Stock Pitch #7 They Secured the Permits. We Secure the 110% Return, Perpetua Resources (NASDAQ:PPTA)

Stop Chasing Noise. This is a Simple, De-Risked Trade With a Massive, Quantifiable Upside. PPTA is on its Way to $28.50 Target.

About a month ago I had a discussion with a friend where we came to an agreement and expected a short-term correction in the gold market as gold had become overbought and investor sentiment had become elevated during the spike in gold to $3,500 per ounce.

I am pleased to report that much progress has been made over the last five weeks. Gold’s Daily Sentiment Index (DSI) has dropped from the very elevated level of 88% bullish around the beginning of April, to a more neutral 66% on Friday (silver DSI at 65%).

While May was the first down month for gold this year, gold is still up 25.3% year-to-date – greatly exceeding the flat-to-down moves in the major market indexes. Gold’s Relative Strength Index (RSI) dropped from over 70% (where corrections typically occur) to around the 50% level from which rallies have begun all throughout this year. Gold’s MACD (Moving Average Convergence Divergence), a popular momentum indicator, has fallen from the extreme +100 level into negative numbers – again where rallies typically begin. Gold is clearly no longer overbought, short-term.

Another positive has been the action in the gold mining stocks during the five-week correction. The miners had been significantly lagging gold, but that has now changed. Over the five weeks since gold’s top on April 22, the GDX ETF of major gold miners has gained 0.8% (and has soared 49.4% year-to-date). Over that same period, the GDXJ ETF (smaller miners) has added an additional 4.3% and is up a whopping 52.8% on the year. Wesdome, a GDXJ component, on Thursday hit an all-time high ($13.72) and is currently up 49% on the year. New Gold, another GDXJ component, hit its highest-level last week ($4.48) since September of 2016 and is up 79.4% year-to-date. The intermediate miners and some of the junior developers are beginning to perk up – a healthy sign for the sector.

While the gold correction could continue a bit longer, it is also now possible that we’ve begun another leg up in this great secular bull market. At some point, we’ll head into a blow-off phase, which has become more likely now that the mining stocks have begun to outperform. As I’ve pointed out in the past, North American buyers, mostly absent from the precious metals markets up to this point, are the primary purchasers of mining stocks. If North Americans start piling into the sector in earnest, joining the overseas buyers who have propelled the gold price higher for several years, we’ll have all the ingredients for a parabolic blow-off. This constructive macro environment provides the ideal backdrop for identifying deeply undervalued, high-quality developers that are poised for a significant re-rating. Perpetua Resources (PPTA) is precisely such a company.

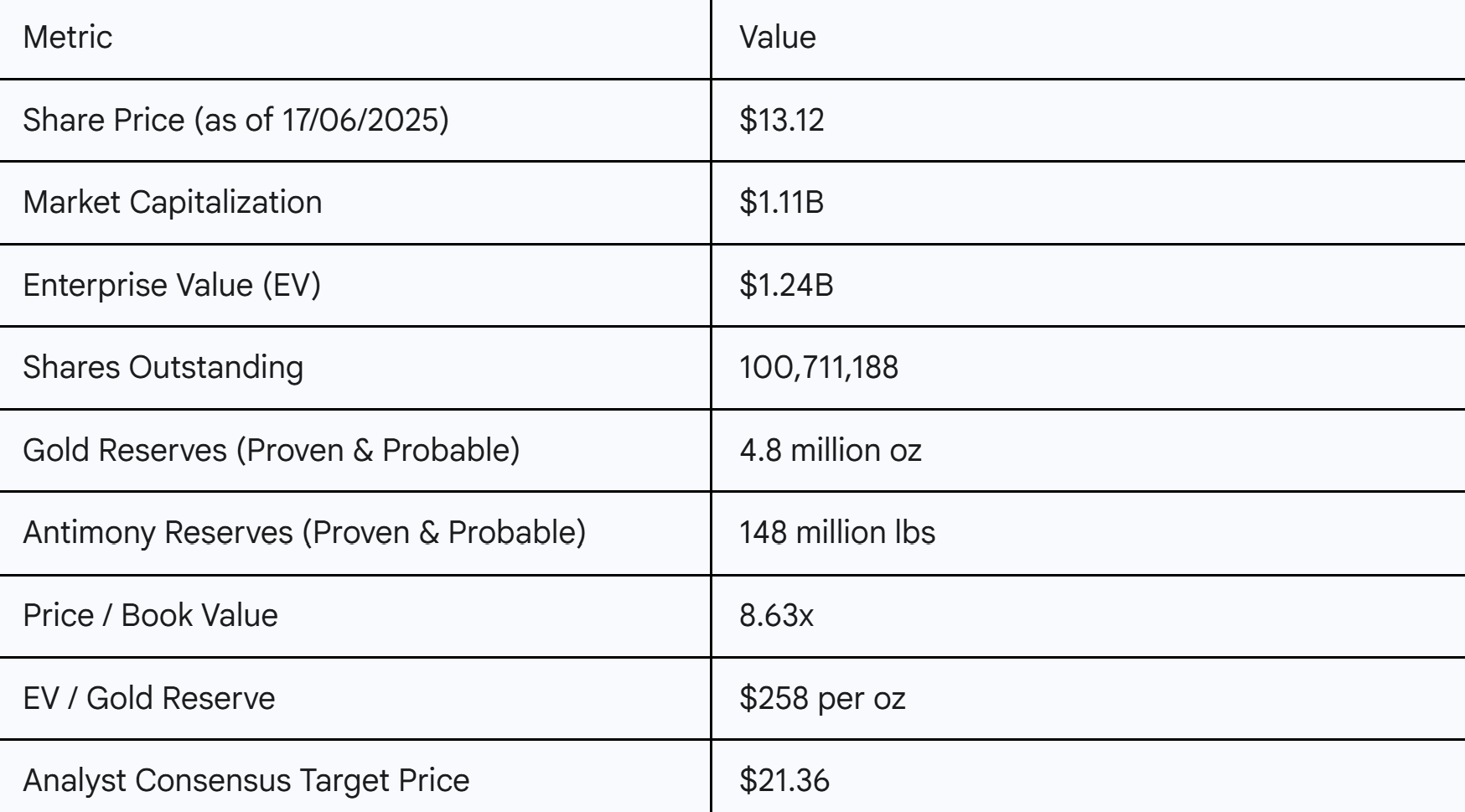

Recommendation & Key Metrics

Recommendation: BUY

Price Target: $28.50

Perpetua Resources represents a rare convergence of a world-class mineral asset, a critical strategic advantage, major de-risking milestones, and a valuation that has yet to reflect these realities. The company is very close to transitioning from a developer to a fully funded, construction-ready producer. As a pre-production company, conventional valuation metrics such as Price-to-Earnings (P/E) or Enterprise Value to EBITDA are not applicable, as reflected by the "NM" (Not Meaningful) figures in its financial summaries (which we will explore later in this post).

Instead, the market values developers based on the quality of their assets and their progress along the de-risking pathway toward production. The key metrics are those that compare the company's market value to the intrinsic value of its mineral reserves and the economic potential outlined in its technical studies. The recent achievement of final federal permits for its Stibnite Gold Project is the single most important de-risking event in the company's history, yet the market has been slow to fully appreciate its significance. This creates a compelling opportunity.

Investment Thesis

Strengths

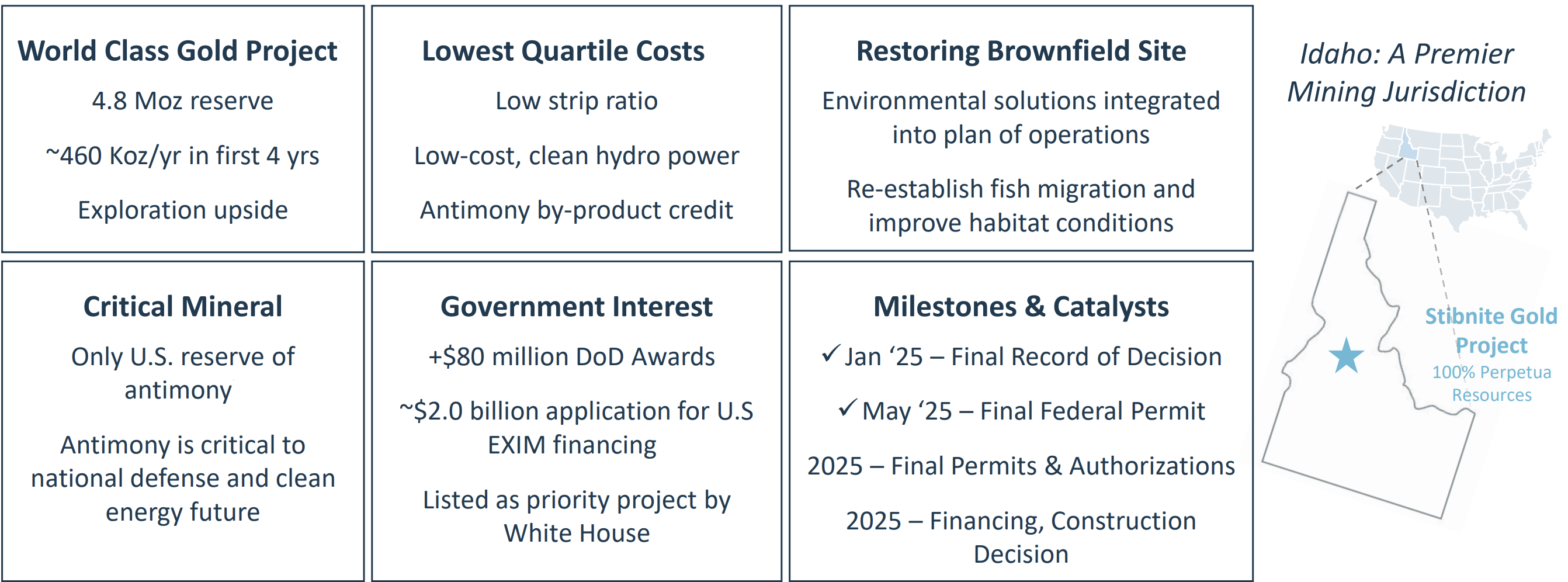

World-Class Asset: The Stibnite Gold Project is not just another gold deposit. It is one of the highest-grade open-pit gold projects in the United States, boasting a reserve of 4.8 million ounces of gold. The project's economics are exceptional, with a projected All-In Sustaining Cost (AISC) below $760 per ounce over the life of the mine and a remarkable ~$435 per ounce in the first four years of production. This places Stibnite squarely in the first quartile of the global cost curve, ensuring high margins even in lower gold price environments.

Strategic Antimony Co-Product: Stibnite’s most unique feature is its large antimony reserve, estimated at 148 million pounds. It is the only identified domestic reserve of antimony in the United States, a mineral officially designated as critical to national defense and the clean energy transition. This is not just a by-product credit; it is a strategic asset that provides a geopolitical moat and significant economic leverage, a point we will explore in detail.

Permitting Milestone Achieved: After a grueling eight-year federal review process, Perpetua has secured its final major federal permits: the Final Record of Decision (ROD) from the U.S. Forest Service and the Clean Water Act (CWA) Section 404 permit from the Army Corps of Engineers. This achievement cannot be overstated. Permitting is the single greatest hurdle for any mining project in a Tier-1 jurisdiction, and its completion removes the largest element of risk from the investment thesis.

Tier-1 Jurisdiction & Unwavering Government Support: The project is located in Idaho, a state with a long history of mining and a favorable operating environment. More importantly, the project has garnered explicit support from the U.S. government. It was selected as a "Transparency Project" by the White House and has been awarded multiple rounds of funding from the Department of Defense, totaling over $75 million, to advance studies on producing military-specification antimony trisulfide. This level of federal backing is exceptionally rare and underscores the project's strategic importance.

Weaknesses

Single-Asset Concentration: Perpetua's fortunes are entirely tied to the successful development and operation of the Stibnite project. Any project-specific setbacks would have an outsized impact on the company's valuation.

Significant Initial CAPEX: The February 2025 financial update pegs the initial capital expenditure at $2.2 billion. While the company has a clear and viable path to funding this, it is a substantial figure that introduces financing and execution risk.

Future Shareholder Dilution: The recently closed $425 million financing was a critical and well-executed step toward funding the equity portion of the CAPEX. However, the sheer scale of the project means that potential cost overruns or changes to the financing structure could necessitate further equity raises, leading to dilution for existing shareholders.

Opportunities

Commodity Price Leverage: The project's Net Present Value (NPV) is highly sensitive to the prices of both gold and antimony. The February 2025 update demonstrated a robust $1.4 billion after-tax NPV using conservative consensus prices ($2,100/oz gold, $10/lb antimony), which skyrockets to $3.7 billion at spot prices ($2,900/oz gold, $21/lb antimony). With many analysts calling for gold to move toward $4,000/oz and the antimony market in a severe supply squeeze, the potential for further upside to the project's intrinsic value is immense.

Financing Package Completion: The company has formally applied for up to $2 billion in debt financing from the Export-Import Bank of the U.S. (EXIM). Securing this loan, which would be the final piece of the funding puzzle, would fully de-risk the project from a financing perspective and act as a powerful catalyst for a stock re-rating.

Resource Expansion: The Stibnite deposit remains open for exploration, presenting a clear opportunity to grow the mineral resource and reserve base over time. This could extend the mine's life and further enhance the project's overall value.

Threats

Construction & Execution Risk: Building a mine of this scale is a complex undertaking. The project is exposed to the risks of construction delays, labor shortages, and equipment procurement challenges, all of which could impact timelines and budgets.

Legal & Activist Challenges: Despite receiving the final federal permits, large-scale mining projects in the U.S. are often the target of legal challenges from environmental and anti-mining groups. While the project's strong local and federal support mitigates this risk, lawsuits could still cause costly delays.

Inflationary Pressures: The project's capital cost estimate of $2.2 billion is based on Q4 2024 pricing. Persistent inflationary pressures in labor and materials could lead to an increase in the final capital cost, potentially requiring additional funding.

The Asset: Stibnite Gold Project

Operational Overview

The Stibnite Gold Project is fundamentally different from a typical "greenfield" development. It is located on a "brownfield" site, an area that was heavily mined for antimony and tungsten during World War II and the Korean War and subsequently abandoned, leaving behind significant environmental legacies. These legacies include 10.5 million tons of unlined, legacy tailings and spent ore that interact with ground and surface water, and a river (the East Fork of the South Fork of the Salmon River) that flows directly into an old mine pit, blocking fish passage.

Perpetua's plan of operations is ingeniously designed to use the proceeds from a modern, large-scale mining operation to fund a comprehensive environmental restoration of the entire district. This is not a token effort; it is central to the project's design and approval. The plan includes picking up, reprocessing, and safely storing the legacy waste in a state-of-the-art, fully lined tailings storage facility (TSF). A key feature is the restoration of the river to its natural channel, reopening miles of critical spawning habitat for salmon and steelhead that have been blocked for over 80 years.

This "restoration mining" model has proven to be a powerful narrative and a significant competitive advantage. It has been instrumental in garnering overwhelming support, evidenced by the more than 23,000 letters submitted in favor of the project during public comment periods. In an investment climate where Environmental, Social, and Governance (ESG) factors are paramount for securing capital and social license to operate, Perpetua's plan transforms a potential liability into a core strength. The company is not just proposing a mine; it is proposing a privately funded environmental cleanup of a historic industrial site, a solution that has resonated powerfully with local communities, the state of Idaho, and the federal government.

Project Economics & Profitability

The core of the investment thesis lies in the project's exceptional economics, which were updated in the February 2025 Financial Update based on basic engineering work. This update confirmed Stibnite's status as a world-class asset with a rare combination of large scale, high margin, and rapid payback potential.

The table below summarizes the key projections, showcasing both the immense potential in the current commodity price environment and the project's resilience at more conservative, long-term consensus prices.

The numbers are compelling. An after-tax NPV of $3.7 billion at recent spot prices demonstrates the project's ability to generate massive shareholder value. The 27.1% IRR at that price deck is robust for a project of this scale. Even more impressive is the project's profitability at lower prices; an IRR of 15.4% at $2,100 gold ensures the project remains economically viable and attractive through commodity cycles.

Cost Structure Analysis: The Antimony Advantage

The key to Stibnite's exceptional profitability is its remarkably low All-In Sustaining Cost, which is driven primarily by the significant by-product credit from its antimony production. The AISC of $435/oz during the first four years is world-class and would make Stibnite one of the most profitable gold mines on the planet upon entering production.

This creates a powerful flywheel effect for the project's economics. The February 2025 update used a spot price of $21.00/lb for antimony. However, the market for antimony has tightened considerably since then. Due to supply disruptions and China's export ban to the U.S., prices have surged. Reports from Q1 2025 showed prices in the U.S. reaching $34,500/MT (approximately $15.65/lb), while some European spot quotes have climbed as high as $51,500 per ton (approximately $23.35/lb). Every dollar increase in the realized price of antimony directly lowers the effective cost of producing an ounce of gold. This means the project's economics are likely even more stronger today than what was presented in the already stellar February update.

Production Profile: High-Grade Starter Pit

The mine plan has been intelligently sequenced to maximize early cash flow and de-risk the project financially. Operations will commence in a high-grade starter pit, which is projected to produce an average of approximately 463,000 ounces of gold per year for the first four years. This front-loading of production, combined with the low AISC during this period, allows the company to achieve an exceptionally rapid payback of its initial capital investment—just 2.2 years at spot prices. This strategy will generate substantial free cash flow early in the mine life, reducing or eliminating the need to tap capital markets for future sustaining capital and allowing the company to self-fund future growth.

Industry Context & Competitive Positioning

Industry Overview

Perpetua Resources is positioned at the meeting point of two powerful, independent bull markets: one in precious metals and one in strategic critical minerals.

The Gold Market

The macro case for gold remains firmly bullish. The recent correction has been a healthy consolidation within a major secular uptrend. Leading financial institutions are forecasting significantly higher prices. J.P. Morgan Research, for instance, expects gold to average $3,675/oz by the fourth quarter of 2025 and climb toward $4,000/oz by mid-2026, citing continued strong demand from central banks and investors seeking a hedge against stagflation and policy risks. Similarly, Goldman Sachs Research raised its year-end 2025 forecast to $3,700/oz, with a potential for $3,880/oz in a recessionary scenario, driven by central bank buying and ETF inflows. This backdrop of rising prices provides a powerful tailwind for all gold producers, but especially for developers like Perpetua whose project economics are highly leveraged to the gold price.

The Antimony Market

The market for antimony is even more compelling, characterized by a structural supply deficit and geopolitically-driven price appreciation. Over 90% of the world's mined antimony is controlled by China, Russia, and Tajikistan. In late 2024, China, which accounts for nearly half of global production, banned all exports of antimony products to the U.S., effectively weaponizing its control over this critical mineral.12

This has created a crisis for U.S. supply chains. Antimony is non-replaceable in its primary military application: as a key component in the primer for hundreds of types of munitions. It is also essential for a growing number of clean energy technologies. Perpetua has already signed a supply agreement with Ambri, a U.S.-based company developing liquid metal batteries for grid-scale energy storage.

The combination of inelastic demand and a severe supply shock has caused antimony prices to skyrocket. Prices in Europe climbed over 75% from 2023 levels, and recent quotes suggest the rally is ongoing. This dynamic makes Perpetua's Stibnite project, as the only domestic source, an asset of immense strategic value to the United States. The antimony is not just a kicker; it's a core part of the thesis that provides a unique and durable competitive advantage.

Porter, Competition, and Competitive Advantage

Threat of New Entrants: Very Low. The barriers to entry in the mining industry are immense. It requires discovering a world-class mineral deposit, which is exceedingly rare, followed by a multi-year, capital-intensive process of drilling, engineering, and permitting. Perpetua has already spent over eight years and hundreds of millions of dollars to clear these hurdles.

Bargaining Power of Buyers: Low. For gold, the market is global and liquid; Perpetua will be a price taker at the prevailing spot price. For antimony, the situation is reversed. Given the critical domestic shortage and lack of substitutes, buyers such as the Department of Defense and strategic industrial partners will have limited bargaining power, likely affording Perpetua premium pricing for its U.S.-sourced material.

Bargaining Power of Suppliers: High. The mining industry relies on a concentrated group of specialized engineering firms (like Ausenco, who worked on the Stibnite update), equipment manufacturers (like Caterpillar and Komatsu), and skilled labor. This gives suppliers significant pricing power, which manifests as a risk of capital cost inflation.

Threat of Substitutes: Very Low. There is no financial or industrial substitute for physical gold as a monetary asset and store of value. For its key defense applications, antimony trisulfide is considered essential and non-replaceable.

Rivalry Among Existing Competitors: High, but Differentiated. The gold development space is crowded. However, very few competitors can match Perpetua's unique combination of advantages. Stibnite stands apart due to its high grade, low-cost profile, advanced permitted status, Tier-1 jurisdiction, and, most importantly, its strategic antimony co-product.

Key Competitors & Peer Comparison

To quantify Perpetua's relative value, it is essential to compare it to other North American gold developers at a similar stage. The table below analyzes Perpetua against its peers, focusing on project quality and valuation. For this analysis, we use Enterprise Value per ounce of gold equivalent (AuEq) reserves, a key metric for valuing developers.

The peer comparison reveals several critical points. While developers like Troilus, First Mining, and Liberty Gold appear cheaper on an EV/oz basis, their projects are at an earlier stage (FS or PFS) and lack the final permits that Perpetua has secured. Integra Resources, also in Idaho, has a smaller project with a much lower NPV.

Perpetua's EV/oz of $234 reflects a market that is beginning to price in its advanced, de-risked status but has not yet assigned it a valuation close to its intrinsic NPV. The massive disconnect between its EV ($1.24B) and its spot-price NPV ($3.7B) is the central valuation opportunity. As the company moves toward a construction decision, its valuation multiple should expand significantly, closing this gap.

Sustainable Competitive Advantage (Economic Moat)

Perpetua's economic moat is not based on a brand or network effect, but on a powerful and durable combination of three factors:

Geological Rarity: The Stibnite deposit is a world-class orebody. Its combination of high grade, large scale, and suitability for low-cost open-pit mining is exceptionally rare. You cannot replicate a deposit like this; you can only find one.

The Permitting Barrier: The company has successfully dealt with the complex, multi-year U.S. federal permitting process. This permit is now an asset in itself—a barrier to entry that has been built over eight years and hundreds of millions of dollars in expenditures, which a competitor cannot easily or quickly overcome.

The Strategic Antimony Moat: The project's status as the only domestic source of a critical, non-substitutable defense mineral provides a unique geopolitical and economic advantage. This has garnered direct government support and funding, and it insulates the project's economics via a valuable by-product credit that no pure gold peer can replicate.

Management, Ownership, and Production

Strong Management

A world-class asset requires a world-class team to build it. Perpetua has assembled a management team with precisely the right experience for this critical phase of development.

Jon Cherry, President & CEO: Appointed in March 2024, Jon Cherry is a seasoned mining executive with over 33 years of experience, specializing in project development and permitting in the United States. His resume is a perfect fit for Perpetua's current needs. He previously served as Chairman, President, and CEO of PolyMet Mining, where he led the NorthMet project through the U.S. permitting process, achieving the highest rating ever given to a mining project by the EPA. Before that, he spent over 20 years at Rio Tinto, where he was the general manager responsible for permitting and developing the Eagle Mine in Michigan—the only primary nickel-copper mine in the U.S.. His direct, hands-on experience in successfully permitting and advancing complex mining projects in the U.S. is invaluable and provides a high degree of confidence in his ability to lead Stibnite through construction.

Jessica Largent, CFO: Jessica Largent brings over 15 years of mining industry finance experience from senior roles at major producers Newmont and Rio Tinto. As Vice President of Investor Relations at Newmont, she was responsible for strategy and relationships with shareholders and analysts. This experience in financial reporting, strategic planning, and capital markets is crucial for managing the complex financing package required for Stibnite.

The strength of this team is not theoretical. Their recent execution of the upsized $425 million equity financing (June17th 2025), which involved a syndicate of major banks and was anchored by a sophisticated resource investor, demonstrates their capability and credibility within capital markets. This was a critical step in de-risking the project's funding path.

Management Ownership and Director Dealings

The shareholder registry provides one of the strongest votes of confidence in the project. Paulson & Co. Inc., a highly respected and sophisticated resource-focused investment fund, is the company's largest shareholder. Prior to the recent financing, they held approximately 45% of the company's shares. Crucially, they did not sell into the offering; instead, they anchored it by making an additional $100 million investment via a concurrent private placement. Following the financing, Paulson holds approximately 31% of the outstanding shares, a massive position that aligns them directly with common shareholders.

The presence of other well-known resource investors like Sprott Inc. and Encompass Capital Advisors LLC further validates the investment thesis. While there has been some minor insider selling by officers over the last year, this is typical for executives managing their personal finances and exercising stock options, and it is dwarfed by the scale of Paulson's continued investment.

Catalyst Re-Rating

Investing in a development-stage company is about investing along a de-risking curve. With federal permits and a significant portion of equity financing now secured, Perpetua has a clear roadmap of upcoming catalysts that should continue to unlock value and drive a re-rating of the stock.

The final, transformative catalyst. Closing the up to $2B loan would fully fund the project and remove all financing overhang.

Each of these milestones represents a significant step in reducing the project's remaining risk profile. As each catalyst is achieved, the market should become more willing to value Perpetua based on the intrinsic net asset value of the Stibnite project, rather than applying a steep discount for development uncertainty.

Valuation, Reverse Thesis, and Conclusion

Valuation & Safety

The valuation case for Perpetua Resources is straightforward and compelling. It is based on the significant disconnect between its current market valuation and the intrinsic economic value of its now-permitted Stibnite Gold Project. The standard valuation methodology for a developer is a Net Asset Value (NAV) approach.

As of the February 2025 Financial Update, the Stibnite project has an after-tax Net Present Value (using a 5% discount rate) of $3.7 billion at recent spot prices. The company's current Enterprise Value is approximately $1.24 billion. This means Perpetua is trading at a Price-to-NAV (P/NAV) multiple of just 0.33x.

This discount reflects the market's pricing of the remaining risks: financing, construction, and execution. However, with federal permits secured and a clear path to full funding, this discount is excessive. As the company achieves the final catalysts outlined in the roadmap—particularly the closing of the EXIM debt facility—its P/NAV multiple should expand toward the 0.7x to 1.0x range, which is more appropriate for a fully funded, permitted project in a Tier-1 jurisdiction entering construction.

A re-rating to just 0.75x of the spot NPV would imply an enterprise value of ~$2.78 billion, or a share price of approximately $27.50, representing a 110% return from the current price. This target does not account for any further increases in gold or antimony prices, which would drive the NPV even higher. The project's robust economics at lower commodity prices—with an NPV of $1.4 billion at consensus prices—provides a substantial margin of safety, suggesting the company is worth more than its current EV even in a more conservative scenario.

What Could Go Wrong?

To maintain a balanced view, it is crucial to consider the risks that could invalidate the thesis.

Major Cost Blowout: The $2.2 billion CAPEX estimate is based on Q4 2024 data. If severe, unanticipated inflation or major construction issues cause the final cost to escalate dramatically, it could necessitate a large, highly dilutive equity financing that would impair shareholder returns.

Financing Failure: The entire plan hinges on securing the large debt facility from EXIM. While the project's strategic nature and government support make approval likely, a failure to secure this loan or securing it for a much smaller amount would create a massive funding gap and jeopardize the project's development timeline.

Commodity Price Crash: While the project is economic at lower prices, a severe and prolonged bear market in both gold and antimony would compress margins, reduce the NPV, and negatively impact investor sentiment and the company's ability to service its debt.

Successful Legal Challenge: The risk of legal challenges from anti-mining groups, while mitigated, has not been eliminated. A successful court injunction could halt or indefinitely delay construction, leading to a catastrophic loss of value.

Conclusion: Why I'm Adding to My Position

Perpetua Resources stands at an intense moment. The company has successfully passed permitting, which is the most difficult phase for any mining developer and has emerged with final federal approvals for a truly world-class asset. The Stibnite project is a rare combination of a high-grade, low-cost gold deposit with the immense strategic advantage of being America's only domestic source of the critical mineral antimony.

The recent panic selling on June 12 was a clear overreaction to macro news and a misunderstanding of the project's fundamentals. The announcements of the final CWA permit, the formal application for the EXIM loan, and additional defense funding have systematically dismantled the bear case and validated the project's path forward. The management team has the precise experience needed to take this project across the finish line, and the ownership structure, anchored by a significant and growing investment from Paulson & Co., provides a powerful endorsement.

The valuation offers a compelling margin of safety and significant upside. The market has yet to fully price in the de-risking that has occurred, leaving the stock trading at a deep discount to the intrinsic value of its asset. As the final catalysts are achieved over the next 12-18 months, I expect this valuation gap to close. It appears Perpetua is well on its way to having a fully funded, fully permitted Stibnite Gold Project and when that occurs, the stock should rerate significantly higher.

We have done several other deep-dives like these, which go in-depth on companies that we think are undervalued. Our three most recent write ups are the following:

If you enjoy posts like these, make sure to subscribe to The Small Cap Strategist.

This post is for informational and educational purposes only and should not be considered investment advice. The author is not a financial advisor. All investment decisions carry risk, and readers should consult with a qualified financial professional before making any investment choices. The author may or may not hold positions in the securities discussed.

Very interesting!