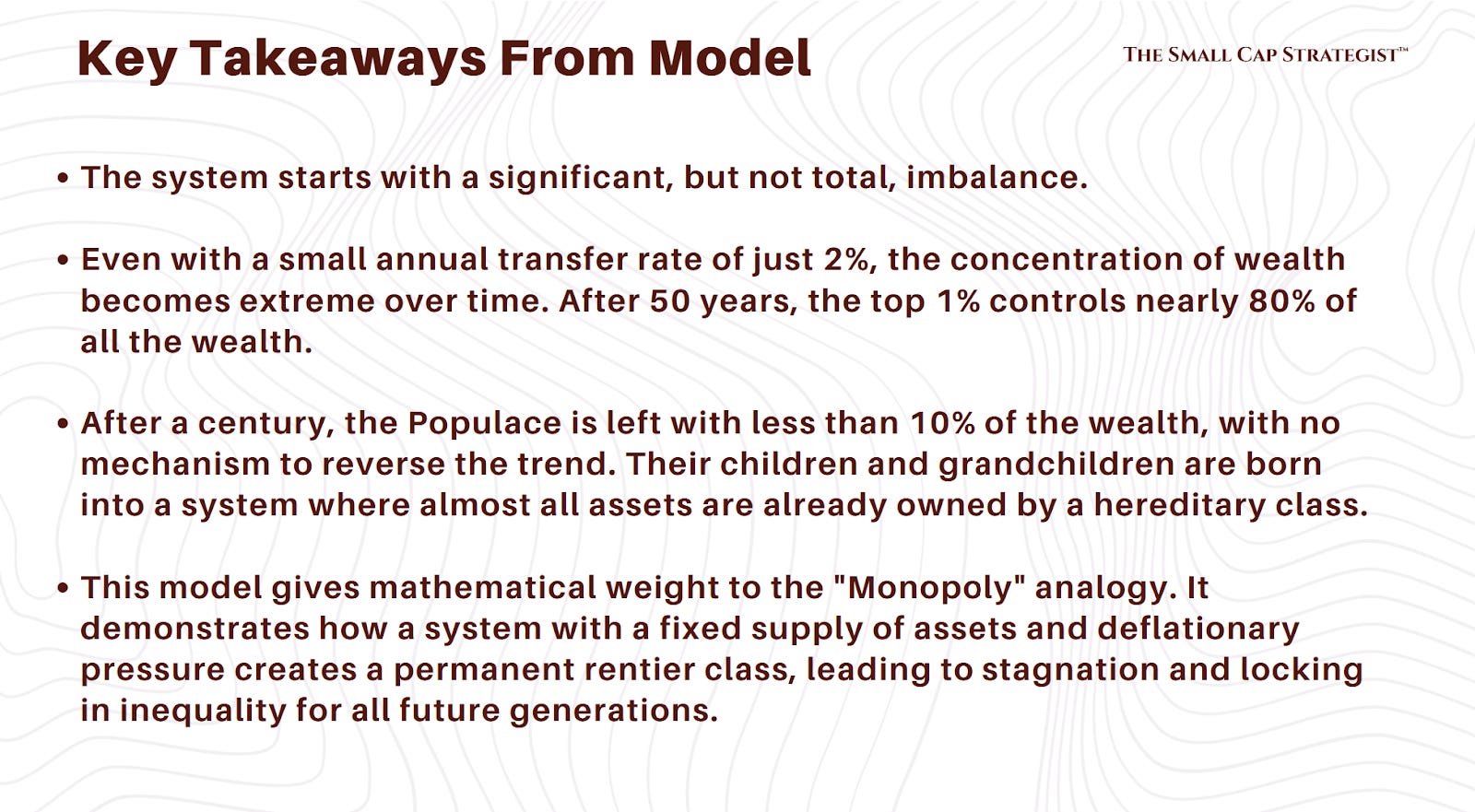

The Creation of a New Aristocracy

This leads to the most disturbing societal consequence of a Bitcoin standard.

It is not a neutral or democratizing force. It is a system that is fundamentally anti-youth, anti-innovation, and anti-social mobility. It is a system designed to create a new, permanent, and entitled aristocracy.

Consider the structure.

Nearly all of the Bitcoin that will ever exist have already been created; as of today, we are approaching 20 million of the 21 million total supply. New entrants into the economy (our children and grandchildren) are born with no Bitcoin endowment. In the deflationary world Bitcoin creates, their labor will be worth progressively less in Bitcoin terms, and the primary mechanism for capital accumulation (credit) will have been destroyed.

The only people who win in this system are those who already hold the Bitcoin.

They become a rentier class, living off the ever-increasing purchasing power of their assets, which grows not because of any value they create, but because of the labor and productivity of everyone else. As Mike Green puts it:

They become a "new form of entitled aristocracy living off of the land that was effectively granted to them by the king".

The Gini coefficient (a measure of wealth inequality) within the Bitcoin world is already far higher than in the broader economy, and this system would lock that inequality in permanently.

It is a game of Monopoly where the first players to the board have already bought Park Place and Boardwalk, and everyone else who joins is destined to land on their properties and slowly bleed out their starting cash, with no hope of ever acquiring property themselves. This is not a foundation for a prosperous and dynamic society; it is a recipe for stagnation and generational conflict.

Inelasticity Trap - How Fund Flows Create the Illusion of Value

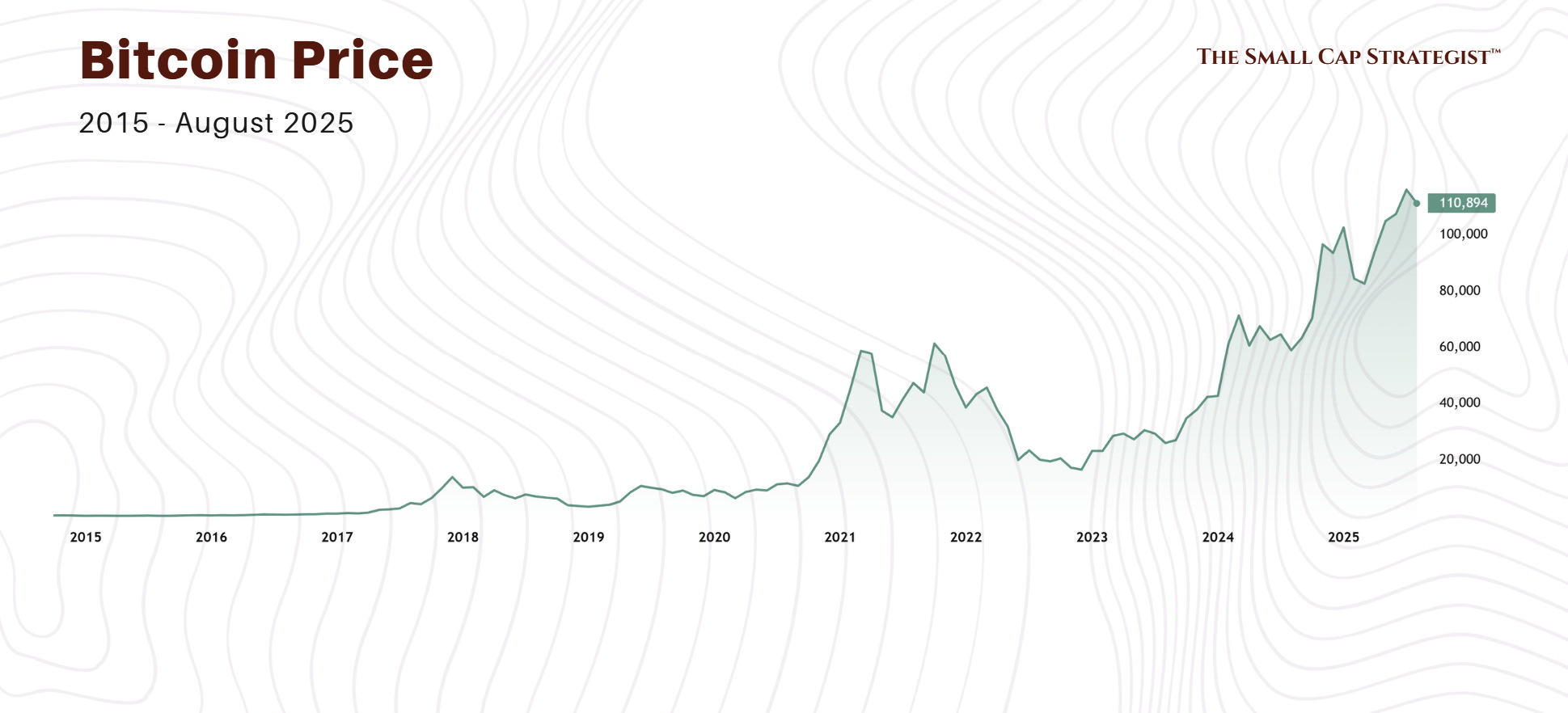

If the macroeconomic case for a Bitcoin standard is so dire, why has its price appreciated so dramatically?

The answer lies not in economics, but in pure market mechanics. Bitcoin's price is not a reflection of its growing utility or fundamental value; it is a direct, almost predictable, consequence of its inelastic supply colliding with new waves of speculative demand.

First, we must acknowledge the crucial pivot in Bitcoin's core narrative. It was originally launched with the title "Bitcoin: A Peer-to-Peer Electronic Cash System". It was meant to be a transactional currency. But as a payment system, it failed. Transaction volumes have remained stagnant for over seven years, and the network can't handle the throughput required for a global payment system.

Faced with this failure, the narrative morphed. Bitcoin was no longer a payment system; it was a "store of wealth," a digital equivalent to gold. This was a tacit admission that it had no real-world utility. Its value proposition was reduced to one thing: the belief that its price would go up. The community even developed a mantra for this strategy: "hodl," a deliberate misspelling of "hold".

This pivot made Bitcoin's value entirely dependent on attracting new buyers.

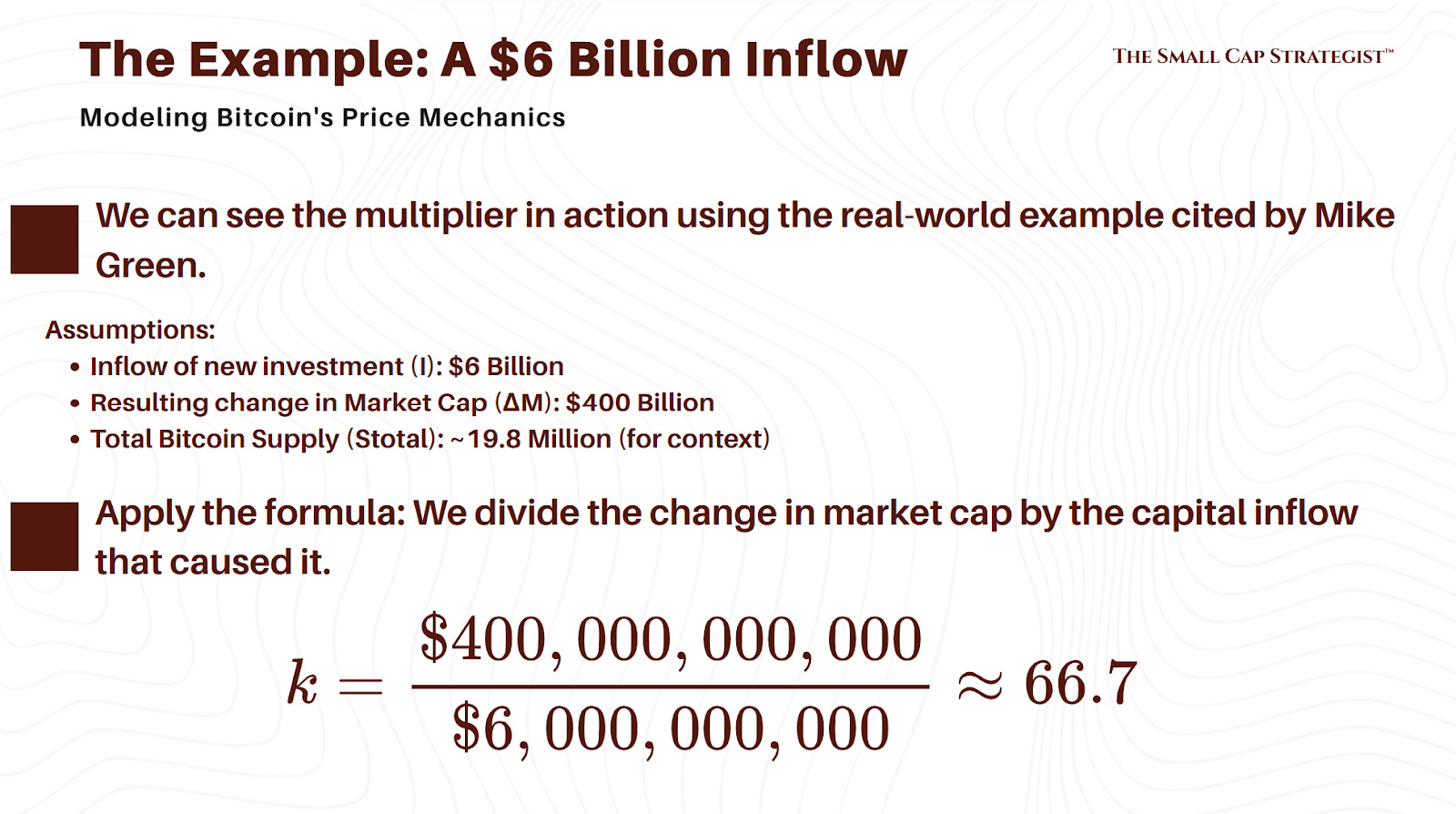

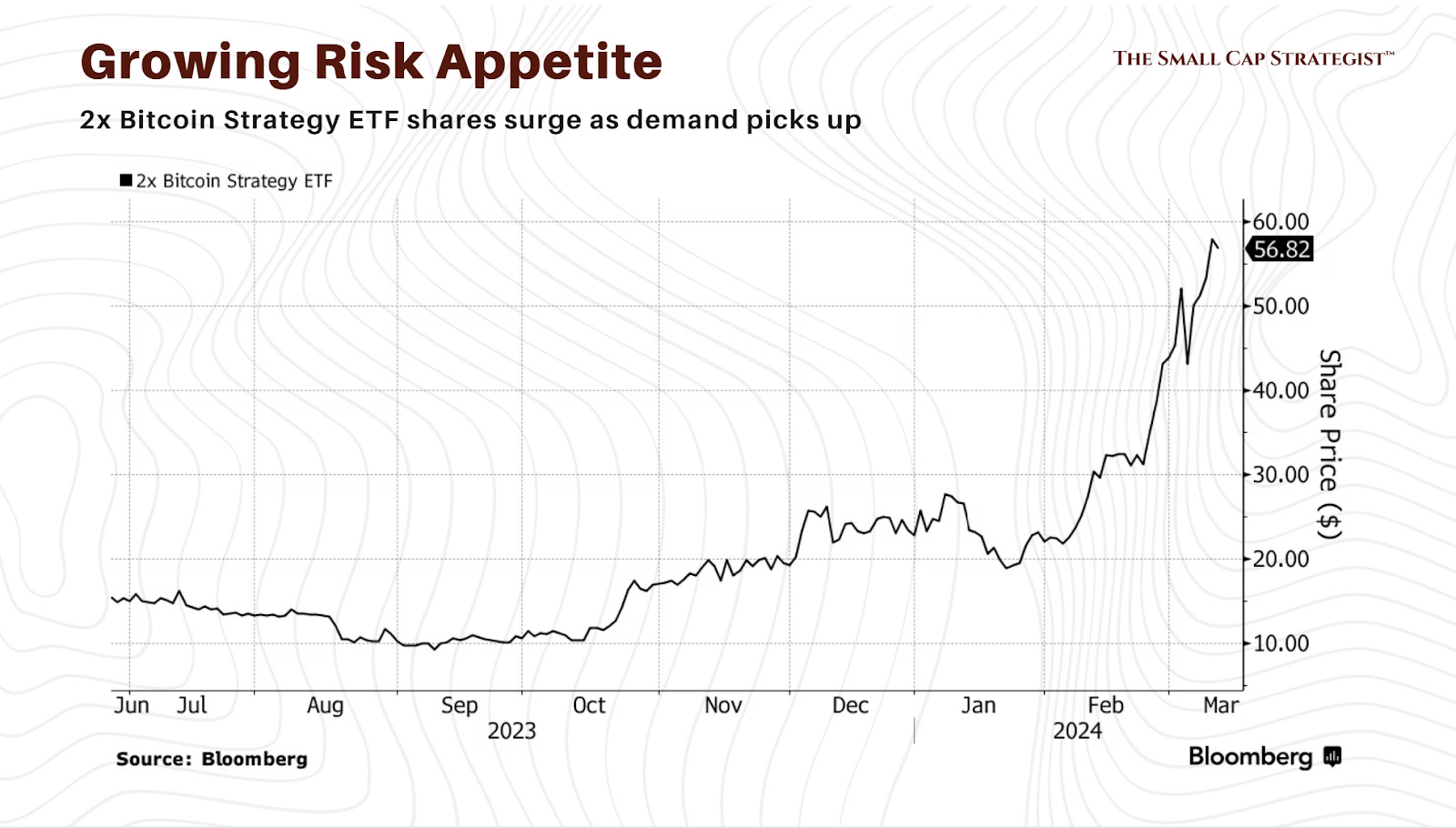

And because its supply is perfectly inelastic, the price has become a simple function of fund flows. The chart presented by Mike Green, showing the relationship between monthly changes in Bitcoin held in funds like ETFs and the change in Bitcoin's price, is staggering. The correlation is nearly perfect. The price of Bitcoin is not a mystery; we know exactly what is driving it: new money flowing into a fixed supply of assets.

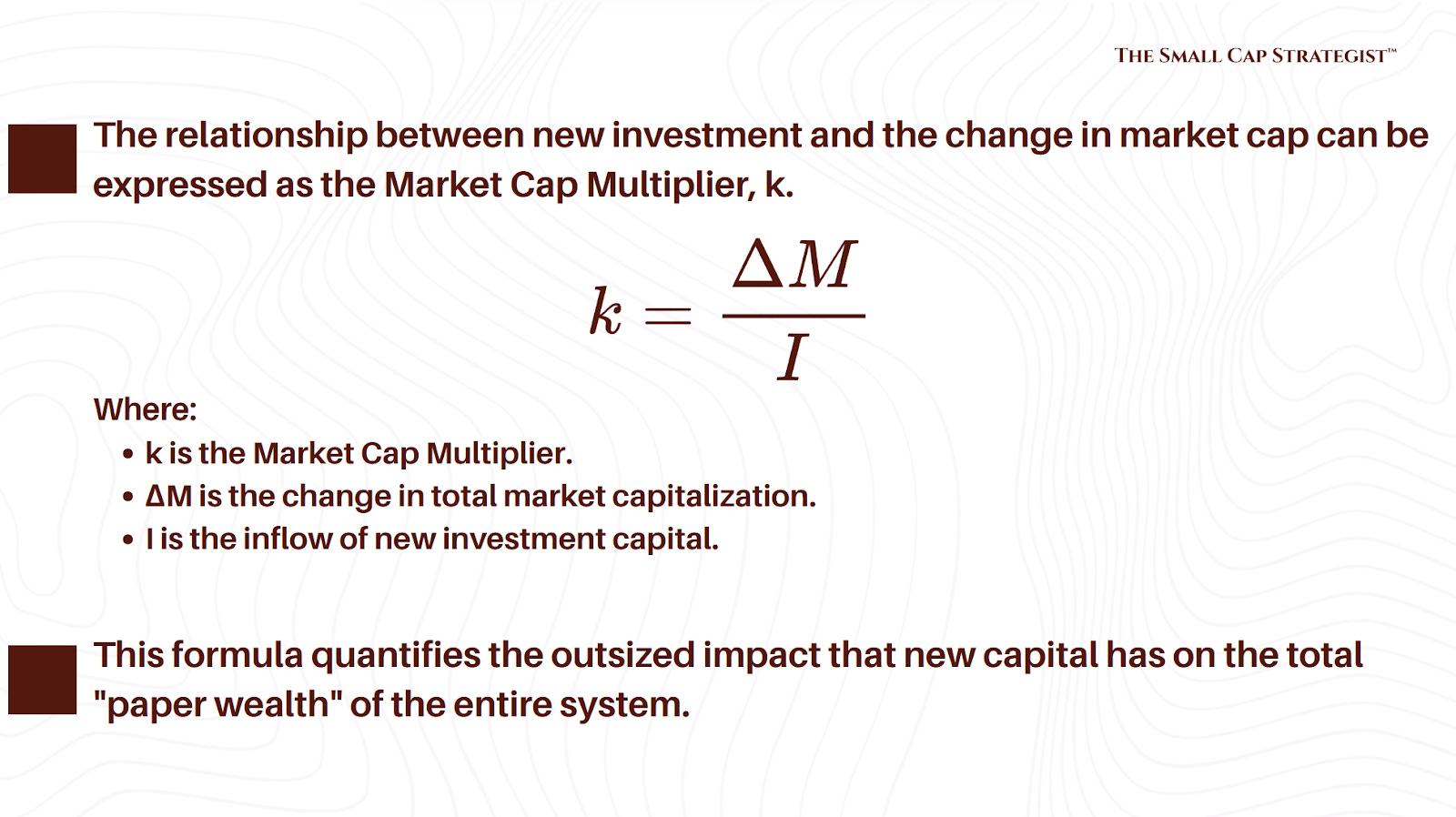

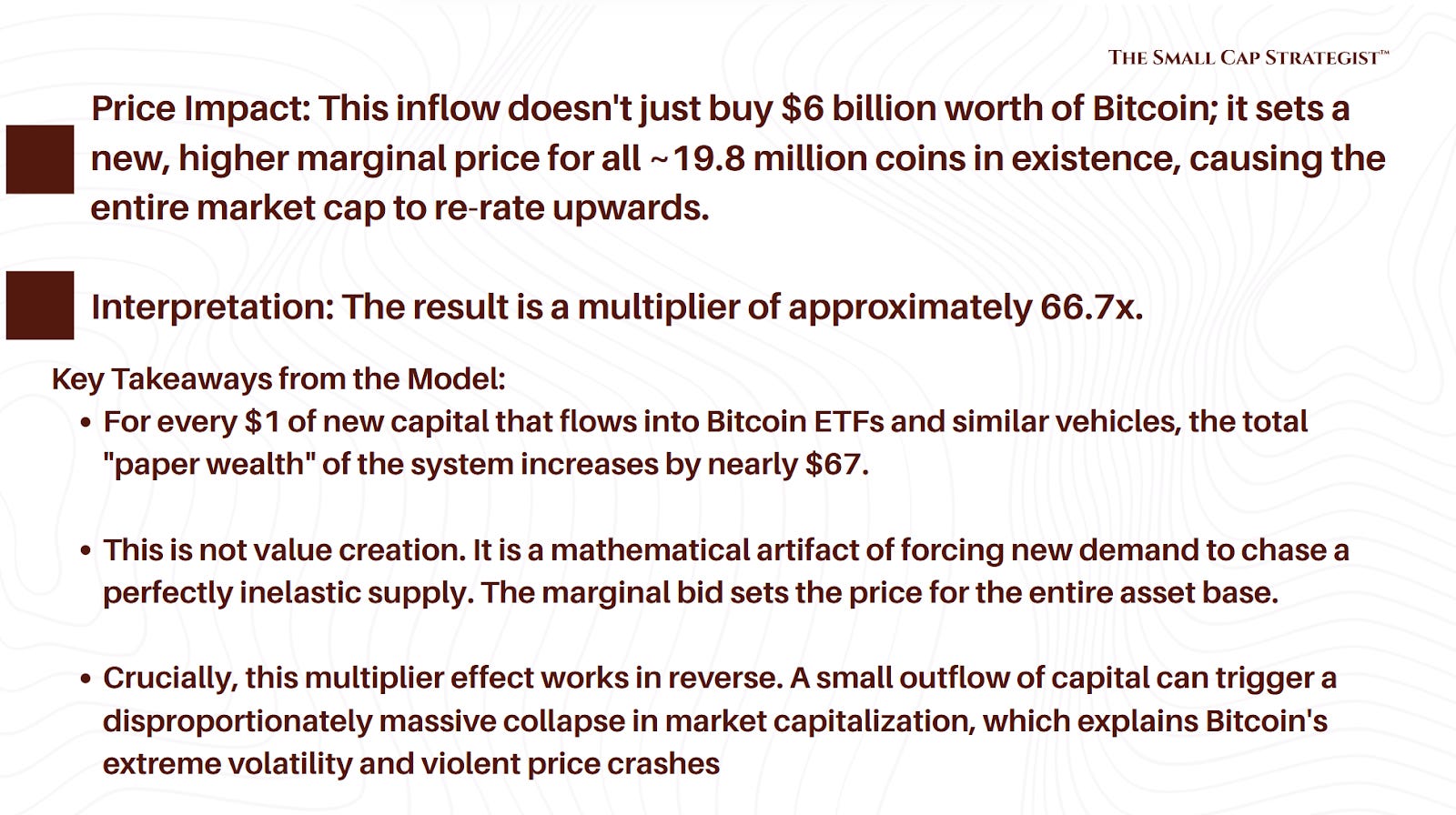

This creates an incredible multiplier effect. As Green explains, an inflow of just $6 billion can create a theoretical increase in the total market capitalization of $400 billion.

This isn't "value creation" in any meaningful sense. It's a mathematical artifact of the system's design. When new demand enters a market with an elastic supply (like the stock market, where companies can issue new shares), that demand can be met by both a price increase and a supply increase. In Bitcoin's market, the supply cannot increase, so 100% of the new demand must be expressed through a higher price for the existing units.

This dynamic creates a reflexive loop that is structurally identical to a Ponzi scheme. While it may not be an explicit fraud, its mechanics are the same: the returns for existing holders are paid for entirely by the capital of new entrants.

Bitcoin generates no yield, no cash flow, no productive output. Its only "return" comes from selling it to someone else for a higher price. The community’s own embrace of the "greater fool theory" is a candid acknowledgment of this reality.

The strategy is to "hodl" until a "greater fool" comes along, propelled by the latest wave of institutional adoption or ETF launches, to buy your coins at a higher price.

The danger of this structure is that it works both ways.

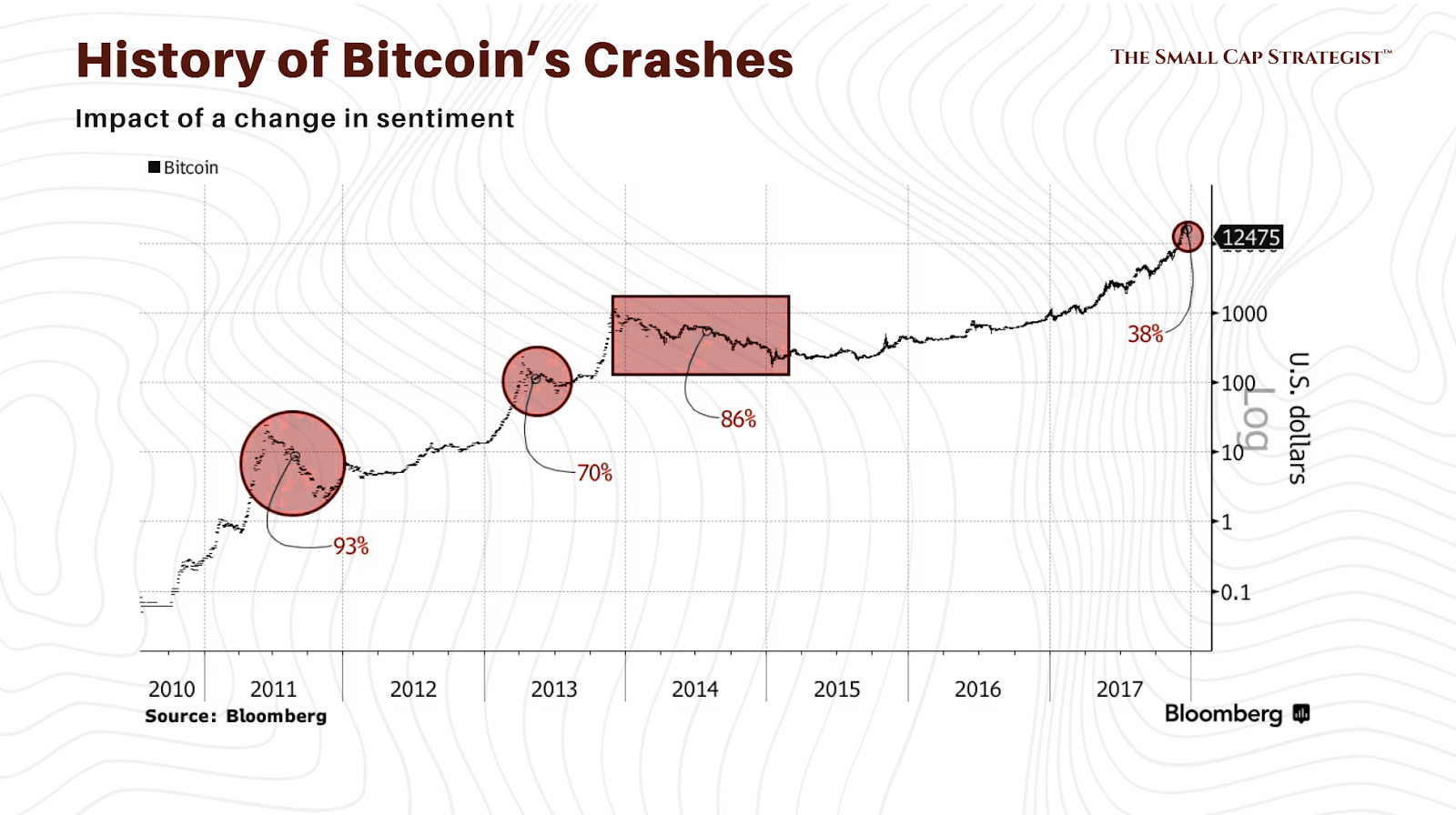

The same inelasticity that causes dramatic price rises on the way up will cause a catastrophic collapse when the flows reverse. Unlike a company such as Microsoft, which even in a market crash is still a profitable business generating billions in cash flow, Bitcoin has no fundamental value to act as a backstop. When sentiment shifts and the flows turn negative, the price will fall with the same mechanical force with which it rose. It is a system with no brakes and no floor.

Bitcoin-Squared - New Financial Engineering

Just when you think the structure couldn't get any more precarious, Wall Street’s financial engineers have added a new layer of leverage and complexity.

We are now in the era of what can only be described as "Bitcoin-squared" - synthetic, leveraged investment vehicles that are embedding crypto risk deep within the traditional financial system.

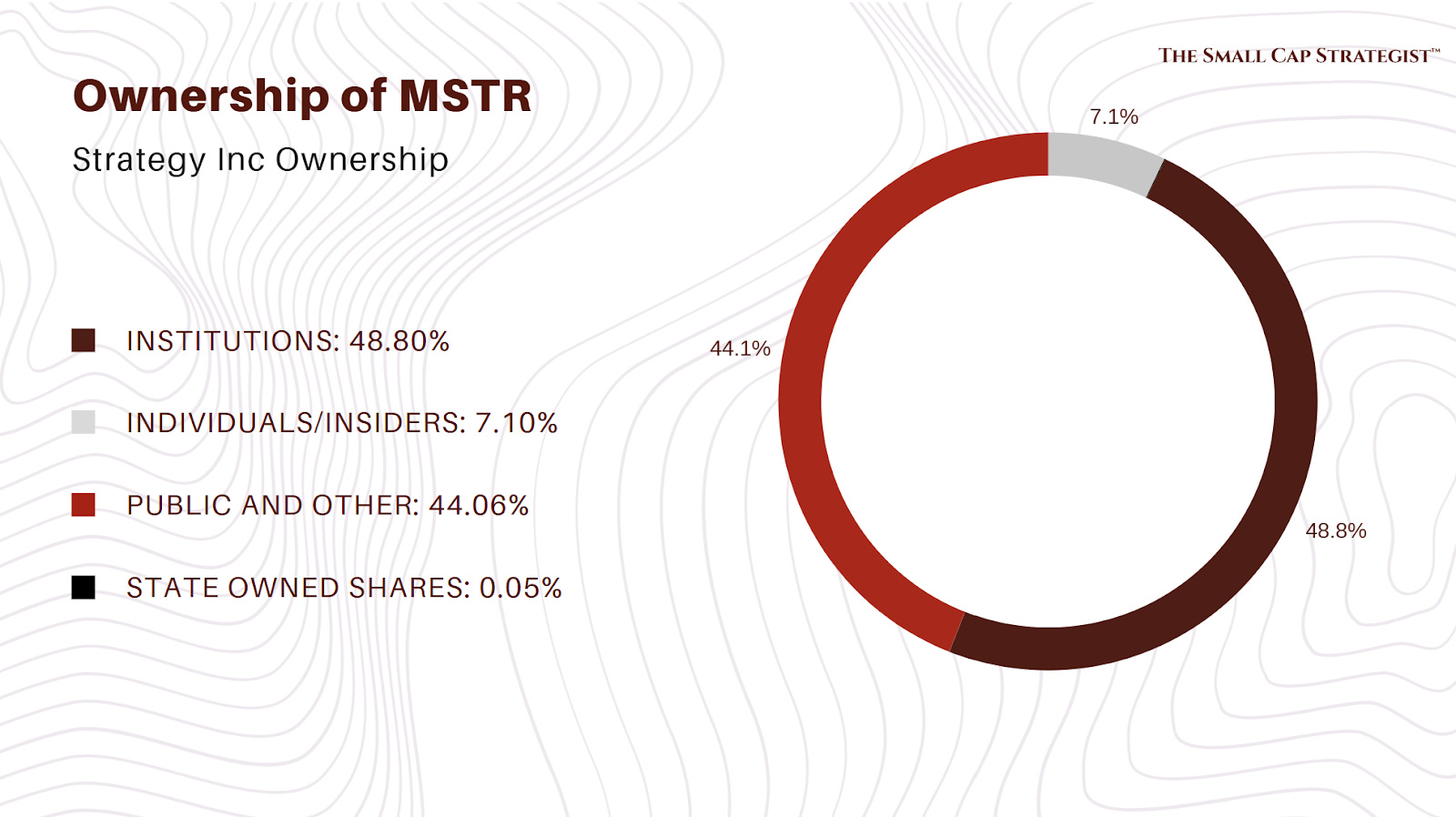

The primary vehicle for this is the Bitcoin Treasury Company (BTC). Inspired by Michael Saylor’s software company MicroStrategy (now rebranded as Strategy Inc.), these are publicly traded companies that have abandoned their original business models to become de facto leveraged Bitcoin funds. They raise capital from public markets (issuing stock, convertible bonds, and other forms of debt) for the primary purpose of buying and holding Bitcoin on their balance sheets.

This development is eerily reminiscent of the financial engineering that preceded the 2008 global financial crisis. The most powerful analogy, laid out in a recent analysis, is that these BTCs are the "CDO-squareds of the crypto universe".

To understand this, let's quickly recap.

A Collateralized Debt Obligation (CDO) was a security built by pooling together thousands of mortgages. A "CDO-squared" was an even more complex and dangerous instrument: it was a security built by pooling together slices of other CDOs. It was a derivative built on a derivative, a layer of leverage and risk built on another layer of leverage and risk. This structure amplified the underlying risk of the subprime mortgage market and spread it to every corner of the financial system.

In this analogy:

Bitcoin is the original CDO: A speculative, non-cash-flowing asset with "little fundamental value" whose price is dependent on a mood of "cultish exuberance".

Strategy Inc. (MicroStrategy) is the CDO-squared: It uses traditional financial instruments (debt and equity) to create a new, leveraged security (its own stock) whose value is derived from the underlying speculative asset. It is, as one commentator bluntly put it:

a "Ponzi scheme upon a Ponzi scheme".

Looking into MicroStrategy

Let's briefly look at the mechanics of Strategy Inc. to see how dangerous this is. The company's legacy software business is largely irrelevant; it generates minimal cash flow and is not growing. We made a full, in-depth analysis of MicroStrategy Inc.’s financials and scheme here:

Its real business is a "flywheel" of financial engineering:

Issue debt or equity to raise fiat currency (e.g., US dollars).

Use that cash to buy Bitcoin.

Point to the rising price of Bitcoin (which its own buying helps support) to justify a higher stock price.

Use the higher stock price as collateral to issue even more debt and equity to buy even more Bitcoin.

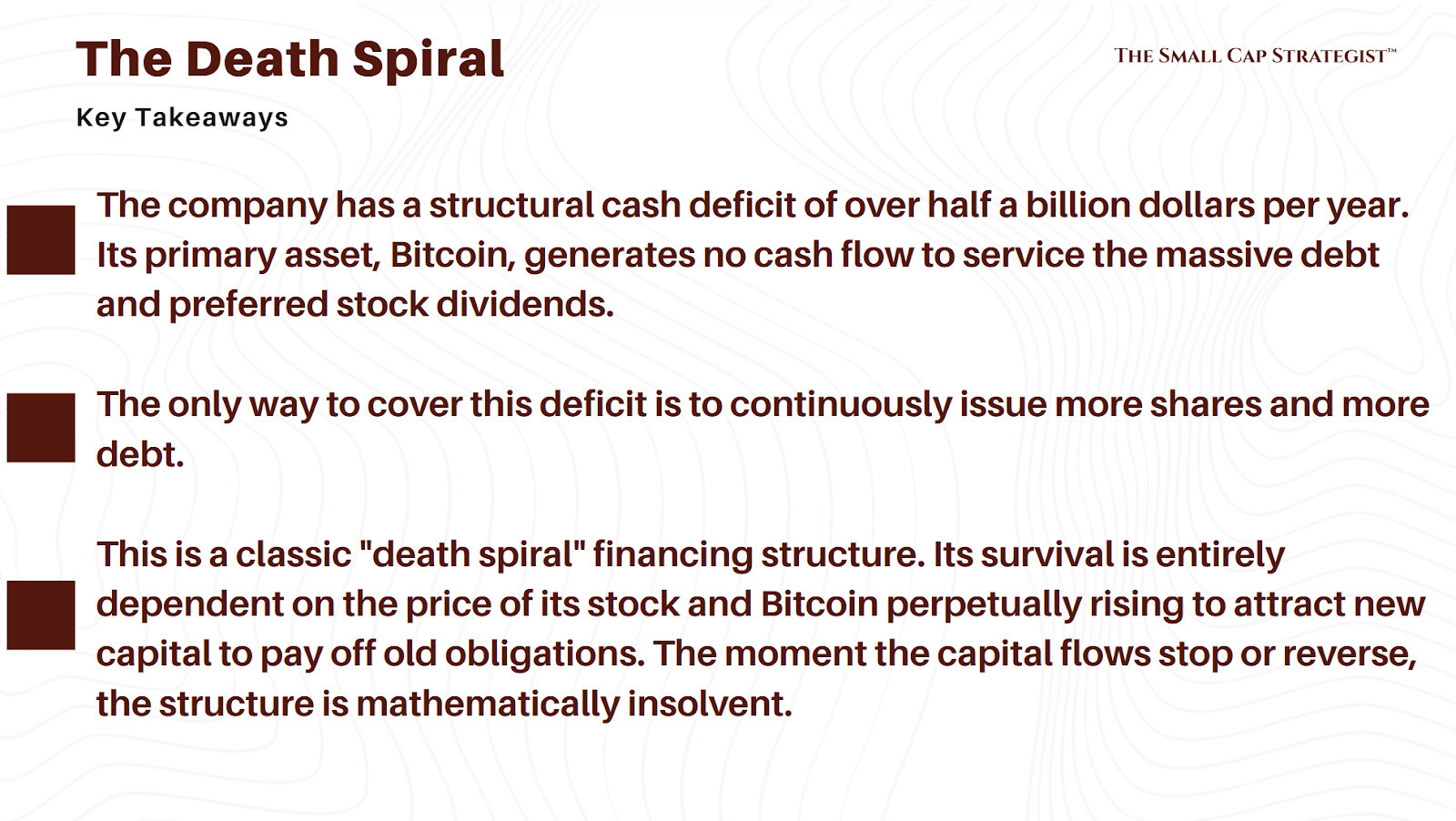

As of late 2025, this strategy has resulted in the company holding over 600,000 BTC while accumulating over $8 billion in total debt. This creates a massive structural vulnerability. Strategy Inc. has very real, contractual fiat cash obligations—interest payments on its billions in debt and potential dividends on preferred stock. Yet its primary asset, Bitcoin, generates zero cash flow. It does not, as Mike Green notes, "sexually reproduce".

This leaves the company in an impossible position. To meet its cash obligations, it has only a few choices:

Pay them with cash from its software business (which is insufficient).

Sell its Bitcoin holdings (which would crater the price of Bitcoin and its own stock, destroying the entire model).

Raise new cash by issuing more stock and debt to pay the interest on the old stock and debt.

This third option is the path they are on, and it is a classic "death spiral" financing structure. It is a model that is entirely dependent on the company's ability to continuously attract new capital at ever-higher valuations. The moment that confidence falters or the fund flows stop, the entire leveraged structure collapses.

Blurring the Lines and Hiding the Risk

The most insidious aspect of this new wave of financial engineering is how it creates a bridge for crypto risk to infect the traditional financial system. Many institutional investors, like pension funds and mutual funds, have mandates that prohibit them from buying crypto directly. However, they are perfectly free to buy the common stock or convertible bonds of a US-listed software company.

By purchasing shares of MSTR, these institutions are circumventing their own risk management rules and acquiring leveraged, synthetic exposure to Bitcoin. This means that the next "crypto winter" won't be contained to the crypto ecosystem. It will trigger defaults in the corporate bond market and cause massive losses in the equity portfolios of unsuspecting investors who thought they owned a software company, but actually owned a highly leveraged crypto fund. The misery, as the saying goes, will be squared.

This is precisely how the subprime crisis metastasized. The risk wasn't contained to a few bad mortgages; it was packaged, synthesized, and sold into every part of the global financial system. Bitcoin Treasury Companies are playing the same role today, creating a transmission mechanism for a new and poorly understood form of systemic risk.

Conclusion: Clear-Thinking Investor

We started this journey by questioning the most fundamental article of faith in the crypto world: that Bitcoin's absolute scarcity is its greatest strength.

After examining it from the perspective of monetary theory, macroeconomic stability, market mechanics, and financial engineering, a different picture emerges.

The core takeaway is that in economics, the type of scarcity matters profoundly. Gold's elastic scarcity is adaptive. It allows the monetary system to respond to the needs of a growing economy, making it a resilient, if imperfect, foundation.

Bitcoin's absolute, rigid scarcity is brittle. It is a feature designed by engineers with little thought for the dynamics of a real-world economy, and it creates a system that is hostile to credit, innovation, and social mobility.

The dizzying rise in Bitcoin's price is not evidence of its success as a monetary good. It is the predictable outcome of a system with inelastic supply fueled by speculative inflows: a dynamic that is inherently unstable. The new layer of "Bitcoin-squared" financial engineering only serves to amplify this instability, creating leveraged time bombs on corporate balance sheets and hiding the risk within traditional portfolios.

Just as we were once joyous at the sight of a stock buyback, we used to see Bitcoin's rising price as a validation of its model. Now, we look at it far more cautiously, with a will to dig deeper into the unsustainable mechanics driving it.

Bitcoin is a fascinating technological experiment and has proven to be a potent speculative vehicle. But its core design makes it a poor foundation for a currency and a dangerous one for an economy. Its greatest proclaimed strength is, in fact, its fatal flaw.

If you enjoyed this post, consider supporting our work by becoming a paid or free subscriber.

You raise some thought provoking counter arguments to how I view Bitcoin which absolutely have some merit. One thing that you miss (and I believe is missed / misunderstood by almost everyone when it comes to Bitcoin) is the role that the cost of mining plays when it comes to the price of Bitcoin (a function of the cost of miners, power and hashrate) and the impact this has on elasticity/scarcity points you raise. You link price to funds flow but don’t consider the impact of the cost of mining - it is forgotten that the ways to acquire bitcoin (ignoring ridiculous BTC treasury companies) is to purchase it or to mine it. Mining will always play a key role, even once all 21 million coins are mined, mining rewards will transition to transaction fees (something referenced in the Bitcoin white paper). In my view, it will also be possible to earn yield on Bitcoin through safe lending once such protocols are established. This is something that realistically can’t happen for gold given its physical properties limit it from realistically acting as a currency and another reason why, in my view, it is a superior store of value over gold in the long term.

I love how you exposed the flaws in the ‘Bitcoin as a global currency’ idea.

But what if that’s the wrong lens?

Isn’t Bitcoin’s true value proposition just being a non-sovereign lifeboat in a world of sinking fiat currencies?

Maybe its rigidity and ‘brittleness’ are exactly what you want in an escape hatch, even if it makes for a terrible permanent home.