Finding Compounders (10x) in APAC's Construction Material Sector

APAC Construction Materials Industry Research With Small/Mid Cap Idea Generation, Understanding The APAC Construction Materials Super-Cycle.

The biggest opportunities are often hidden in plain sight. While global headlines chase the ephemeral trends in software and AI, one of the most powerful secular growth stories of the next decade is being built, quite literally, from the ground up. The Asia-Pacific region is in the midst of a multi-trillion-dollar construction boom, and for the prepared investor this offers a wealth of untapped potential.

Welcome to The Small Cap Strategist. Our mission is to look past the obvious mega-caps and uncover the high-growth, under-the-radar companies poised to dominate their niches. Today, we're applying that lens to our third deep dive on the APAC region: the construction materials market.

You might think this sector is just about global giants like CRH and Holcim. But the real story for a strategist lies in the industry's structure. It's a landscape defined by fragmentation, hyperlocal monopolies, and a constant cycle of M&A, the perfect ground for identifying future winners and strategic acquisition targets. This analysis builds on our previous work in the region, where we uncovered opportunities such as these:

Inside this post you will find:

The Market Broken Down: We'll break down the entire value chain, from the local quarry's geographic moat to the global logistics of a cement powerhouse.

The Four Core Theses: An actionable framework based on Consolidation, the 'Green Premium,' Digital Transformation, and Niche Dominance.

Regional Outlook: An analysis of the distinct opportunities in China, India, Japan, South Korea, Australia, and the high-growth ASEAN nations.

The Strategist's Watchlist: A list of small and mid-cap companies in each region that are positioned to capitalize on these powerful trends.

If you want to build a portfolio of unique, high-conviction ideas and gain an edge by understanding the powerful forces shaping global markets, subscribe to The Small Cap Strategist and join a community of discerning investors.

A Multi-Trillion Dollar Market

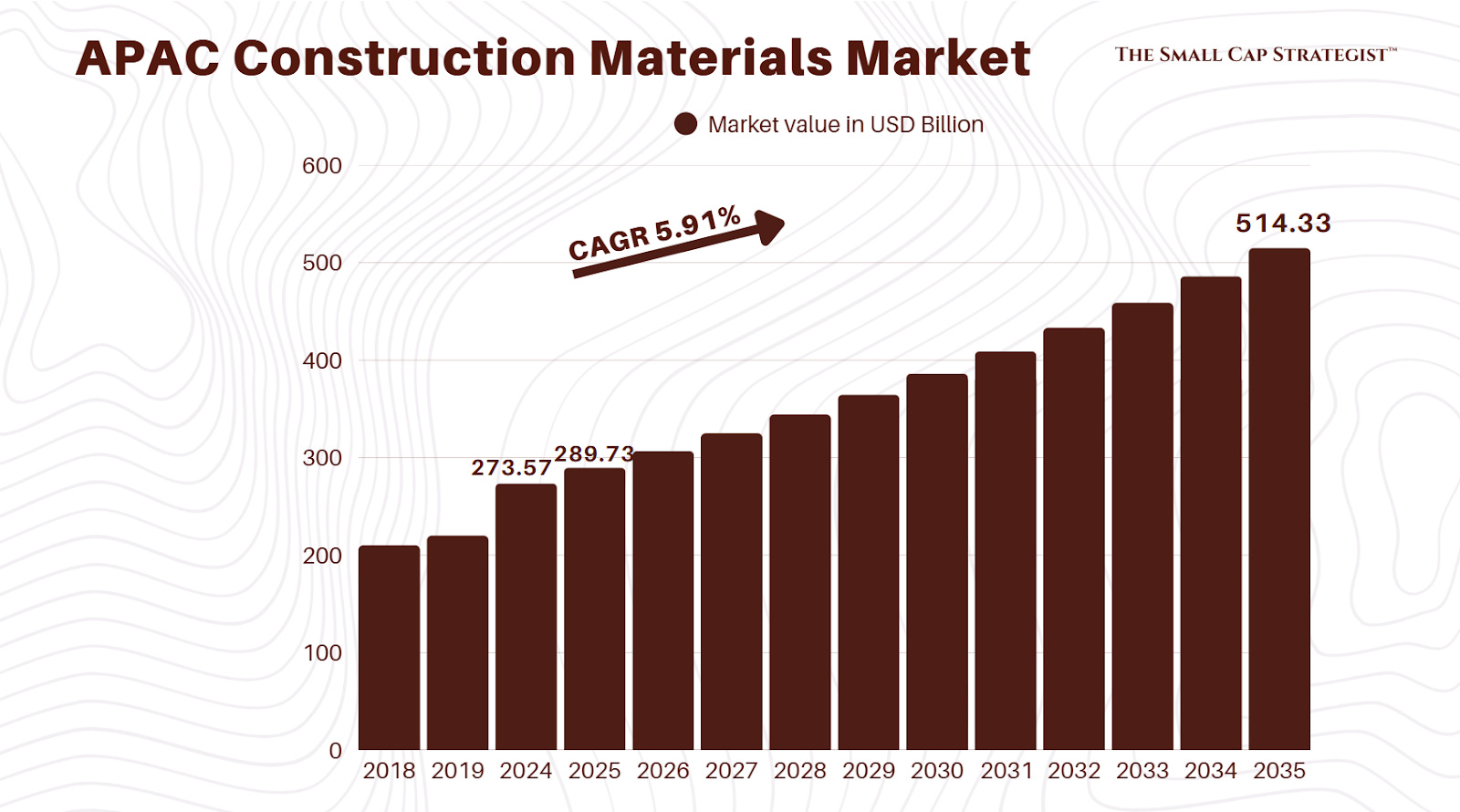

The scale of the APAC construction materials market is impressive. Valued at over USD 273.57 in 2024, the sector is forecast to expand at a compound annual growth rate (CAGR) of approximately 5% to 6% through 2035, reaching an estimated value of USD 514 billion by that year. This market does not exist in a vacuum; it is the essential supplier to a broader regional construction industry valued at over USD 5.6 trillion. The CAGR demand is due to the 21st century’s trend of mass urbanization and consequent infrastructure investment.

The primary demand driver is the trend of urbanization seen in the APAC region. By 2050, an additional 1.2 billion people are expected to reside in Asia's cities. The United Nations projects that the urban population in APAC will reach 3.1 billion by 2030, an increase from 2.4 billion in 2020. This migration creates a non-discretionary, long-term demand for every part of the built environment. In China, the urbanization rate is moving towards a projected 75% by 2035, creating a constant need for new housing and urban amenities. Similarly, India must construct an estimated 20 million new housing units annually to accommodate its urbanizing population.

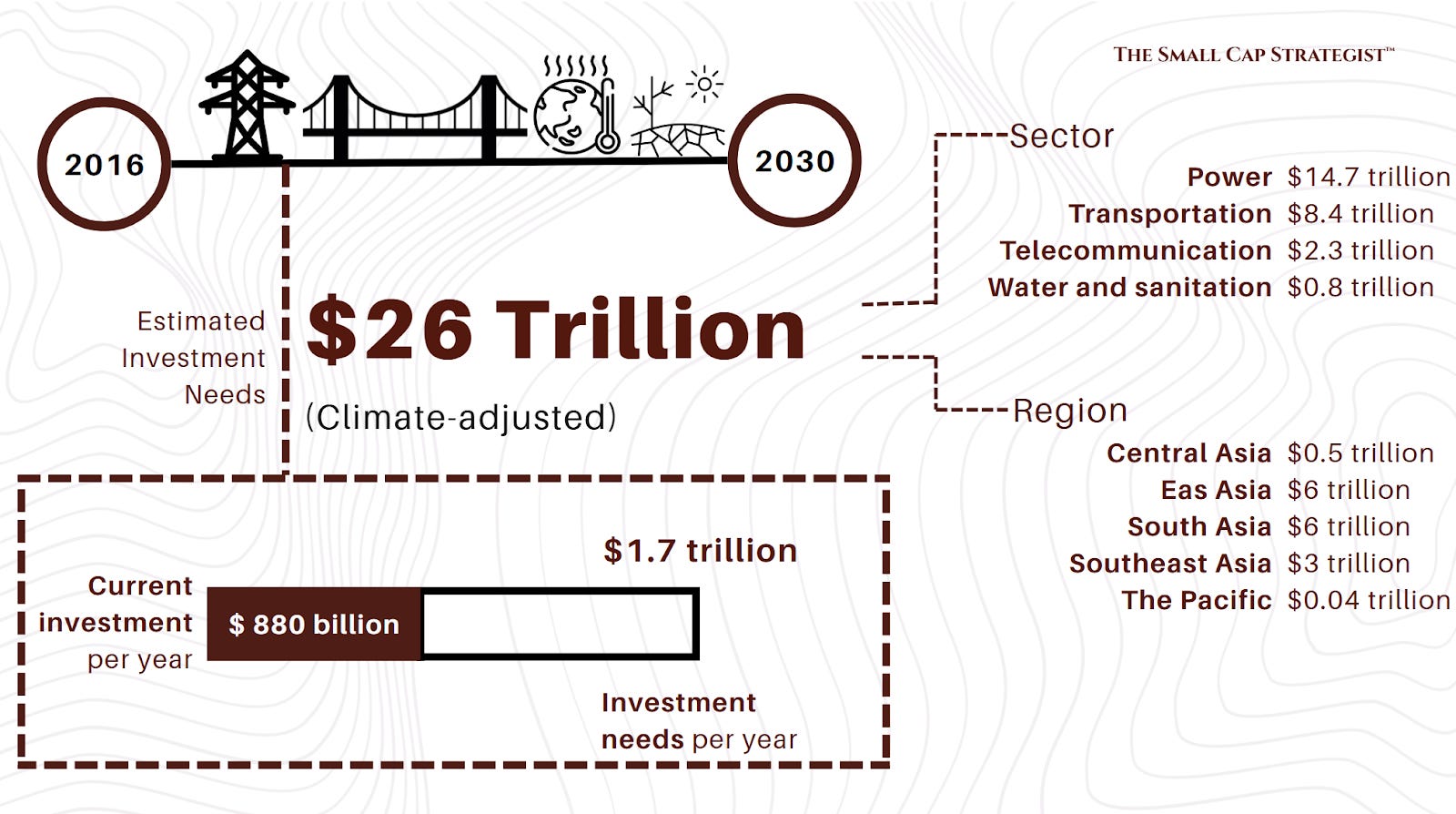

Governments across APAC, along with multilateral institutions, are channeling trillions of dollars into foundational projects to support economic growth, enhance connectivity, and improve living standards. The Asian Development Bank (ADB) has quantified this need, estimating that the region requires infrastructure investments totaling USD 26 trillion between 2016 and 2030. This translates to an annual spending requirement of USD 1.7 trillion to maintain growth momentum.

China's ambitious Belt and Road Initiative (BRI) and 1,100 other projects have contributed to more than USD 1 trillion in cumulative engagement since 2013. These projects create a large and sustained demand for Chinese construction materials and services across Asia. At the national level, countries are pursuing their own transformative programs. India's Smart Cities Mission and "Housing for All" scheme are designed to modernize urban centers and address the housing deficit, directly contributing to demand for cement, steel, and aggregates. Japan has committed to a substantial infrastructure budget of around 10 trillion JPY over the next decade to upgrade its world-class systems and prepare for events like the 2025 World Expo.

The confluence of these powerful drivers points toward an almost guaranteed demand curve for construction materials for the foreseeable future. The demographic and policy-driven nature of this demand provides a high degree of certainty. Therefore, the central question for investors shifts from if materials will be needed to which companies are best positioned to execute the delivery. The primary risks and opportunities within the sector are not found in demand forecasting but in understanding the operational realities of the business. The winners will be those who can overcome the immense challenges of logistics, supply chain management, resource permitting, and labor availability.

Value Chain Deconstruction

A reader must understand the differences in the construction supply chain to accurately assess risk and identify opportunities.

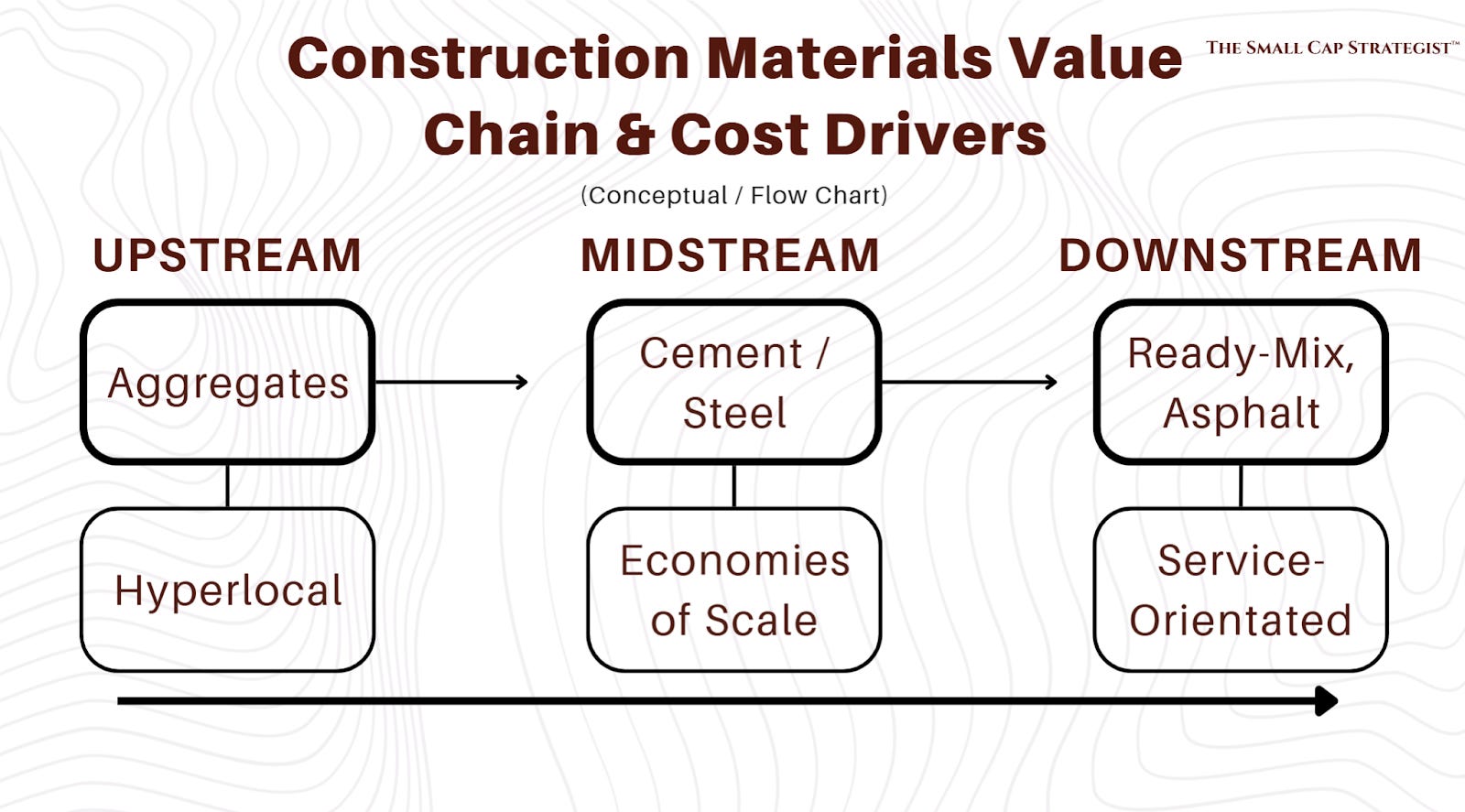

Upstream

Aggregates are at the beginning of the supply chain. These include crushed stone, sand, and gravel used for constructing foundations. As my own operational experience has shown, the aggregates business is fundamentally hyperlocal. These materials are heavy, bulky, and have a low value-to-weight ratio, which makes transportation costs a dominant component of their final price. A quarry's competitive advantage is almost entirely defined by its geographic location and proximity to a major demand center.

Shipping aggregates more than a short distance by truck quickly becomes uneconomical, creating natural, localized monopolies. The centre of the business model is securing long-life, permitted reserves in strategic locations that can last for decades. This is why the industry sees a company profile of several quarries, each serving a specific, geographically constrained market.

Midstream

Cement and steel represent the capital-intensive part of the industry. Unlike aggregates, these are more standardized, higher-value products that can be economically transported over much longer distances. This allows for a more consolidated market structure, where massive production facilities serve entire regions or even international markets. Success in the cement and steel business is predicated on achieving economies of scale, managing high energy costs through efficient kiln and furnace technology, and operating sophisticated, multi-modal distribution networks. Industry giants like China's Anhui Conch Cement and China National Building Material (CNBM) have built their empires on this model of massive scale and logistical efficiency

Downstream

The downstream segment is where basic materials are transformed into higher-margin products and services. This is where the value chain extends closest to the end customer. After my conversation with a Specialist working in CRH and Summit Materials, I found out that vertical integration into downstream activities is a critical strategy for capturing a greater share of the project value, ensuring quality control, and building durable customer relationships. This segment includes:

Ready-Mix Concrete: Cement, aggregates, and water are combined at local batching plants and delivered to construction sites in mixer trucks. These plants must be located within a short drive of job sites due to the perishable nature of the product.

Asphalt: Aggregates are mixed with bitumen at asphalt plants, which are often co-located with quarries to minimize transport costs for the primary input. The asphalt is then used in paving operations for roads, highways, and parking lots.

Value-Added Services: This includes everything from on-site technical support and custom product formulation to full-service paving and construction services.

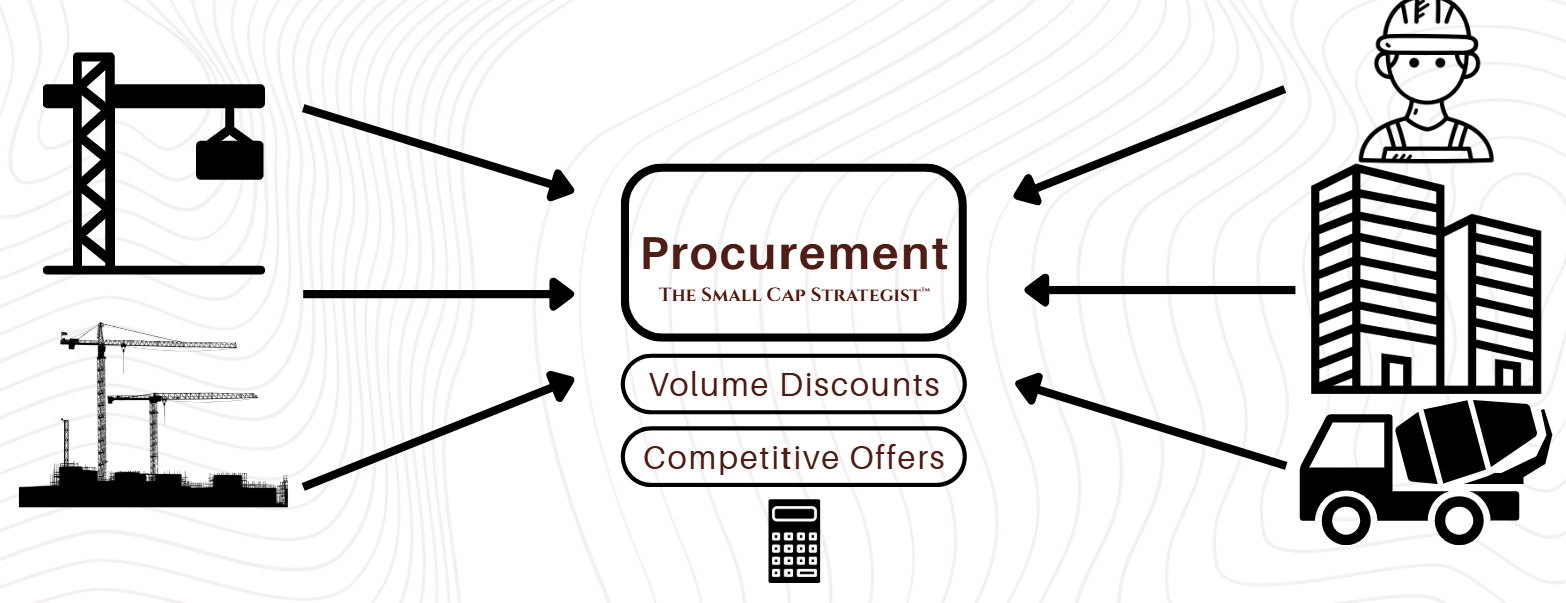

The procurement models used by customers reflect this value chain complexity. Large general contractors on major infrastructure projects may purchase bulk materials like concrete directly from the manufacturer. Smaller subcontractors, however, typically rely on a network of wholesalers and distributors who provide essential services like holding inventory, breaking bulk, and offering just-in-time delivery to multiple job sites. In some cases, the entire material and service package is subcontracted, with the subcontractor managing all procurement and installation.

This structure dictates the investment profile of companies operating at different points in the chain. An investment in a pure-play aggregates company is a bet on its strategic land positions and logistical efficiency; its moat is geography. An investment in a cement or steel company is a bet on its ability to manage commodity cycles, energy costs, and production scale. An investment in a vertically integrated company is a bet on its ability to capture margin at multiple points and deliver a complete solution to the customer. This framework is necessary for analysing the market and generating targeted investment ideas.

Competitors

The market is populated by several types of companies:

Global Integrated Majors: A handful of powerful multinational corporations, including CRH, Holcim, and Heidelberg Materials, operate across the globe. These companies bring large scale, access to capital, and a vertical integration and growth through acquisition strategies. Their presence in APAC allows them to deploy global best practices in operations, sustainability, and technology.

Chinese State-Owned Enterprises (SOEs): SOE’s include Anhui Conch Cement and China National Building Material (CNBM). They have a large portion of the market share in the Chinese domestic market and are increasingly expanding their influence across the region, used in China's Belt and Road Initiative. Their competitive advantages lie in their scale, state support, and integration into national strategic objectives.

Regional Champions: In many APAC countries, there is a main player. Two examples are Larsen & Toubro (L&T) in India, a diversified conglomerate with a massive presence in construction and engineering, and Siam Cement Group (SCG) is a key player in Thailand and the broader ASEAN region. These companies possess deep local market knowledge, extensive distribution networks, and strong relationships with domestic stakeholders.

Fragmented Market Share of Smaller Players: Fragmentation of small caps is most pronounced in the hyperlocal aggregates sector and in the distribution and specialty materials segments.

A critical strategic imperative that defines this industry is growth through Mergers and Acquisitions (M&A). Using what I gathered from the Former Executive Vice President & Chief Operating Officer at Summit Materials, large players systematically acquire smaller ones to achieve several strategic goals: to enter new, high-growth geographic markets, to secure strategically located resource reserves (quarries), to vertically integrate into downstream products and services, and to consolidate market share to gain pricing power. This constant churn of M&A is a fundamental feature of the industry's structure.

This dynamic creates an interesting dynamic for investors. The fragmented nature of the market means there is a continuous supply of potential acquisition targets. For the major players, M&A is the primary engine of inorganic growth. For investors, this means that well-managed small and mid-cap companies are not just standalone investments based on their organic growth prospects. They also possess a potential "call option" on being acquired by a larger strategic buyer, often at a significant premium to their trading value. Therefore, identifying these high-quality, strategically positioned smaller companies is a core thesis for generating alpha in the APAC construction materials sector. They are the building blocks from which the industry's future giants will be assembled.

Characteristics in Each Sub-Sector

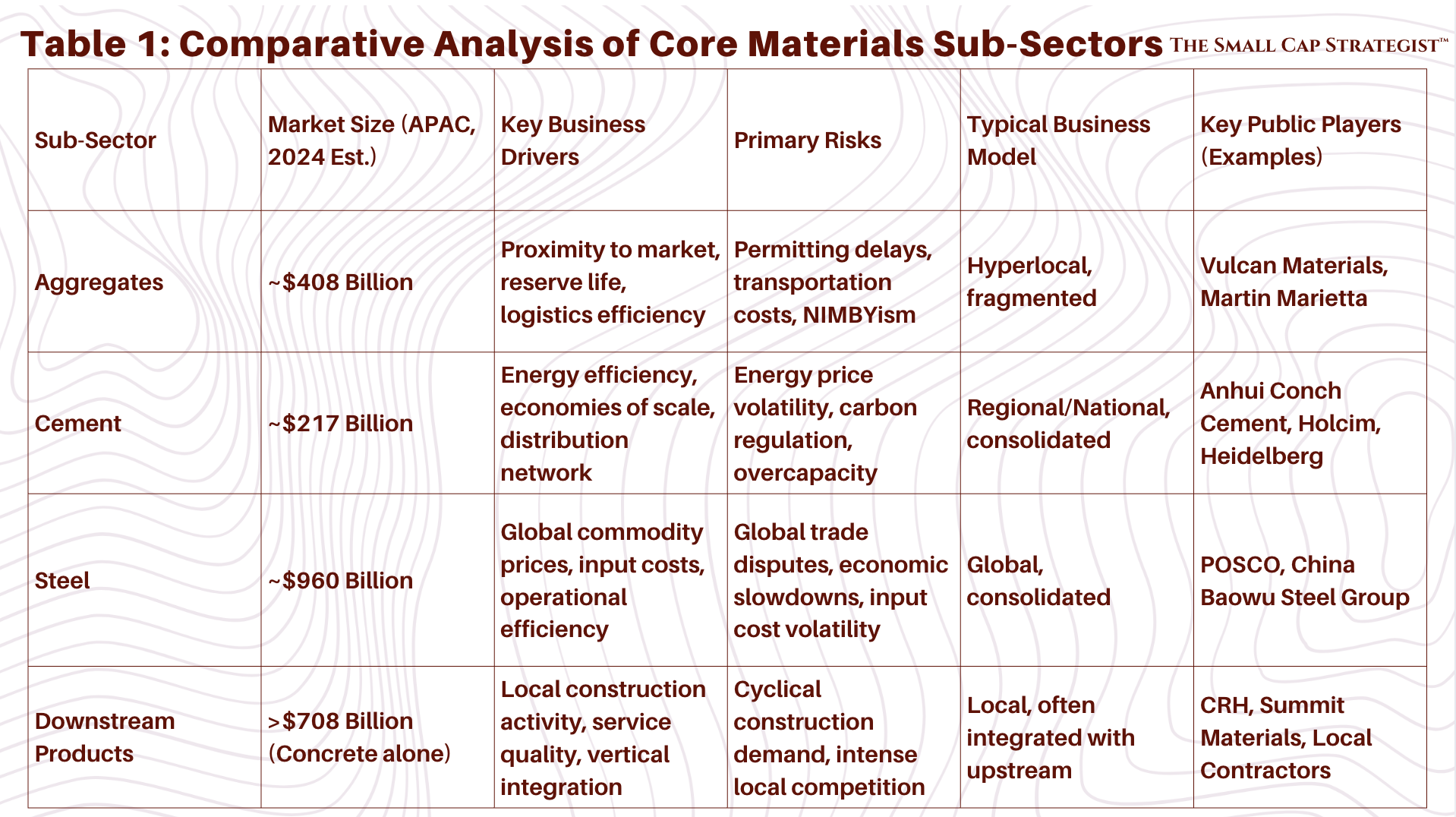

To construct a strong investment strategy, it is important to look into the specific characteristics of each major material sub-sector. Each segment (upstream to downstream) operates with distinct market dynamics, business models, and risk profiles. A good understanding of these differences is necessary for targeted capital allocation.

Aggregates (Crushed Stone, Sand, Gravel)

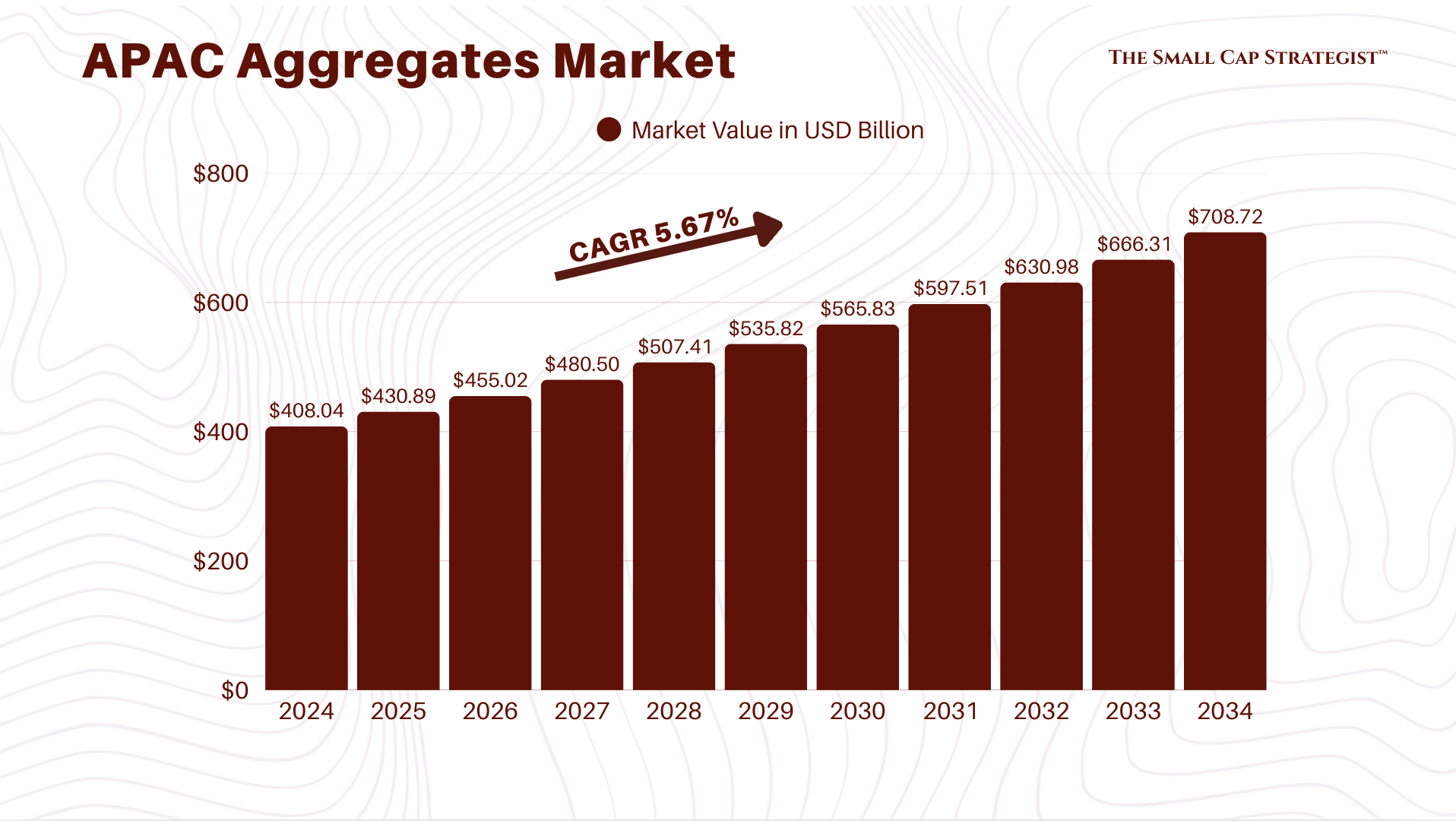

Aggregates are the highest-volume products in construction materials. The APAC aggregates market is valued at approximately USD 408 billion in 2024 and projected to grow at a CAGR of 5.67% to reach USD 708.72 billion by 2034. This growth is a direct function of the region's infrastructure and housing boom.

The business model for aggregates is dictated by geology and geography. As a heavy, low-cost commodity, the economics of aggregates are dominated by transportation costs. This makes the business inherently local. The formula for long-term profitability is the ownership or long-term lease of permitted quarries with high-quality reserves located in close proximity to major metropolitan areas or infrastructure corridors. This proximity creates a significant cost advantage over more distant competitors, establishing a strong economic moat. The industry is therefore characterized by a network of localized markets rather than a single regional or global one.

Growing environmental regulations and the depletion of natural sand and gravel deposits near urban centers, are driving a strong push for the use of recycled aggregates. These are produced by crushing construction and demolition waste (CDW), such as old concrete and asphalt. This practice not only conserves natural resources but also reduces landfill pressure, creating a circular economy within the construction sector. There is rising demand for lightweight aggregates, such as expanded clay or sintered fly ash, which can reduce the overall dead load of a structure, allowing for more efficient design and lower foundation costs, particularly in high-rise buildings.

Cement

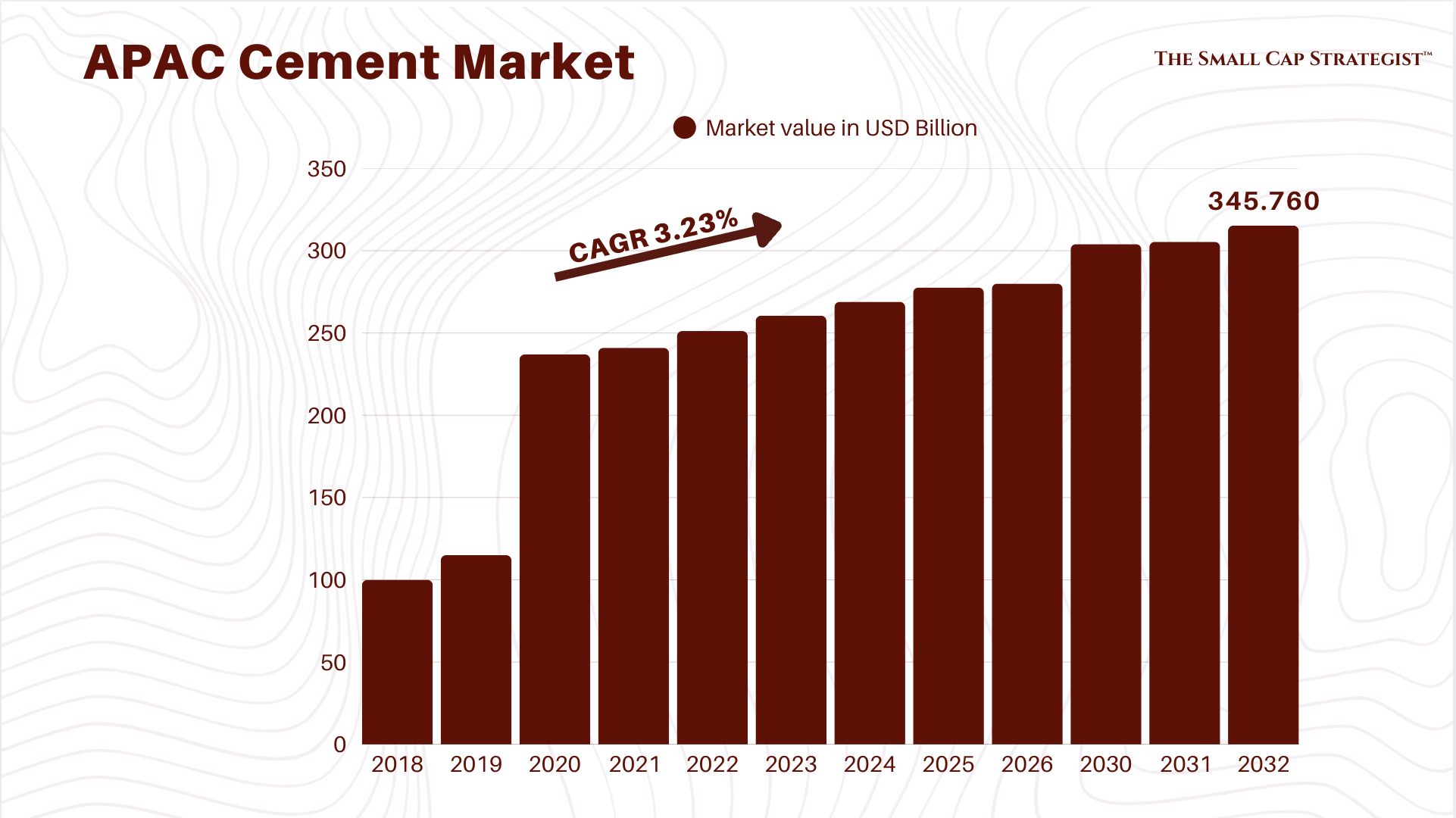

Cement is the binding agent that transforms aggregates into concrete, making it indispensable to modern construction. The APAC cement market was valued at USD 260.55 billion in 2023 and is forecast to grow at a CAGR of 3-6% through 2032. While China is the world's largest producer and consumer by a wide margin, its consumption is largely domestic. In contrast, countries like Vietnam have become major exporters, supplying markets across the region.

The cement business model is defined by high capital and energy intensity. Manufacturing involves heating limestone and other materials to extreme temperatures in large kilns, a process that consumes high amounts of energy. Consequently, success hinges on several factors:

Economies of Scale: Large, modern production plants are necessary to reduce per-ton production costs.

Energy Efficiency: State-of-the-art kiln technology and the use of alternative fuels are critical for managing one of the largest variable costs.

Distribution Networks: As a product that can be transported economically over longer distances than aggregates, cement producers rely on sophisticated, multi-modal logistics networks, utilizing sea, rail, and truck transport to serve broad geographic markets.

The dominant product type in the market is blended cement, where a portion of the energy-intensive clinker is replaced with other materials like fly ash, slag, or limestone. This not only reduces cost but also lowers the carbon footprint of the final product, a key consideration in today's market.

The single most important trend for the cement industry is decarbonization. Cement production is responsible for approximately 7% of global CO2 emissions, making it a primary target for climate regulation and ESG-focused investors. This has started a push to develop and commercialize low-carbon cement. This involves maximizing the use of supplementary cementitious materials (SCMs), exploring novel binders like calcined clay, and investing in long-term solutions like carbon capture, utilization, and storage (CCUS). This trend represents both a significant risk for incumbents slow to adapt and a massive opportunity for innovators.

Steel

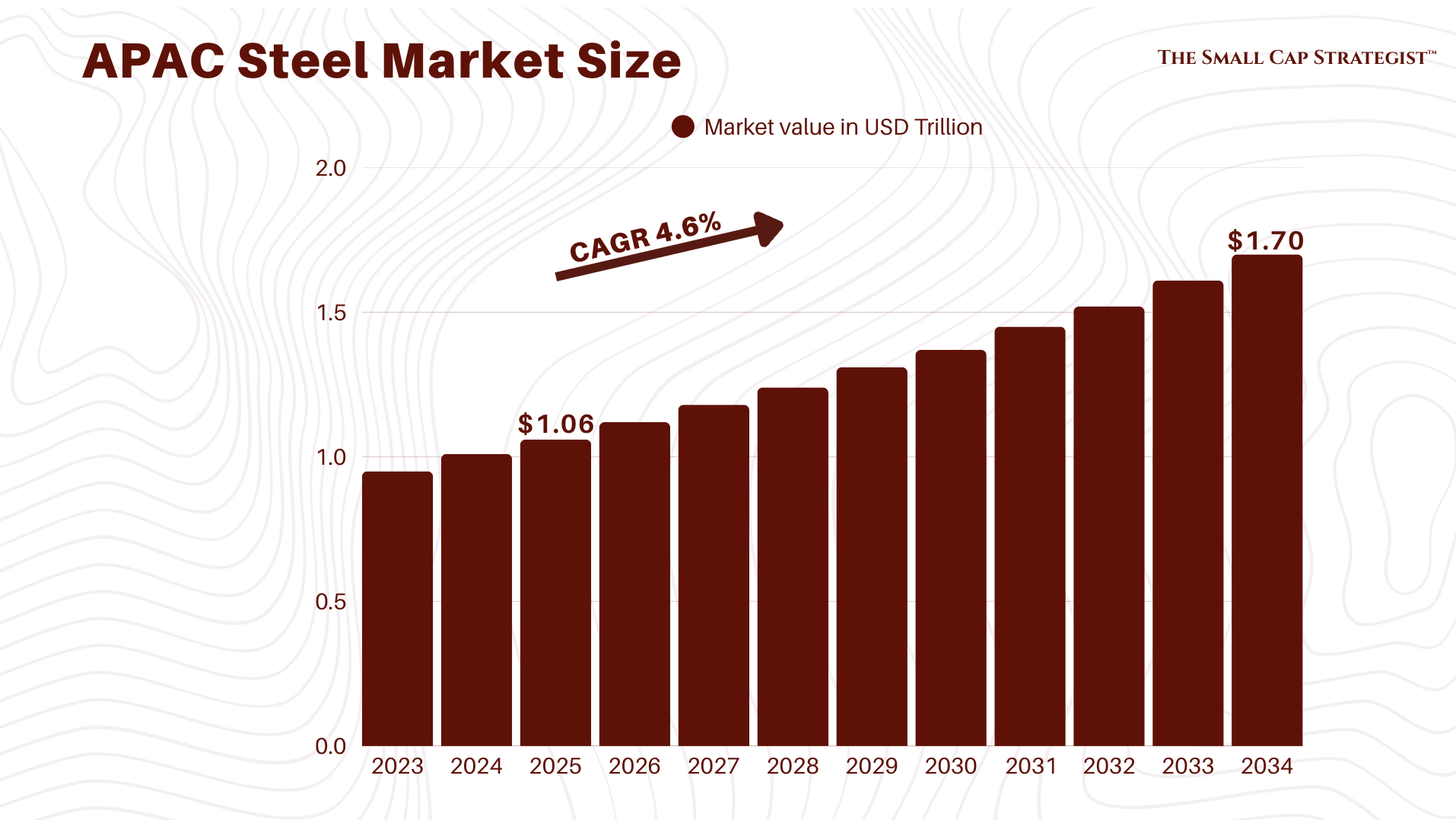

The APAC steel market, valued at USD 1010 billion in 2024, is projected to grow at a CAGR of around 4.6%. The building and construction sector is the largest end-user, accounting for roughly 46% of demand, with the automotive and manufacturing sectors also being significant consumers.

Unlike aggregates, steel is a truly global commodity. Its business model is subject to international price fluctuations, geopolitical trade policies, and high energy costs. Producers focus on operational efficiency in their mills, securing reliable and cost-effective sources of raw materials (iron ore and coking coal), and differentiating their offerings by producing higher-value, specialized products. This includes advanced high-strength steels (AHSS) and ultra-high-strength steels (UHSS) that offer greater strength with less weight, a key demand from both the automotive and construction industries.

Similar to the ESG focus in cement, the steel industry is under immense pressure to decarbonize. The concept of "Green Steel" is gaining momentum, driving investment in alternative production methods. This includes shifting from traditional blast furnaces to electric arc furnaces (EAFs), which can use recycled steel scrap as a primary input, and exploring breakthrough technologies like hydrogen-based direct reduced iron (DRI) to eliminate the use of coal in the steelmaking process.

Value-Added & Downstream Products (Ready-Mix Concrete, Asphalt, Precast)

This segment is the most profitable step in the materials value chain, where basic materials are converted into customized solutions for specific projects. The APAC concrete market alone is a massive opportunity, projected to reach USD 902 billion by 2030.

The business model for downstream products is frequently part of a vertically integrated strategy. Large materials producers forward-integrate to capture more of the value chain. Ready-mix concrete plants are established in urban centers to ensure timely delivery to local construction sites. Asphalt plants are often co-located with aggregate quarries to streamline the supply of the main raw material. This integrated model provides greater control over quality and logistics, enhances supply security, and allows for the capture of margin at multiple points in the value stream.

A key trend in this segment is the shift from product sales to solution selling, or the "servitization" of materials. Customers are increasingly buying an outcome, not just a commodity. This includes services like just-in-time delivery coordinated with project schedules, on-site technical support to ensure proper application, and the development of custom product formulations to meet specific performance requirements (e.g., high-strength concrete for a skyscraper core).

Furthermore, the rise of prefabrication and modular construction is fundamentally changing this segment. By moving construction activities from the job site to a controlled factory environment, modular methods improve quality, reduce waste, and accelerate project delivery. This creates demand for precisely engineered precast concrete components, structural steel frames, and other factory-finished modules, blurring the lines between materials supplier and manufacturer.

To provide a clear investment lens, the distinct characteristics of these sub-sectors are summarized below.

Key Trends Changing Construction

Digitalizing Construction

The construction industry, historically one of the least digitized sectors, is now integrating itself with technology. Faced with challenges like skilled labor shortages and rising costs, companies are using digital tools to improve efficiency, collaboration, and project outcomes.

Several key technologies are at the forefront of this digital shift:

Building Information Modeling (BIM) and Digital Twins: BIM has moved from a niche design tool to a foundational platform for modern construction management. It involves creating a 3D model of a project that is enriched with data. This "digital twin" of the physical asset serves as an accurate project idea for architects, engineers, contractors, and owners. BIM allows for advanced visualization, automated clash detection (identifying where different systems like plumbing and electrical interfere before construction begins), and 5D BIM, which integrates cost and scheduling data directly into the model. This process is managed within a Common Data Environment (CDE), a cloud-based platform that ensures all parties are working from the most current information, drastically reducing errors and rework.

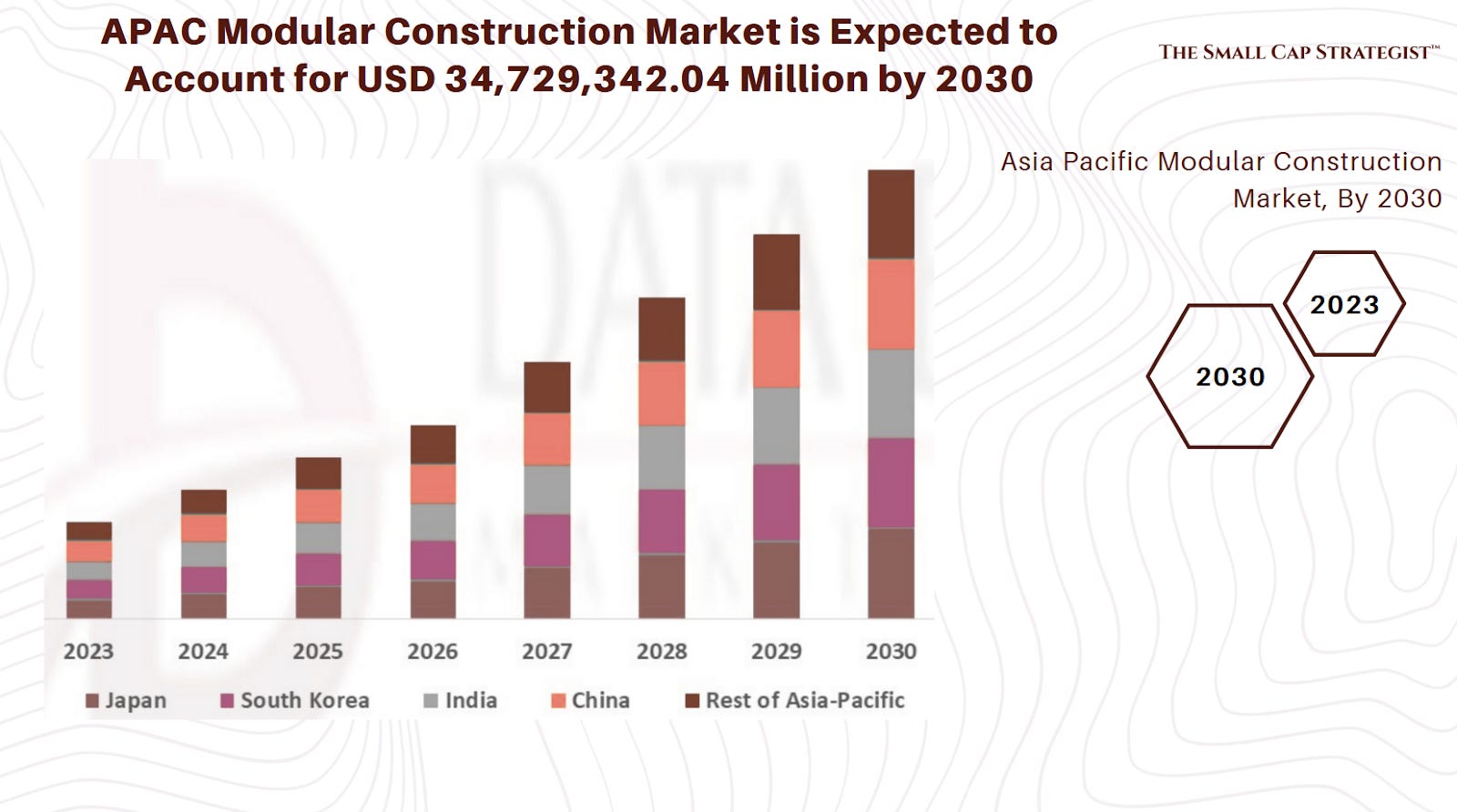

Prefabrication and Modular Construction: This trend, also known as off-site construction, involves manufacturing building components from wall panels to entire rooms in a controlled factory setting before transporting them to the site for assembly. This industrialization of construction offers numerous advantages: it dramatically accelerates project timelines, improves quality control, reduces on-site labor requirements, and minimizes material waste. The APAC modular construction market is a testament to this trend's potential, projected to grow from USD 43 billion in 2025 to USD 71.2 billion by 2032. While adoption faces headwinds in some markets like Australia due to fragmented regulations and initial cost premiums, the long-term efficiency gains are interesting.

3D Printing (Additive Manufacturing): While still an emerging technology, 3D construction printing holds potential. Large-scale printers to extrude materials like concrete layer by layer can create complex architectural forms that are difficult or impossible with traditional methods. More importantly, it offers the promise of near-zero waste, reduced labor, and significantly faster construction speeds. The APAC market for 3D printing in construction is forecast to experience explosive growth, projected to reach USD 1.9 billion by 2030 from a very small base today.

Digital Supply Chains: The logistics of moving vast quantities of heavy materials to job sites is a core challenge. Companies are now deploying digital solutions to manage this complexity. IoT sensors on trucks and equipment, AI-powered logistics platforms for route optimization, and digital procurement systems are being used to improve visibility, track materials in real-time, and ensure just-in-time delivery, reducing on-site congestion and costs.

Technologies like BIM and prefabrication necessitate earlier and deeper collaboration, breaking down the traditional, sequential silos between design, material supply, and construction. For a modular builder to be effective, they must be involved in the initial design phase to ensure components are optimized for factory production. The factory itself becomes a critical node in the supply chain. A comprehensive BIM model requires simultaneous data input from architects, structural engineers, MEP (mechanical, electrical, plumbing) engineers, and material suppliers. This inherently favors companies with more integrated business models that can manage these more complex workflows. It also creates opportunities for new, platform-based businesses that act as the digital connective tissue for the entire project ecosystem. Companies that fail to adapt and remain as simple, disconnected commodity suppliers risk being marginalized, as their products become just one interchangeable element in a much more sophisticated, digitally managed value chain.

Evolving Business Models

Sustainability and digital trends are forcing construction materials companies to completely change how they do business. The traditional approach of simply extracting, producing, and selling a physical product is no longer sufficient for long-term success. The most successful players are evolving to offer more integrated, service-oriented, and sustainable solutions.

The vertically integrated model remains the dominant and most proven strategy for large-scale players. As demonstrated by global giants like CRH and Holcim, US leaders like Vulcan Materials and Martin Marietta, and the Chinese SOEs, controlling the value chain from the quarry to the construction site provides immense strategic advantages. By owning the upstream resources (aggregates), the midstream production facilities (cement, asphalt), and the downstream service capabilities (ready-mix delivery, paving), these companies can control costs, ensure security of supply, manage quality, and capture margin at multiple points. This model creates a significant competitive moat that is difficult for smaller competitors to replicate.

However, alongside this dominant model, several innovative approaches are emerging, particularly among more agile players:

Servitization (XaaS - Anything-as-a-Service): This model shifts the focus from selling a product to selling a complete solution or an outcome. A well-known example from an adjacent industry is Hilti, which offers tool fleet management as a service rather than just selling power tools. In the materials space, this could manifest as "Concrete-as-a-Service," where a supplier contracts to provide a guaranteed volume of concrete meeting specific performance criteria, delivered on a precise schedule, and manages the entire logistics and quality control process for a comprehensive fee. This model builds deeper, stickier customer relationships and moves the supplier up the value chain from a simple vendor to a critical project partner.

Circular Business Models: Driven by the sustainability trend, a new class of companies is emerging whose entire business is built on the principles of the circular economy. These firms specialize in "urban mining"—collecting, processing, and re-manufacturing construction and demolition waste into valuable new materials, such as recycled aggregates, reclaimed wood, or recycled plastic composites. This model not only addresses pressing environmental challenges like resource scarcity and landfill waste but also creates a new and often cost-competitive source of raw materials located directly within urban demand centers.

Platform and Digital Marketplaces: The rise of e-commerce is finally reaching the construction industry. New online platforms and marketplaces are being developed to connect material buyers—especially small-to-medium-sized contractors—directly with a wide range of suppliers. These digital platforms can bypass traditional, multi-layered distribution channels, offering greater price transparency, wider selection, and more efficient procurement. This is particularly disruptive in the fragmented, non-institutional segment of the market.

Investment Guidance - Regional Analysis & Small/Mid-Cap Ideas

China Market Overview

China remains, by far, the world's largest construction market, with an industry value of USD 1.3 trillion and a robust growth rate of 7.2%. For decades, its growth was fueled by an unprecedented pace of urbanization and massive-scale infrastructure development. While these drivers remain potent, the strategic focus of the Chinese government and construction industry is undergoing a significant pivot. The new emphasis is on higher-quality development, sustainability, and the adoption of advanced technologies. This is reflected in the strong push for green buildings, which accounted for 65% of new urban construction in 2023, and the increasing use of prefabrication and advanced materials like high-performance concrete and smart glass. The Belt and Road Initiative (BRI) also continues to serve as a powerful engine for demand, creating export markets for Chinese materials and engineering services across Asia and beyond.

Investment Thesis

The most compelling investment opportunities in China are no longer in pure-play commodity producers focused solely on volume. Instead, the focus should be on companies that are aligned with the government's strategic pivot towards "green development" and high-tech construction. This includes niche specialists in new materials, environmental protection technologies (e.g., waste-to-energy, water treatment), and digital construction solutions. It also includes established players who are demonstrating a successful transition to higher-value, more sustainable business models.

India: The World's Next Great Construction Boom

Market Overview:

India stands at the brink of a multi-decade construction boom. The country's construction materials market is projected to nearly double in size, from approximately USD 41 billion in 2024 to USD 77 billion by 2035, expanding at a CAGR of nearly 6%. This explosive growth is underpinned by powerful, non-negotiable demographic and economic forces. Rapid urbanization is expected to swell India's city-dwelling population to 600 million by 2031, creating immense demand for housing. This is being met by ambitious government initiatives like the "Smart Cities Mission" and "Housing for All," which aim to build 20 million new homes. Furthermore, a burgeoning middle class with rising disposable income is fueling demand for both residential and commercial real estate.

Investment Thesis:

Given the sheer scale of domestic demand, a broad-based exposure to Indian-focused materials producers is a powerful investment thesis. Companies in the core segments of cement and aggregates are particularly well-positioned to benefit from the direct demand created by infrastructure and housing projects. As the market matures, there will also be growing opportunities for companies that enable greater efficiency, sustainability, and value-added services.

’

Japan & South Korea: Leaders in Technology, Sustainability, and Value-Added Materials

Market Overview

Japan and South Korea represent the technologically advanced and mature end of the APAC construction spectrum. While overall growth is more modest than in emerging Asia, these markets are defined by high-value activities. Japan's construction materials market is forecast to grow at a CAGR of approximately 4.8%, driven by major infrastructure renewal projects (including preparations for the 2025 World Expo), the constant need for seismically resilient structures, and a strong regulatory push for sustainability. Similarly, South Korea's market is expected to grow at a CAGR of around 4.7%, fueled by large-scale government infrastructure spending, urban regeneration projects, and a focus on high-tech, eco-friendly building practices.

Investment Thesis

The optimal investment strategy in these mature markets is to focus on technological leaders and niche specialists. This includes companies at the forefront of developing high-performance materials (e.g., for earthquake-proofing, advanced insulation, lightweight composites), firms that are leaders in green innovation and circular economy solutions, and providers of advanced digital construction technologies.

Australia

Market Overview

Australia is a developed and stable construction market, with industry output forecast to grow at an average annual rate of 2.8% between 2025 and 2027. The market is driven by three key factors: significant government investment in transport and social infrastructure, a resilient residential housing market, and a strong and accelerating push towards sustainability and modern methods of construction. There is a particular emphasis on adopting prefabricated and modular building systems to address labor shortages and improve efficiency, although challenges in regulation and cost remain.

Investment Thesis

In this mature market, the best opportunities lie with companies that are aligned with the future of construction. This means focusing on firms specializing in sustainable and recycled materials, leaders in prefabricated and modular systems, and service providers that cater to the needs of the large-scale infrastructure and residential sectors. The recent acquisition of Adbri by CRH exemplifies the ongoing consolidation trend and highlights the value inherent in integrated domestic material suppliers.

ASEAN (Indonesia, Vietnam, Malaysia, Thailand, Philippines): The High-Growth Frontier

Market Overview

The Association of Southeast Asian Nations (ASEAN) is a dynamic and diverse region that represents the high-growth frontier of the global construction industry.

Indonesia: Growth is driven by rapid urbanization, a rising middle class, and major government infrastructure investment, including the development of the new capital, Nusantara.

Vietnam: The market is experiencing a boom fueled by strong economic growth, significant foreign direct investment (FDI) in manufacturing, and rapid urbanization in cities like Hanoi and Ho Chi Minh City.

Malaysia: The construction sector is supported by ongoing infrastructure projects, such as the Kuala Lumpur-Singapore High-Speed Rail, and an increasing focus on sustainable development.

Thailand: A mature but steady market led by major domestic players like Siam Cement Group (SCG), with growth driven by infrastructure, commercial, and tourism-related projects.

Philippines: Demand is strong, powered by the government's ambitious infrastructure programs and a significant housing backlog.

Investment Thesis

The ASEAN region offers the highest potential for top-line growth. The primary investment strategy is to identify the leading local players in core materials segments (cement, aggregates, steel) and construction services. These "national champions" are best positioned with the local knowledge, distribution networks, and political relationships to capture the immense growth driven by the region's development.

Investment Thesis for the APAC Materials Sector

Recap of the Four Core Investment Theses

Four overarching themes emerge as critical frameworks for identifying value and potential outperformance in the APAC construction materials market:

Consolidation: The industry is structurally geared for consolidation. The fragmented nature of the market, particularly in aggregates and downstream products, creates a continuous pipeline of M&A opportunities for large, well-capitalized players. From an investment standpoint, this means that well-managed small and mid-cap companies with strong regional positions or unique assets are not only organic growth stories but also potential acquisition targets that can deliver significant premiums.

Green Premium: Sustainability is no longer a peripheral concern but a core driver of competitive advantage. Companies that are leaders in developing and marketing low-carbon products (like green cement), recycled materials, and other sustainable solutions are building a durable economic moat. They can command higher prices, win preferential contracts, and attract ESG-focused capital, creating a new basis for market leadership.

Digital: The construction industry's digital transformation is accelerating. Firms that successfully adopt and integrate technologies like Building Information Modeling (BIM), prefabrication, and digital supply chain management will unlock significant efficiencies, reduce costs, and improve project outcomes. This technological proficiency will be a key differentiator, separating the most profitable and resilient companies from the laggards.

Niche Specialists: While global giants compete on scale, smaller players can thrive by dominating a specific product or geographic niche. A company that is the undisputed leader in a specialized material (e.g., high-performance composites, architectural finishes) or the most efficient operator in a contained regional market can generate superior returns and become an attractive, strategic asset.

Framework for Evaluation

Geographic Exposure: Where does the company operate? Is it positioned in a high-growth emerging market like India or Vietnam, where the primary driver is volume? Or is it in a high-value mature market like Japan or South Korea, where the drivers are technology and innovation?

Position in the Value Chain: What does the company actually do? Is it an upstream aggregates producer whose moat is its land assets? A midstream cement or steel giant competing on scale and efficiency? Or a downstream service provider whose value lies in customer relationships and integrated solutions?

Business Model: How does the company compete? Is it a low-cost, high-volume commodity producer? A vertically integrated player capturing margin at multiple stages? Or an innovator pioneering a new model based on servitization, circularity, or digital platforms?

Sustainability & Technology Adoption: Where does the company stand on the two most important transformative trends? Is it a leader in green materials and digital construction, investing in R&D and building a "green moat"? Or is it a laggard at risk of being left behind by new regulations and market demands?

Final Word

The Asia-Pacific construction materials sector represents one of the most powerful and durable secular growth stories available to investors today. The sheer scale of the region's needs provides a level of demand certainty that is rare in the global economy. While the industry faces challenges, including cyclical economic pressures, logistical complexities, and the urgent need to decarbonize, these challenges also create opportunities. The companies that can survive this environment successfully are positioned for substantial and sustained value creation. The blueprint for building a successful portfolio is clear.

Thank you for reading The Small Cap Strategist, if you enjoyed this post consider subscribing.

This post is for informational and educational purposes only and should not be considered investment advice. The author is not a financial advisor. All investment decisions carry risk, and readers should consult with a qualified financial professional before making any investment choices. The author may or may not hold positions in the securities discussed.