Where the Cost Went

What an invoice reveals about a Gulf crisis that the oil price could not

Haifa Al Khaifi has worked in the energy sector globally at C-suite level for more than three decades. She now works in the private sector and sits on several international Boards as an Independent Director & Strategic Advisor. She is also a private investor backing female founders with equity.

Jesal Asher-Rajda is the Executive Director of Al Ansari Group, where she leads governance, transformation, and strategic growth. Her career spans international consulting, family business leadership, and board service, with a passion for developing leaders, mentoring the next generation, and giving back to the community.

The cost of a Gulf crisis does not vanish when the shooting stops. It migrates.

On the morning of 24 July 1987, the supertanker Bridgeton was steaming north through the Persian Gulf at the head of the first convoy the United States Navy had ever run for a commercial ship, when a mine hit her hull like a five-hundred-ton hammer.

Her master, Captain Frank Seitz, had no warning. The blast snapped the stays on his radar mast and threw loose gear across the bridge. He ordered the engines stopped, but a fully loaded supertanker does not stop the way a thought does; even crash astern, the Bridgeton took thirty minutes and three miles to come to rest. The Navy escorts around her, smaller and thin-skinned, slowed and held. Seitz got on the radio and told them what he thought they should do. Get in behind the tanker. Her enormous hull could absorb another mine. Theirs could not.

The convoy reformed in that order, the battleship-grey escorts tucked in behind 400,000 tonnes of crude oil and steel, and proceeded north at reduced speed with the mission intact. It’s a strange image, the warships sheltering behind the merchant vessel they had been sent to protect, and it is the right one to begin with, because it is almost exactly what was about to happen to the cost of the crisis. The biggest, best-capitalised hull would take the blow. The smaller ones would tuck in behind it. And the thing everyone was watching, whether the oil would keep moving, turned out to be the wrong thing to watch.

The oil kept moving. That is the part the record is clearest on. Across the whole of the operation that the Bridgeton convoy began, the United States General Accounting Office later found that the feared disruptions to oil supply did not occur, that production in the Gulf actually rose over the period, and that the gap between what crude cost loading in the Gulf and what it cost landed in the United States did not meaningfully widen. Mines were laid, missiles were fired, tankers were hit, and the macro picture in the physical oil system stayed close to undramatic.

The drama had moved somewhere else, into a layer almost nobody outside the trade was looking at.

Two weeks after the Bridgeton, on 10 August 1987, another tanker, the Texaco Caribbean, struck a mine in the Gulf of Oman, outside the strait, in water that had been considered safe. 2 days after that, the underwriters at Lloyd’s of London did something that tells you where the crisis actually lived. They did not declare the Gulf closed. They redrew the map. They imposed a war-risk charge of 0.125% of hull value on ships calling at ports in the United Arab Emirates before they even entered the Gulf, extending the boundary of priced danger into water where no shot had been fired. A contemporaneous headline in Lloyd’s List that week read, in full, “Waiting Gulf Ships to Pay War Premium.” The ships were not waiting because the channel was blocked. They were waiting while the commercial parties worked out who would carry the surcharge.

This is worth sitting with, because it is the whole mechanism in miniature. The visible, competitive cost of the crisis, the freight rate, the physical passage, was not where the system absorbed the shock. The shock was absorbed in the administered cost of insurance, repriced not by the movement of ships but by the decisions of underwriters, and then redistributed. It went into premiums. It went into wages: when Chevron sent its crews into the Gulf, it offered each man the option to disembark first, and then paid a 100% bonus to those, virtually all of them, who stayed aboard. It went into time, because a tanker waiting at anchor in the Gulf kept accruing war-zone bonuses and war-risk premiums for every day it sat there. The cost did not vanish and it did not stop the trade. It was moved off the part of the ledger everyone reads and onto the parts they do not.

And it fell unevenly. The strong hulls absorbed it. Kuwait Petroleum kept fixing ships; state-backed and strategically necessary cargo moved at adjusted economics. The weaker balance sheets tucked in behind or pulled out: Mobil instructed its company-owned ships to stay south of Ras Tanura, and the Norwegian owner Bergesen withdrew from the Gulf altogether. The trade did not halt. It was redistributed, absorbed as a margin cost by those who could carry it and transmitted as exit to those who could not.

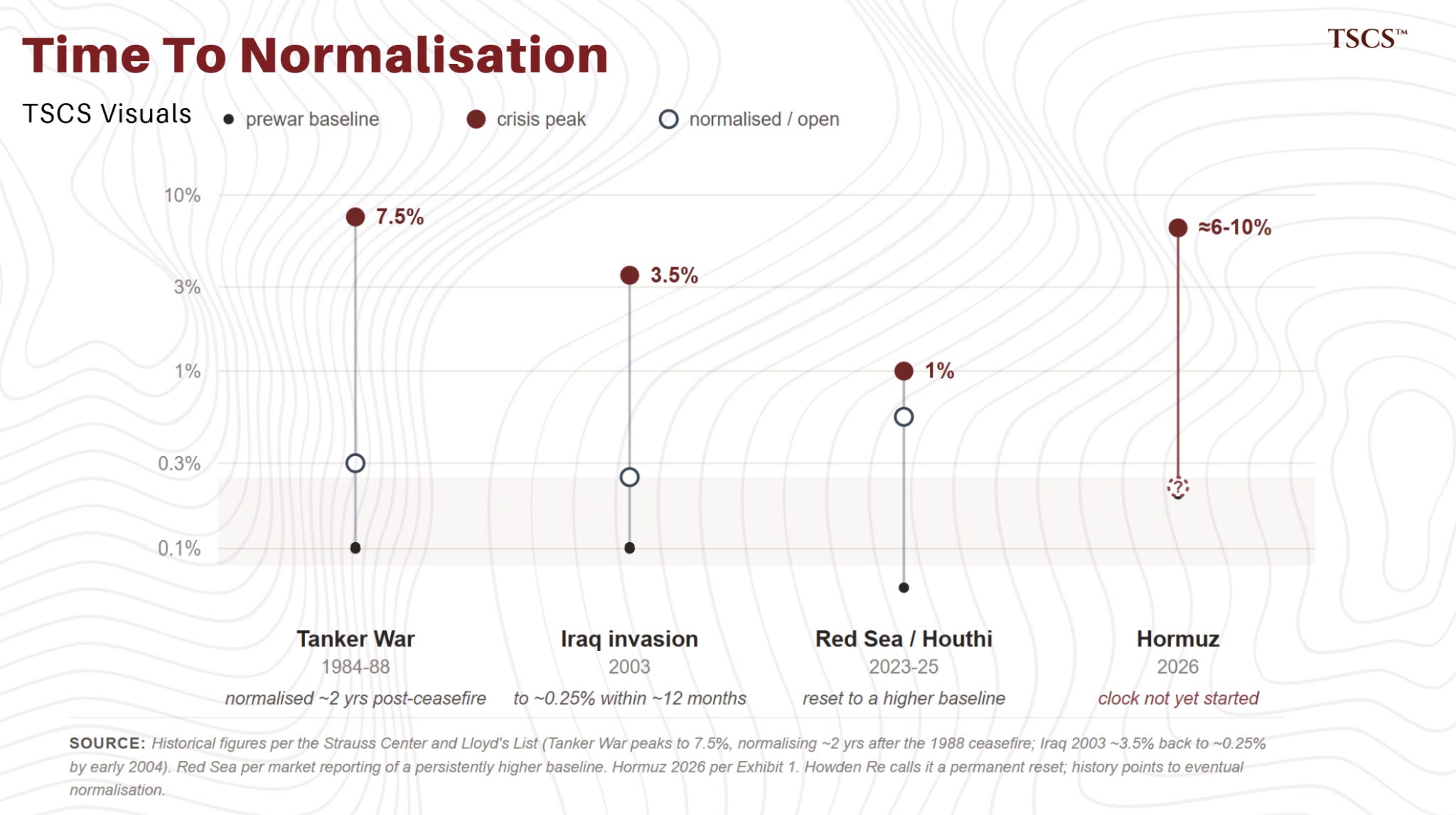

None of this lasted at crisis pitch. As the ceasefire held into 1988, the underwriters cut their rates, and by the summer of 1990, before Iraq’s invasion of Kuwait rewrote the region again, Gulf war-risk pricing had fallen back to a fraction of its wartime peak. The surcharge ratcheted up faster than the danger and came down slower, but it did come down. What did not fade was the architecture: the habit, now reflexive in the London market, of pricing Gulf war-risk separately and by the voyage, of widening the danger zone faster than any physical disruption, of reaching for the seven-day breach premium and the war-zone exclusion the moment the strait makes the news. That muscle memory is 40 years deep, and it is why the events of 2026 unfolded the way they did.

40 years later the same waters are contested again, the ceasefires are being announced and broken in the same week, and the cost is moving to the same place it moved in 1987. This time there is a set of invoices to show it.

The Anomaly

By the first week of July 2026, the crisis kept trying to look over.

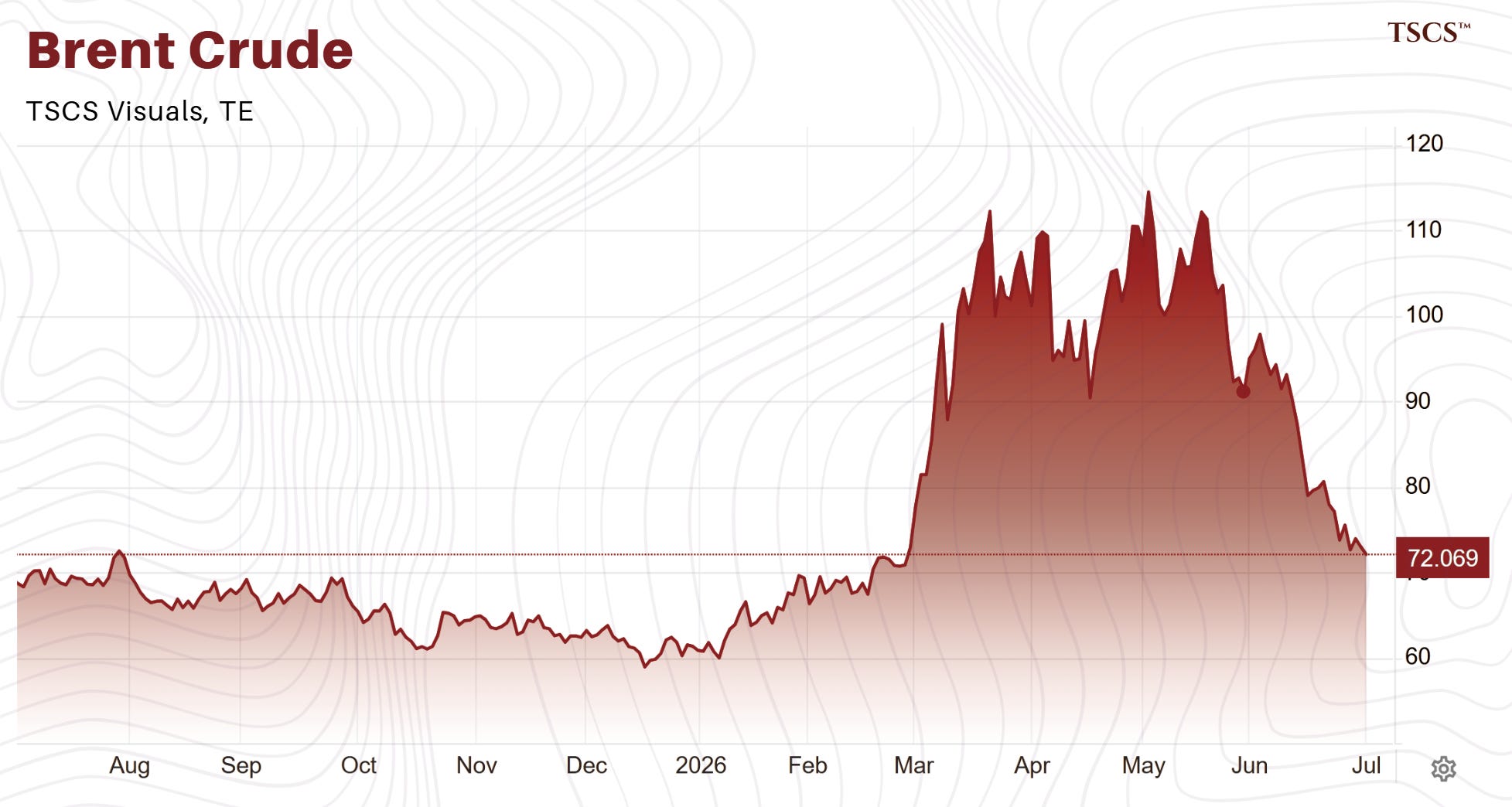

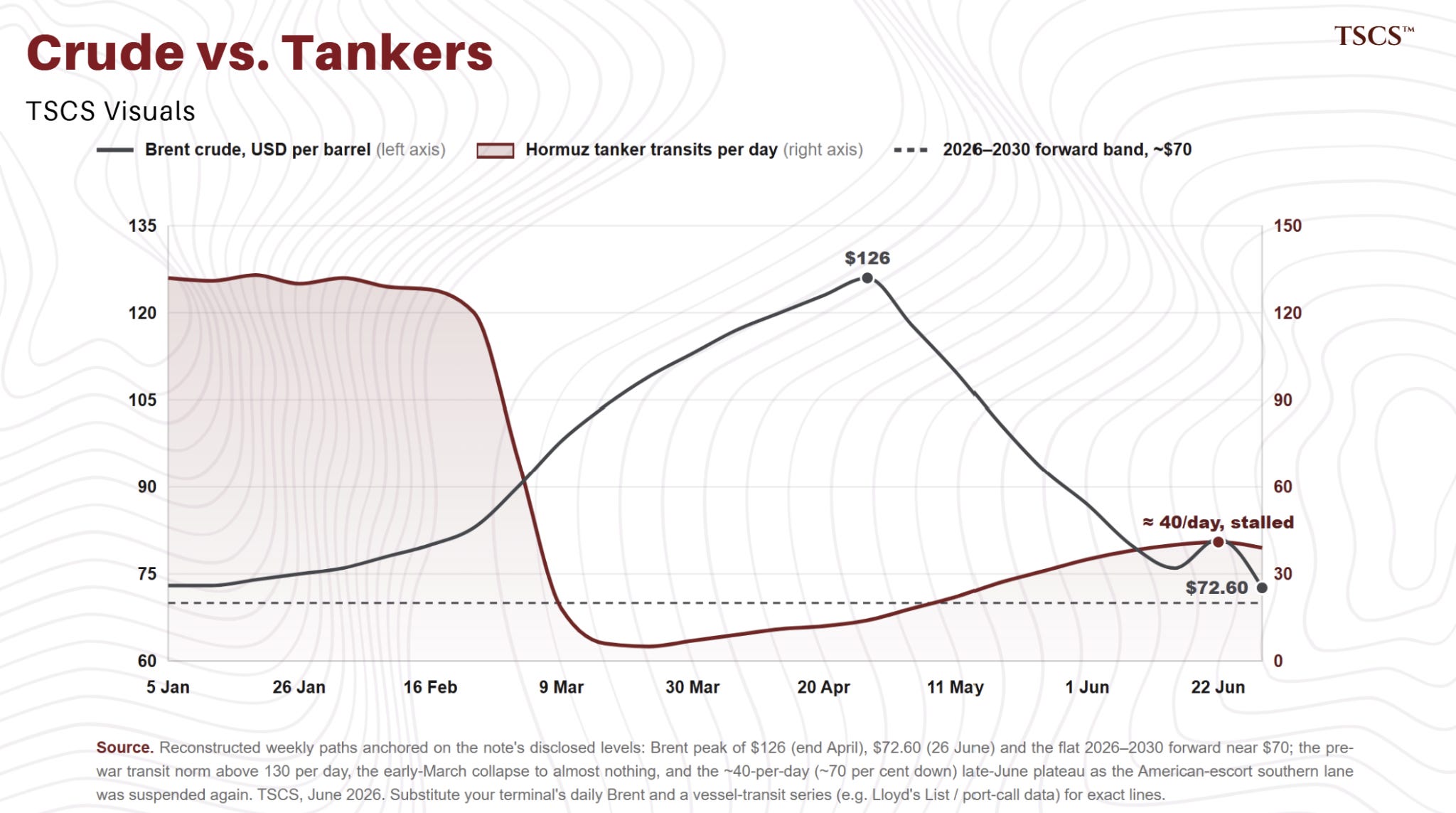

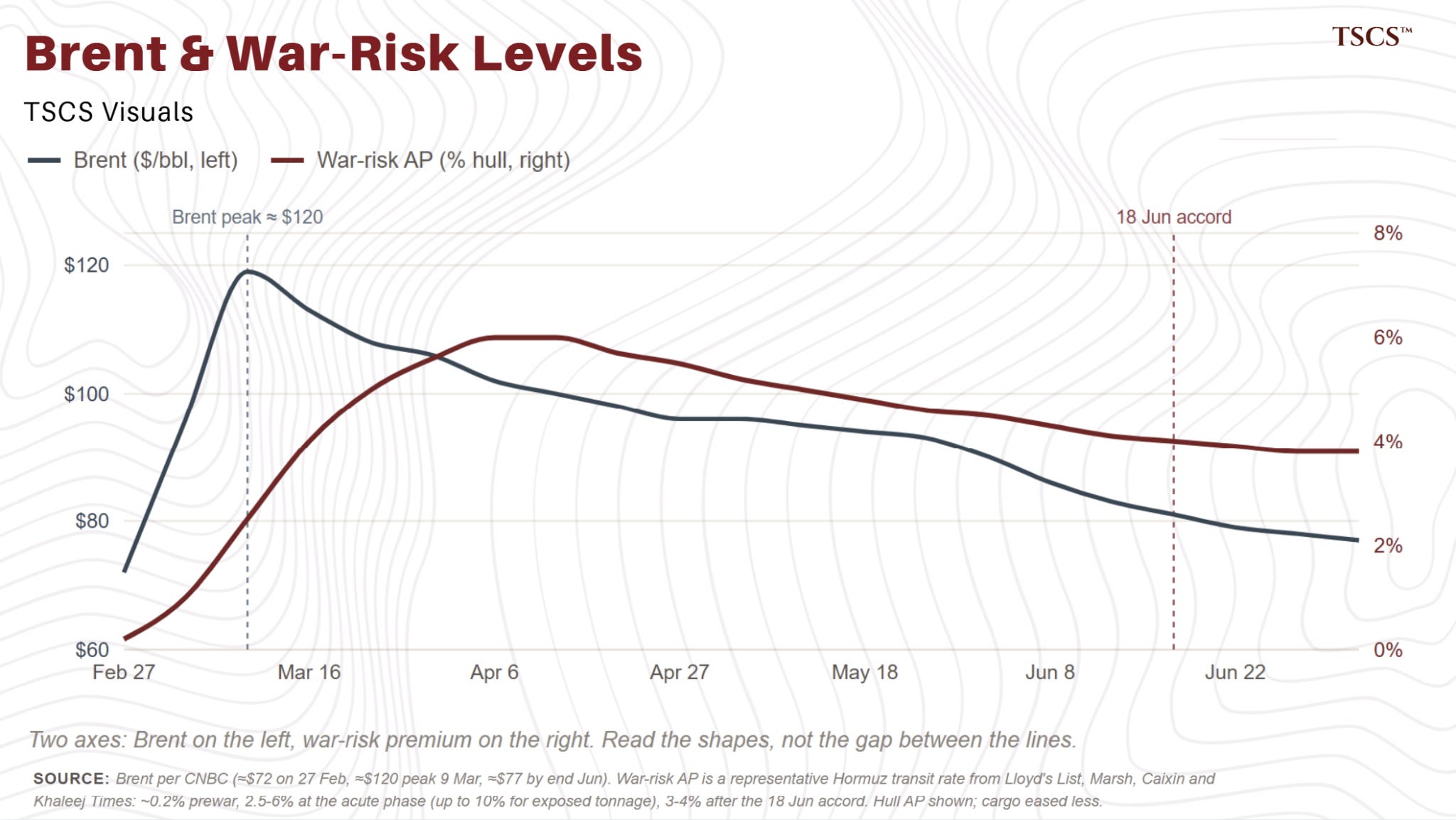

Brent had round-tripped. Brent, which had surpassed $100 within days of the war beginning and peaked in the mid $120s in March, printed $114 again in early May and was back around $70 in the first days of July, and the forward curve out to 2030 sat in a flat band around $70. The reasons it got there are a tangle of returning supply and soft demand that has only partly to do with the strait, and untangling them is another article’s job.

The Strait of Hormuz had been declared reopened under a ceasefire and a coordination arrangement, and Saudi Aramco had resumed loadings at Ras Tanura after a near four-month halt.

Then the ceasefire failed: strikes landed in late June, another vessel was hit in the strait, and further military action followed in the first days of July, before the two sides agreed a one-week de-escalation, paused their talks for the week, and opened a direct communications line to keep incidents contained.

Inside that scheduled window the commercial news turned fast. Qatar announced that all maritime activities would resume, the first loaded LNG carriers since the war moved through the strait, India lifted its emergency gas curbs as Middle East supply restarted, and buyers opened talks on longer sanctions waivers.

The price chased every one of these headlines in turn.

If you were watching the oil price, the story kept finishing and then restarting. The oil price is also the one number in this episode that was guaranteed to tell you the least.

So we looked at the water instead.

Tanker crossings through Hormuz, which ran at well over 100 a day before the war, collapsed to almost nothing in early March. By late June they had recovered, partly, 35 to 40 a day against a pre-war norm of 130 or more and by the end of the month the recovery had stalled rather than continued.

The traffic that did move had split in two, a northern lane running under local coastal coordination and a southern one under American escort.

Exports have recovered faster than transits, with Gulf crude flows working back toward 3/4 of pre-war levels as backlogs cleared, but the count of ships willing to make the passage, stayed at less than 1/3 of normal.

The first days of July brought the biggest change: inside the scheduled de-escalation week, the first loaded LNG carriers of the war came out through the strait, and Qatar announced that all maritime activities would resume.

The improvement is real. Whether this is the beginning of the recovery or another head fake is precisely the question the rest of this is about.

That gap between price and transits is the first clue.

The flat price reverts fastest because it’s the most traded and most arbitraged in the system. It keeps pricing a resolution that keeps not arriving, ING’s head of commodities strategy wrote in the first days of July that the market is treating this temporary ceasefire as a permanent deal and has overshot to the downside.

What it doesn’t tell you is where the cost of the crisis actually went.

To find that, you stop reading the price of oil and start reading the price of moving it, line by line, on an invoice.

The Migration

Here’s what the migration looks like on a single chart.

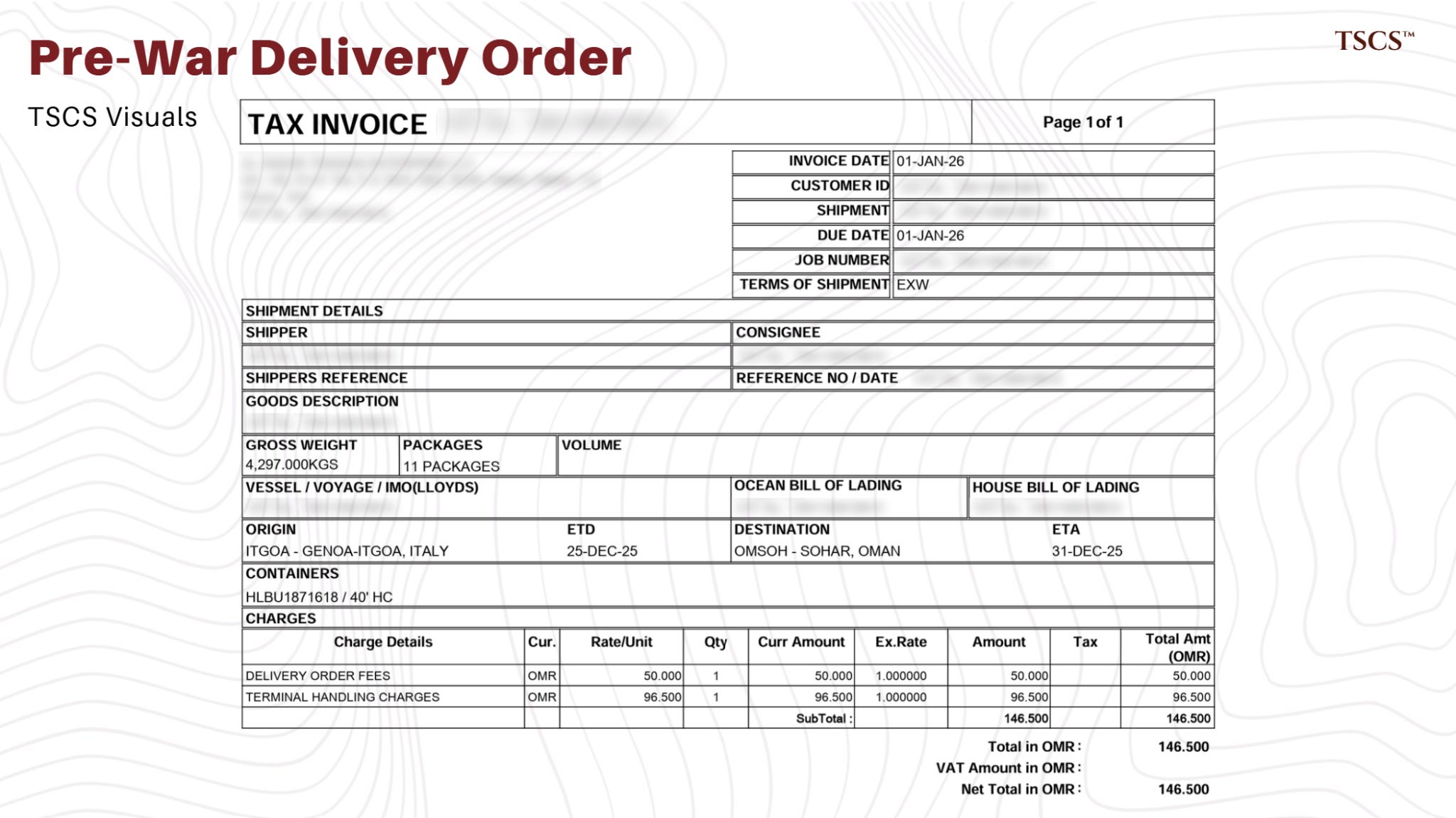

A representative commercial invoice reviewed for this analysis shows the changes in freight costs during the period.

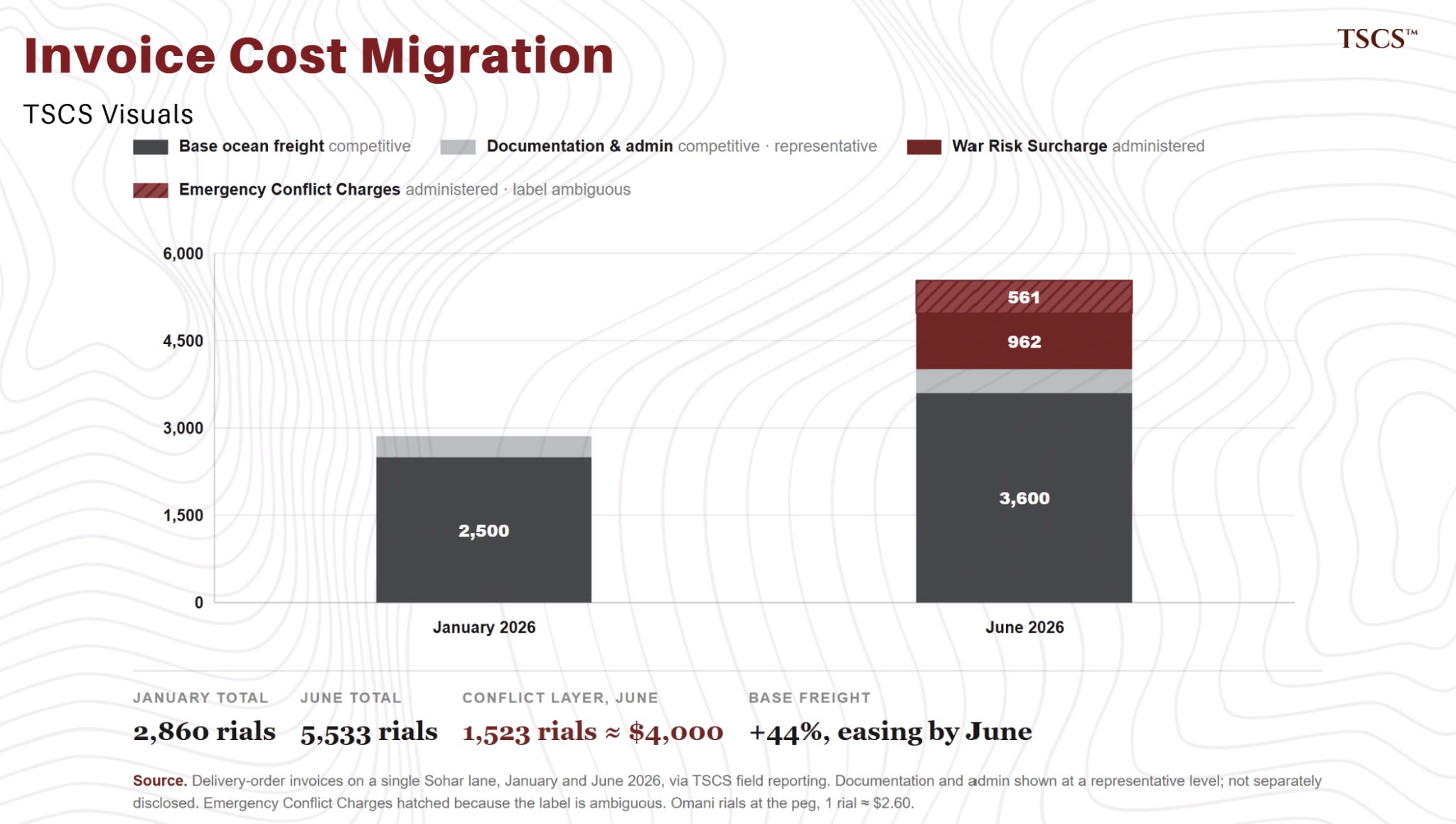

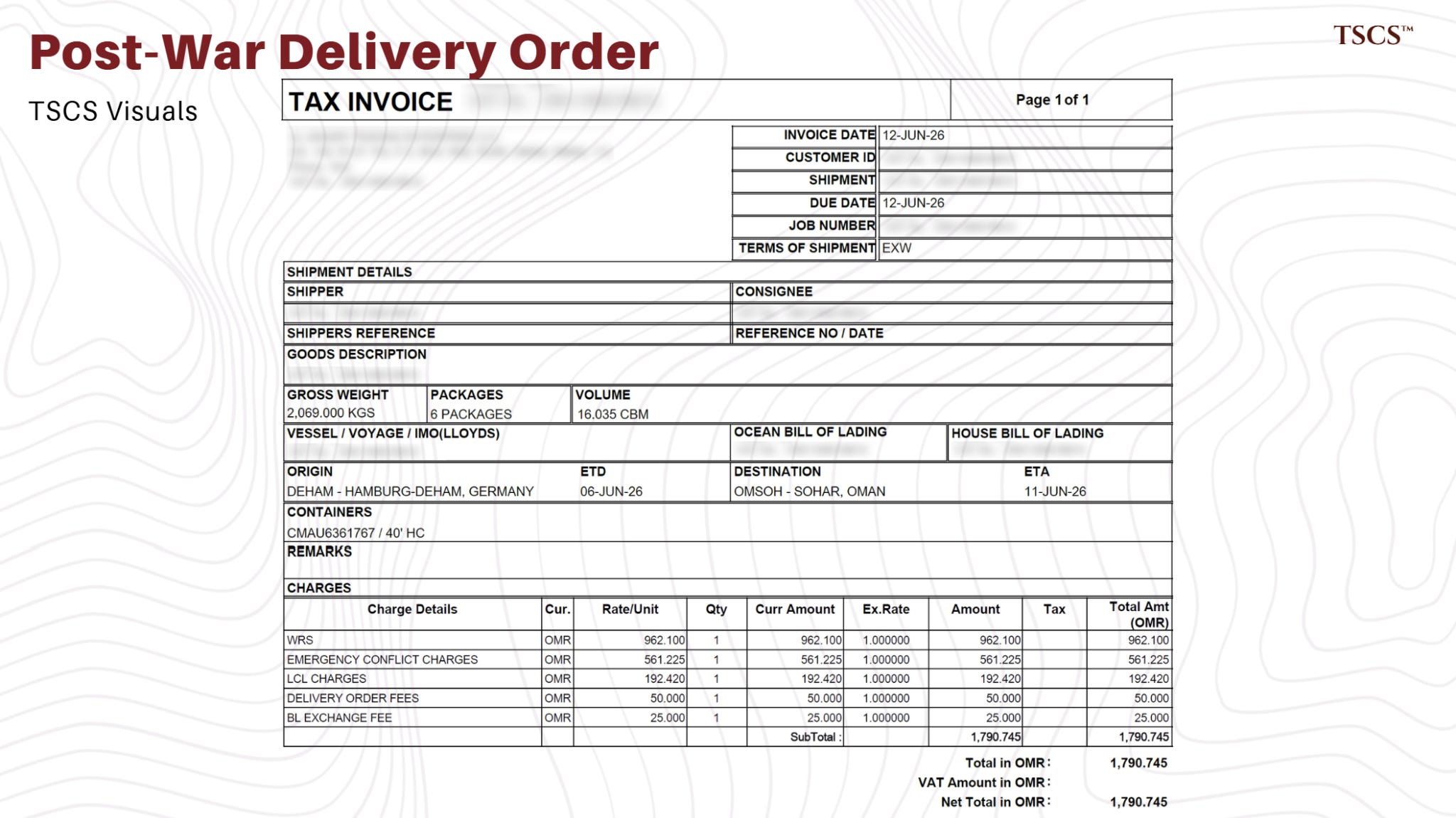

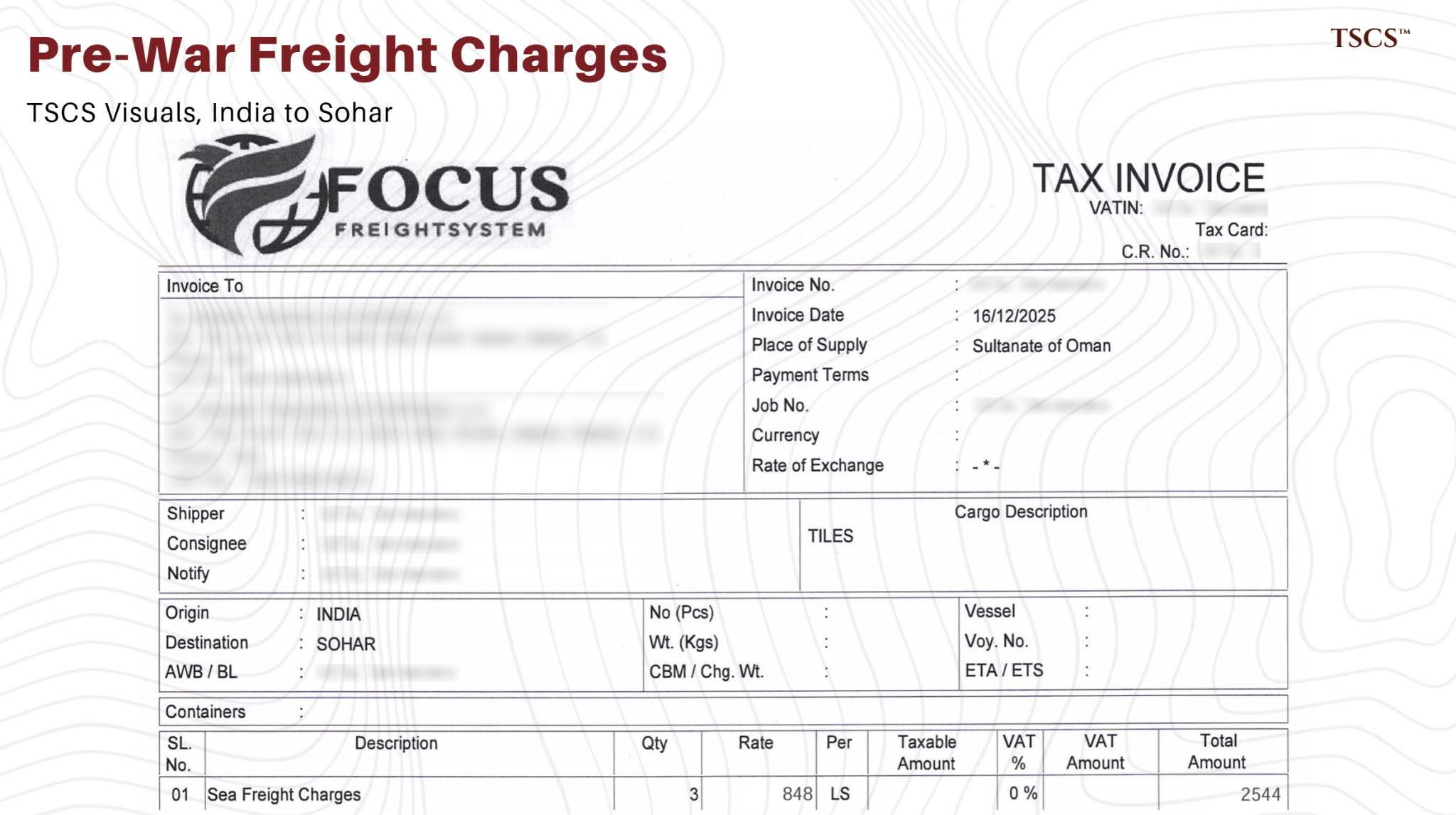

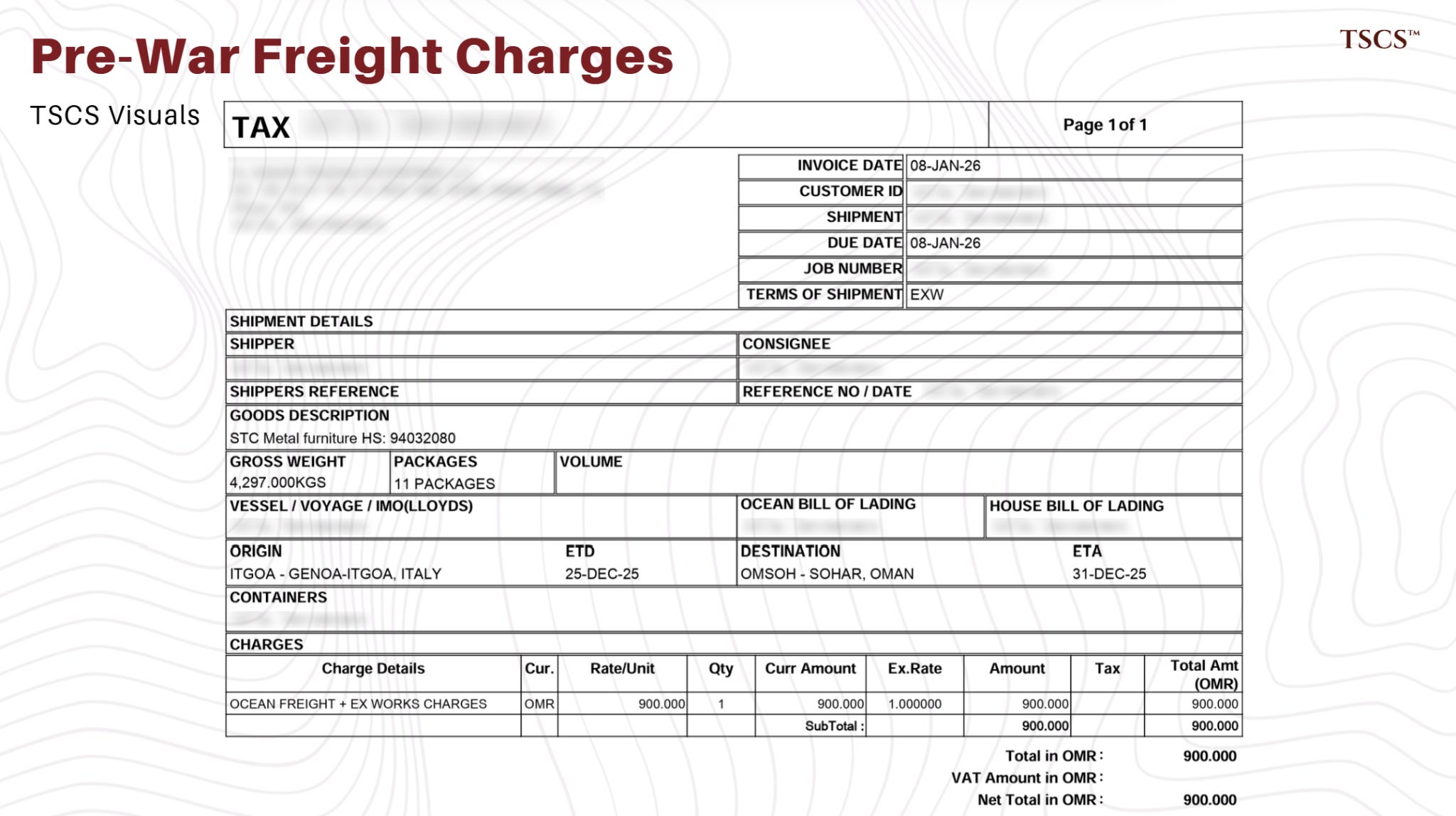

In January 2026, before any of this, a delivery-order invoice for a routine shipment into an Omani port outside the strait carried the line items you would expect: ocean freight, handling, documentation, the small administrative charges of moving a container from one place to another.

The total was unremarkable (as expected).

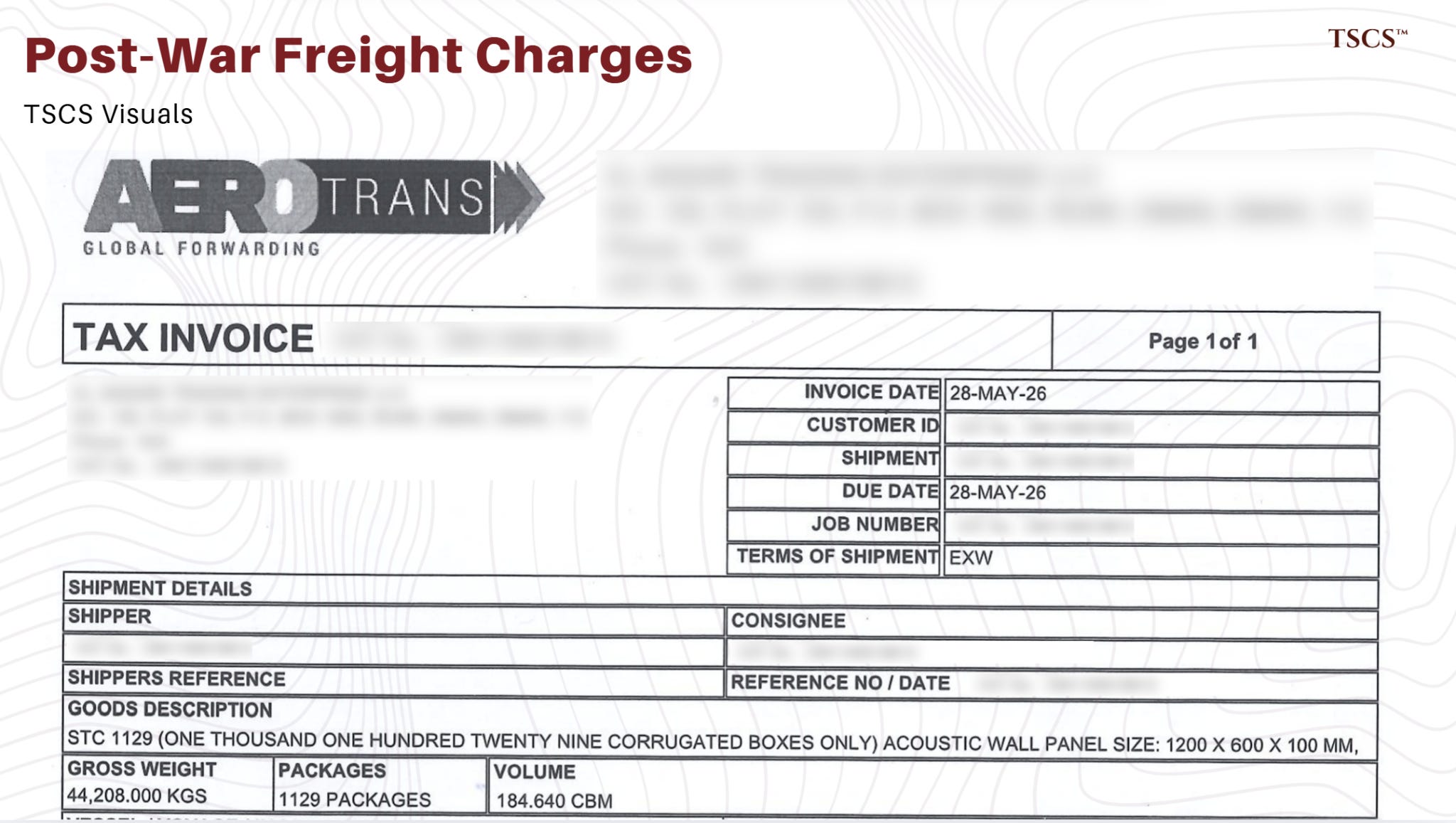

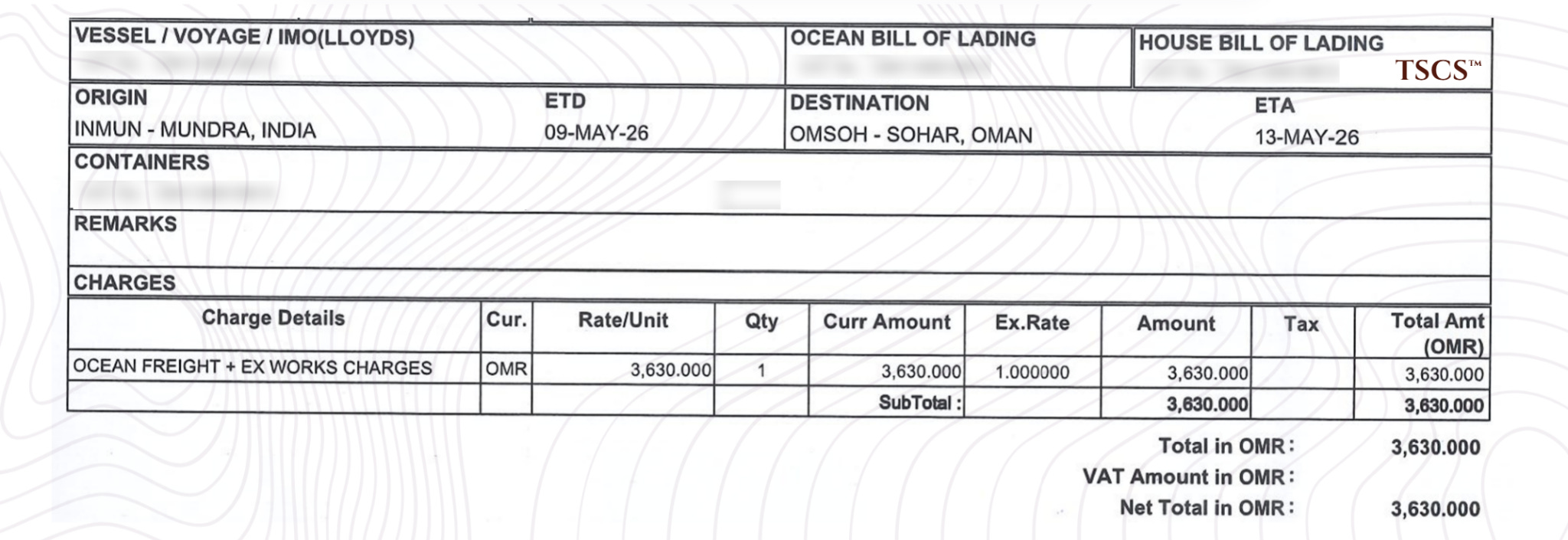

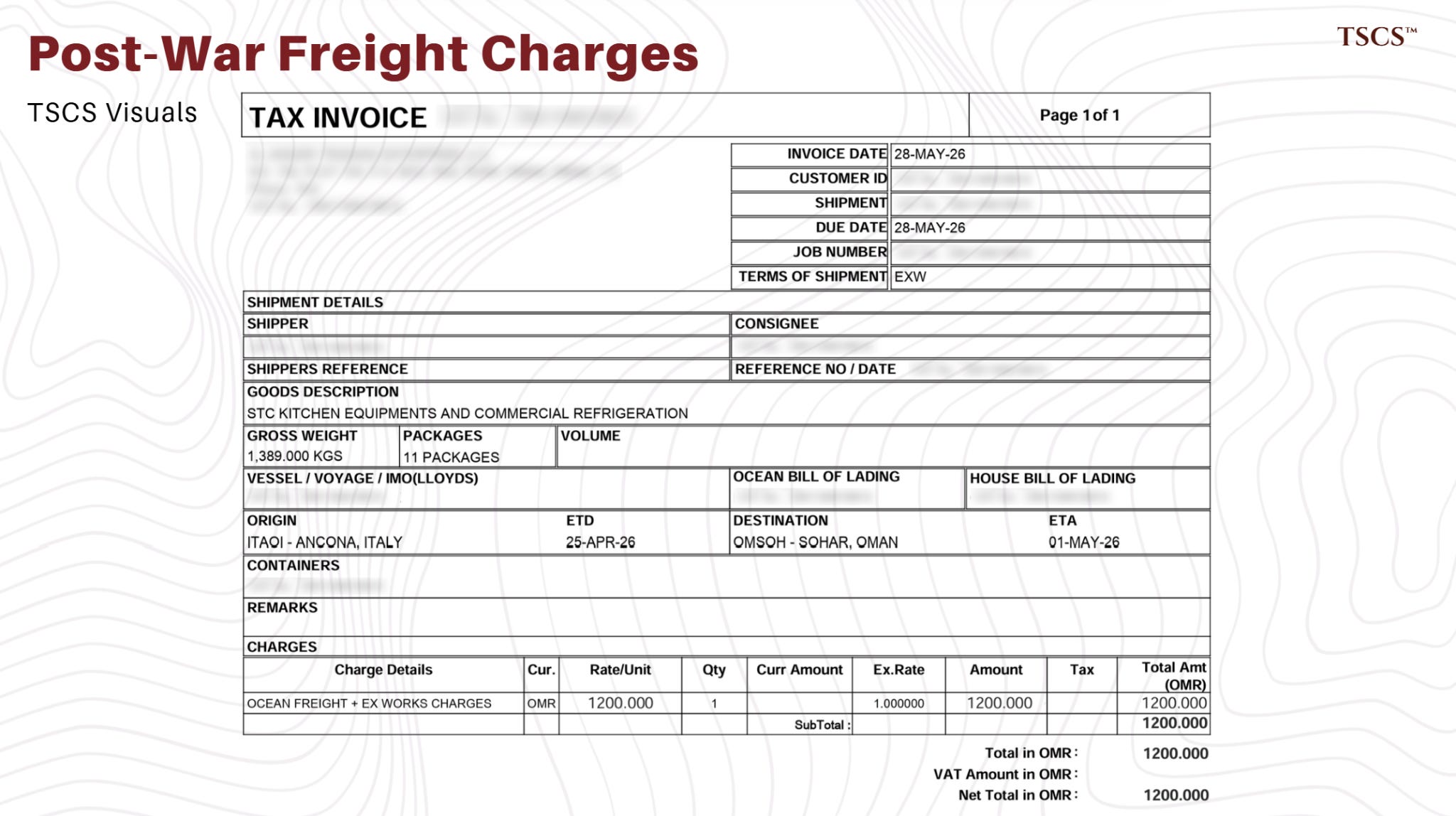

In June, an invoice from the same forwarder, on the same lane, into the same port, carried two new lines that had not existed earlier.

One was labelled War Risk Surcharge, at 962 Omani rials. The other was labelled Emergency Conflict Charges, at 561 Omani rials. Together, a little over 1,500 Omani rials of cost, around $4,000, that simply was not there in January.

We’ve read a lot of freight invoices. We had not, before this one, seen a line item called Emergency Conflict Charges.

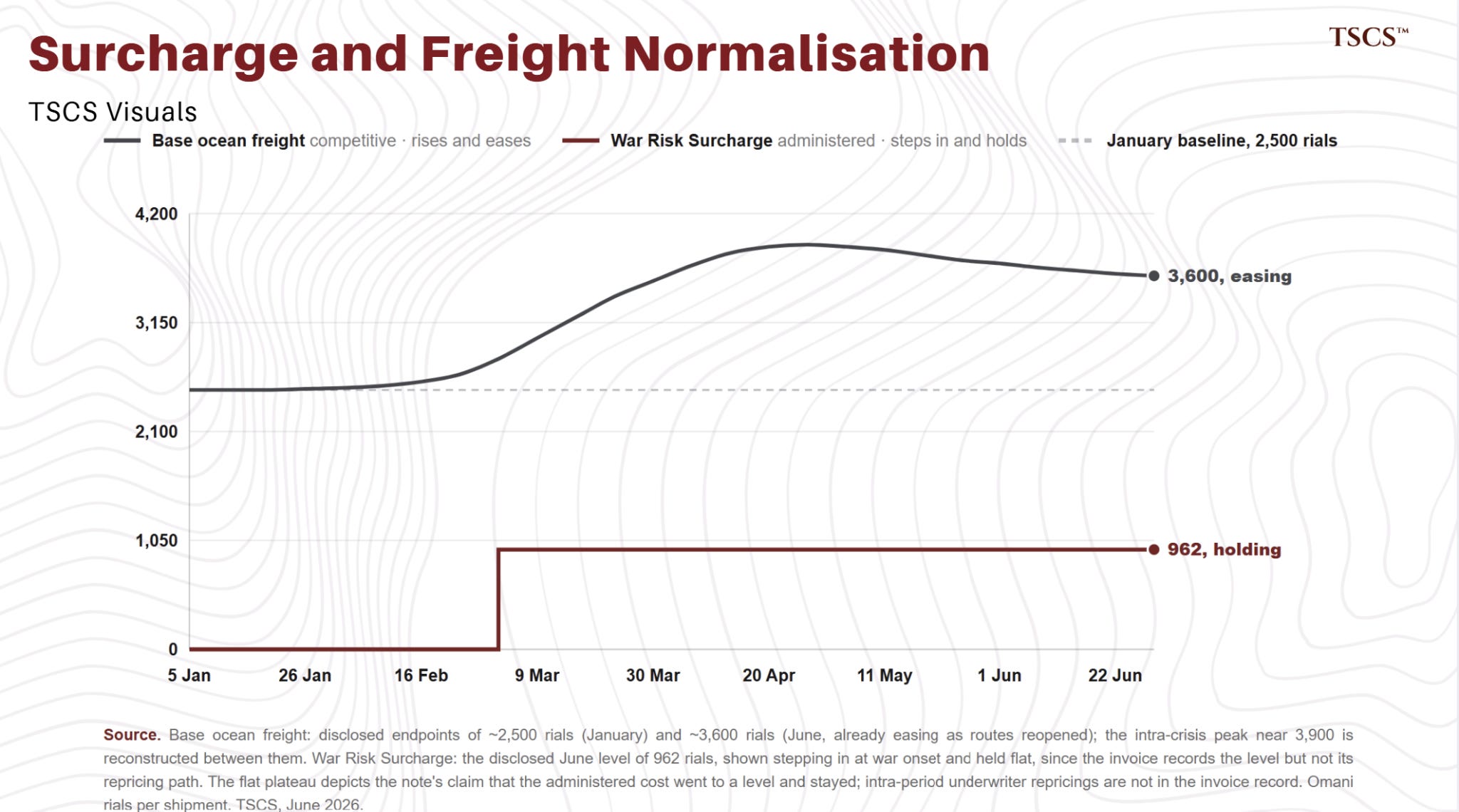

Set against those two lines, base ocean freight on the lane rose from around 2,500 Omani rials to about 3,600, a 40% increase, and by June it was already easing as routes reopened.

The competitive cost of moving the goods behaved as expected. The administered cost, the war-risk line, went from nothing to four figures and stayed.

That’s the migration in miniature.

It’s worth being specific about what these two lines are, because they aren’t the same kind of cost. The War Risk Surcharge is the carrier passing through the price of marine war-risk insurance, the premium an underwriter charges to cover a hull and its cargo through a zone the market has designated dangerous. It’s essentially a cost set by an underwriter and repriced only when the underwriter decides to reprice.

The Emergency Conflict Charges line is harder to place with the same confidence. It may be a second insurance pass-through under another name, or it may be a carrier charge for the rerouting and congestion the conflict caused, which would make it partly a competitive cost wearing an alarming label.

One invoice can’t prove that the cost stayed elevated across time; that’s the job of the market-wide premium data, which comes next. What the invoice does, which no index can, is show the mechanism in close-up, on a real shipment.

There’s an obvious objection to building anything on one piece of paper. This is one piece of data. This is simply a pattern the market data shows in aggregate, which is a different and more modest claim than a regularity, and a more useful one than a statistic, because you can see the names of the charges.

FYI, this invoice exists because the shipment happened. The cargo that didn’t move generated no invoice at all, trade that can’t survive a cost doesn’t generate a record of itself; it just stops. Which means the document in front of us, for all that it shows, understates the disruption rather than overstating it.

The Split

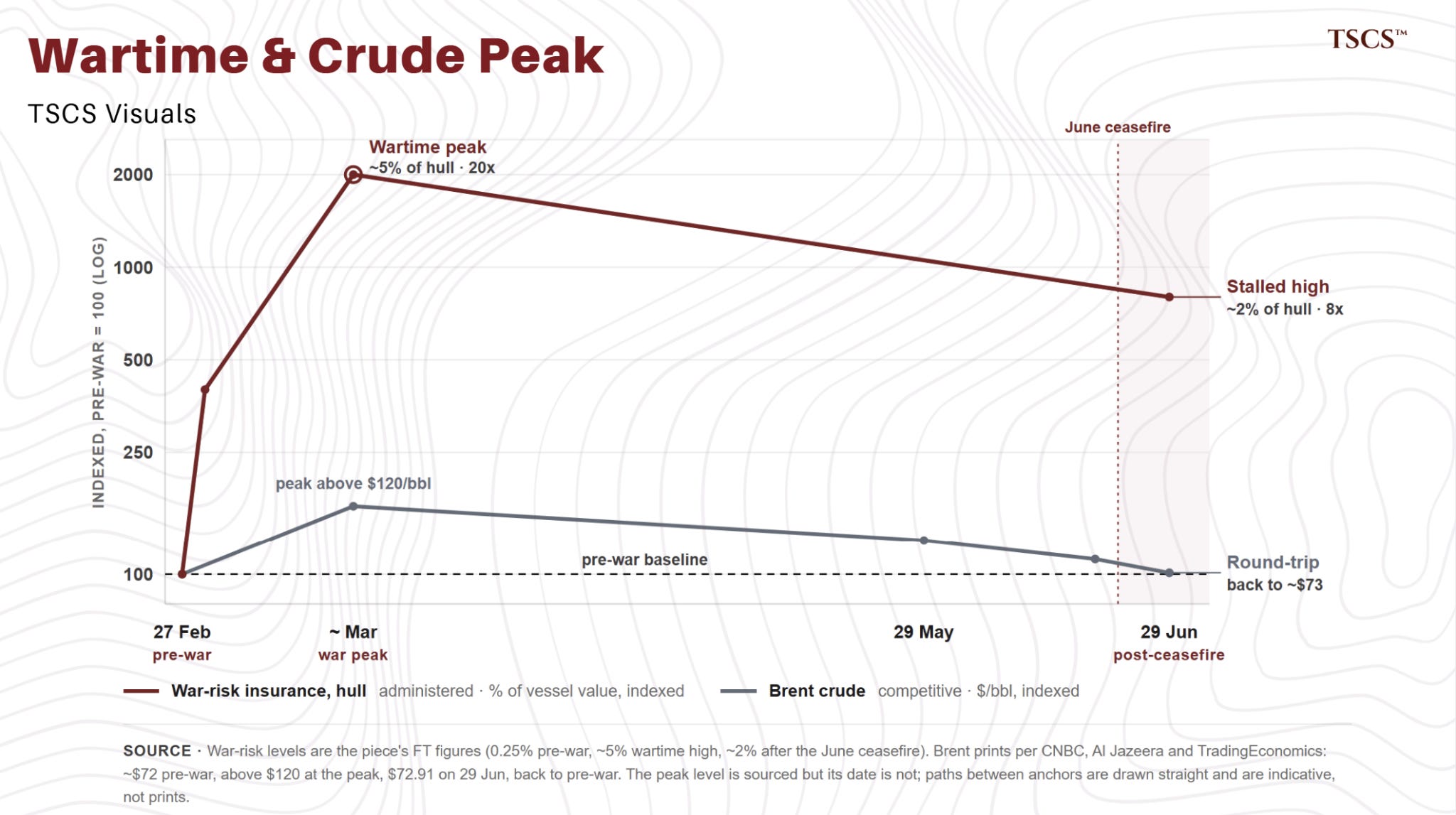

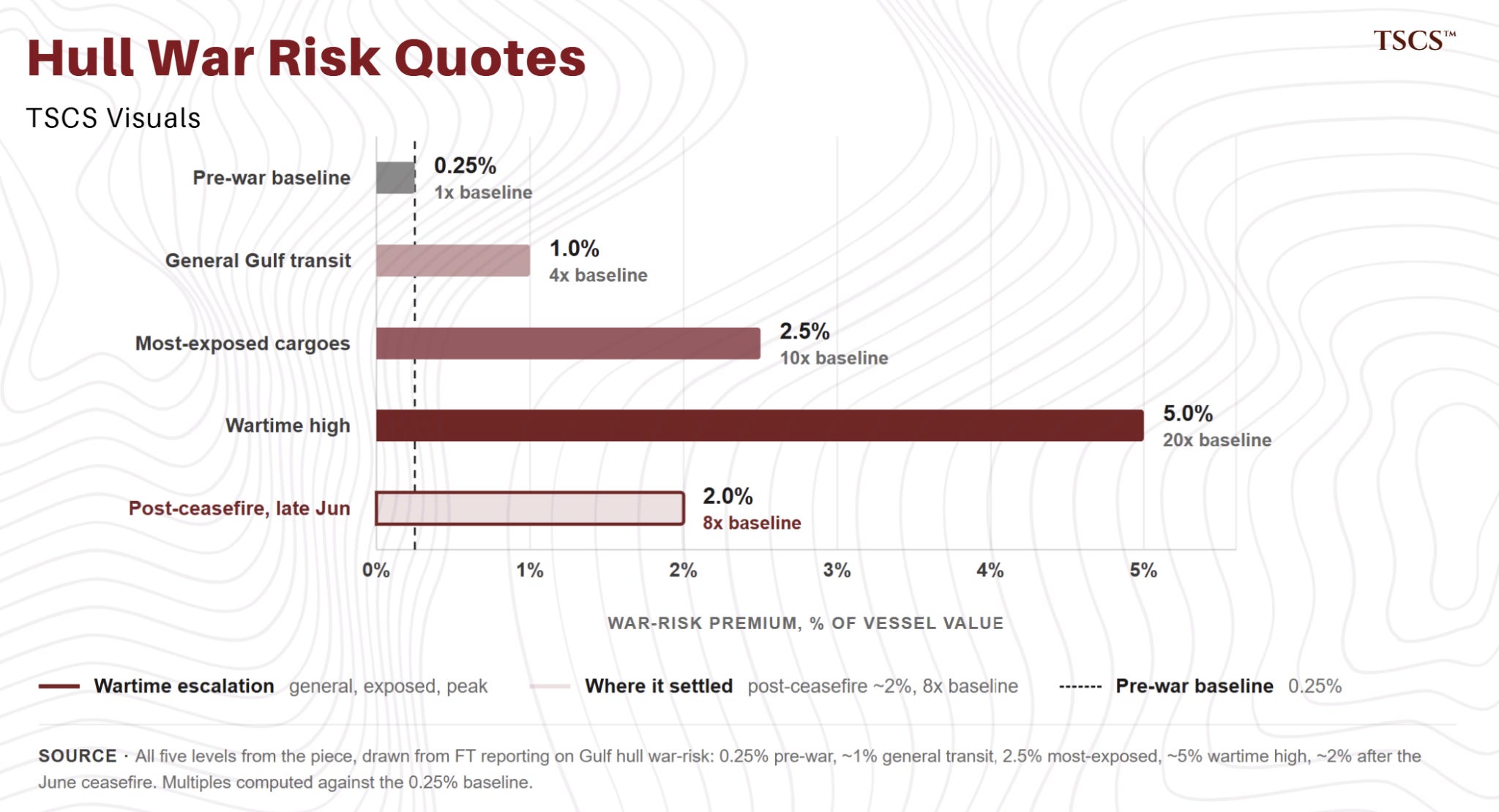

Marine war-risk insurance is quoted as a percentage of a ship’s hull value, and before the war that percentage for the Gulf sat at around 0.25%, a figure underwriters had grown comfortable with after years of relative calm.

When the strikes began at the end of February, it moved the way the invoice moved. Within days the rate for general Gulf transit ran to around 1%, 4x the baseline, and for the most exposed cargoes, ships transiting the strait itself, or carrying an American or Israeli connection, underwriters were quoting 2.5%, 5%, in the worst cases higher still.

Then, as the immediate danger eased, the two layers began to move apart.

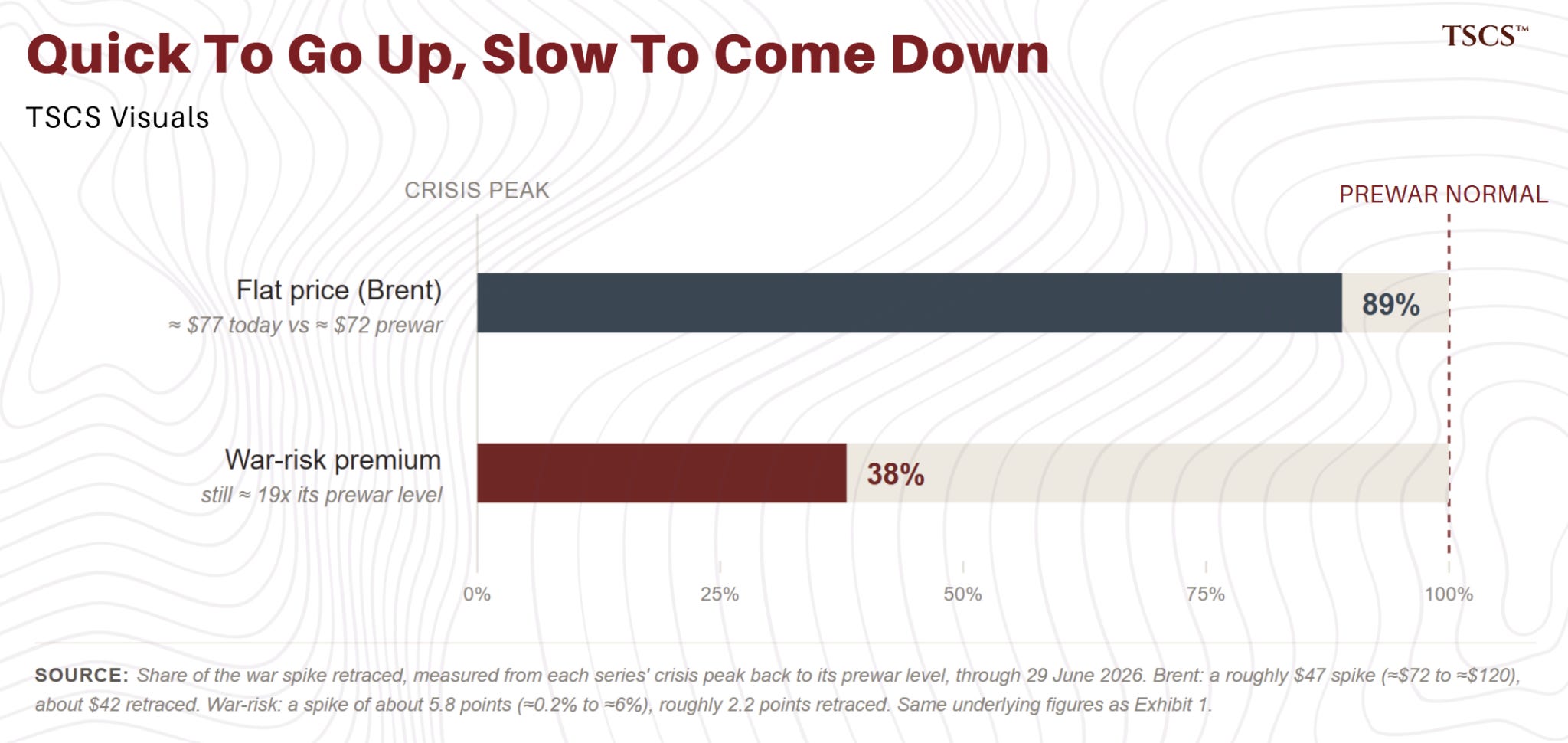

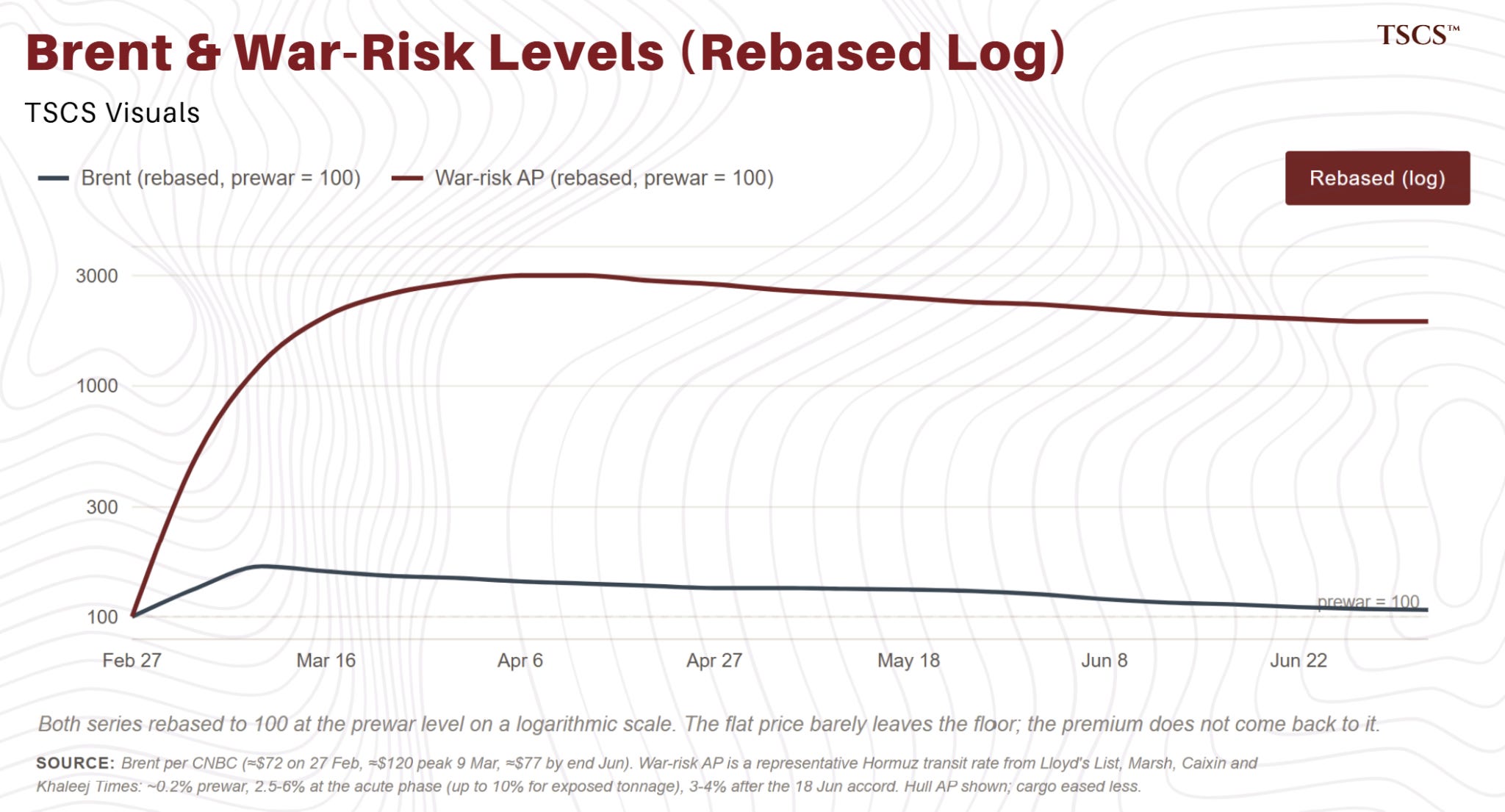

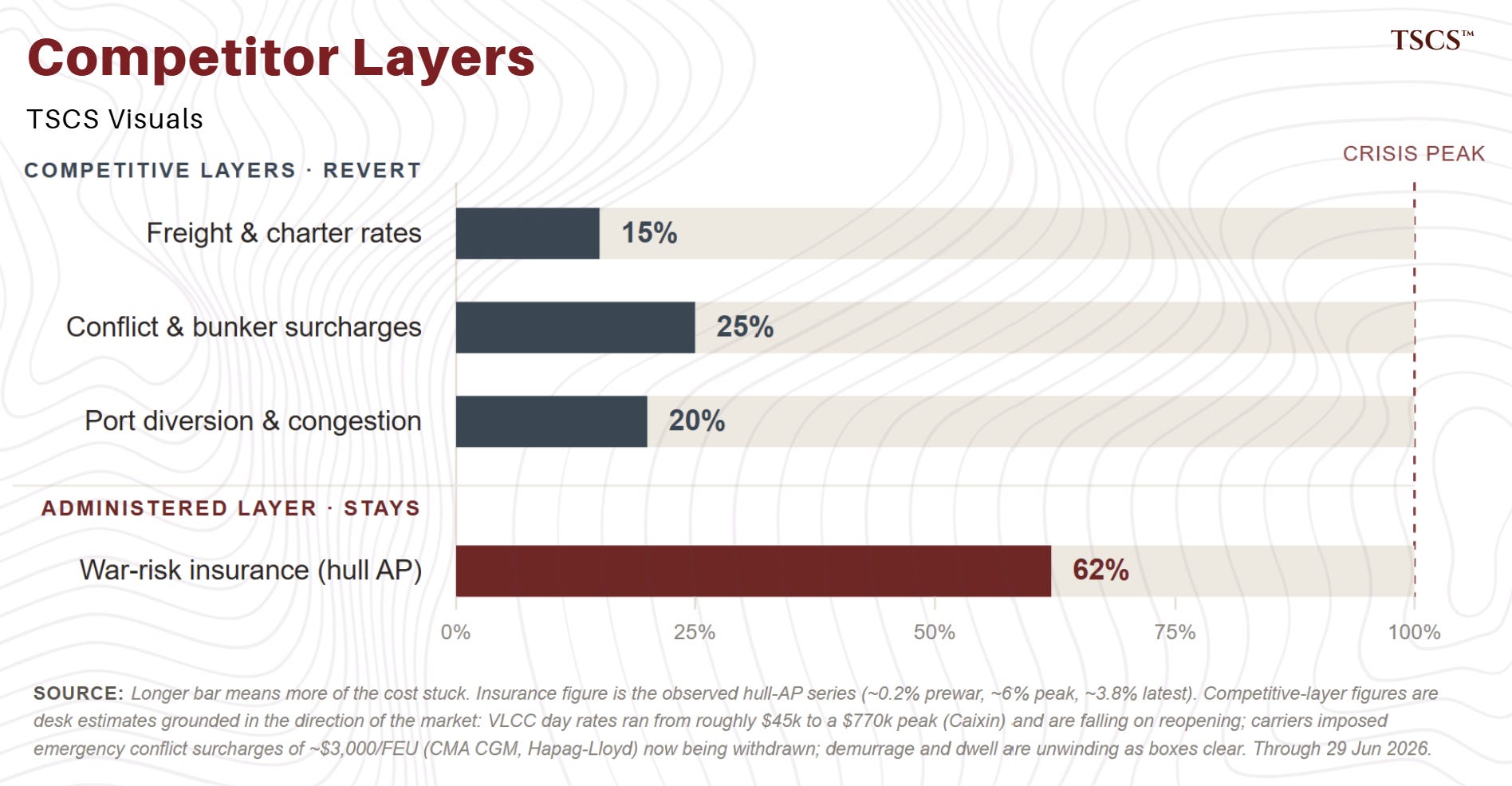

Competitive costs did what competitive costs do. Freight rates on the disrupted lanes turned over and started back down. The oil price round-tripped. Everything priced by the physical movement of ships reverted toward where it had started.

However, administered cost didn’t follow. After the June ceasefire, hull war-risk came down from its peak, but the Financial Times reported it falling only to around 2% of vessel value, from a wartime high near 5%. It had roughly halved, and it was still something close to an order of magnitude above where it began.

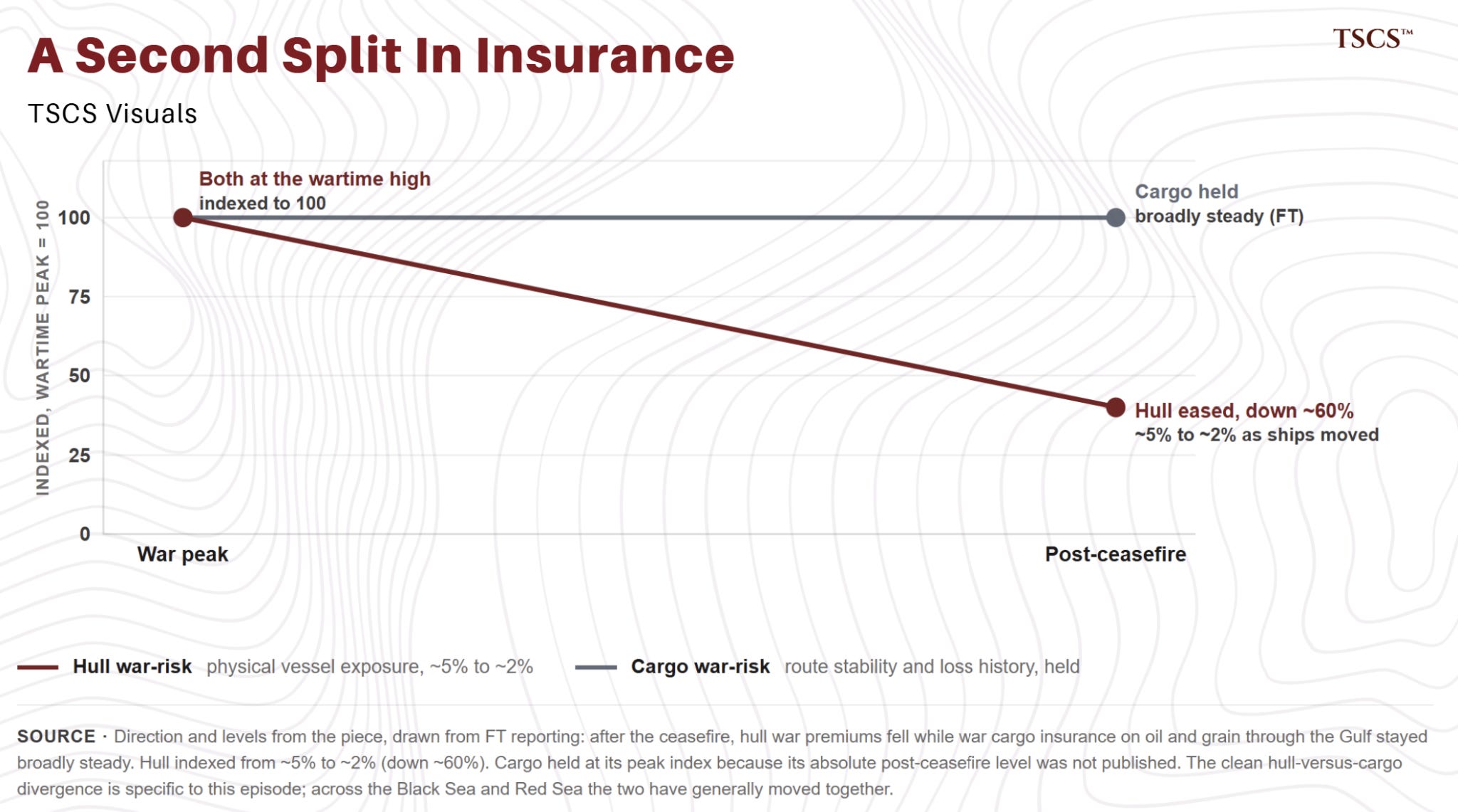

And inside the insurance layer there’s a second split. Hull cover and cargo cover aren’t the same instrument, and here they didn’t move together.

Hull war-risk is priced against a vessel’s physical exposure on a given transit, so when ships began moving again it started to come down. Cargo war-risk is priced slower: the underwriter’s read of route stability and loss history, metrics that don’t reset on a ceasefire announcement, least of all one that had already been broken once.

So as the hull rate eased, the cargo rate hasn’t. After the ceasefire, war cargo insurance on oil and grain through the Gulf stayed broadly steady while hull war premiums fell (per FT).

We’ll be careful about how far to push this, because across earlier crises, the Black Sea, the Red Sea, hull war-risk and cargo war-risk have generally moved up and down together as the security picture changed.

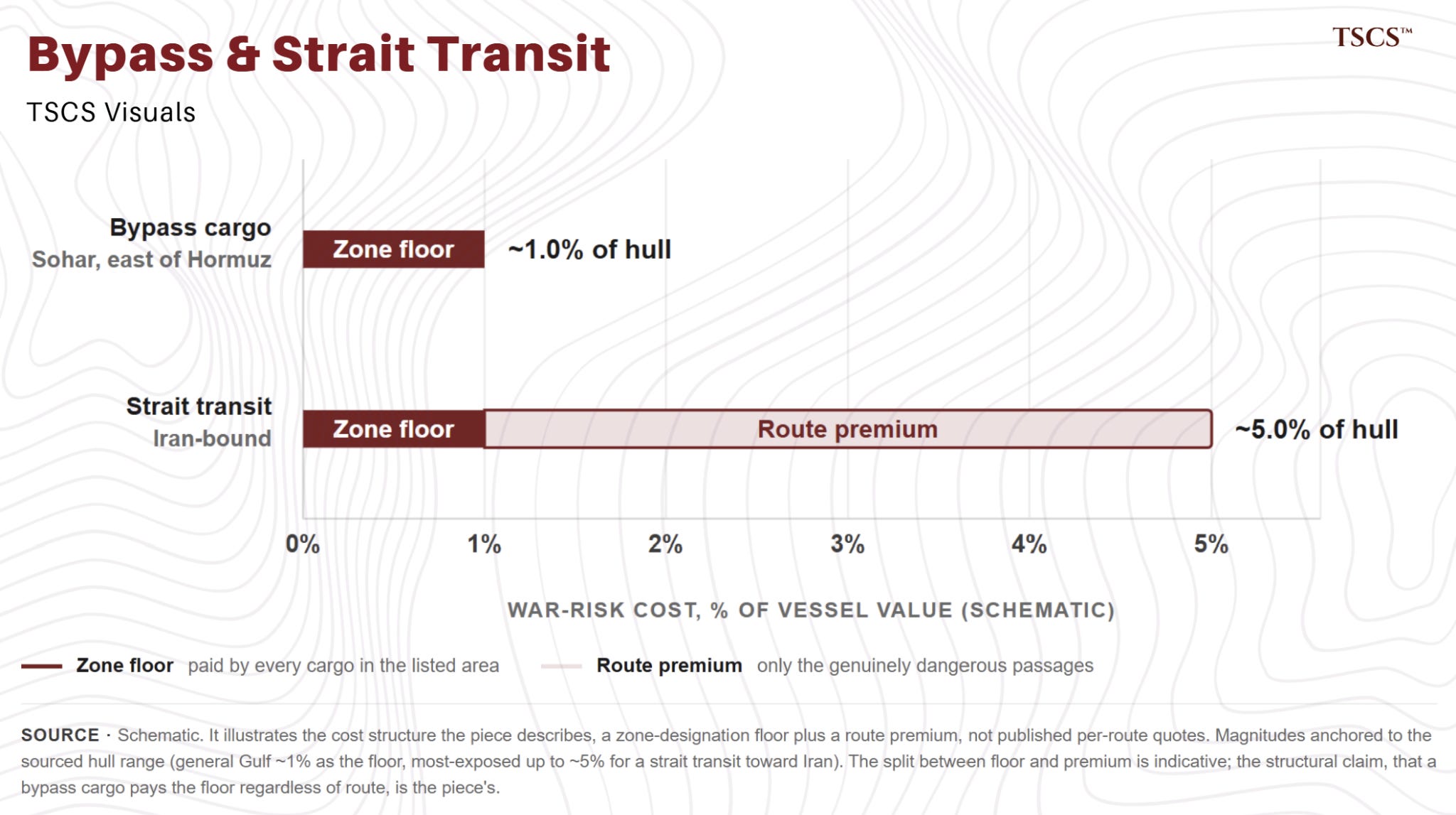

There’s one complication. War-risk cost is not one flat number imposed regardless of route. It’s better understood as a floor set by the zone designation, which everyone inside the listed area pays, with a route premium stacked on top for the genuinely dangerous passages. So, a cargo that never went near the strait still paid a war-risk floor, because the zone it was designated into carried the cost regardless of the route the ship took.

Why Does It Persist?

So why does the administered layer lag? Why, with the flat price round-tripping and the headlines moving on, does the war-risk line refuse to follow?

The first answer is the simplest.

The danger has not gone away. The ceasefire announced in the middle of June was broken within days, then both sides agreed a one-week de-escalation in the waterway, paused their talks, and opened a direct communications line to keep incidents contained. Underwriters aren’t pricing on headlines. The cargo war-risk premium is not lagging the resolution. There is no resolution yet.

The second answer is structural, and it’s why the premium will lag even once the shooting stops. War-risk cover is administered. It comes off when an underwriter decides to take it off, and underwriters obviously won’t move on optimism. They move on the formal removal of a zone’s war-risk listing.

Willis Towers Watson told clients in May that war-risk rates were unlikely to fall after a ceasefire, because actuarial pricing resets only as sustained incident-free transit data accumulates, a process the industry measures in years.

The Joint War Committee, which maintains the listed-area designation, meets quarterly and requires multiple consecutive clean assessments before a zone even becomes a candidate for removal.

The claims arithmetic points the same way: Howden Re estimates $2 to 3 billion of war and political-violence claims from this crisis against roughly $1.5 to 2 billion of annual global premium for the entire segment, a loss ratio past 100%, which is not the position from which underwriters cut prices. And one regional broker put the near-term version plainly: 2 to 4 weeks of confirmed de-escalation before pricing even begins to respond.

None of that is satisfied by a ceasefire announcement, particularly one that has already failed once.

The people who set these rates have been unusually direct about it. We asked one London underwriter when the Gulf rates would come down, and they replied simply that premiums are quick to go up and slow to come down. The reinsurance broker Howden Re has gone further, arguing that the Red Sea disruptions of the past two years and the Hormuz crisis of this one together amount to a permanent upward reset of the marine war-risk baseline, and that rates will not retreat meaningfully until the danger zone is formally lifted and stays lifted. RBC’s Helima Croft put the same thought in market terms: pre-war transit levels may turn out to be the high point for the foreseeable future, if the security picture around the strait remains unresolved.

But there’s a third piece of evidence which shows risk wasn’t just repriced. Capacity became significantly constrained.

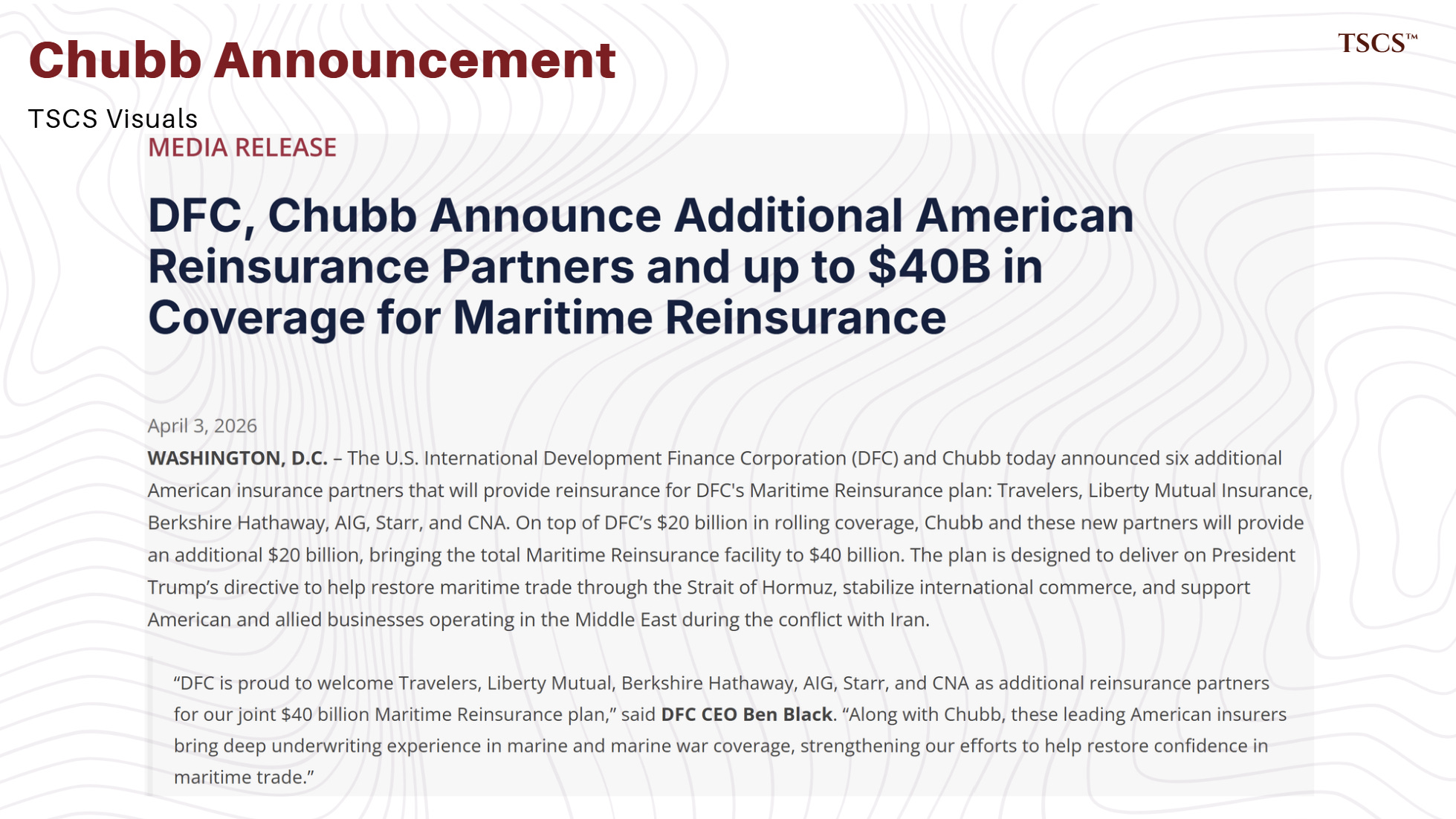

As the war-risk insurers issued cancellation notices and pulled their capacity in early March, the cover that keeps tankers moving started to disappear, and a government stepped into the gap. The United States, through its Development Finance Corporation, put up a reported $40 billion backstop, administered by Chubb to reinsure marine war-risk that the private market would no longer carry.

The World Economic Forum described the moment nicely: governments are increasingly underwriting markets. This should give one pause.

When the state has to become the insurer of last resort, it’s a structural failure of the private market.

However, it’s important to note: the Tanker War of the 1980s, the closest precedent, does not support the idea that one crisis permanently resets Gulf war-risk pricing for years.

There, the surcharge ratcheted up faster than the danger and came down slower, exactly as it’s doing now, but once the ceasefire finally held, the rates did come down, and within a couple of years Gulf war-risk had fallen back close to where it started.

The safest claim is that the administered layer stays elevated longer than the physical danger appears to justify, over the months and quarters of the underwriting horizon, and then, if the danger truly recedes, it normalises.

Howden’s permanent reset and the historical pattern of eventual normalisation are in tension.

What can be said with more confidence is narrower and, for now, sufficient: the normalisation clock does not start until the danger actually passes.

For now, it’s here to stay.

Where The Rent Went

If the cost migrated into the insurance layer, then it didn’t migrate into the places most people assumed it would.

The intuitive story of a Gulf disruption is that the trade reroutes and the alternative ports collect the rent: ships that will not enter the strait divert to the nearest hub outside it. It’s a clean story, and those who stood to gain from it told it enthusiastically.

It’s also, on the evidence, not what happened.

The diversion was real, but it was temporary, and the durable economic benefit accrued somewhere else entirely.

Let’s start with where the diverted volume went, because it probably isn’t where you would think.

The natural assumption was that Oman’s ports, sitting just outside the strait, would absorb the rerouted Gulf traffic.

They largely did not.

The gateways that absorbed most of the diverted volume were those with the deepest existing land-side machinery outside Hormuz, where trucking, customs and inland connectivity were already most developed.

Capturing diverted flow at short notice depends on surrounding machinery, trucking capacity, landed cost, inland connectivity, as much as on geography.

On this occasion the volume moved fastest to where that machinery was already deepest, and it is precisely that machinery Oman is now building out.

The following reporting drew on candid, off-the-record access across the region’s ports, shipping lines and trading houses, granted on the understanding that identities and commercial detail would not be exposed.

Those promises hold throughout what follows.

It was a conversation with one of the many port officials we spoke with across the region that explained why the diverted volume was never going to stay.

Routing of this kind is an efficiency game. Operational patterns normalise over time, they said, and cargo routing decisions continue to be driven by efficiency and economics: when the cheapest route reopens, the cargo returns to it.

A diversion forced by a closed strait reverts on reopening. It reverts the moment the obstruction clears, which is what the partial reopening began unwinding.

So if the rerouting was temporary and the volume mostly went elsewhere, where did the durable cost land?

The same official was unambiguous about where the durable cost settled.

Insurance providers were among the most obvious beneficiaries of the disruption, through increased risk premiums, while the shipping companies passed their additional costs through as surcharges and took no direct margin gain.

And they drew the distinction this whole piece has been building toward, in almost these words: operational patterns will normalise, but insurance costs may remain elevated for longer. The administered layer stays.

And it’s not just a single account: the hull-premium series shows the same thing from the top down, across the whole Gulf.

That’s the key finding of this analysis, and it reframes the question for the country at the centre of the story.

If the durable economic benefit accrued to the insurance market rather than the bypass ports, then the most repeated claim about this crisis, that Oman, sitting at the mouth of the strait, was handed a windfall, deserves a more careful reading than it usually gets.

Which is what the next section does.

Who Is Holding It

If the cost migrated into the war-risk layer, it’s worth asking who is now collecting it.

The answer is a short list of specialist underwriters: if the cost really did lodge in the administered layer and stay there, it should be visible as margin in the accounts of the firms that write the cover.

It is.

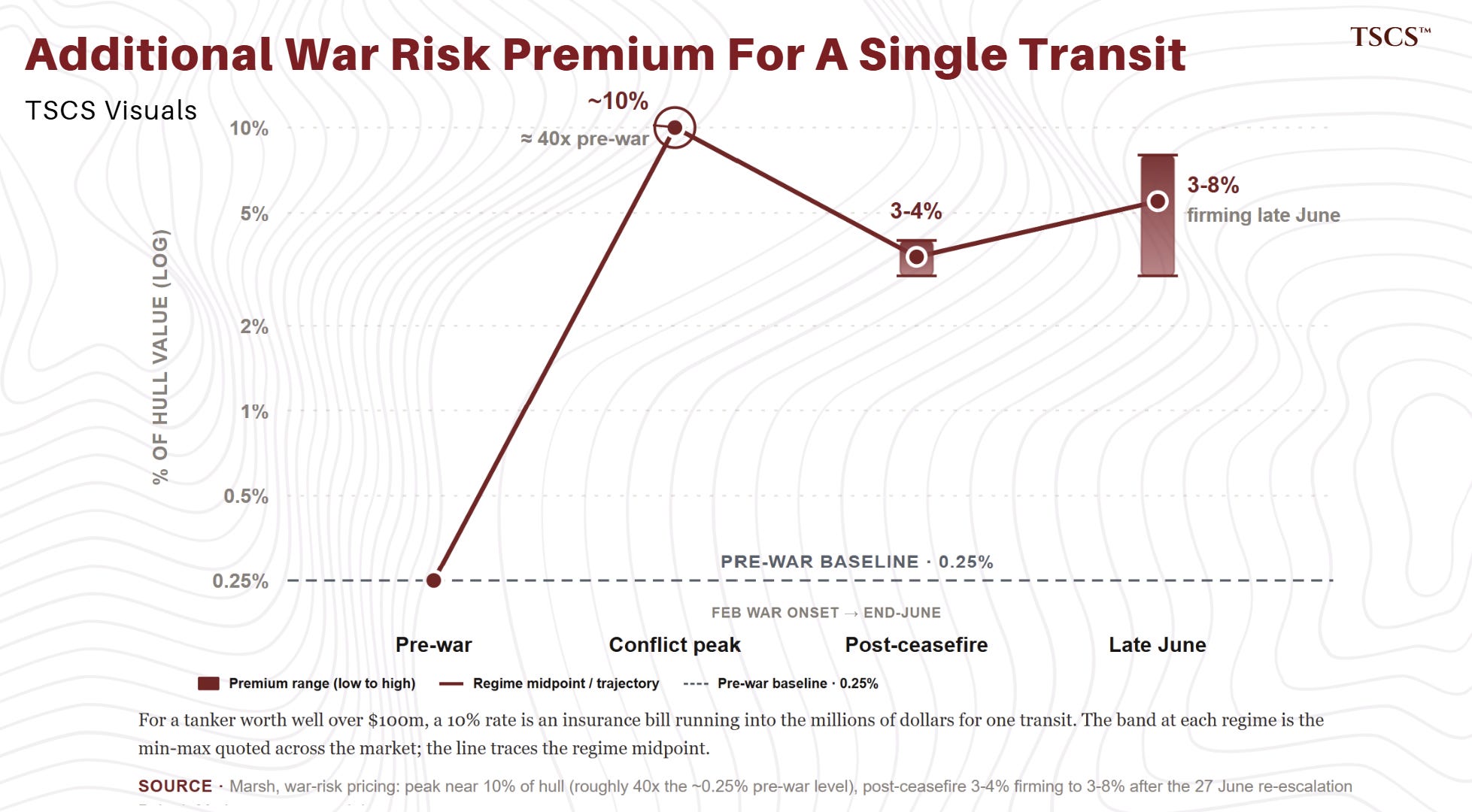

Before the war, the additional war-risk premium for a Hormuz transit sat at around 0.25% of a ship’s hull value. At the peak, Marsh’s UK war leader put it as high as 10%, a rise of close to 4,000%. For a large tanker worth well over $100m, that’s an insurance bill running into the millions of dollars for a single transit.

Even after the June ceasefire the number didn’t normalise: Marsh’s global head of marine put the post-ceasefire rate at 3-4% of hull value, and as the ceasefire buckled into early July the range quoted across the market moved back up to 3-8%.

The firms positioned to write that repriced layer are the specialist Lloyd’s and London-market underwriters with dedicated marine-war, cargo-war and political-violence books.

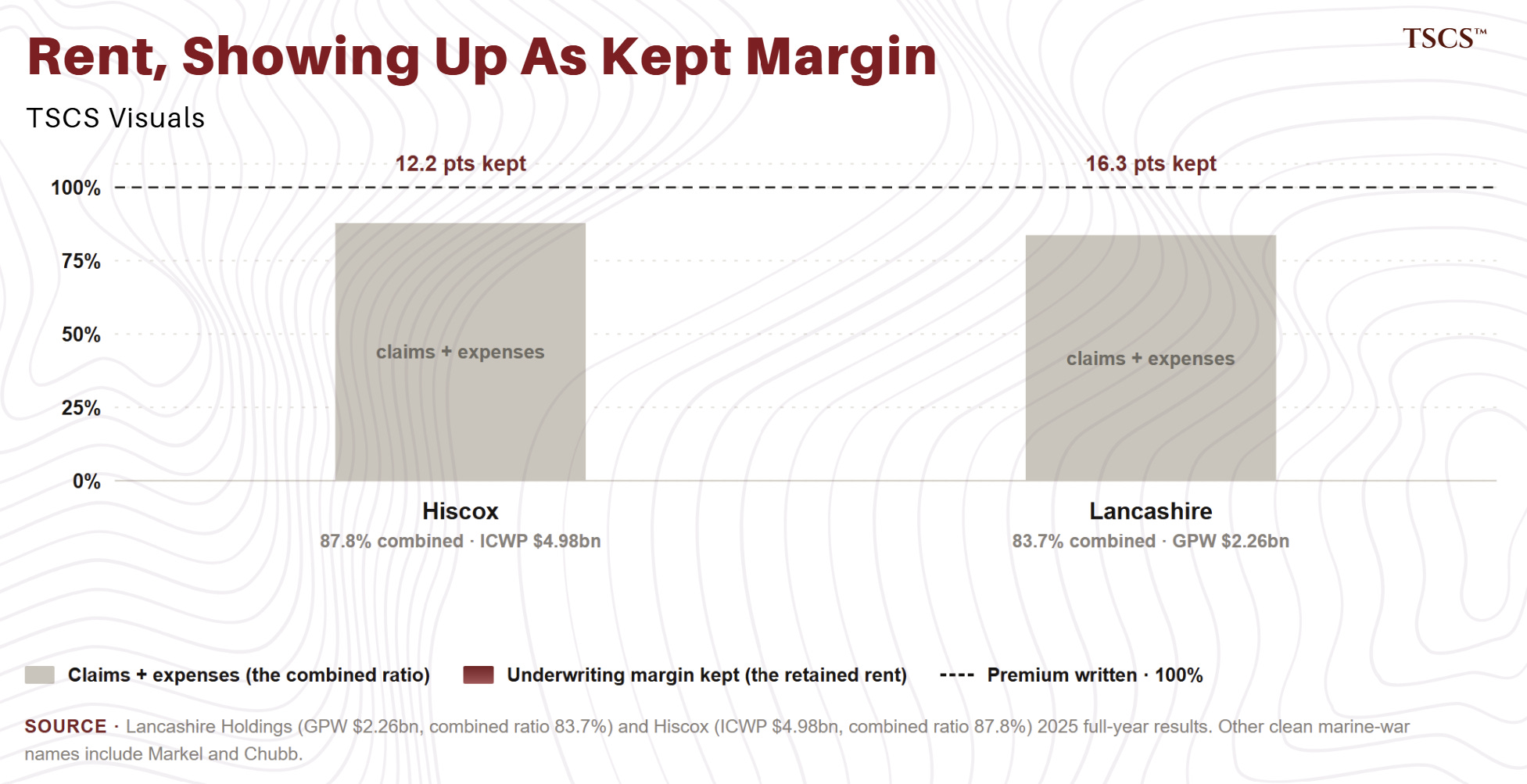

These are not household names, but their 2025 results show what a well-priced specialist book looks like going into a repricing.

Lancashire Holdings, whose product set explicitly includes marine hull, marine war and cargo war, wrote $2.26bn of gross premium in 2025 at an 83.7% combined ratio, and told its own regulator that marine hull and war lines were still benefiting from geopolitical risk supporting pricing even as the broader market softened.

Hiscox, another London-market specialist, wrote $4.98bn at an 87.8% combined ratio, its best in a decade, and said explicitly that geopolitical uncertainty was driving demand in its marine, energy and specialty lines.

On the US side, Chubb was named lead underwriter of a new Lloyd’s consortium for Hormuz transits in June, offering up to $200m of hull-and-liability capacity and another $200m for cargo, and Markel writes marine war through its London platform with published war capacity in the 100s of millions.

A note on an ‘obvious’ not so obvious beneficiary: Beazley, the clearest specialist beneficiary on paper, having announced a $1bn marine-war consortium in April, agreed in March to an all-cash takeover by Zurich; its shareholders approved the deal in April and it’s expected to close in H2 this year.

That means the war-risk upside now accrues to the acquirer, not to Beazley’s equity, and the shares trade as a deal spread rather than as an expression of the marine-war thesis.

It’s a useful reminder that “the sector that captured the rent” and “a clean way to own it” are not the same thing.

But there’s still something the market can missy. The broad marine and specialty market is soft, with abundant capacity pushing ordinary rates down, and the headline pricing indices show it.

The specialist carriers are redirecting capital into exactly the repriced layer, through consortia and through sidecars, the third-party-capital vehicles that let an underwriter write more of a good risk without putting all of its own balance sheet behind it.

Hiscox launched a sidecar in its marine, energy and specialty lines to add capacity and earn fee income while managing its net exposure. Beazley built its consortium. Chubb and Lloyd’s built theirs.

These are capital-allocation decisions, and they can create a lagged uplift in earnings and franchise position that doesn’t show up in a headline rate index while the broader market looks soft. The repriced rent is partly hidden, because listed carriers report marine, specialty and London-market bundles rather than a standalone war-risk line.

You have to know where to look.

Unfortunately, the reporting bundling that hides the rent also makes it hard to size: you can see the exposure and the strategic direction clearly, but the exact war-risk profit is an inference. Second, the durability of this rests on the same fact we rest on.

War-risk cover is priced in short, seven-day windows that reprice fast in both directions. It’s sticky on the way down only while the danger persists. The moment the strait durably calms, those short-dated rates can fall as quickly as they rose.

So the insurers holding the migrated cost are, in the end, holding a bet on non-resolution, the same bet the flat price refused to make and the underwriters made instead.

As of the end of June, with the ceasefire broken and rates firming again, that bet was still paying.

Insurance is one market, and one market can be a quirk. A completely different instrument, watched by different desks, says the same thing.

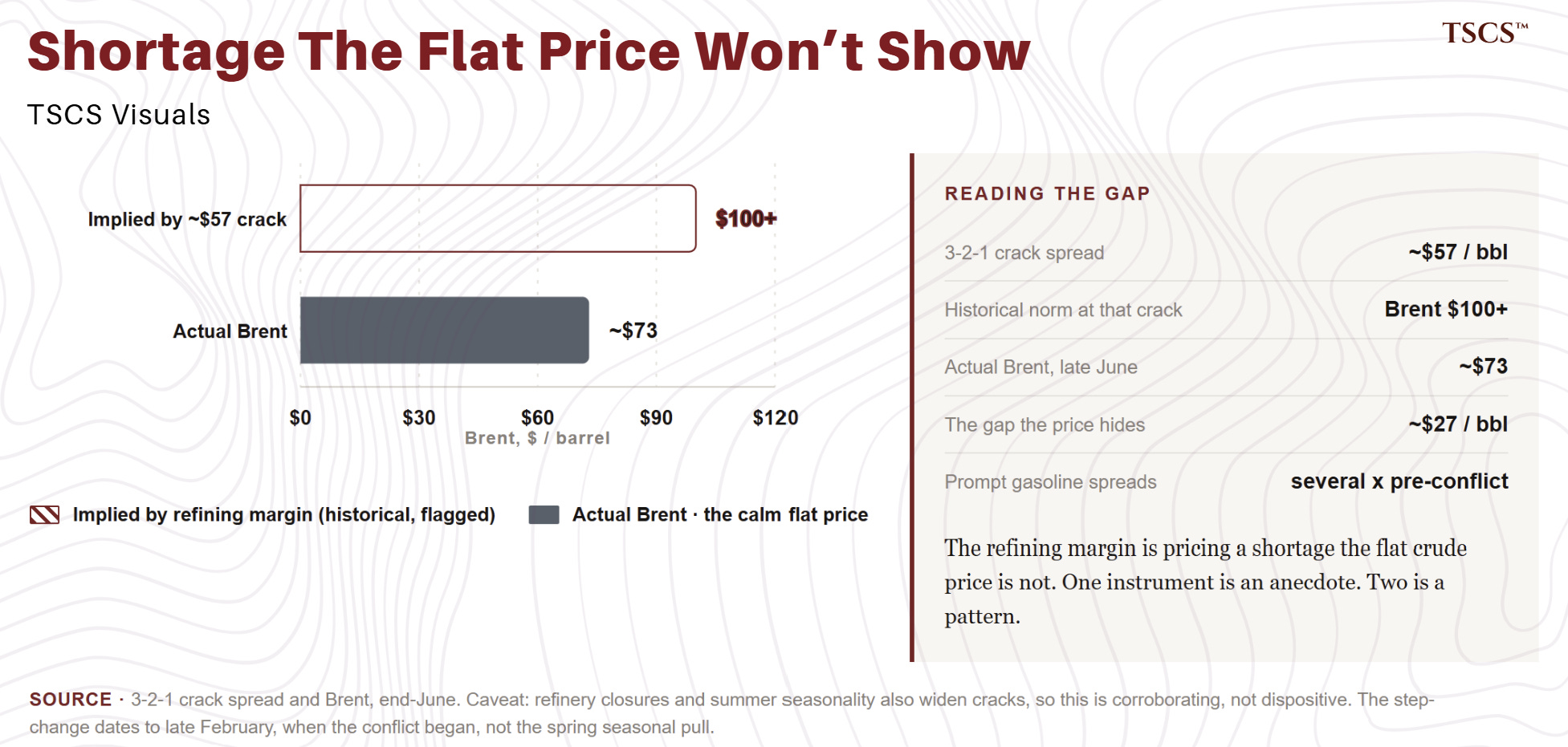

The 3-2-1 crack spread, the refiner’s rough margin on three barrels of crude, was still printing near $57 a barrel in the first days of July, about $172 across the three-barrel spread. A crack that high has historically gone with Brent above $100.

The margin to refine a barrel is behaving as though the world is short of product while the crude price behaves as though nothing is wrong, which is the same shape as the insurance layer in a different market. The prompt gasoline spreads agree, running several times their pre-conflict level, with gasoline holding on the last crude pullback.

Unlike the insurance premium this margin is competitive and will mean-revert, so it’s not sticky per se. If the calm now scheduled outlasts its week, this margin should be among the first things to fade.

Three Ships

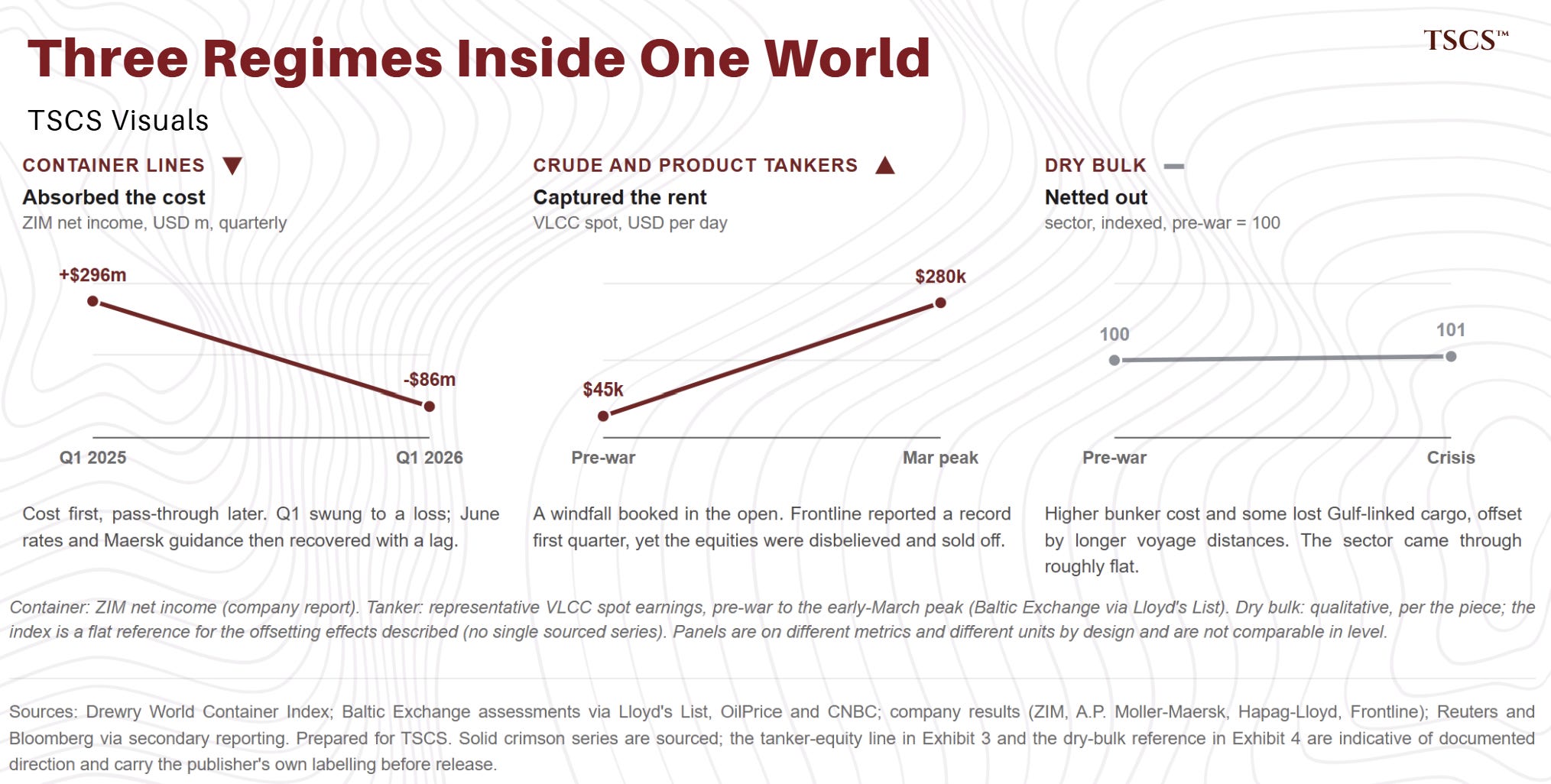

Oman is trying to build a way around the chokepoint. The ships that still have to pass through it, or reroute around it, are where the same cost shows up in a different form, and looking at them corrects a mistake the market tends to make. It treats shipping as one trade. In this crisis it was at least three.

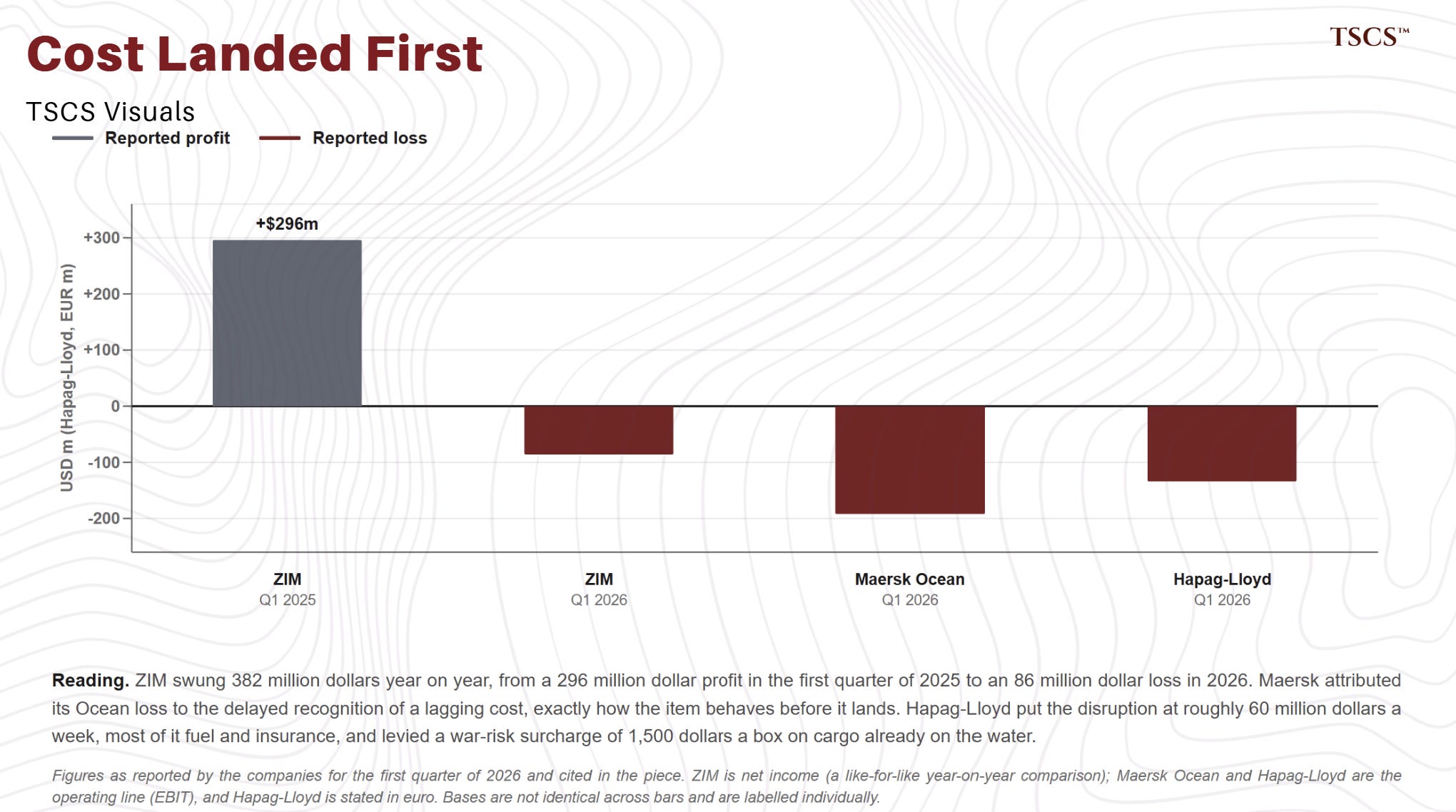

Container lines: ZIM, which runs a Gulf-serving network, reported a net loss of $86m for the first quarter against a $296m profit a year earlier, and its chief executive said that the conflict had caused a sharp increase in fuel costs, that the impact on the first quarter was minimal, but that the company expected a more meaningful effect in the second quarter, before higher freight rates and surcharges could, in his words, begin to take hold.

Hapag-Lloyd, over the same quarter, swung to a group operating loss of around €134m, said the Middle East conflict had forced reroutings and longer transits that raised its costs, and by its own account was losing something like $60m a week on the disruption, most of it fuel and insurance. It imposed a war-risk surcharge of $1,500 a box, and later stacked further emergency charges on cargo that was already on the water.

Maersk’s ocean division lost $192m at the operating line, a negative margin, and management attributed the limited first-quarter hit to timing, to the delayed recognition of costs, which is precisely how a lagging cost item behaves before it lands.

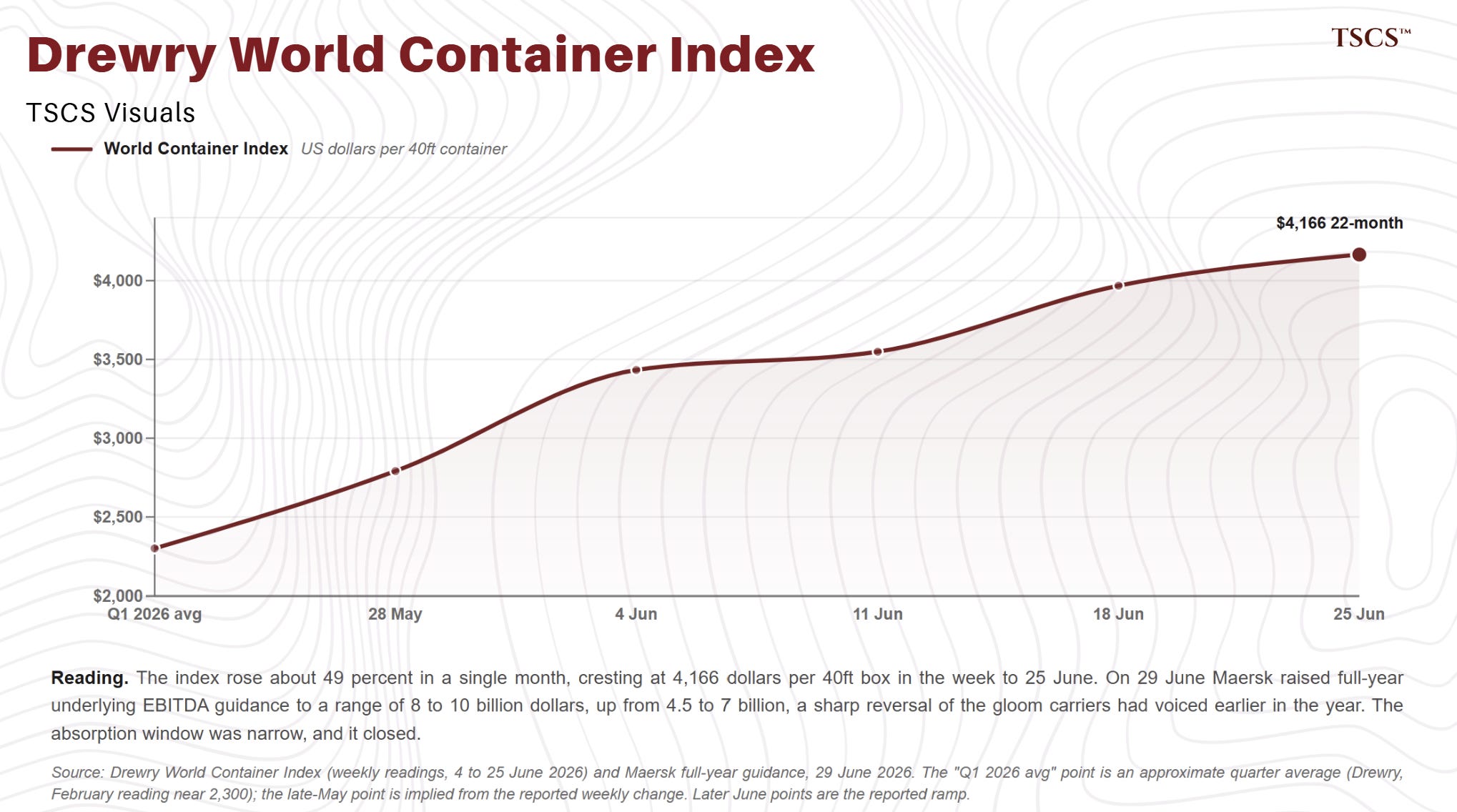

By late June, container freight rates had climbed to their highest since the autumn of 2024, the carriers were still making their surcharges stick, and Maersk raised its full-year guidance sharply, citing an extended stretch of disruption that had kept rates elevated.

So the container lines are a straightforward demonstration of the sequence: the cost absorbed first, visible in a compressed quarter, and the recovery arriving with a lag, exactly as the man from ZIM said it would.

The window where the absorption is visible is narrow, and closing.

Tankers are the opposite case.

Where the container lines ate the cost and waited for the pass-through, the crude and product tanker owners captured a windfall in plain sight. With tonnage removed from effective supply and voyages lengthened by rerouting, spot earnings for the largest crude carriers ran into six figures a day and the owners booked it straight to profit and guided the next quarter higher still.

There was nothing hidden about it. It was reported, and then it was guided.

Those tanker equities didn’t rise on the windfall. Many of them sold off. The market looked at record daily rates and decided they would not last, that the strait would calm and the tightness would drain away, and it priced the reversion rather than the spike.

Again, both hold only while the danger holds. If the strait durably reopens, the war-risk premium falls and the tanker tightness drains and both trades unwind together. If it doesn’t, both persist. The market has sold both on the assumption that resolution is coming.

The whole argument of this is that resolution kept being announced and kept not arriving.

Dry bulk sat in the middle, and completes the correction to the one-trade view. The bulk carriers felt the higher fuel cost and lost some Gulf-linked cargo, fertiliser in particular, but the hit was offset by longer voyage distances and stronger flows elsewhere, so the sector came through roughly flat rather than clearly up or down.

Three regimes, then, inside a single word. A reader who buys or sells shipping as one thing is averaging across three contradictory realities.

The point in this research is narrower and, we think, more durable than any single position.

You can watch the cost land, quarter by quarter, in the accounts of the firms that carry the world’s cargo.

Oman - Turning Position Into Throughput

Oman is where this story is most often told in the shorthand of a windfall, so it’s worth being precise about what the crisis revealed and what Oman is doing with it.

The familiar version, heard in Muscat, is that the crisis was Oman’s moment: sitting at the mouth of the strait, outside the chokepoint, it would absorb the ships that would not enter the Gulf, the trans-shipment business would migrate south, and a decade of deep-water investment would finally pay out.

The evidence points to a more useful frame, one of position and readiness rather than a one-off windfall, and it’s the frame Oman itself is now operating on.

Start with what the disruption tested. It tested the land-side machinery that turns geography into throughput: trucking capacity, customs flow, border coordination, competitive landed cost, and it highlighted the importance of continuing investment in the logistics systems that convert geographic position into sustained throughput.

In the immediate weeks, the volume that diverted moved fastest to where that machinery was already most built-out. That’s a map of the infrastructure agenda that converts position into cargo, and it’s where national effort is now concentrated.

The second point sharpens the first. The cargo that diverted was never going to stay. Trans-shipment routing naturally follows cost, and the moment the strait reopened the efficiency logic began pulling the diverted boxes back to their old paths.

Whatever any bypass port captured in the worst weeks was, again, temporary. A strategy built on rerouted volume lasts only as long as the danger does; which is why Oman’s own approach is not built on it.

The prize lies elsewhere.

A disruption like creates a moment in which every shipper, trader and underwriter who watched Hormuz become impassable is actively re-pricing their dependence on.

The window is open now.

It closes as the strait normalises and the memory fades. The lasting gains from any chokepoint crisis go to whoever institutionalises inside that window.

This is where Oman is moving. Its comprehensive economic agreement with India, in force since the first of June, is what this window rewards: duty-free access across almost the entire tariff schedule, which gives a buyer a standing, cost-based reason to keep sourcing through Oman long after this is over.

This agreement has been in process for a while but its timing could hardly be better, and its structure helps convert this into lasting advantage: a durable change to the economics of trade, formalised while counterparties are most motivated to diversify. India’s crude purchases from Oman rising from a low base is an early signal of the same logic.

The point, then, is not whether Oman was handed a windfall. It’s that Oman is treating the disruption as it should be treated, as a window to lock in permanent advantage while the infrastructure that turns position into throughput is actively built out.

That’s the mechanism most consistent with the approach Oman is already pursuing, and the moment is still doing the selling, and the encouraging part is that Oman is already running it.

On the operational side, the country isn’t stationary. The work is real. The Ministry’s Naql platform has processed more than 429,000 electronic land-transport transactions. A port community system piloted at Sohar cut a ship’s stay from 48 to 24 hours, and goods clearance from over 5 to 2 hours, the kind of operational gain that, scaled across the network, catches the value. A blockchain-based transport-document pilot ran across nearly 110,000 trucks. The Sohar-to-Al Buraimi road, the artery to the border crossings, is getting 5 new bridges by the end of 2026. A freight-rail agreement with Hafeet Rail is structured around seven container trains a week and nearly 200,000 TEU of annual capacity once the network is built. And as recently as late June, Asyad and CMA CGM signed a framework agreement for a new $400 million logistics terminal at Sohar.

No single one of these is transformational on its own. Together, they are the signature of a country deliberately building the very machinery that turns position into throughput.

The forward asset is the energy-transition build at Duqm.

ACME’s green-ammonia development at Duqm, with land agreements inside the national hydrogen framework, a first phase already underway with offtake support from Yara, and a commitment on the order of $4 billion around its later phases. Alongside it sits HYPORT Duqm, a serious consortium with bp as operator, advancing toward a final investment decision within the 2026-to-2027 window that Oman’s own energy ministry has set for its hydrogen programme. Beyond those two is a deeper pipeline, bp, Shell, a Posco-Engie consortium, still at the memorandum stage.

Taken together, we see national framework built to convert intent into investment.

That progression points to where the durable value accrues as Oman executes.

The lasting winners from a crisis like this were never the ports that briefly caught the diversion. They are the builders of what comes after the boxes move: the inland links, the terminals, the energy-transition capacity, the infrastructure of a Gulf that has decided it can no longer depend on a single strait.

On the evidence of what it’s already putting in the ground, Oman is positioning itself among the builders.

How that translates into specific opportunities is a question for another day; the point here is that the country is doing deliberate work that turns a moment into a durable advantage.

Window of Opportunity

The opportunity is real, but it’s time-limited, and the value goes to whoever institutionalises fastest while the moment still concentrates minds.

That places a premium on one capability above all others: execution speed, the ability to turn strategy and infrastructure into coordinated operational response at the pace a crisis demands.

The regional benchmark for that capability is now well established.

When the disruption hit, customs authorities across the Gulf stood up fast-track green corridors, sealed trucks under full customs supervision, pre-arrival cargo data, advanced inspection, extended transit periods, direct overland routing.

Where these were operationalised at speed, the throughput response was dramatic: declarations and cargo value moving through the fast-track lanes rose by multiples within a single month.

That’s what closing the coordination gap looks like when a state treats it as an operating problem. This is a repeatable, well-documented playbook, now available to every port economy in the region, Oman included.

Oman has the institutional architecture to do this. There’s a ministerial committee for the logistics system and border crossings, an executive committee beneath it, an implementation arm in the Oman Logistics Center, active dealmaking platforms, and a growing body of operational agreements.

The strategic intent and the coordinating bodies are in place.

The ongoing focus is on continuing to strengthen coordination and implementation across the logistics ecosystem.

Oman is pursuing a diversification of its trade and logistics base while simultaneously funding the very infrastructure that diversification requires, a demanding sequence for any state, and one that rewards focus and pace over breadth. The countries that convert a chokepoint crisis into lasting advantage are those that pick the highest-leverage moves and execute them before the window narrows.

So the evidence suggests a useful way of interpreting Oman’s position. The crisis opened a real and time-limited window, and it handed Oman a precise, well-priced diagnosis of which capability to prioritise: operational coordination speed.

Oman has responded on the parts that build durable advantage, real platforms, real infrastructure, and at least one bankable project at Duqm, and the strategic direction is set.

The next phase is the continued implementation of the programmes already underway.

That is an achievable, well-defined objective. Decision maker in Oman reading this can execute: experience from previous disruptions suggests that the jurisdictions able to implement efficiently are the ones best positioned to capture the long-term benefits. The position is genuine. The method is proven. Converting the first into a result is now, principally, a question of execution tempo, and that is the most closable gap of all.

Oman is one instance of something the whole Gulf is doing. Look at where the region is still putting money. The UAE has been driving a second oil pipeline east to Fujairah, on the Gulf of Oman side of the strait, to lift the volume it can export without passing through Hormuz at all. Saudi Aramco ran its East-West pipeline, the overland route from the eastern oilfields to the Red Sea, up to its full capacity through the first quarter. Oman and the UAE pushed on with the Hafeet rail corridor, an overland link between their networks.

And on 29 June, days after the ceasefire, Oman’s Asyad and the shipping line CMA CGM signed a framework agreement to develop a $400 million logistics terminal at Sohar, the port that, in the words of the reporting, had become the alternative route for Gulf trade during the war. CMA CGM’s own chief executive described the point of it as reliable inland access and greater resilience for supply chains.

We’ll be careful not to claim the crisis built all of this, because it did not. Most of this infrastructure is years old in conception.

The Gulf has been trying to reduce its dependence on the strait for a decade, for reasons that include the Red Sea, the general fragility of a single chokepoint, and plain diversification, and it would have been building a good deal of it regardless of what happened in February.

The signal is that none of it slowed when the oil price went back to pre-crisis levels, that fresh money kept going in.

You don’t sign a new agreement to build a bypass terminal, on the 29th of June, if you believe the strait will be reliable indefinetly. The people committing this capital have the most direct exposure to Hormuz and the best information about it, and they are voting, with their balance sheets, that the risk is chronic.

That’s the same conclusion the war-risk underwriter reached and the refining margin reached, arrived at from a third direction by the people who would have to live with a reopening that failed. The people building around the strait are putting money regardless.

The Absorption Race

There’s one question left, and it’s the one that decides whether any of this reached beyond the people who write insurance for a living. The cost migrated, it stuck, and it went to the underwriters rather than the ports.

But somebody is paying it. Who, and what happens to them?

One conversation from within Gulf commodity trading gave us a way to frame it, and we’ll pass on the wisdom. In that business, a cost increase like this one cannot easily be passed down the chain, because the competition will not follow and the customer won’t want it.

So the supplier absorbs it, out of margin. Absorption, they said, has a limit. A few months is manageable. Somewhere past half a year it stops being a margin problem and becomes a question of whether the supplier is still there.

It’s fairly straightforward, sticky costs only stay invisible for as long as someone can afford to swallow it. That reframes the whole question as a race.

The administered premium is sticky, we have established that. Whether it ever transmits, into higher prices, into suppliers that fail, into something a credit market eventually feels, depends entirely on whether the disruption outlasts the capacity to absorb it.

If the danger runs longer than the absorbers can hold, the cost stops being swallowed and starts being passed on.

We are about 4 months in, and this is where the temporary version of the story falls apart.

The absorbers only stay ahead if relief arrives. Late June was the low: the recovery stalled at roughly 70% below pre-war transit, the traffic split into a coordinated northern corridor and an escorted southern one, the southern lane was suspended after a vessel was struck in it, and ships were hit on the 25th and again on the 27th.

The first days of July then brought a scheduled week of de-escalation, the first loaded LNG sailings of the war, and a resumption announcement from Qatar. That is good relief for traffic. It’s not yet relief for cost.

So we won’t write the verdict, because the data won’t let us.

The more likely outcome is still that this ends as a margin event, painful and survived, because 4 months is not yet 6 and the strongest balance sheets can carry the cost a while longer.

But the alternative scenario is still possible.

The absorbers live in that gap, and they are holding their breath.

Additionally, the burden didn’t fall evenly: who could afford to take it, and who couldn’t. A trading house with a global network and its own ships can carry a surcharge and wait out a war. A low-margin operation can’t, and there is at least anecdotal reason to think some did not.

Conversations from within the logistics chain described shippers of chrome and gypsum and other low-value bulk, cargo for which the war-risk surcharge was a large fraction of the entire freight bill, simply ceasing to move.

We can’t put a number on how many; that kind of exit leaves almost no trace, which is part of the point. The trade just stops, and it stops in places that don’t get covered.

So the answer is not in yet, and the honest thing is to say so and tell you where it will be written.

We will watch and follow up on the prices of the absorbed inputs over the next two quarters, and watch for the failures, the consolidations, the small operators who don’t come back.

If prices lift and marginal suppliers start going under before the danger recedes, the absorbers lost the race and the cost transmitted. If normalisation comes first, the balance sheets that swallowed it will have been righ, this fades into a footnote about the year insurance got expensive.

Which way it breaks is what we have yet to see.

What can be said now is what oil price could never tell you and a single invoice could.

The cost of a Gulf crisis does not vanish when the shooting stops, or pauses, or when the headlines lose interest.

A wonderful narrative but it’s a lot of words to say “I goofed on my oil call”.

Thank you for such detailed insights, helping to lift the fog of war