You Sold The Bottom

Everyone gave up on gold right before the meeting that decides it.

Gold fell ten percent over the past month and every wire blamed the war. Three days before Warsh’s first FOMC, Jim Grant went on Meb Faber and said the whole frame is backwards.

He’s right, and the selloff is the proof. I’m buying the most hated trade in the market into June 17.

If you were loud about gold at five thousand and you have gone quiet at four thousand two, this is for you. If you sold somewhere in the March panic, it is especially for you, because the thing that looks like the thesis dying is the thesis working, and I can show you exactly why.

My own money first, so you know I’m not narrating from a desk. Gold miners are about a fifth of my book and have been for most of a year.

I’ve been long the whole way down, I called the March bottom in Gold Is Not Failing, and I have put my misses next to my hits in public. So this isn’‘t a victory lap.

It’s the part where the one man who can make the bear case on gold better than any bear alive sat down on a podcast and made my argument for me, then handed me a second wall I had underweighted.

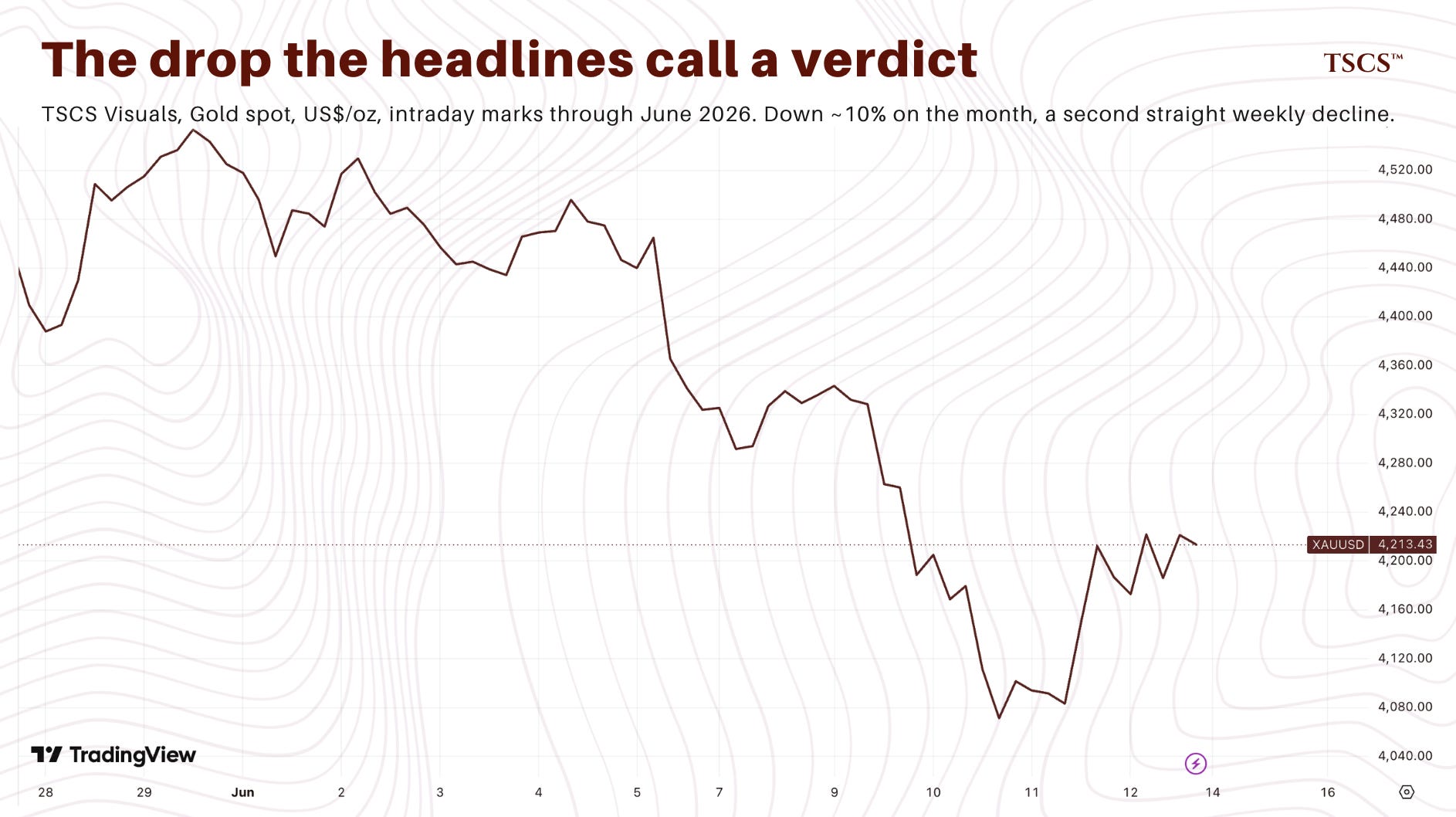

Gold sits around four thousand two hundred dollars, down 10% over the past month, a quarter below its January high, into a second straight weekly decline.

Open any wire and you get the same story. Iran. Hormuz. Energy feeding inflation. A new Fed chair with a hawk’s reputation. War is bad for gold, the screen says, because war means inflation, inflation means higher for longer, and higher for longer means you dump the metal that pays you nothing.

That reading is backwards, and the drop is how you know.

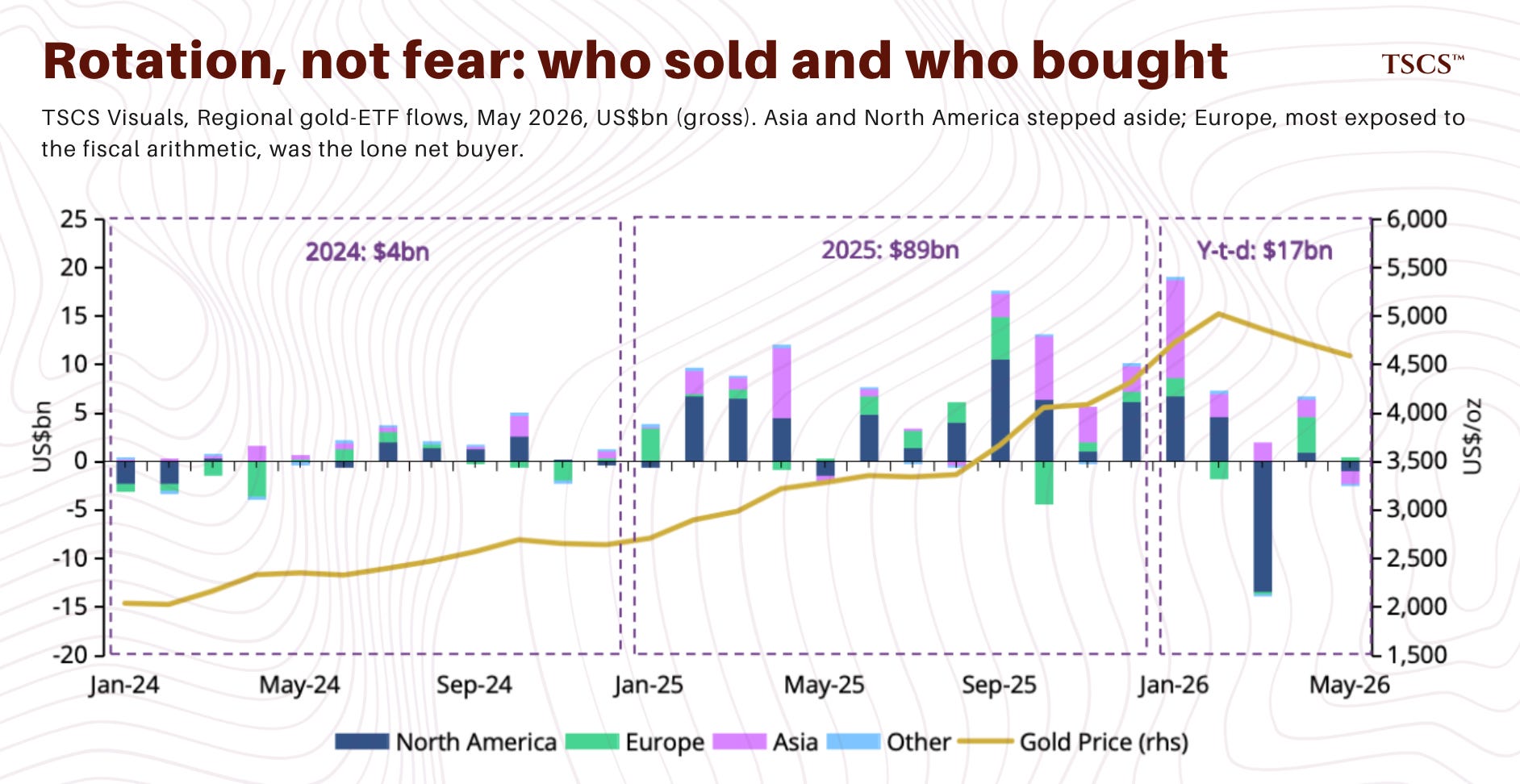

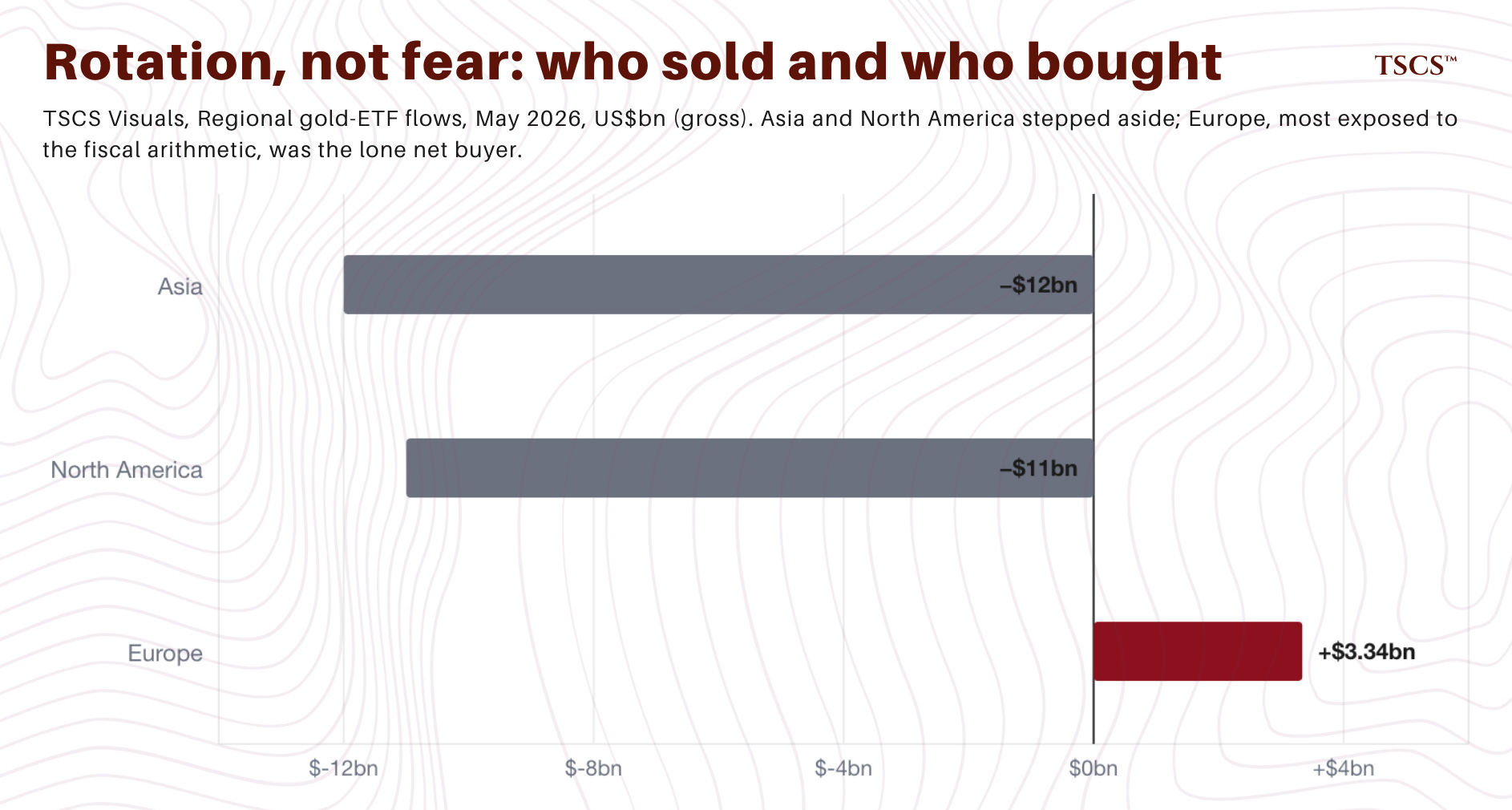

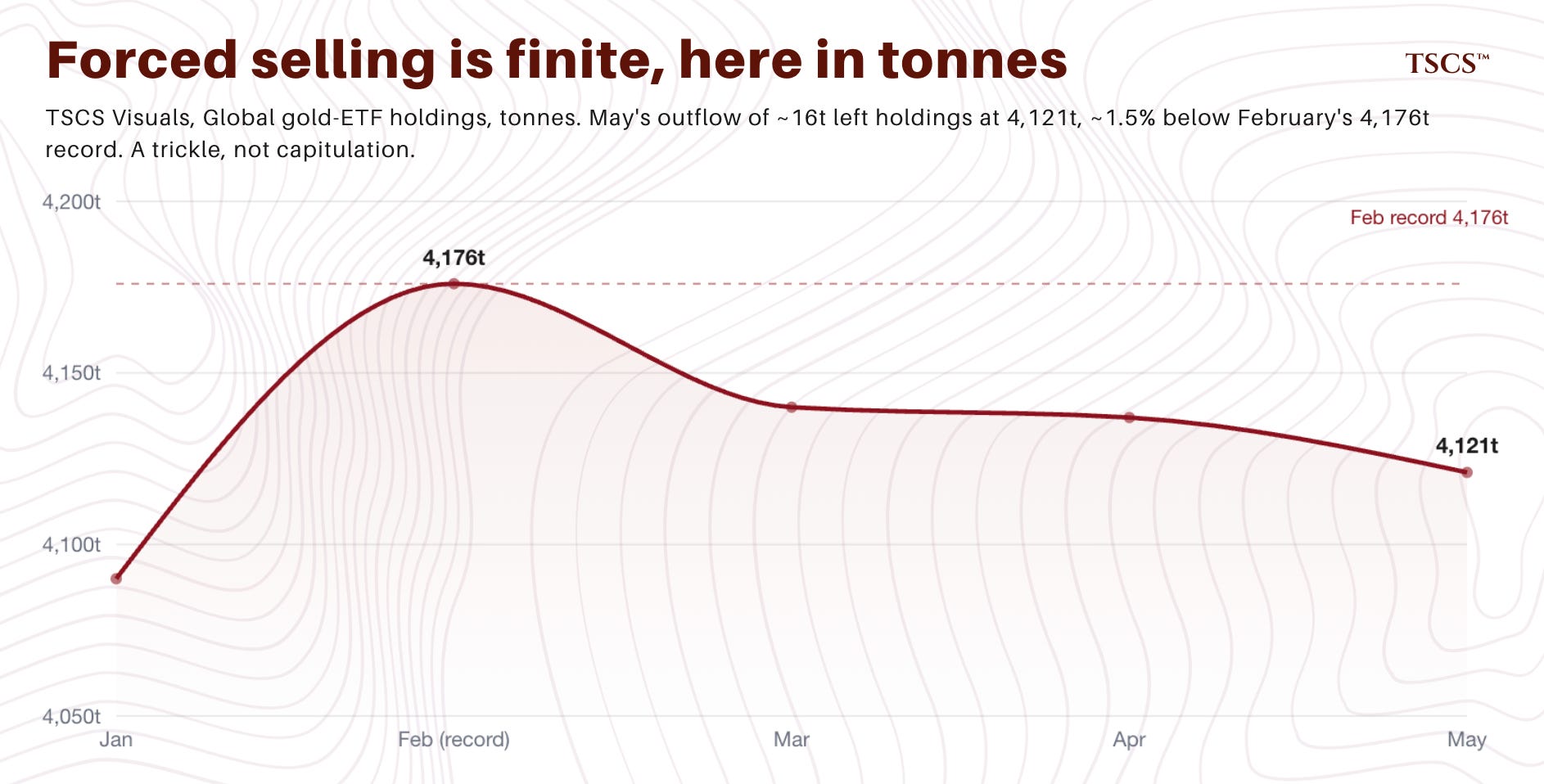

Nobody abandoned gold in May. The ETFs shed two billion dollars, sixteen tonnes, four tenths of one percent of what they hold, and total holdings stayed at 4,121 tonnes, within a percent and a half of February’s record, with flows for the year still positive at seventeen billion.

That is not capitulation. It is a crowd that rode the easiest macro trade of the first quarter, watched a firm dollar and a repriced Fed raise the cost of holding it, and rotated into technology to keep up with a benchmark.

Tech ETFs took their biggest inflow since early 2024. The sellers were North American profit takers stepping aside and Chinese holders selling a weaker local price into a stronger renminbi. Europe, the one balance sheet most exposed to the fiscal arithmetic this whole thesis rests on, bought. People rotated out of gold to chase a hotter trade.

That is not the same as giving up on it.

CHART: Global gold ETF flows by region and average gold price

The real forced selling, the violent kind, already happened, back in March, the dollar liquidity event I wrote about at the time.

By May it had dwindled to a trickle with holdings near a record. The capitulation everyone keeps bracing for is behind us.

That was the moment to buy, and we are past it.

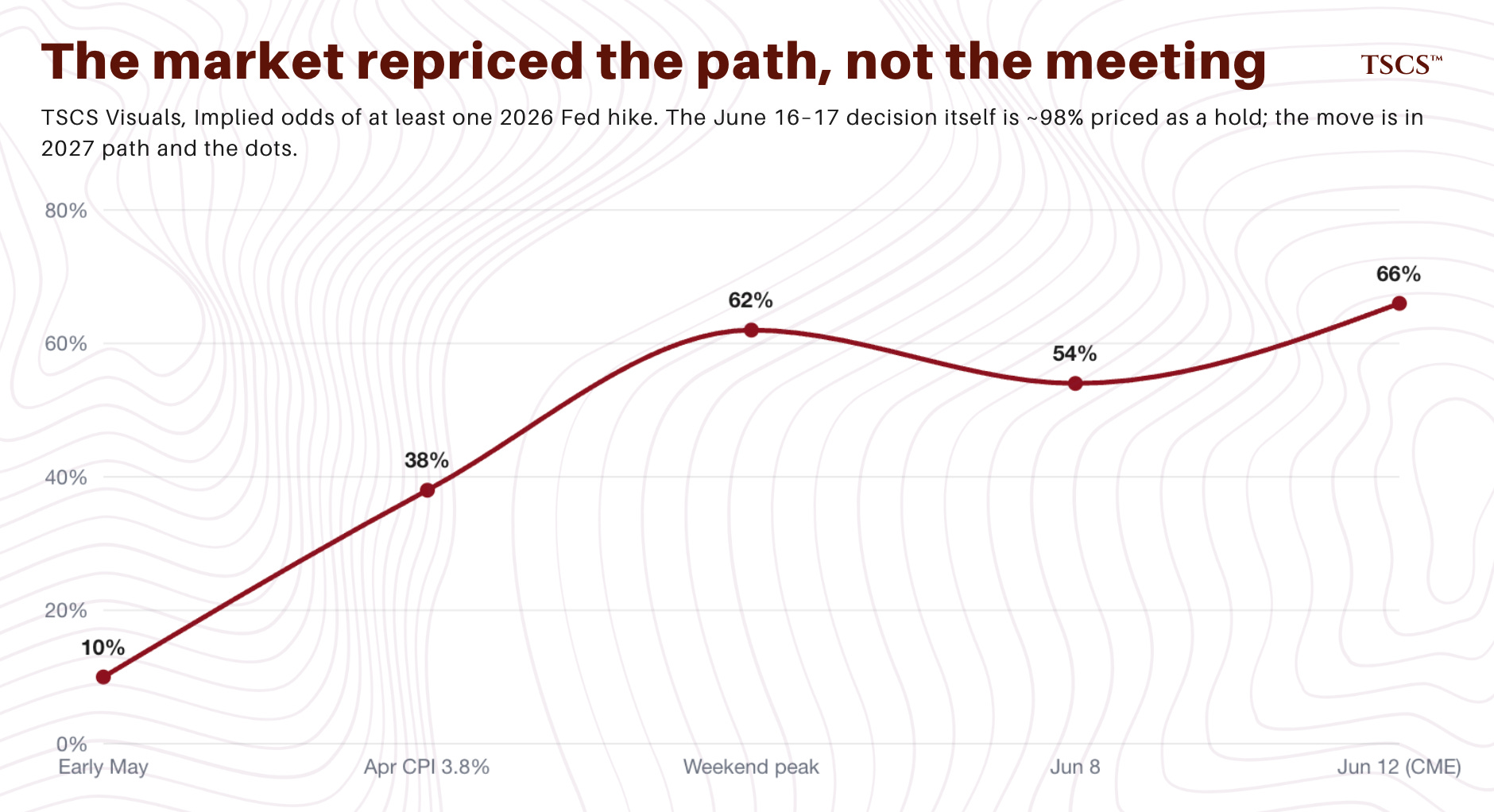

Look at what the market has priced into this meeting.

It has thrown out every rate cut it once expected for 2026 and now leans toward a hike by year end, on the hottest inflation in years and a chair who wants to look tough.

Under the old rules that is the worst backdrop gold can face, rising real rates with a Fed pushing them higher, and gold is just sitting in it, taking it. All of which is a problem only if the market is right that the Fed can deliver those hikes.

It cannot, and that is the entire trade.

Then I listened to Jim Grant.

Grant has put out Grant’s Interest Rate Observer since 1983 and owned gold for forty years, and the forty years matter more, because he is no gold bug.

He will tell you cheerfully that the bear case is close to airtight.

It pays you nothing, and Buffett and Munger were right that it just sits in the vault. He bought near the 1980 top at $850, watched it fall to around $500, and sat through the miners losing eighty and ninety percent from 2011 to 2016. He has been punished by this trade for longer than most of my readers have been alive, and he still holds it, because by his measure the dollar has lost about ninety nine percent of its value against gold, and that is not a forecast, it is arithmetic.

So when he looks at the same tape everyone is selling and says, flatly, that war is bullish for gold, the timing is worth your attention.

His point is not the war. It is the Fed.

Here is where he meets the argument I made in Gold Is Dead Money nine days ago, and extends it.

I laid out the trap in its public form. A government whose net interest bill has doubled toward a trillion dollars, with a third of its marketable debt to roll inside a year, cannot carry positive real rates for long without the interest line spiralling.

The exits from that are default or debasement, and both are bullish for the one asset that is nobody’s liability.

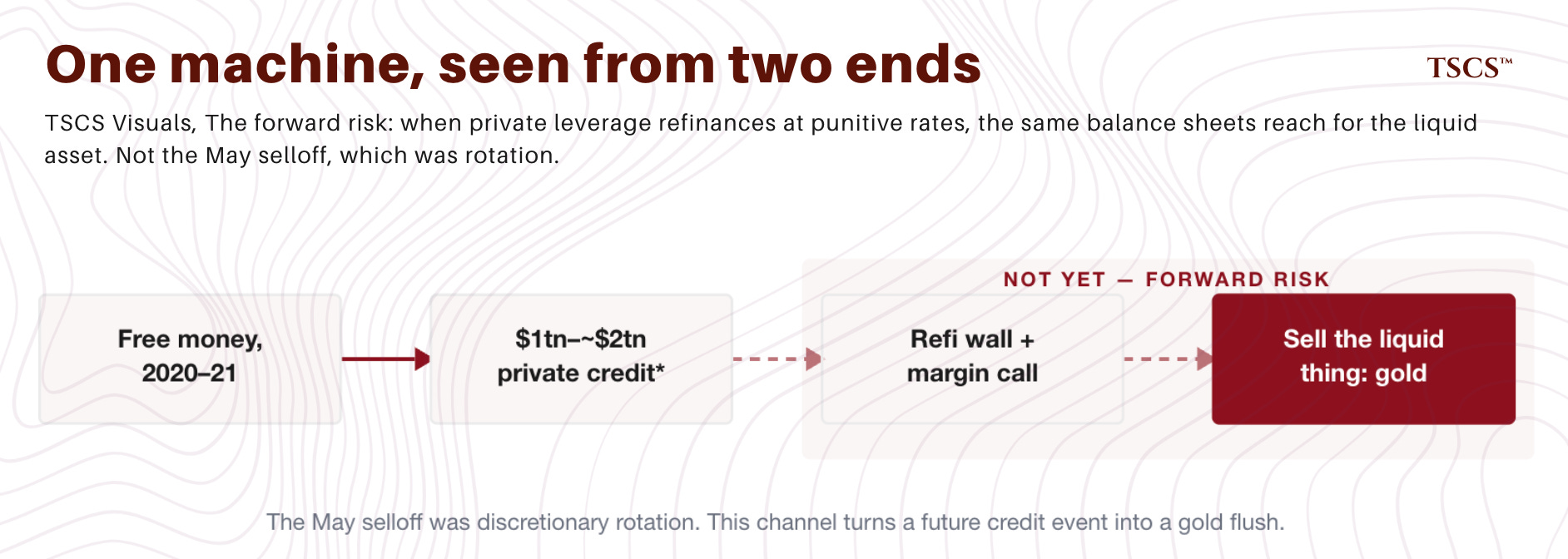

That is the sovereign wall, and it is the one that binds now. Grant arrives at the same trapped Fed from the private side, the side I had underweighted, though it binds later rather than this quarter.

The leverage that private equity and private credit took on at near zero in 2020 and 2021 has to be refinanced, and whenever it lands it lands at multiples of the rate it was struck at. A Fed that commits to higher for longer is not just holding rates, it is guaranteeing that wall refinances at punitive levels when it arrives.

So the box has two walls. The sovereign one is now, the private one is building, and a Fed staring at both cannot deliver a sustained hiking path, whatever the market is pricing this week, without breaking something.

And then Grant named a number I have been circling in the private credit work.

By the broadest measure, the one Moody’s uses, about a third of six trillion dollars of life insurance assets sits in private credit. The cleaner, narrower cuts are lower, closer to a trillion in private placements, and the all-in number lands somewhere in between depending on definition. The direction is not in doubt and the structure is real. A large and growing slice of insurer balance sheets, floating rate or close to it, sits under the Apollo and Athene model that minimises equity and maximises spread, the model in which Apollo originates and oversees essentially all of Athene’s assets.

That is the leverage I have been mapping in the private credit series, wearing the costume of a constraint on the Fed.

It is also, precisely, the redemption mechanism I described in Nobody Wants Gold.

When a margin call comes, you do not sell the illiquid thing that caused the problem, because you cannot.

You sell the liquid thing that has nothing to do with it, and in a forced unwind that liquid thing is gold.But be clear that this is not what drove the selloff in front of us.

The May flows show the sellers were discretionary generalists rotating into technology, not margin called balance sheets dumping bullion. This is the forward risk, the second wall.

When the private leverage refinances at punitive rates, the same balance sheets the Fed cannot afford to break are the ones that reach for the liquid asset, and that is the channel that turns a credit event into a gold flush.

Today it is a threat still loading, not the mechanism behind the tape. Two walls. One of them has not arrived yet.

You will object that the Fed already did this, that it took the funds rate above five percent in 2022 and 2023 and the system held. It did not entirely.

That cycle broke the British pension complex and three sizable American banks, Silicon Valley, Signature and First Republic. What it didn’t do was cascade, and the people who promised it would were wrong.

So why’s the constraint tighter now? Because the cushion that absorbed those hikes is thinner. The debt was cheap then and has since rolled into higher coupons, the interest bill has doubled toward a trillion, and the slice of leveraged credit that must refinance climbs every year into a wall that thickens through 2028 and 2029.

I won’t tell you the cushion is gone, because a third of federal debt still does not mature for five years and the average maturity sits near multi-decade highs.

I’ll tell you it is smaller, unevenly spread, and far thinner for the sovereign and for the weakest leveraged borrowers than it was in 2022. The Fed could raise into leverage once. The 2022 cycle is not the counterexample to the trap. It is the down payment on it.

Which is why the two reasons the screen gives you to sell gold are both the reason to own it.

One is the war, which is Grant’s target. The other is rising real rates, the naive version of which I have argued against since Gold Is Dead Money, because on a sovereign this insolvent, rising real rates are the buy signal and not the sell.

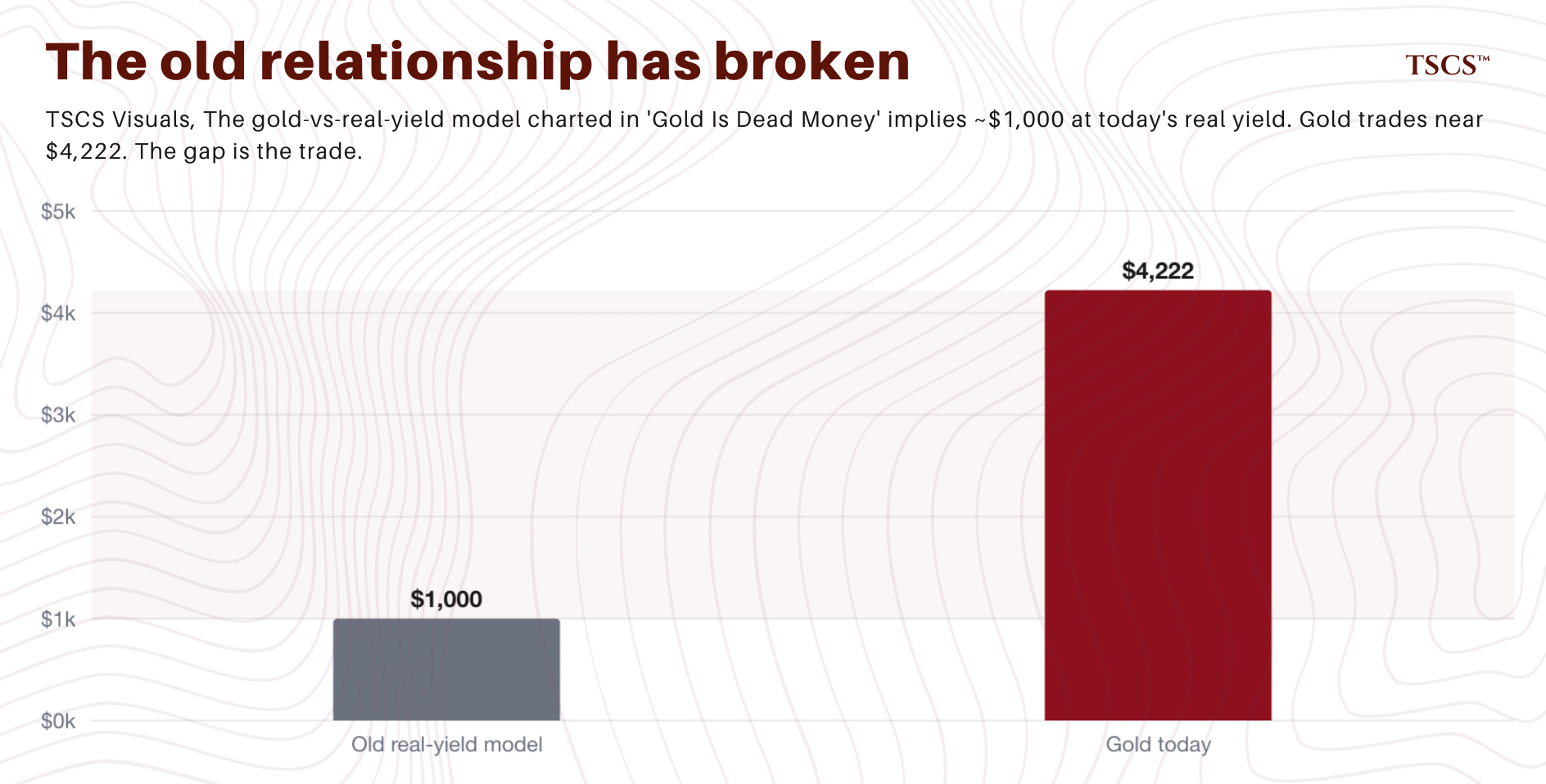

The relationship that used to govern the metal, gold against real yields, is broken. The model I charted in Gold Is Dead Money, gold against real yields, would put the metal near $1,000 on a real yield this high, and it is sitting around $4,200. That gap does not repair on a press conference.

If you want to know how badly a crowd can misjudge a rate setup, Grant gave the cleanest example I have ever heard.

In the spring of 1984 the thirty year Treasury briefly traded at fourteen percent while CPI ran around four. Ten points of real yield, in a government bond, the single most obvious one-decision trade of a lifetime, and almost nobody took it, because they were anchored on the brutal bond bear market that came before it and could not believe the regime had changed.

The most obvious bargain in hindsight was the most hated in real time. Gold at $4,200, forgotten, down on the month, sliding into a hawkish new chair, is that kind of hated right now.

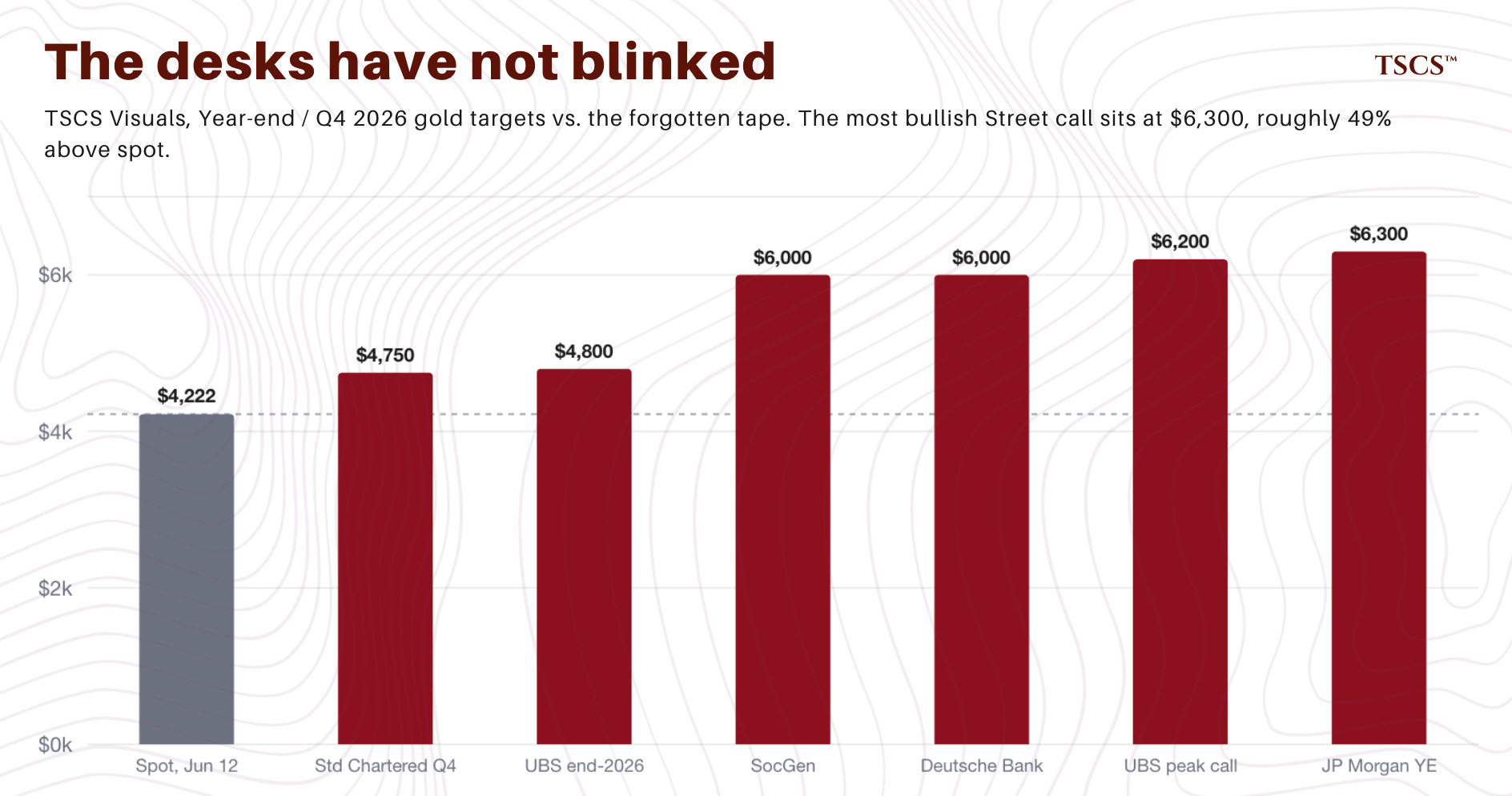

And note who has not blinked. The most bullish desks on the Street still carry targets well above the tape into year end, J.P. Morgan at six thousand by the fourth quarter, even as the metal sits abandoned at forty two hundred.

I’m not going to pretend this is a clean long, because it simply isn’t, and Grant would say so first.

Kevin Warsh chairs his first meeting on June 16 and 17. He is a genuine hawk with a sound money streak, the market is pricing a near certain hold at ninety seven percent, so the risk into the meeting is the tone and the dots, not the rate.

A hawkish Warsh and a dollar that keeps bidding could hand the complex the fifteen to twenty percent flush I’ve now made my base case in Nobody Wants Gold, the kind that takes a leg out and makes everyone who bought feel like an idiot for a few weeks.

Be precise about where it comes from, because the flows have already told you.

The gold specific selling is largely spent. Positioning is neutral and managed money stopped selling and added modestly in May, so there is no crowded long left to wash out.

A flush from here is not gold being abandoned, it is gold being sold as a funding source in a broader risk off, the same risk off that forces the sale is the only thing that revives safe haven demand and brings the buyers back.

It’s not the thesis breaking. It’s just improving entry, with the recovery built into the move that causes it.

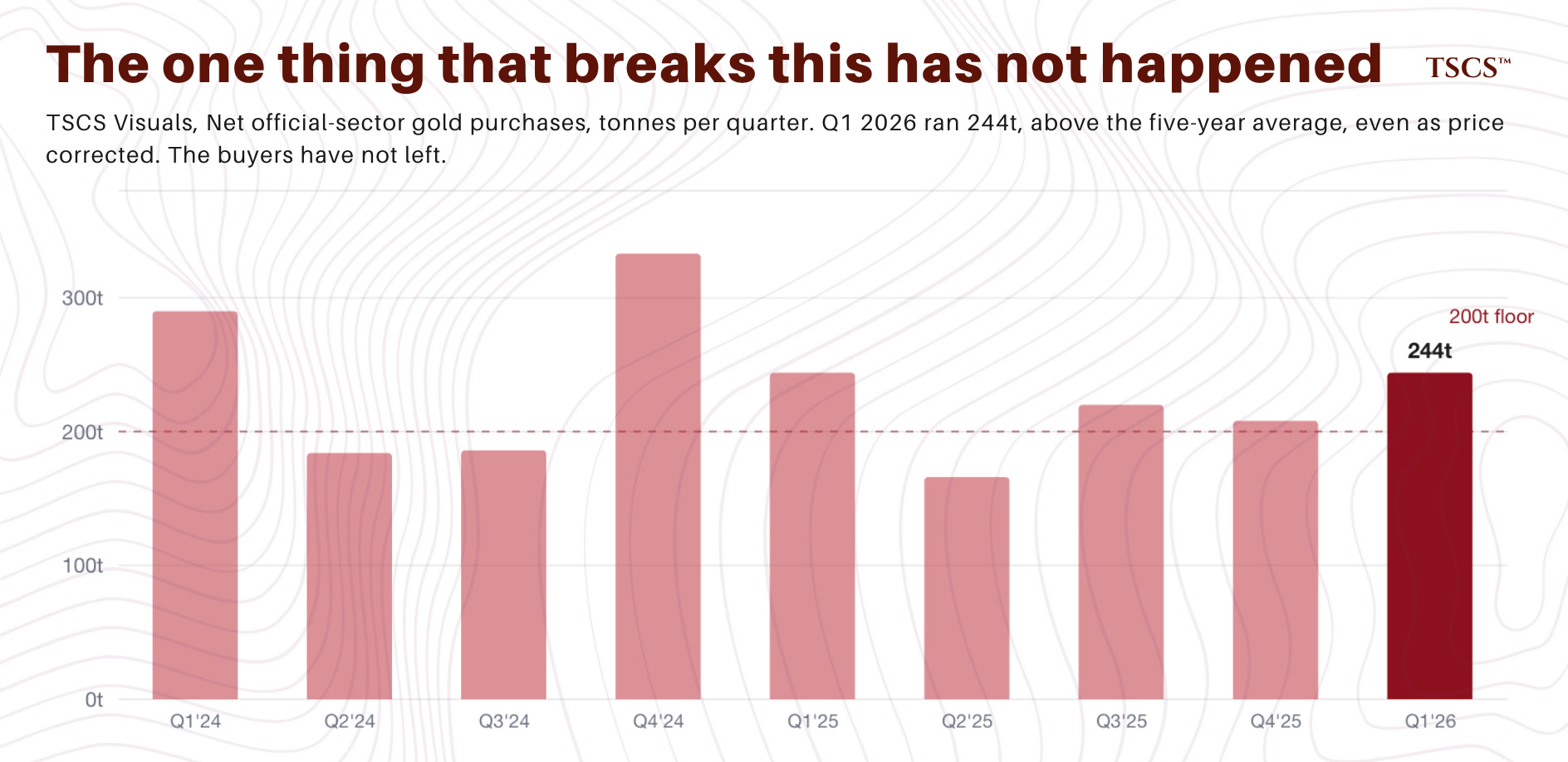

The one thing that actually breaks this is the official sector, the central banks doing most of the buying, stepping away for two straight quarters, and through the latest data they have not.

A press conference doesn’t do that. A new chair sounding tough doesn’t do that. Be honest about the path and you don’t get faked out of the position.

The backdrop under all of it is the truest sentence Grant said.

Inflation is not too much money chasing too few goods. It is just too much money.

Right now it’s showing up as AI capital expenditure, as farmland selling for three hundred thousand dollars an acre to a data center that does not care what the corn was worth, the greatest capital draw since the railroads, running on convictions Grant calls factually indefensible.

That money is being created and it’s going somewhere, and it’s not going into the forgotten metal the man who has owned it for forty years just told you to keep.

It is also the cleaner path to the same flush, the one I flagged in Nobody Wants Gold that needs no barrel of oil to move.

The largest IPO in history just happened. SpaceX priced this week and pulled seventy five billion dollars out of the market, close to three times the old record, with OpenAI and Anthropic both expected to follow above a trillion. Between them they could drain what the entire dot com class of 2000 did, with a handful of names instead of three hundred. That money comes out of something, and funds chasing the new paper sell what they can, which is gold. Oil flush, liquidity flush, same drain from two ends.

Markets can do anything, Grant likes to say, quoting Richard Russell, just as soon as you think you have it figured out.

So I won’t tell you gold cannot fall from here, because it can, and it might, into Warsh.

What I will tell you is that one of the most respected financial historians alive, a man who knows the bear case cold and has bled for this trade for forty years, sat down this week and said war is bullish and the Fed is trapped, in the days before the meeting the whole market is watching for the wrong reason.

I am adding to the miners. Not in spite of how it feels. Because of how it feels.

Everything you have just read is the why, and it is free, because the thesis always is.

The what is not. The five names I own, where each one sits today, the exact levels and the order in which I am putting my cash to work, and the kill switch on every one of them, are in Nobody Wants Gold, behind the wall:

If you intend to do anything before June 17, you want the names before the meeting, not the “I wish I checked” after it.

That’s the whole proposition. I’ve covered this basket since June 2025. I called the bottom in Gold Is Not Failing and the bond market pressure point in Cash, Not Bonds, both before the fact, and I’ve been wrong in public and said so because a framework that only gets talked about when it works is marketing and not research.

Probability-weighted calls, the misses printed next to the hits, the kill switches in writing, and the positioning behind the wall.

If this was useful, send it to someone who still thinks war is bearish for gold and that the miners are uninvestable. Both halves of that sentence are the point.

This is not investment advice.

This is a very insightful article that covers the essentials for understanding both the recent doldrums in the gold market and the longer-term case for owning the metal.

One point that may deserve more emphasis is that the latest drawdown in gold (and silver as well) can be traced, at least in part, to the stronger-than-expected U.S. employment report released on June 5. Better-than-expected job creation and an unemployment rate that held up more firmly than anticipated led markets to price in a stronger economic outlook and a potentially higher interest-rate path, reinforcing expectations of a more hawkish monetary stance.

I also agree with your argument that the simplistic notion that “war is bad for gold” is generally incorrect. However, the latest conflict in the Persian Gulf appears to be an important exception. While liquidity-driven selling undoubtedly played a major role ‒ as you correctly note, market stress forced marginal holders to liquidate gold alongside other assets ‒ the conflict also disrupted demand from some of gold’s most important buying regions. Major physical buyers in the Middle East and Asia, including India, China and Dubai, have been preoccupied with the energy crisis and trade disruptions that followed the outbreak of the war and intensified after the closure of the Strait of Hormuz. In that sense, the conflict may have weighed on gold through both forced selling and weakened physical demand. Therefore, as the war winds down, gold can catch that tremendous bid again.

Overall, an excellent piece that helps explain recent price action without losing sight of the fundamental reasons for investing in gold.

A sharply written essay. We will see these gold prices are cheap in hindsight, because the US debt load will continue to grow.

It’s a me issue, I don’t understand why life insurers having $2 trillion in private credit is an issue. Is it a maturity mismatch, borrow cheap at short term rates and lend to private equity long term at higher rates? Or is it because they own Treasuries, took out floating rate swaps, and used the proceeds to buy riskier private credit? I’ll figure it out.